A new IPO company's opening price on the US stock market, combined with the relentless trading activity of thirsty capital after the weekend break, led Hyperliquid to experience epic price discovery. The historic high of HYPE drew the attention of global traders to this 24/7 platform and a team called TradeXYZ.

Hyperliquid is a high-performance blockchain specifically designed for derivatives, featuring an order book that runs entirely on-chain. HIP-3 is its third improvement proposal: anyone who stakes about 500,000 HYPE as a deposit can launch their own perpetual contract market on this chain, trading US stocks, indices, commodities, and even companies without an IPO. Hyperliquid provides matching, margin, and on-chain settlement, and deployers define which trading pairs, which oracle to use, and how high the leverage can go.

TradeXYZ is the first trading platform deployed under the HIP-3 framework. By pricing the market over the weekend and trading IPO pre-contracts, TradeXYZ attracted the attention of Wall Street in less than a year of launching.

Besides TradeXYZ, several other HIP-3 trading platforms have been deployed, attempting to replicate HIP-3's success through their respective advantages.

However, the results have been less than satisfactory.

Recently, the Hyperliquid ecosystem project Felix announced that its HIP-3 trading platform would begin shutting down on June 19, with all markets being settled one by one.

Felix is the first HIP-3 trading platform to deploy silver and crude oil trading pairs on Hyperliquid, with OIL, GOLD, and SILVER bringing in considerable fees and approximately $3 billion in trading volume from December last year to January this year. Now, it has become the first officially exiting HIP-3 deployer.

Why did a once-leading player close its doors first?

「We are not TradeXYZ」

Felix founder 0xBroze reviewed this failed attempt.

First, the quoted assets were wrong. HIP-3 trading platforms must choose a stablecoin for perpetual contracts, and the earliest launch, TradeXYZ, opted for USDC. At the time, this was not a well-considered decision, as Hyperliquid had not yet initiated the stablecoin bidding, while Felix, launching later, chose USDH as a natural progression since using USDH could obtain fee discounts.

What they did not anticipate was that later Hyperliquid entered Growth Mode, significantly reducing trading fees, leaving USDH with little advantage, and instead turning it into "a burden of liquidity fragmentation." Users holding USDC needed to convert to USDH to use Felix, and market makers were reluctant to provide liquidity for USDH related markets. In hindsight, 0xBroze believes that USDH resembled a pawn Hyperliquid used to pressure Circle for revenue sharing.

Second, TradeXYZ was the first to arrive. It opened on the first day HIP-3 launched, about a month earlier than Felix. This month was not just a time difference; the early brand captured user mindset and had ample time to push the next batch of markets continuously.

Moreover, TradeXYZ had more trading pairs. As the only deployer using USDC, TradeXYZ quickly built a moat with the number of trading pairs. 0xBroze believes that there was probably an asset-liability sheet advantage behind it. TradeXYZ could afford the auction fees for Ticker and liquidity costs. Felix, with limited funds, had to choose trading pairs more cautiously.

Finally, there were "airdrop hints." Early users of TradeXYZ speculated they would airdrop tokens because the team behind TradeXYZ had previously auctioned and obtained the spot Ticker UNIT on Hyperliquid. The expectation of the airdrop elevated TradeXYZ's early user count, trading volume, open interest, and liquidity, forming a flywheel that Felix could never catch up to.

Summarized in one sentence: We failed because we are not TradeXYZ.

Matthew Effect

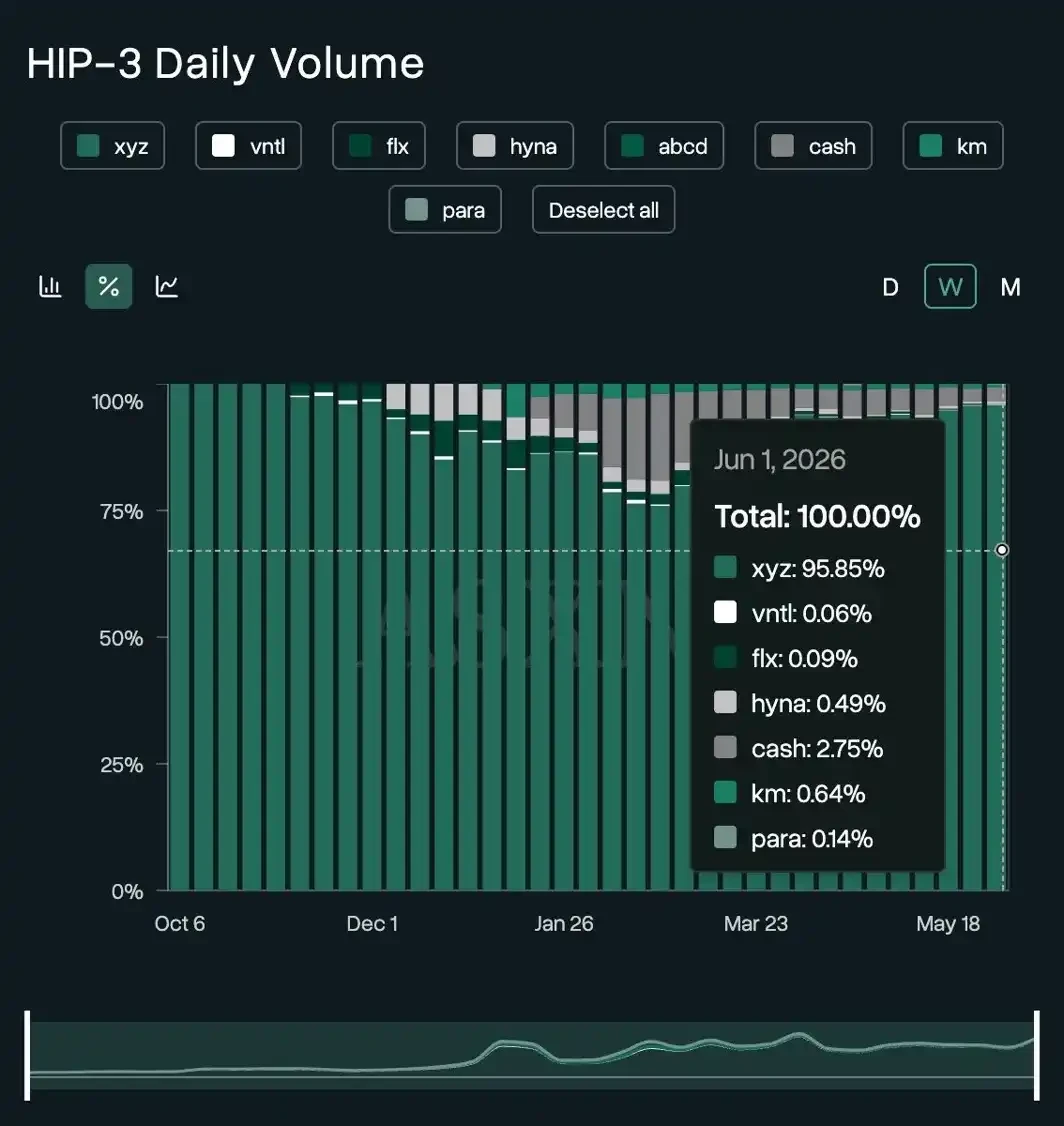

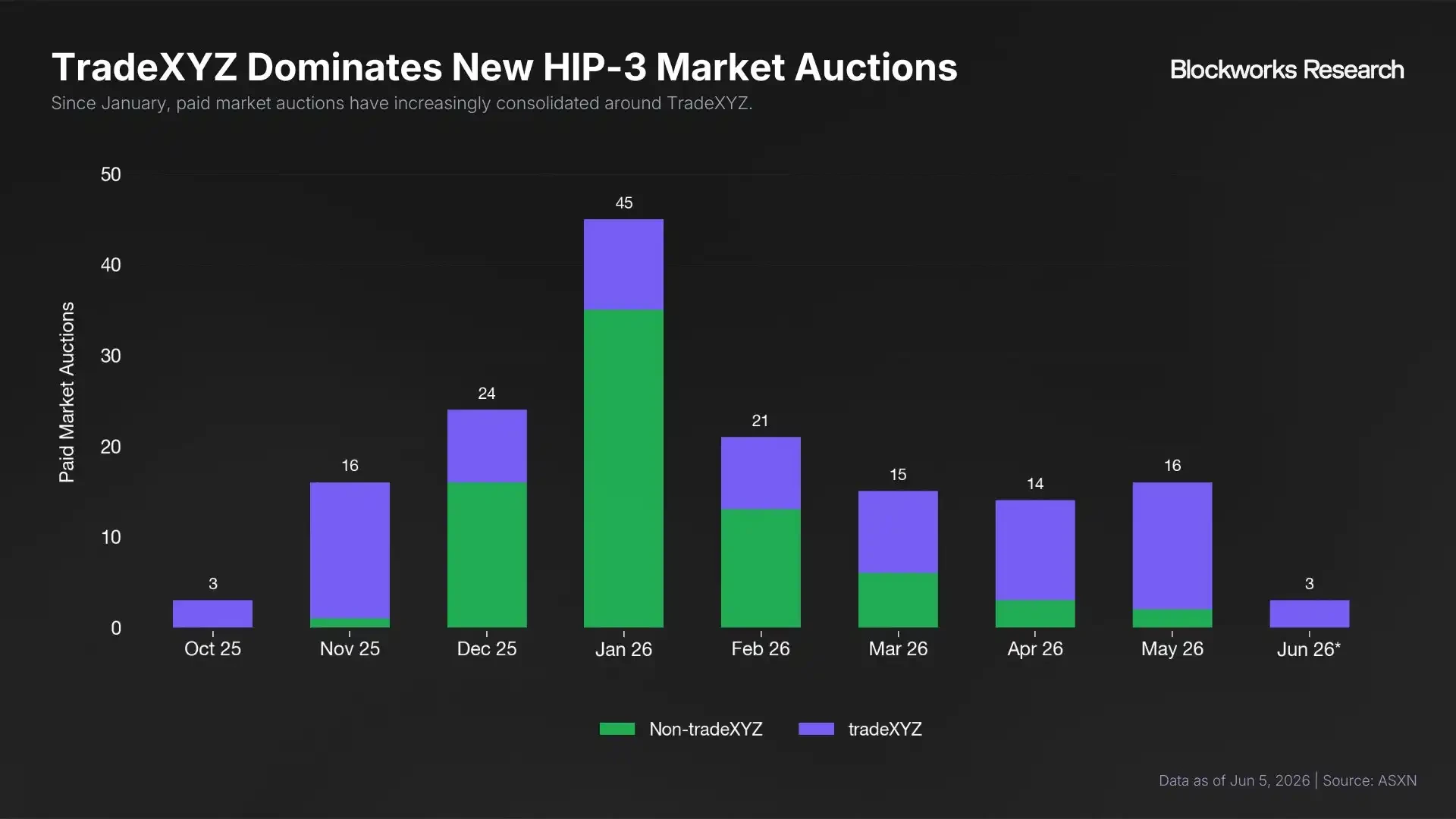

First, let's look at trading volume. As of the first week of June, TradeXYZ held a monopoly on 95.85% of HIP-3 trading volume. The remaining seven collectively accounted for less than 5%, with the second-place dreamcash at only 2.75%, and the third-place Kinetiq's Markets at 0.64%, HyENA at 0.49%.

Source: ASXN

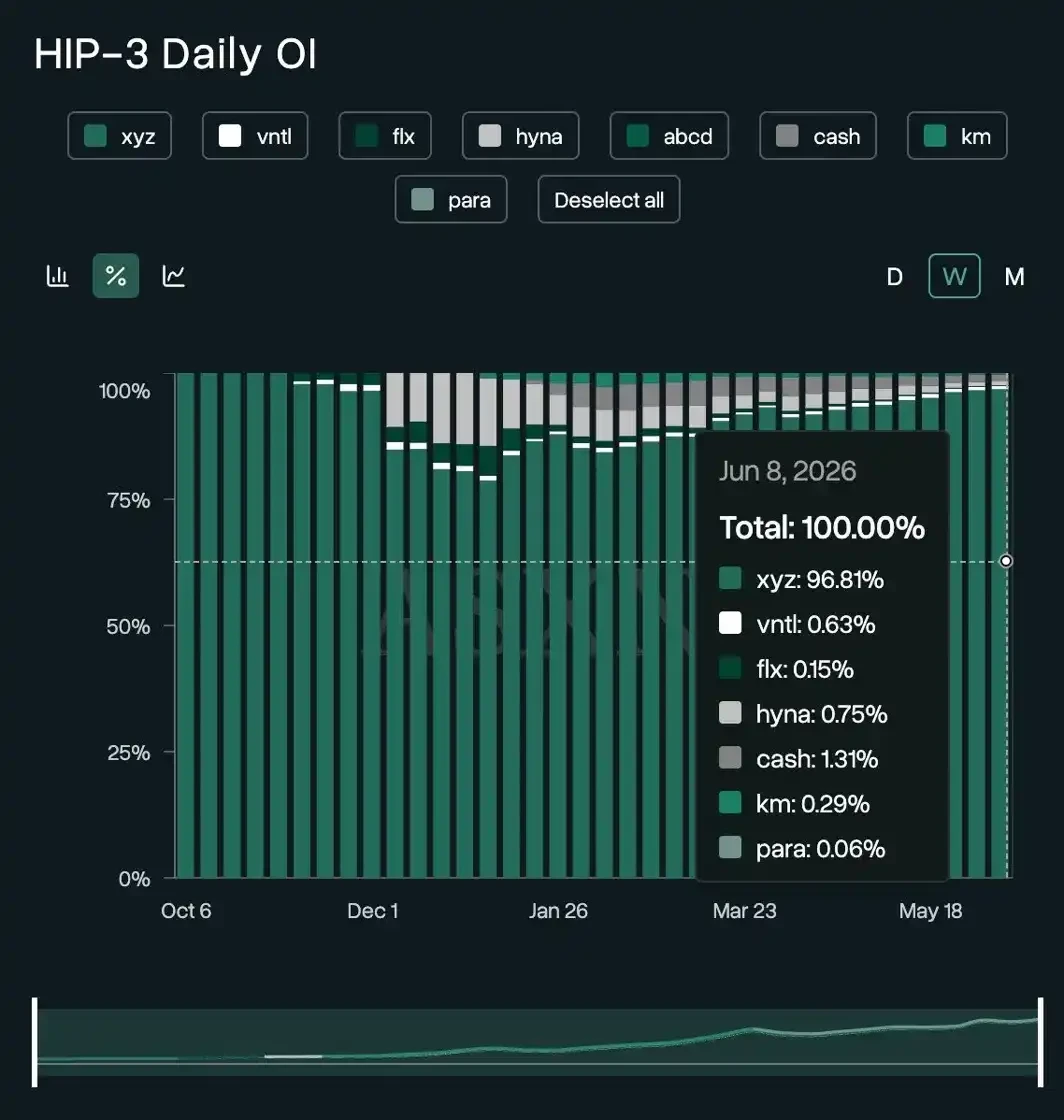

The concentration of open interest is even higher, with TradeXYZ accounting for 96.81%.

Source: ASXN

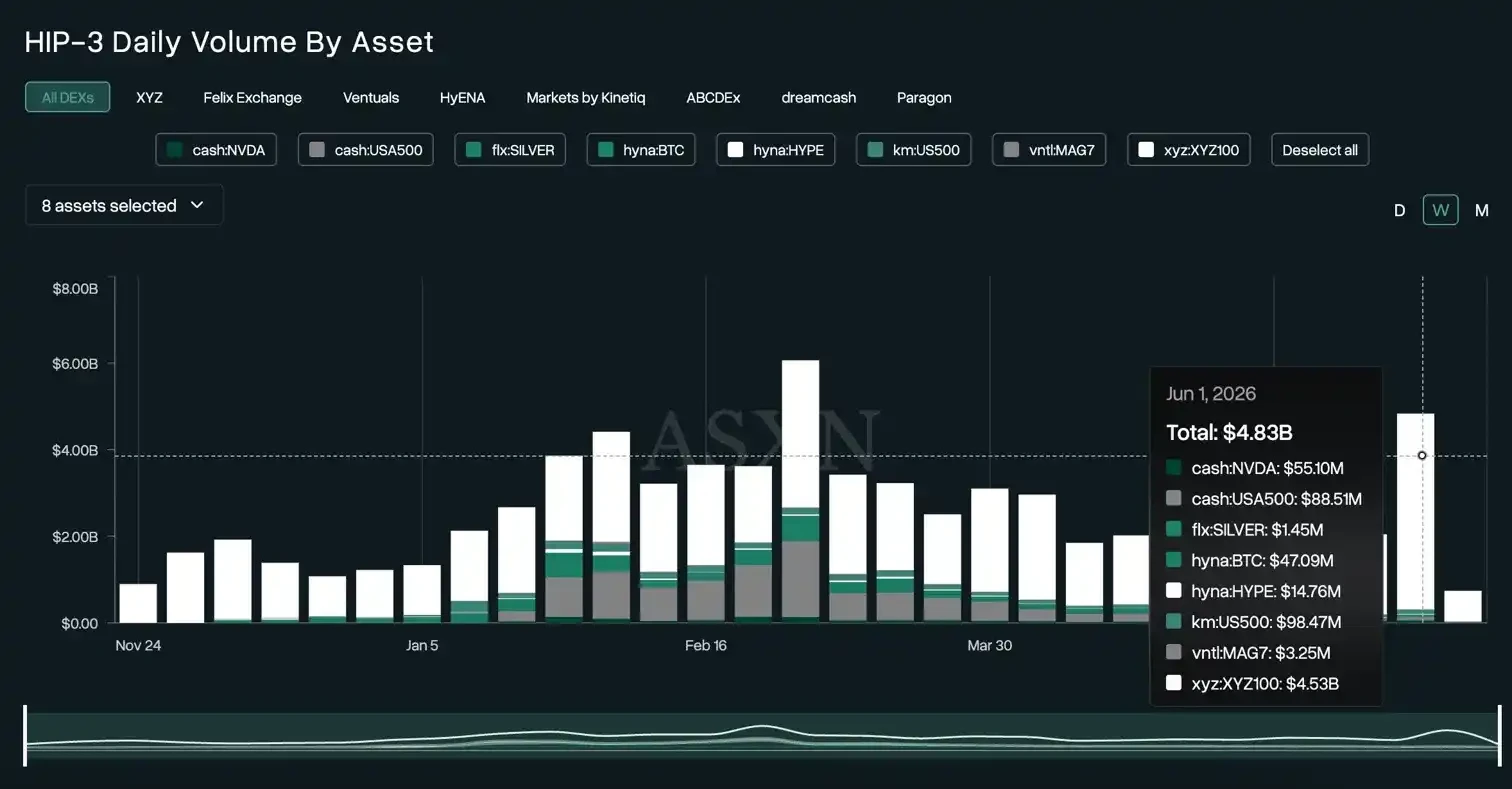

This monopoly pattern has almost persisted throughout. From the launch of the HIP-3 proposal in October last year to May this year, TradeXYZ's volume share never dropped below 60%.

In the first week of June, the total trading volume for HIP-3 reached $4.8 billion, with TradeXYZ's XYZ100/USDC trading pair alone contributing $4.53 billion.

Source: ASXN

High Costs, Low Returns

To understand why other deployers are struggling so much, one must lay out the costs of opening a HIP-3 trading platform.

Two costs are clearly marked. Deploying a HIP-3 trading platform requires staking 500,000 HYPE, equivalent to about $30 million (calculating HYPE at $60).

Source: HypurrScan

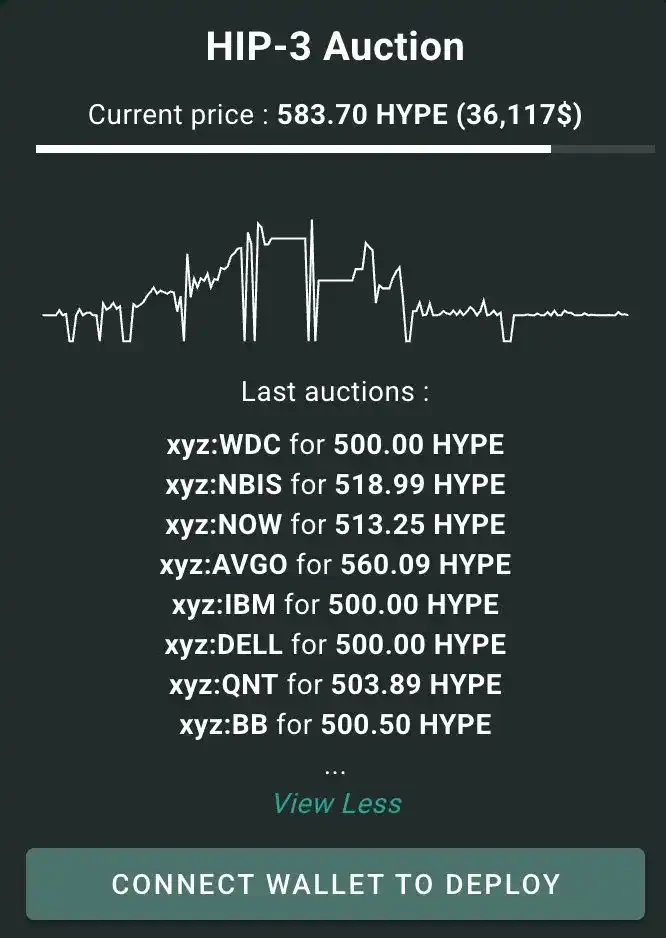

The second cost is the Ticker auction; for each new trading pair, one must buy the next Ticker through auction, with an average transaction price around 500 HYPE, approximately $30,000. Currently, this auction market is monopolized by TradeXYZ, and since February, there has been decreasing enthusiasm for participating in auctions among non-TradeXYZ players.

Source: Blockworks Research

Opening a HIP-3 trading platform incurs not only high costs but also very thin profits.

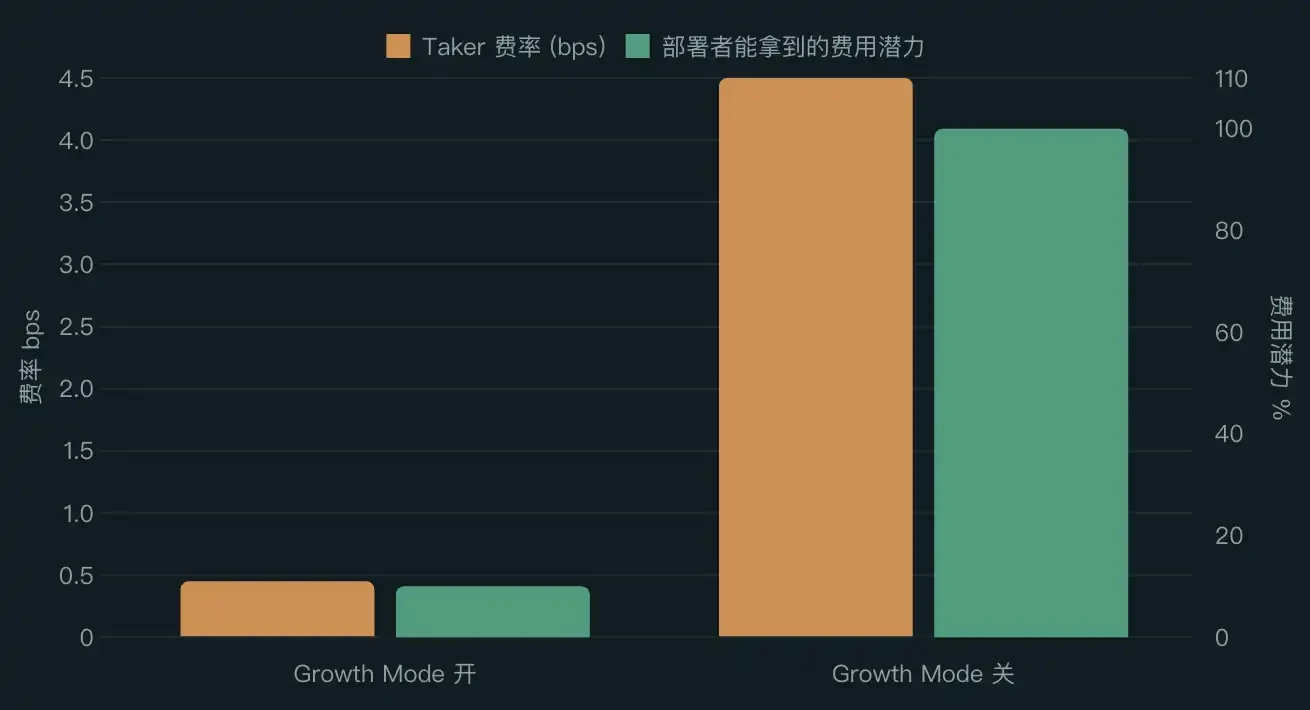

In order to match the fee rates of traditional brokers for their perpetual contracts, Hyperliquid introduced Growth Mode. When Growth Mode is activated, Taker fees are drastically reduced, allowing users to open an NVDA position here cheaper than at Interactive Brokers. The trade-off is that deployers can only earn about one-tenth of the potential fee income.

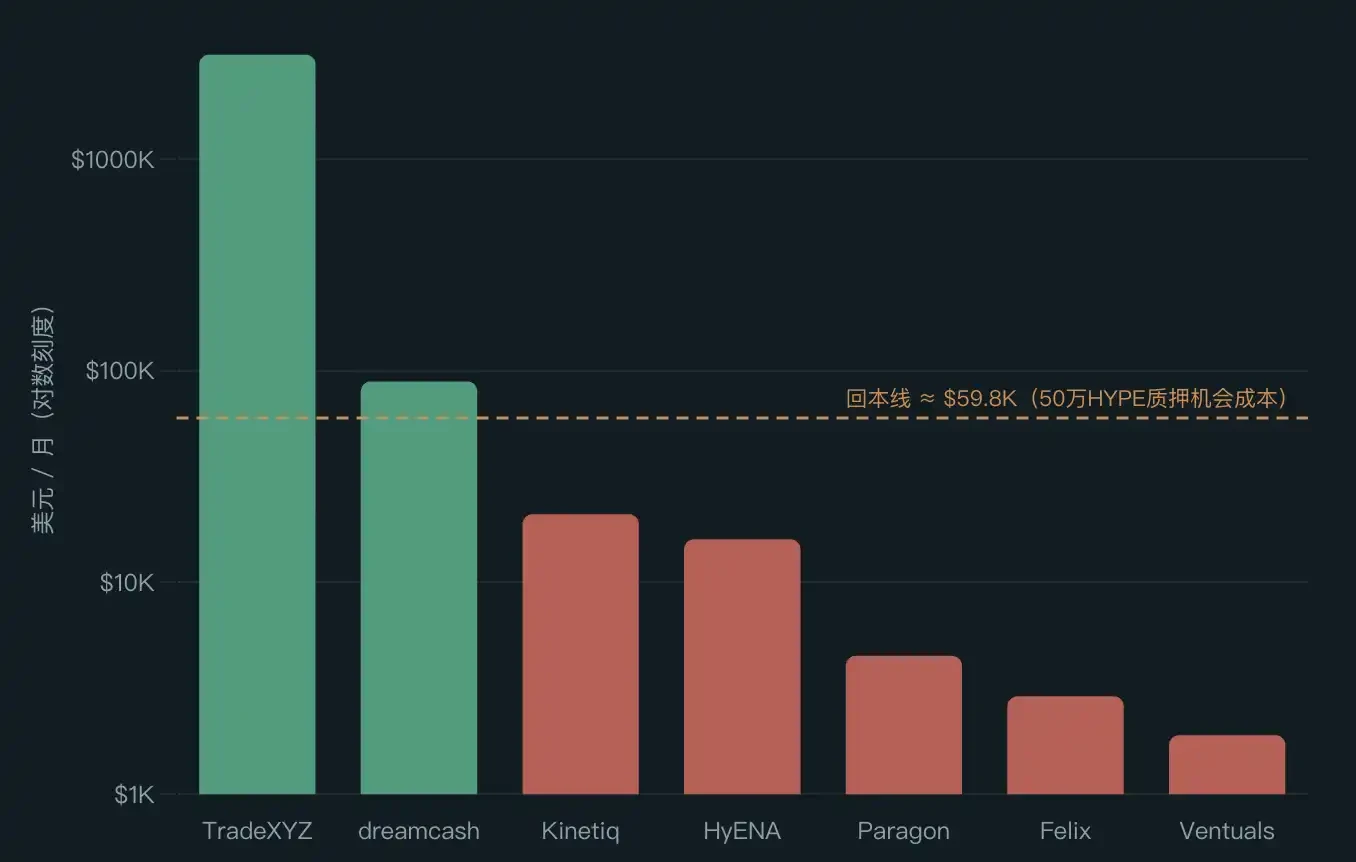

If a deployer does not open a trading platform and directly stakes 500,000 HYPE, at an annual yield rate of approximately 2.3%, they could receive about $60,000 each month. This means that simply opening a trading platform has to surpass the opportunity cost of "doing nothing," with monthly fee income needing to exceed $60,000.

Here are the revenue figures for various trading platforms in May: TradeXYZ earned approximately $3.1 million, dreamcash about $89,000, Kinetiq around $21,000, and HyENA around $16,000. The remaining platforms were all below $5,000.

Except for TradeXYZ, only dreamcash managed to break even. All other deployers didn’t even cover the opportunity cost of 500,000 HYPE. This doesn't even take into account market making, oracle, team salaries, and liquidity incentives, which are harder to quantify expenses.

Source: Blockworks Research

The State of Things

The few trading platforms that are still holding on have their own methods of survival.

Dreamcash quotes assets as USDT0, backed by Tether. Tether provides it with about $200,000 in trading incentives weekly, translating to approximately $867,000 a month, far exceeding the platform's fee income. Coupled with the expectation of an airdrop, dreamcash firmly sits in second place in trading volume.

Kinetiq Markets has an innovative "crowdfunding mechanism." Kinetiq developed a platform called Launch, which founder Omnia describes as a combination of "Shopify + Kickstarter," allowing others to deploy their customized HIP-3 trading platform using 500,000 HYPE raised through crowdfunding. Markets itself is a model of this mechanism, meant to demonstrate that Launch's model can work, rather than competing with TradeXYZ for trading volume.

The Road Ahead

Felix will certainly not be the last HIP-3 trading platform to close down, as there is not much room left for other players to adjust.

Perhaps one could venture into niche or new markets that TradeXYZ is unwilling to touch, but Felix has already validated for everyone that the end of this road is "once volume is made, it gets copied and drained by TradeXYZ."

Alternatively, one could change distribution channels to establish their own user base in newly added markets, circumventing this red ocean of Hyperliquid native traders. Kinetiq's Launch is an attempt in this direction but has yet to successfully run through.

However, if there is no relaxation at the cost end, the current monopolistic pattern is likely to persist.

There have been proposals in the community to lower the staking threshold of 500,000 HYPE and set auction prices lower but floating with the price of HYPE. From this perspective, a decrease in HYPE's price is not necessarily a bad thing, as it allows more projects to build on Hyperliquid at a lower cost.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。