Original author: Zhao Ying

Original source: Wall Street Watch

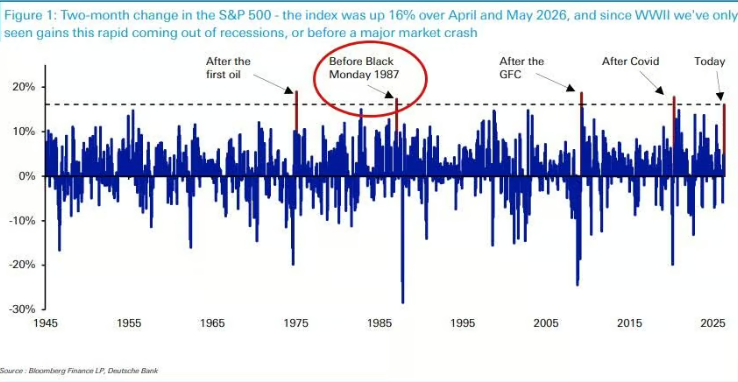

The strong rebound of U.S. stocks in the past two months is triggering historical alarms. The S&P 500 index rose by 16% from April to May, a surge that has only occurred four times since World War II, three of which took place during the recovery phase after economic recessions, while the only precedent outside a recession context was just months before the "Black Monday" crash in 1987.

Deutsche Bank macro strategist Henry Allen pointed out that the current rally is not taking place against the backdrop of an economic recovery from a recession, making the historical comparisons particularly striking. Meanwhile, credit spreads remain at historical lows, but signals of pressure on the consumer front are accumulating, expectations for interest rate hikes from the Federal Reserve are heating up, and the divergence between the sovereign bond market and the stock market continues to widen.

Amid multiple risk factors overlapping, market tail risks are unusually concentrated. Henry Allen wrote in the report, "The current distribution of tail risks is extraordinarily prominent, whether in terms of geopolitics or the market itself."

Rare historical precedent, only this one case in a non-recession context

The S&P 500 index saw a gain of 16% from April to May, which has only occurred four times since World War II.

Three of these instances occurred during powerful rebounds following recessions: the recovery after the COVID-19 pandemic from April to May 2020, the rebound following the global financial crisis from March to April 2009, and the recovery after the first oil crisis from January to February 1975.

The 4th instance was from January to February 1987. At that time, there were only a few months left before the "Black Monday" in October of that year—on that day, the S&P 500 fell by 20% in a single day.

Henry Allen emphasized that the current rally is supported by fundamentals, including enthusiasm for artificial intelligence and strong economic data, but "the speed of gains has already surpassed all recent precedents." In an economy that has not emerged from a recession, such a rapid rebound has historically never ended well.

Additionally, the S&P 500 is currently expected to achieve a double-digit gain for the fourth consecutive year, a record that has not been seen since the late 1990s.

Credit market overly optimistic, consumer pressure signals ignored

The strength in the stock market is also spreading to the credit market. The credit spreads in both the U.S. and Europe are currently narrower than before the U.S.-Iran conflict erupted, indicating a high tolerance for risk in the market.

However, warning signals on the consumer front are accumulating. The U.S. savings rate in April was only 2.6%, a level that has only been seen during two periods in history: a certain month in 2022 (when excess savings accumulated during the COVID-19 pandemic were being exhausted), and just before the outbreak of the global financial crisis. Meanwhile, the University of Michigan consumer sentiment index hit its lowest level on record since 1952 in May.

The monetary policy environment is also tightening. The European Central Bank is widely expected to raise interest rates this month, and expectations for the Federal Reserve to raise rates in 2026 are also heating up—April's U.S. PCE inflation year-on-year reached 3.8%, supporting this expectation.

Henry Allen pointed out that historically, a hawkish stance from the Federal Reserve often coincides with widening credit spreads, as seen in 2022, late 2018, and 2015 to 2016. The current calm in the credit market is in stark contrast to this historical pattern.

Bond market under pressure, divergence from stock market continues to widen

While the stock market and credit market demonstrate a high immunity to geopolitical risks, the sovereign bond market has taken a distinctly different path.

In the past month, the 10-year U.S. Treasury yield has almost completely followed oil price fluctuations, significantly decoupling from other asset classes. In mid-May, sovereign bond yields reached multi-year highs: the 30-year U.S. Treasury yield rose to 5.18%, the highest since 2007; the 10-year German bond yield rose to 3.19%, the highest since 2011.

At that time, the stock market was just a step away from its historical peak, while bond yields were at levels not seen in over ten years. This divergence has yet to show any signs of convergence.

Henry Allen believes that the bond market more directly prices inflation and fiscal risks, and thus is more sensitive to geopolitical shocks. The ongoing divergence between the stock market and the bond market is itself a reflection of the current fragility of the market.

Oil prices unexpectedly stable, becoming a key pillar for risk assets

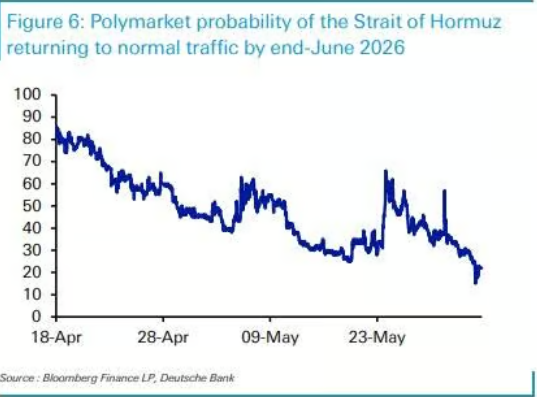

The blockade of the Strait of Hormuz has lasted far longer than the market initially expected, but the response of oil prices has been surprisingly mild, which to some extent explains the resilience of risk assets.

When the U.S.-Iran conflict erupted on February 28, the White House initially expected actions to last 4 to 6 weeks. However, as of now, the Strait of Hormuz remains under blockade. According to predictive market data from Polymarket, the probability of a return to normal navigation by the end of June has plummeted from about 80% in mid-April to 22%.

Despite this, the oil futures curve remains relatively stable. Just two weeks after the conflict erupted on March 13, Brent crude oil futures for six months settled at $85.66 per barrel; as of June 1, the contract price is still around $84.88, nearly unchanged.

Henry Allen noted that because the oil futures curve has not shown significant upward movement, investors have not incorporated the serious stagflation risks into pricing, thus avoiding larger-scale sell-offs in risk assets. However, he also warned that if the Strait of Hormuz remains blocked, it remains uncertain whether this support can be sustained.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。