Original author: Ye Zhen, Wall Street News

Bank of America strategist Hartnett issued a warning: If the upcoming inflation data exceeds expectations, it will directly trigger a sell-off of risk assets. Historical data shows that in the past 100 years, once CPI breaks 4%, the S&P 500 index averages a 4% drop in the next 3 months and a 7% drop in the next 6 months.

Moreover, market "sell signals" continue to strengthen, large IPOs like SpaceX will withdraw record liquidity, and the global central banks' hawkish shifts towards risk pose an extremely vulnerable moment for the tech bubble.

The U.S. stock market is facing a severe stress test in June. Michael Hartnett warned that a series of intensive macro events and a sharp withdrawal of market liquidity could push global bond yields significantly higher, thereby bursting the current tech asset bubble.

According to Wind Trading Desk, Hartnett stated in his latest research report that the upcoming U.S. CPI data is the core catalyst for this "June storm". If the latest inflation data exceeds expectations, it will directly trigger the sell-off mechanism for risk assets. Historical data indicates that when inflation breaks through key warning levels, it often triggers a deep correction in the U.S. benchmark stock index in the following months.

Meanwhile, the intensive resolutions and statements from global central banks are currently dominating market direction. In particular, the upcoming Federal Open Market Committee (FOMC) meeting led by new Federal Reserve Chairman Waller will determine the fate of U.S. stocks and long-term bond yields, with any unexpected tightening signals likely to deal a heavy blow to investors.

Amid extreme bullish sentiment in the market, Bank of America's internal sentiment indicators have issued a strong "sell signal". Coupled with the unprecedented withdrawal of market liquidity from upcoming massive tech IPOs, current risk assets are in an extremely vulnerable position.

Key inflation data approaching, U.S. stocks facing historic retracement risk

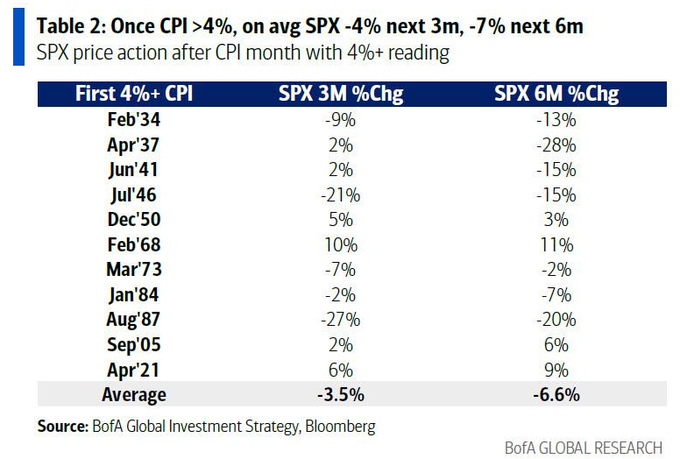

The U.S. CPI data set to be released on June 10 is the primary test the market faces.

In the past three months, the data has averaged a month-on-month increase of 0.6%, and a 0.4% increase over the past six months. If the May CPI month-on-month growth exceeds 0.4% (with current market expectations at 0.5%), this would mean that the U.S. CPI year-on-year growth will surpass 4% and could approach 5% before the U.S. midterm elections. This trend will make risk assets extremely uneasy.

Historical data shows that in the past 100 years, once CPI breaks 4%, the S&P 500 index averages a 4% drop in the next 3 months and a 7% drop in the next 6 months.

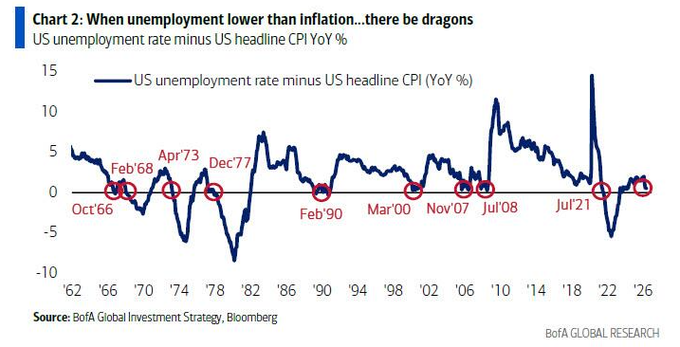

Another inflation indicator that cannot be ignored is the intersection of unemployment rate and CPI.

In May, there exists a "very low probability but highly impactful possibility" that the U.S. unemployment rate (consensus expectation 4.3%) equals or drops below the inflation rate (consensus expectation 4.2%), which would be the 7th occurrence since 1960. In years when inflation is close to or above unemployment (such as 1966, 1973, 2008, and 2021), the Federal Reserve typically takes rate-hiking actions, and Wall Street's memories of those years are often painful.

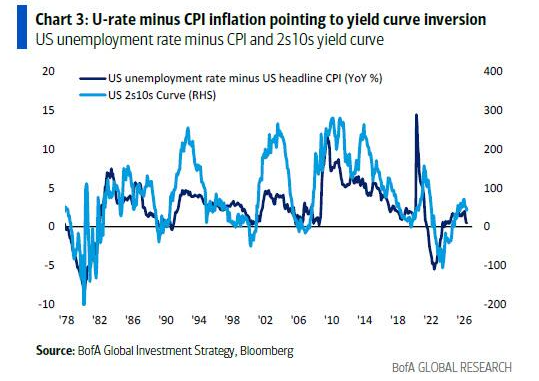

Additionally, the difference between the unemployment rate and CPI is highly correlated with the U.S. yield curve, which currently points to a recent curve inversion, another signal negatively impacting risk assets.

Global central bank intensive resolutions, bond yields may end the prosperity

"Prosperity and bubbles are ultimately terminated by bonds." Michael Hartnett reiterated this logic in his report.

He warned that a series of events in June could cause the UK 30-year government bond yield to exceed 6%, the U.S. to exceed 5%, and Japan to exceed 4%. Given that the current market is filled with bullish positions and optimistic earnings expectations, the surge in yields is undoubtedly negative for risk assets.

Global central banks are currently significantly behind the inflation curve. Among 68 global central banks, 46 currently have inflation levels exceeding their targets or the absolute midpoint of their target ranges. In this context, the European Central Bank (ECB) has a 98% probability of raising rates by 25 basis points, while the Bank of Japan (BoJ) has an 83% probability of a 25 basis point increase, the latter urgently needing to prevent the yen from falling below the "Maginot Line" of 160 yen to 1 dollar.

The June 17 FOMC meeting led by Waller is considered one of the two most important events of the month.

The market currently faces a policy dilemma: If Waller is too dovish, long-term yields will move towards 6%; if too hawkish, the S&P 500 index will face a risk of retreating towards the 7000 point region; whereas a "Goldilocks" moderate statement could possibly push the New York Stock Exchange Composite Index (NYA) past the historical high of 24000 points.

As Waller mentioned in 2024, global central banks seem complacent at a near 3% inflation rate, with the 2% inflation target no longer taken seriously, and this compromise is extremely dangerous.

Wealth effect boosts inflation, extreme sentiment triggers "sell signal"

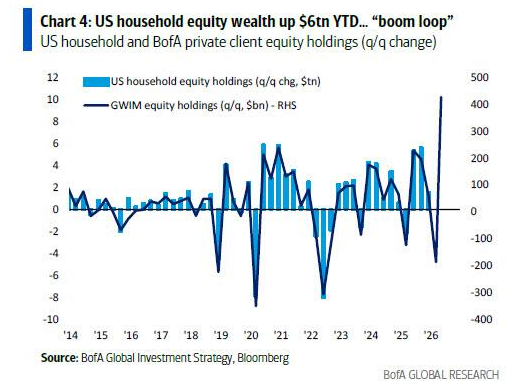

From a macroeconomic perspective, the U.S. is experiencing a K-shaped recovery driven by wealth and stock market "prosperity cycles".

American households' stock wealth has increased by $6 trillion since the beginning of the year, and this "wealth-price spiral" directly exacerbates inflationary pressure. Despite economic prosperity, voter sentiment is not uniform, and Trump's inflation support rate is now lower than Biden's lowest level.

In terms of capital flows, investors are currently exhibiting extreme tendencies to chase tech bubbles. Last week's data showed a cash inflow of up to $122 billion, a record $39 billion into bonds, and a $23.1 billion inflow into the stock market. Meanwhile, cryptocurrency saw an outflow of $2 billion, and gold an outflow of $3.1 billion, indicating that investors are selling other assets to pursue tech and semiconductor sectors.

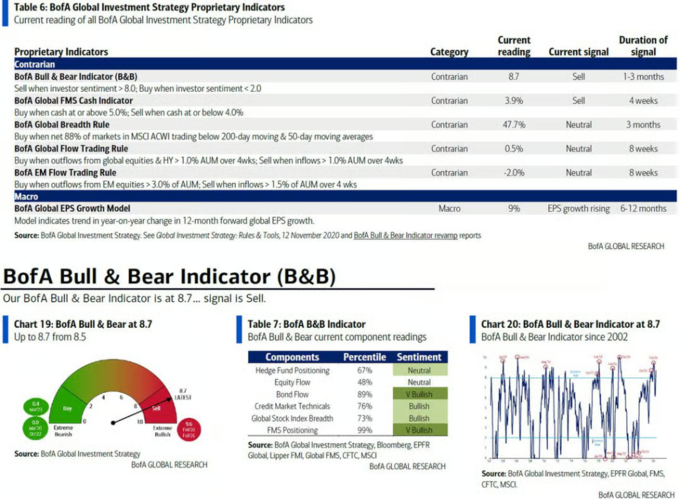

The extreme capital flow has caused Bank of America's Bull/Bear indicator to rise from 8.5 to 8.7, intensifying the "sell signal" triggered two weeks ago.

Historical data show that of the 17 "sell signals" since 2002, global stock markets averaged losses of 2% to 3% in the following 2 to 3 months, with maximum drawdowns reaching 15% to 20%. Additionally, global breadth indicators show that 48% of global stock markets are in overbought conditions.

Massive IPOs withdraw liquidity, non-economic events exacerbate market turmoil

In addition to macroeconomic data, the largest non-economic event risk in June comes from substantial supply in the capital markets.

SpaceX's initial public offering (IPO) will start trading next Friday, alongside the offerings of Anthropic and OpenAI, as well as the end of related lock-up periods, which will withdraw record liquidity from the market. Such a tightening of liquidity may act as a market catalyst, potentially surpassing the decisions of central banks.

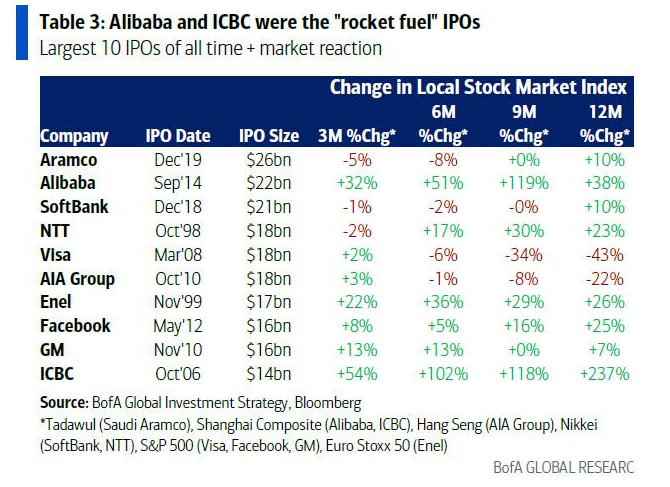

The impact of historical massive IPOs on the market has shown divisions.

While Alibaba and Industrial and Commercial Bank's IPOs acted as catalysts for the market, the listings of Visa and AIA marked the "peak" of the market, with the S&P 500 index and Hang Seng Index experiencing significant declines in the 9 to 12 months following these IPOs.

Hartnett believes that this political shift is the core reason for the current historical lows in Latin American bond yields and spreads (down to the lowest 217 basis points since November 2007), and a similar political rightward trend is also evident in Europe.

For investors, this signifies a profound and substantive reassessment of global economic policy preferences occurring recently.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。