TL;DR

- Rubin cabinet system memory configuration adjustment leads to a collective pullback in the AI memory sector.

- The true market reassessment is not about AI memory demand, but rather about the profit distribution among different memory segments.

- Related stocks: MU (US), NVDA (US), 000660.KS (Korean stock), 005930.KS (Korean stock), SMH (US ETF), SOXX (US ETF)

A supply chain report regarding Nvidia's Rubin cabinet has caused an initial decline in the AI memory sector.

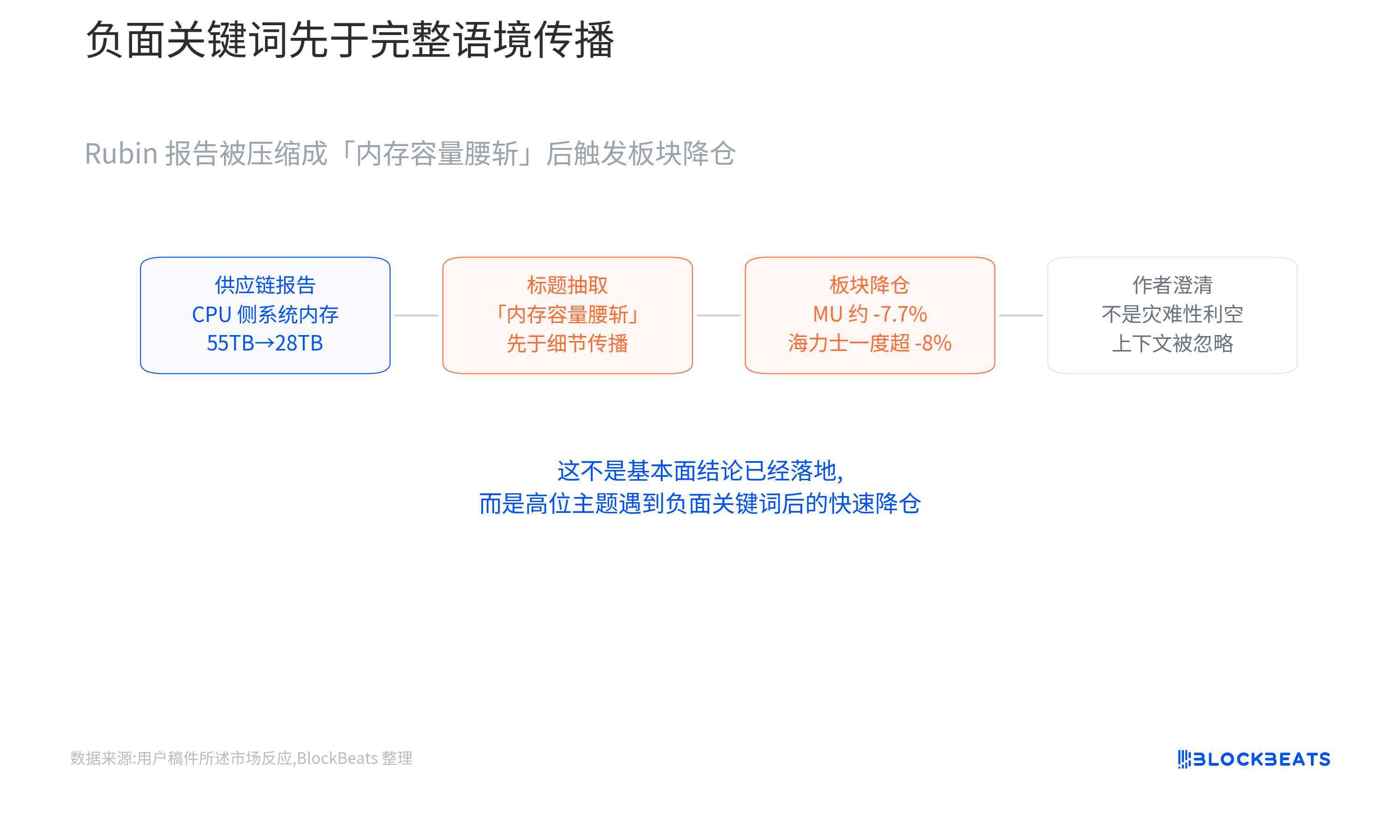

The report mentioned that the memory capacity per cabinet might decrease from about 55TB to around 28TB. Following this, Micron fell by about 7.7% in a single day, and SK Hynix opened the next day with an over 8% drop initially. More subtly, report author Dylan Patel later clarified that many forwards only captured the most alarming part, and this was not a "disastrous negative" report.

The significant reaction to this event is due to its impact on the most sensitive aspect of the AI hardware market. Recently, the market has not been trading on an ordinary memory cycle, but rather on the expectation that after mass production of Rubin platforms, AI cabinets will continue to drive demand for HBM and associated memory, thereby elevating the revenue and pricing power of memory suppliers. Since this year's GTC, HBM4, SK Hynix's market share, and Micron's chase for AI memory have been key threads in the market's repeated trading.

However, the notion of "memory being cut" is too simplistic.

The adjustment disclosed by SemiAnalysis mainly refers to the configuration changes in CPU side SOCAMM and LPDDR in the Rubin NVL72 cabinet. Most systems may use 96GB modules instead of higher-capacity 192GB modules, reducing the memory capacity per cabinet from the planned approximately 55TB to about 28TB. This change will affect the system memory value in a single cabinet but does not directly lead to a simultaneous reduction in GPU side HBM4 demand.

What really needs to be clarified is which profit pool this adjustment affects and what expectations the market is currently trading.

Why did AI memory stocks collectively drop sharply?

The market is reacting to positions in high-profile themes encountering negative keywords.

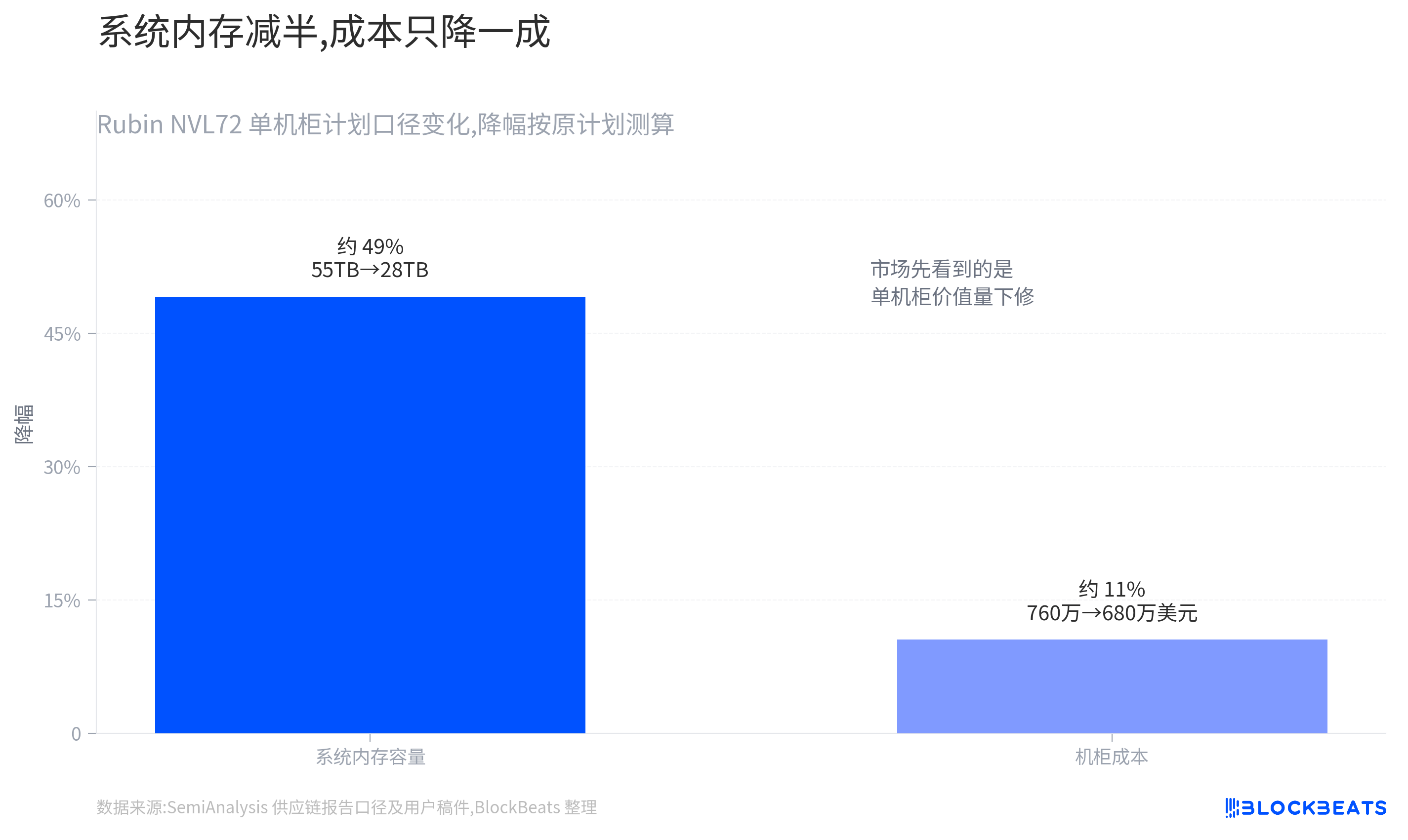

What has been confirmed so far is that the market's reaction is quite severe, but the event itself remains at the level of a supply chain report. SemiAnalysis revealed that Nvidia may adjust the CPU side SOCAMM configuration to ensure the delivery rhythm of Rubin NVL72. The report mentions figures indicating a reduction of memory capacity per cabinet from about 55TB to around 28TB, and cabinet costs decreasing from approximately $7.6 million to about $6.8 million. These figures should be understood as the reporting standard from SemiAnalysis and are not yet the final BOM (Bill of Materials) confirmation from Nvidia.

In the past few quarters, the rise in AI memory stocks has been supported by a straightforward narrative: the more AI cabinets there are, the scarcer advanced memory becomes, leading to thicker supplier profits.

The simpler this story is, the more lethal the impact of negative headlines becomes. Once "memory capacity is halved" appears, the market will first revise down the value of memory per cabinet, rarely differentiating which type of memory is being adjusted.

Micron's reaction best illustrates the problem.

It is both a traditional DRAM supplier and a beneficiary of AI server memory upgrades. A significant part of the flexibility the market previously assigned to it came from the repricing of "AI memory is no longer just a cyclical product." If the memory capacity of the Rubin cabinet system drops, investors will immediately worry whether Micron's revenue expectations in the SOCAMM and LPDDR segments have been overly inflated.

SK Hynix also fell, indicating that this impact has extended beyond a single supplier.

It is stronger in the HBM sector, and there were previous reports that it secured most of the HBM orders related to Vera Rubin. However, when AI memory trading becomes crowded, funds will not wait for all details to be clarified before acting. The simultaneous drop in memory stocks reflects a contraction in sector risk appetite, rather than each company being subjected to the same fundamental impact.

Dylan Patel's subsequent clarification actually points to this issue. He stated that the report did not intend to create a "disastrous" narrative, and many overlooked the context.

In market terms, it means that funds did not complete a full trade of a supply chain analysis, but rather they were trading on a rapid reduction in exposure after a high-profile sector encountered negative keywords.

AI memory begins to redefine profit pools

This time, the primary adjustment involves the system memory on the CPU side, not the HBM4 beside the GPU.

The memory within the Rubin cabinet cannot be summed up with just one term. The simplest breakdown consists of two layers:

The first layer is the HBM4 on the GPU side, which serves the acceleration chips themselves;

The second layer consists of the CPU-side SOCAMM and LPDDR, more like the operating memory of the entire system.

The former determines the speed at which data is fed to the GPU, while the latter impacts overall scheduling, maintenance, and performance on certain workloads.

The "55TB to 28TB" mentioned by SemiAnalysis mainly pertains to the CPU side system memory.

It may change the number of SOCAMM modules, their capacity, and the purchasing amount within each Rubin NVL72 cabinet. If most systems shift from 192GB modules to 96GB modules, the unit value of high-capacity SOCAMM indeed decreases, which could pressure the revenue elasticity of related suppliers.

However, the GPU side HBM4 is a separate line.

The Rubin platform still revolves around the Rubin GPU and Vera CPU, and HBM4 remains a core memory segment for GPU packaging and computational power release. Current information does not indicate that HBM4 capacity or Rubin GPU shipments are being simultaneously reduced. Previous forecasts still regard HBM as one of the most scarce and price-controlling segments in AI servers, with SK Hynix seen as a major beneficiary.

AI cabinets can be understood as extremely expensive high-performance servers.

HBM is closer to being high-speed memory mounted next to the GPU, while SOCAMM is more akin to the replaceable system memory of the entire machine. This adjustment primarily affects the latter.

For holders, the distinction is quite direct: If Micron has a larger exposure in the SOCAMM segment, a reduction in unit value will first impact its expectations; SK Hynix's HBM logic is relatively independent, but in crowded trading, it will similarly be dragged down by sector sentiment.

Directly extrapolating a reduction in system memory configuration to a collapse in HBM4 demand lacks sufficient evidence.

A more reasonable breakdown is that the CPU-side profit pool indeed faces downward pressure, while the GPU side HBM still depends on the overall shipment and HBM4 order rhythm for Rubin.

The AI memory market can no longer be covered by a single narrative that "all memory is strong." Micron, SK Hynix, and Samsung Electronics have different exposures in HBM, SOCAMM, traditional DRAM, and NAND, and different types of memory within the same cabinet correspond to different prices, gross margins, and supply-demand constraints.

Can cost reduction lead to more cabinet shipments?

An optimistic interpretation arises from cost and delivery rhythm.

SemiAnalysis's estimates suggest that Rubin NVL72 cabinet costs may decrease from about $7.6 million to around $6.8 million, a reduction of about $800,000.

For cloud vendors like Microsoft, Google, Amazon, and Meta, AI cabinets are not just about buying hardware, but also calculating hourly computing costs, supply times, and stability in large-scale deployments.

If a reduction in specification can enable faster delivery of Rubins, the decline in value per cabinet might be offset by more cabinets being shipped.

The logic isn’t complicated. If high-capacity SOCAMM is tight on supply, Nvidia's choice of easier-to-deliver configurations can lower the BOM of each cabinet and reduce the risk of particular components hindering the overall delivery.

For buyers, if the lower system memory configuration does not significantly affect core workloads, getting the cabinets sooner might be more appealing than waiting for the fully equipped versions.

The problem is that this step remains speculative for now.

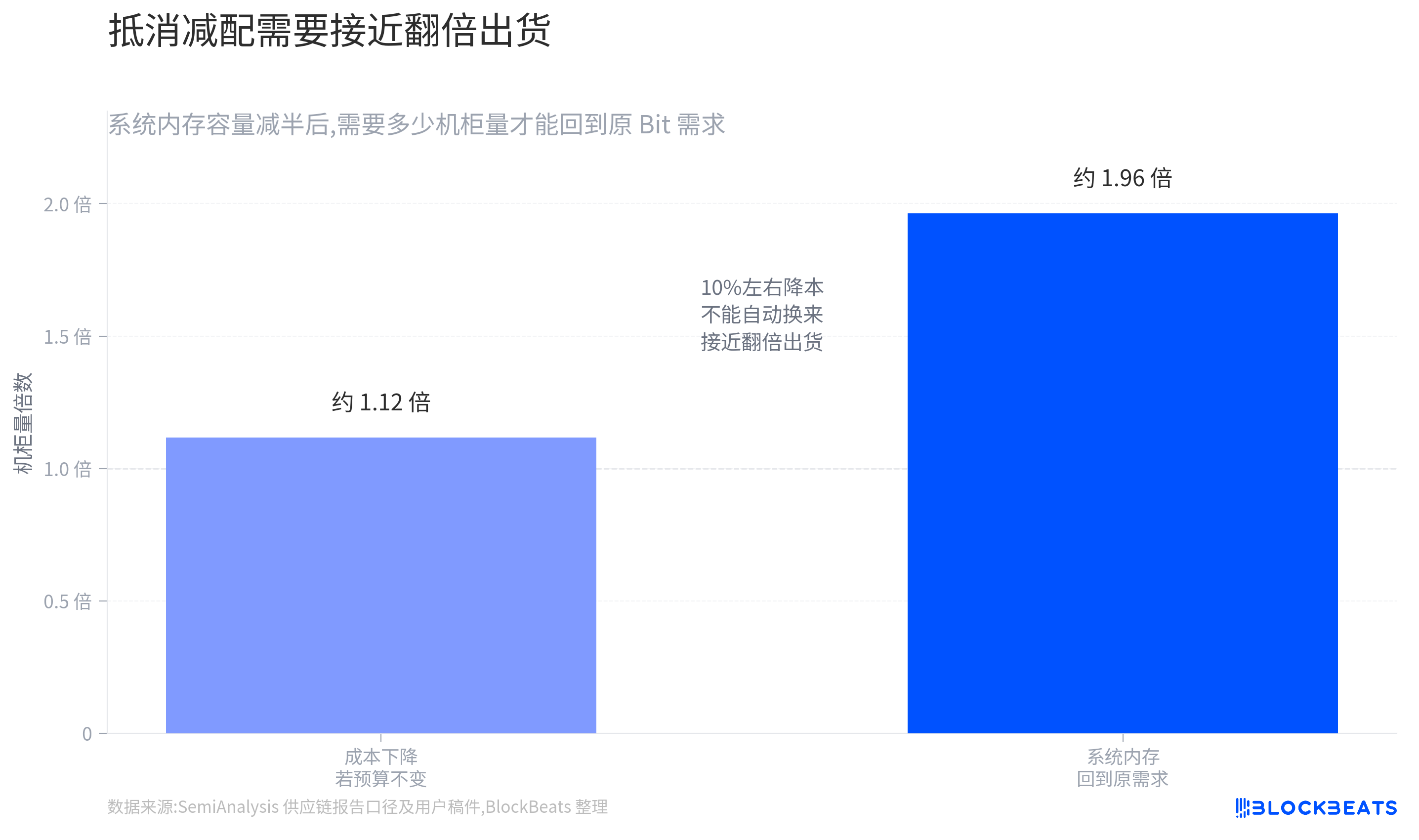

A decrease in costs does not automatically equate to an increase in orders. To offset "declining unit value" with "increased total cabinet quantity," Nvidia needs to deliver more Rubin NVL72s, and cloud vendors also need to increase or pull forward purchases.

Existing materials have not yet provided public orders, quarterly guidance, or actual shipment data to prove this.

In a simple scenario, if a certain type of SOCAMM's capacity is nearly halved in each cabinet, total cabinet shipments would need to significantly increase in order to bring the total Bit demand for this segment back to the original expectations.

Even if costs decline by about 10%, it does not directly imply that customers will buy enough cabinets. Large cloud vendors' procurement is also influenced by power, data center construction, GPU supply, advanced packaging, and networking equipment; a single decrease in BOM is just one variable among many.

The situation with HBM is relatively more stable, but not completely immune.

If total Rubin shipments remain strong, HBM4 will still be one of the most directly benefiting segments; however, if subsequent evidence shows that overall delivery is hampered by other bottlenecks, HBM will also be impacted by the platform's shipment rhythm.

The distinction is that this report did not directly lower HBM4 configurations, and the market is waiting for total cabinet shipment volumes rather than fixating solely on SOCAMM capacity numbers.

Shipment data is the real pricing anchor

The biggest risk currently is that the market first reassesses by splitting profit pools and later data does not support an optimistic explanation.

If Nvidia or the supply chain eventually confirms that the Rubin NVL72 will long-term adopt a lower SOCAMM configuration, while total cabinet shipments do not show significant upward revisions, CPU-side system memory suppliers will face more persistent revenue expectation compressions.

For Micron, the key is not just the overall label of "benefiting from AI memory," but rather the revenue breakdown across different products.

In subsequent earnings reports and conference calls, it will be essential to see if management discloses the growth rhythm of DRAM, SOCAMM, and HBM related to AI servers, and whether gross margins have changed due to specifications, pricing, or customer negotiations.

If the company only provides an overall optimistic demand statement but cannot explain the impact of SOCAMM configuration adjustments, the market may continue to apply discounts.

For SK Hynix, the validation point leans more toward HBM.

If its HBM4 order share, shipment rhythm, and pricing remain strong, this pullback would appear more like a fluctuation in sector sentiment; however, if subsequent total Rubin shipments or HBM delivery rhythms also show downward revisions, the market will then expand the impact from SOCAMM to the HBM mainline.

This also reflects a typical change in the AI memory theme as it progresses.

In the early stages, the market bought into the direction: the more AI cabinets built, the scarcer advanced memory became.

Now, representative stocks have accumulated significant gains, and funds are starting to check whether each piece of profit is truly being realized. A single detail in the supply chain can trigger a 7%-8% daily fluctuation, indicating that sector trading has become crowded and negative information is more easily amplified.

Until actual shipments and earnings reports are separated out, qualifying this pullback as “all bad news is out” or “AI demand collapse” is still too early.

A more prudent view is to acknowledge the pressure of the CPU-side unit value adjustment, while separating the pricing of HBM4 from SOCAMM.

The next factors most likely to change judgments will still be whether Nvidia confirms the final BOM for Rubin NVL72, whether the actual shipment plans for Rubin cabinets can be upgraded, and how Micron, SK Hynix, and Samsung Electronics' exposure and gross margins in HBM and SOCAMM/LPDDR evolve.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。