TL;DR

Stablecoin Competition Changes Lanes: From trading medium to payment settlement network; the value chain restructured into issuance, distribution, settlement, yields, and compliance

Restructuring of Issuance and Distribution: The focus of competition shifts from issuance capability to user entry points; the stablecoin market may form a dual-layer structure of universal coins and scenario-specific coins

Battle for Settlement Rights: Stablecoins enter real commercial flows; corporate financial management becomes a significant increment; machines start becoming new settlement主体

Rights to Reserve Earnings: Interest from reserve assets becomes the core income; value redistribution reshapes the competitive landscape; yield products evolve into financial infrastructure

Opportunities: Cross-border payments and settlements; corporate funds management; rights to reserve earnings; AI Agent settlement demand; clear regulations driving institutional participation

Risks: Regulatory and compliance risks; interest rate cuts compress reserve earnings; data bubble risks; changes in competitive landscape; systemic concentration risks

Outlook and Conclusion: The development direction evolves into a new dollar account system; winners need to master issuance, distribution, settlement, yields, and compliance capabilities

Stablecoins are transitioning from trading tools in the cryptocurrency market to the underlying interfaces for institutional payments, corporate fund management, and machine economies. Visa sees 2026 as the strategic year for stablecoins, emphasizing that cross-border payments, corporate treasury management, and merchant settlements are the main lines. Recently, Western Union announced the launch of a dollar payment stablecoin USDPT on Solana; Coinbase announced it would become the official fund deployer of USDC on Hyperliquid; Circle partnered with Kyriba to integrate USDC into the corporate treasury management platform already in use; Coinbase provides x402, Stripe participates in payment infrastructure, and AI Agent payments transition from narrative to cloud service product layers... These events collectively indicate that the stablecoin value chain is spilling over: from exchanges to corporate finance systems, from DeFi yield pools to merchant settlements, from manual click payments to machine automatic purchasing of APIs, data, computing power, and content.

I. Stablecoin Competition Shifts: From Trading Medium to Financial Infrastructure

In the past, the competition of stablecoins was often simply understood as “who has a larger market cap, who has stronger liquidity.” However, as use cases expand from exchanges to DeFi, payments, settlements, and corporate funds management, stablecoins are no longer just a dollar substitute in the cryptocurrency market but are gradually becoming the infrastructure of on-chain finance and global payment networks.

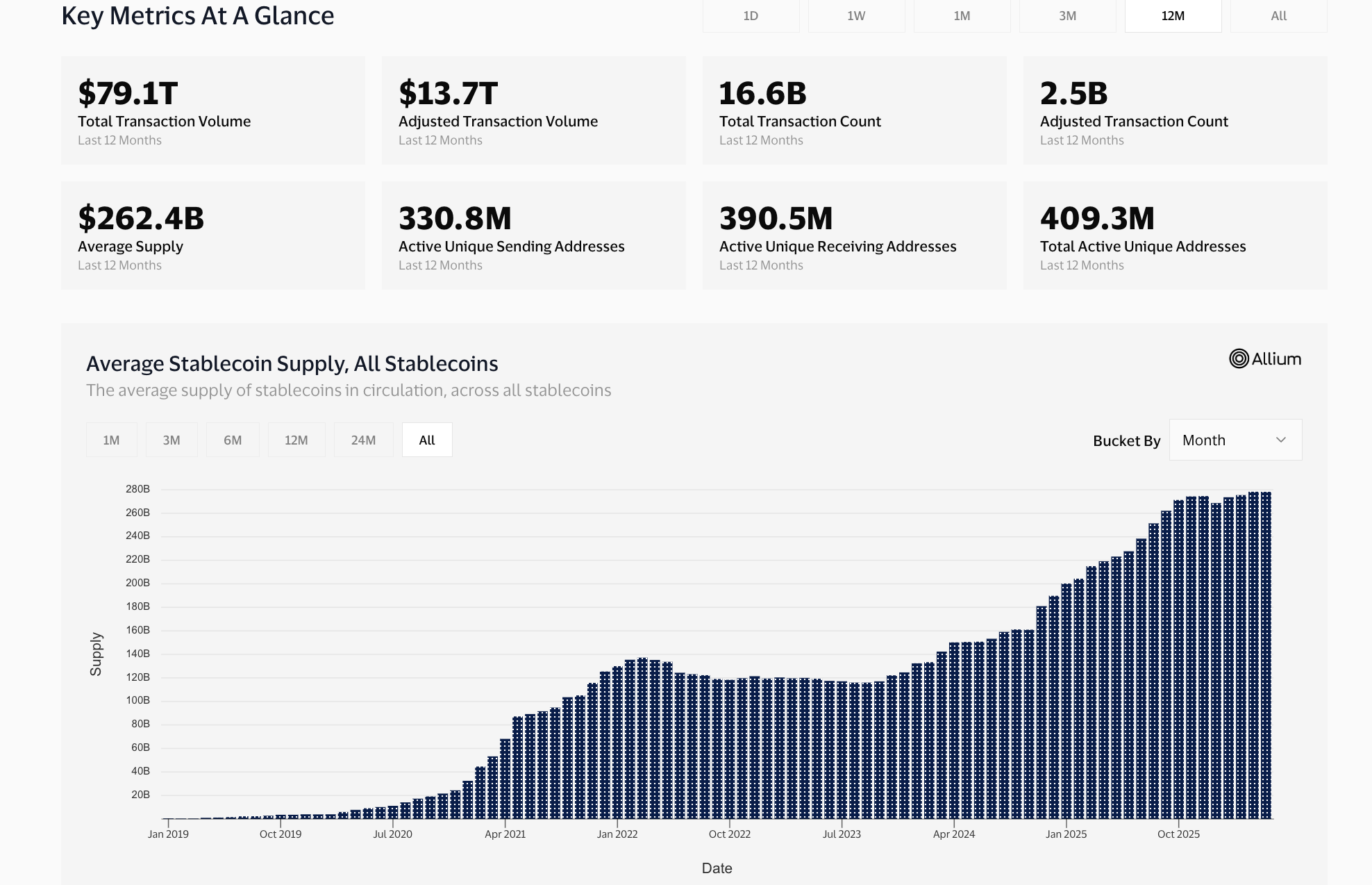

According to Visa Onchain Analytics, the current total supply of stablecoins has rapidly expanded from less than $1 billion in 2019 to nearly $280 billion today, more than doubling from approximately $120 billion at the end of 2023, setting a historical record. Over the past 12 months, the adjusted trading volume of stablecoins reached $13.7 trillion, with over 400 million active addresses, indicating that stablecoins are transitioning from liquidity tools within the cryptocurrency market to an important settlement infrastructure in the global digital economy.

Source: https://visaonchainanalytics.com

1.1 Evolution of Stablecoin Roles: From Trading Medium to Payment Settlement Network

The first stage of stablecoins is as a trading medium. It addresses dollar pricing, hedging, and liquidity issues in cryptocurrency trading. USDT has maintained long-term leadership due to the liquidity inertia formed by exchanges, market makers, OTC networks, and users in emerging markets. For many users, USDT is not just a token but an entry point to dollar liquidity.

The second stage is as on-chain financial collateral. With the development of DeFi lending, DEX, perpetual contracts, and RWA protocols, stablecoins begin to assume the roles of collateral, liquidation, market making, and the underlying assets of yield products. At this stage, stablecoins are not only “tradeable” but also need to be “composable.” USDC's importance increases during this stage because it is more readily accepted by institutions, compliant trading platforms, and DeFi protocols.

The third stage is the payment settlement, balance sheet, and machine payment phase. This stage is currently underway. Stablecoins no longer only serve crypto-native users but are entering cross-border remittances, merchant collections, platform revenue sharing, on-chain salaries, B2B settlements, and financial institution fund transfers. After traditional payment institutions enter, the logic of competition for stablecoins further changes: while the issuance scale is important, those who can have lower distribution costs, broader cash inflow and outflow networks, stronger compliance licenses, and more stable reserve management capabilities may gain higher profit margins in long-term competition.

This is why the stablecoin market is experiencing a “multi-center structure.” The advantage of USDT lies in global liquidity and transaction networks, while USDC’s advantage lies in compliance and institutional settlement; PayPal USD’s advantage lies in its payment brand and user network; USDe’s advantage is in bringing the revenue mechanism into the stable asset narrative, and USDS’s advantage stems from the years of accumulated on-chain collateral and governance system of MakerDAO/Sky. They are not competing in the same dimension of perfect homogeneity but are vying for dominance at different stages of the value chain.

1.2 Reconstruction of the Stablecoin Value Chain: Issuance, Distribution, Settlement, Yields, and Compliance

The value chain of stablecoins can be broken down into five layers:

The first layer is the issuance layer, responsible for mapping off-chain dollar assets to on-chain tokens, mainly represented by Tether, Circle, Paxos, etc.;

The second layer is the distribution layer, responsible for bringing stablecoins to users and enterprises, with the main participants being exchanges, payment companies, wallets, etc.;

The third layer is the settlement layer, responsible for the circulation of stablecoins within exchanges, public chains, payment networks, and merchant systems, with the main participants being public chains, trading platforms, merchant systems, AI Agent protocols, etc.;

The fourth layer is the yield layer, deciding how to allocate reserve yields, protocol revenues, market-making income, and derivative income, including government bond interest, DeFi yields, distribution income, protocol revenues, etc.;

The fifth layer is the compliance layer, determining whether the issuing entity can continue to operate, reach institutional users, and complete exchanges and settlements within different jurisdictions.

In the past, the market primarily focused on the issuance layer and market cap layer; in the future, greater attention is needed on the distribution layer, settlement layer, yield layer, and compliance layer. Stablecoin issuers, payment networks, enterprise software, cloud service providers, and public chain infrastructures are reorganizing value around these layers. Stablecoins are evolving from a singular product to a competition of multi-level financial infrastructures.

II. Restructuring of Issuance and Distribution: The Entry Points of Stablecoins Are Being Redefined

The competition for stablecoins appears to be a competition for issuance rights, but it is actually evolving into a joint competition for both issuance and distribution rights. As the barriers to stablecoin issuance decrease, it is no longer scarce to simply “be able to issue coins”; what is truly scarce is who can continually reach users, retain liquidity, and embed stablecoins into real transactions, payments, and application scenarios.

2.1 From Issuance Competition to Entry Competition

As the market matures, different types of institutions are beginning to construct stablecoin distribution systems around their respective strengths. The stablecoin market is also evolving from a single competition to a pattern of multiple distribution networks developing in parallel.

The first type is the crypto-native distribution network, represented by USDT. Its core advantage comes from the liquidity system composed of exchanges, market makers, wallets, and OTC networks. Whether it’s spot trading, contract margins, cross-border fund transfers, or on-chain asset allocations, USDT has become one of the most commonly used base assets. Especially in emerging markets and high-frequency trading scenarios, USDT essentially fulfills the role of a digital dollar circulation medium. Its advantage does not lie in compliance, but in its strong accessibility and liquidity depth.

The second type is the institutional and corporate distribution network, represented by USDC. In comparison to USDT, USDC's development path places greater emphasis on the institutional market. Circle not only issues stablecoins but also actively promotes USDC's entry into banks, payment institutions, financial technology platforms, and corporate treasury management systems. Taking the cooperation between Circle and Kyriba as an example, USDC has been incorporated into corporate funds allocation, cash management, and liquidity management processes. For enterprises, the value of stablecoins is no longer just as a trading tool but as a new funding management infrastructure. As more and more companies begin to explore on-chain settlement and cross-border funds management, institutional networks are expected to become important sources of stablecoin growth.

The third type is the payment and application distribution network. USDPT launched by Western Union, PYUSD launched by PayPal, and PYUSDx promoted by MoonPay and M0 all belong to this direction. Unlike traditional crypto organizations, these participants have established payment channels, brand recognition, and user bases. Their goal is not primarily to enter DeFi but to integrate stablecoins into existing payment systems and application ecosystems. For Western Union, stablecoins can become a new carrier for global remittance networks; for PayPal, stablecoins can further strengthen its digital payment ecosystem. As application platforms begin to have their entry points for stablecoins, the competitive boundaries of stablecoins are also expanding from the financial market to the internet application layer.

These different types of distribution networks are not in a completely competitive relationship, but rather resemble a competition for different liquidity flows and user groups. The crypto-native network connects trading liquidity, the institutional network connects corporate fund flows, while the payment and application networks connect consumption scenarios and daily payment demands. The future competition in the stablecoin market will increasingly reflect competition between different networks.

2.2 The Stablecoin Market May Evolve Towards a Dual-Layer Structure

From a long-term development perspective, the stablecoin market is unlikely to evolve into a single stablecoin monopoly but may form a dual-layer structure similar to internet infrastructure.

The first layer is the universal stablecoin layer. Its main function is to bear open market liquidity, cross-platform transfers, and global settlement. Users, institutions, and protocols need an asset with wide acceptance and high liquidity as a medium of value exchange. Currently, USDT and USDC are the most likely candidates to continue to fulfill this role. They possess large circulation scales, mature redemption mechanisms, and extensive ecological support, thus able to continue acting as the foundational layer of the on-chain dollar system.

The second layer is the application-specific stablecoin layer. These stablecoins do not seek to become universal assets in the entire market but instead serve specific ecosystems and scenarios. For example, payment platforms can issue payment stablecoins; gaming ecosystems can issue gaming stablecoins; AI platforms can issue stablecoins for Agent payments; and enterprises may issue stablecoins for internal settlements and funds management. They emphasize scenario binding, user operation, and closed commercial models rather than overall market liquidity.

The logic behind this trend is very similar to the development of the internet. The internet ultimately formed a structure coexisting with open protocols and application platforms; the stablecoin market may also form a pattern of coexistence between universal stablecoins and scenario-specific stablecoins. Universal stablecoins are responsible for value circulation and cross-platform settlements, while application stablecoins are responsible for meeting specific scenario demands, together forming the future on-chain dollar system.

Thus, competition for issuance rights may eventually evolve into infrastructure competition. In the future, the most valuable participants may not be singular stablecoin issuers but rather those able to connect universal stablecoins with application stablecoins and provide issuance, redemption, settlement, liquidity management, cross-chain interoperability, and compliance services at the network level. Whoever can become a connector between different stablecoins is more likely to occupy a core position in the next stage of competition.

III. Battle for Settlement Rights: Payment Networks, Corporate Treasury, and AI Agents Entering Simultaneously

Stablecoins genuinely become financial infrastructure not based on their ability to transfer on-chain, but rather their capability to enter high-frequency, high-value, low-friction real settlement scenarios. As stablecoins gradually step out of the cryptocurrency market, their competition focus is shifting from liquidity to settlement networks. Whoever can master more real payment scenarios has a greater opportunity to become an important part of the next generation of dollar infrastructure.

3.1 Payment Network Battle: Stablecoins Begin Entering Real Commercial Flow

Cross-border payments have long been regarded as one of the most accessible scenarios for stablecoins. Compared to traditional banking systems, stablecoins can achieve 24/7 transfers, faster arrivals, and lower cross-border friction, hence more payment institutions are integrating them into their infrastructure.

Visa emphasizes that the core driving force behind institutions adopting stablecoins is not crypto trading but rather cross-border fund flows, merchant settlements, corporate payments, and improved operational efficiency. Western Union's launch of USDPT should be understood within this framework. For Western Union, its true value is not merely issuing a new stablecoin but using its globally covered agent network, cash inflow and outflow channels, and remittance scenarios to embed stablecoins into existing payment systems. If a deep integration of stablecoins with traditional remittance networks can be achieved, USDPT will not only compete for on-chain users but also the global cross-border payment and remittance market.

In the long run, the competition for stablecoin payment networks essentially revolves around capturing real money flow. Those who can connect more merchants, payment institutions, and cross-border funding needs will have a better chance of mastering the next phase of settlement rights.

3.2 Corporate Treasury: Stablecoins are Entering Corporate Balance Sheets

Compared to consumer payments, corporate funds management may represent a larger market. The collaboration between Circle and Kyriba indicates that stablecoins are gradually evolving from trading tools to corporate treasury infrastructure. For CFOs and finance teams, they do not care much about on-chain narratives but are more focused on efficiency in fund allocation, cash utilization, auditing compliance, and liquidity management capabilities.

Traditional multinational corporations often face challenges such as banking hours, lengthy fund arrival periods, and multi-layer approvals when conducting cross-border fund transfers. Stablecoins provide another option: companies can achieve 24/7 fund transfers, more real-time liquidity management, and more transparent tracking of funds.

This means that the distribution channels for stablecoins are changing. In the past, stablecoins were primarily accessed by users through exchanges, wallets, and DeFi protocols; in the future, they may also enter corporate daily operating processes through ERP, financial management systems, and treasury platforms. If this trend continues, corporate fund systems are anticipated to become one of the most significant sources of stablecoin demand following the cryptocurrency trading market.

3.3 AI Agent Payment: Machines Start to Become the New Settlement Entities

In addition to human and corporate participants, a third potential settlement entity is emerging—AI Agents.

AWS Bedrock AgentCore Payments supports AI agents to use stablecoins for payments, Coinbase launched the x402 protocol, and Stripe is also participating in related payment infrastructure development. The core logic of x402 is to enable machines to perform payment actions in a human-like manner: when the server returns HTTP 402 Payment Required, the Agent can automatically complete payment according to preset rules and obtain API, data, content, or computing services.

The significant importance of this mechanism lies not in the current transaction scale but in standardizing “machine payments” as a protocol-level capability for the first time. Machine payments are fundamentally different from traditional payments. Human payment relies on manual decisions, while AI Agents may need to automatically purchase an API call, a segment of real-time data, content access, or short-term computing resources. These types of scenarios often feature high frequency, small amounts, automation, and programmability, while stablecoins inherently possess advantages in 24/7 settlements, on-chain verifiability, and programmatic control.

Of course, AI Agent payments are still in a very early stage. Data collected by IOSG shows that x402 is currently mainly focused on crypto-native and AI-native services, and the coverage of merchants remains limited, while some transaction activities may also be incentivized. Cryptorefills supports AI Agents to use USDC to purchase gift cards, eSIMs, and mobile top-ups, which are one of the few real-world cases already in use, but there is still a long way to go before forming a large-scale commercial network.

IV. Rights to Reserve Earnings: The Core Profit Pool of the Stablecoin Business Model

If issuance rights determine who can create on-chain dollars, and settlement rights determine who can control money flows, then the rights to reserve earnings dictate who can acquire the most stable and sustainable profit sources within the stablecoin system. Historically, the market has focused more on the circulation scale of stablecoins but has overlooked the underlying earnings structure. As stablecoins gradually evolve from trading tools to financial infrastructure, the allocation rights concerning earnings generated from reserve assets are becoming the core focus of the new round of competition.

4.1 Reserve Assets: The Most Important Source of Profit for Stablecoins

The most crucial aspect of the stablecoin business model is the interest income generated from reserve assets. When users hold fiat-backed stablecoins like USDT and USDC, the issuers usually allocate the corresponding reserve funds to low-risk assets such as U.S. Treasury bonds, reverse repos, money market funds, and bank deposits. Users receive a price-stable digital dollar, while issuers receive the earnings generated from these reserve assets.

In the zero-interest rate era, this model’s profitability was not prominent. However, with U.S. interest rates remaining high, reserve earnings are gradually becoming one of the most important income sources in the stablecoin industry. For stablecoins with circulation scales of hundreds of billions, even a few percentage points of annual yield can create considerable cash flow.

This is why stablecoin competition is increasingly gaining attention from traditional financial institutions. Compared to trading platforms that rely on market activity, the reserve earnings model boasts stronger sustainability and predictability. As long as stablecoins can maintain circulation scales, issuers can continuously obtain earnings. From a business model perspective, stablecoins are essentially becoming a digitized balance sheet business: users provide funds, issuers manage reserve assets, and earn the interest spread.

4.2 Earnings Distribution: Stablecoin Competition is Entering the Value Redistribution Stage

As reserve earnings scale expands, the market is beginning to focus on another question: who should these earnings rightfully belong to? In the traditional model, most of the earnings are retained by the issuers. Users gain price stability and liquidity, while the interest generated from reserve assets primarily belongs to the issuing institutions. This model has helped USDT, USDC, and similar projects establish sustainable profit systems and has facilitated the rapid development of the industry.

However, as the market matures, more and more participants are beginning to attempt to redistribute this portion of earnings.

One direction is yield-bearing stablecoins. Users holding stablecoins can directly share a portion of the earnings generated from reserve assets. Products like sUSDD and sUSDe belong to this concept. Compared to traditional stablecoins, yield-bearing stablecoins resemble on-chain money market funds, maintaining relatively stable value anchoring while returning earnings to holders.

Another direction is to reinvest reserve earnings into ecosystem expansion. For instance, some stablecoin issuers will utilize reserve earnings to subsidize payment networks, provide liquidity incentives, or promote on-chain application growth to enhance the distribution and settlement capabilities of stablecoins. The transfer networks constructed around USDT within the TRON ecosystem, as well as new stablecoin infrastructures like Plasma attempting to attract users through lower-cost settlement experiences, fundamentally embody the approach of transforming reserve earnings into network growth.

This shift indicates that stablecoin competition is transitioning from competition based on circulation scale to competition focused on earnings distribution. In the future, when users choose a particular stablecoin, they will not only consider its safety and liquidity but also how much earnings they can gain and whether they can participate in value sharing.

4.3 From Yield Products to Financial Infrastructure

The significance of rights to reserve earnings lies not only in generating profits but also in their potential to become the underlying asset for constructing new financial infrastructure. In recent years, more and more DeFi protocols have started to repackage and redistribute stablecoin yields. For example, Pendle splits future yields into PT and YT, allowing users to trade principal and earnings rights separately; lending protocols allow yield assets to be used as collateral for further financing; structured products and yield aggregators continue to amplify the application scenarios of stablecoin yields.

Based on yield-bearing stablecoins, the market is forming a new layer of yield assets. Stablecoins are no longer just payment tools or value storage tools but are beginning to take on functions similar to short-term Treasury bonds, money market funds, or even cash management products. For users, their appeal comes from the combination of stability and yield; for protocols, their value lies in being significant underlying assets for lending, derivatives, and yield trading markets; for issuers, this means higher fund retention rates and stronger ecological stickiness.

In the long run, rights to reserve earnings may be more strategically valuable than issuance rights themselves. Issuing stablecoins merely creates a form of digital dollar, while mastering rights to reserve earnings means controlling the ability to continuously generate cash flow from the entire on-chain dollar system, thereby becoming one of the most critical competitive resources in the next generation of on-chain financial systems.

V. Opportunities and Risks: The Stablecoin Value Chain is Reshaping the Global Dollar System

After more than a decade of development, stablecoins have gradually evolved from trading tools in the cryptocurrency market to crucial infrastructures connecting on-chain finance and the real world. From payment settlements to corporate fund management, from reserve assets to AI Agent payments, stablecoins are continuously expanding their application boundaries. However, despite the optimistic expectations of the market, the stablecoin industry remains in its early stages, facing significant challenges such as regulation, competition, and business models while also holding vast growth potential.

5.1 Opportunities: Stablecoins are Becoming Next-Generation Dollar Infrastructure

The biggest opportunity for stablecoins lies in their potential to become the dollar infrastructure of the global digital economy era.

Payment and settlement markets still possess substantial growth potential. The traditional cross-border payment system has long been plagued by high costs, low efficiency, and extended settlement cycles, while stablecoins have inherent advantages such as 24/7 operation, global reach, and programmable settlements. As institutions such as Visa, Mastercard, PayPal, Stripe, and Western Union continue to lay out stablecoin infrastructure, stablecoins are gradually entering mainstream payment systems from the cryptocurrency market.

Corporate funds management may become one of the most significant incremental markets in the future. The collaboration between Circle and Kyriba indicates that stablecoins are beginning to enter corporate funds allocation, cash management, and cross-border settlement scenarios. For multinational companies, stablecoins are not just payment tools but have the opportunity to become new funding management infrastructures.

Reserve earnings are driving innovation in on-chain financial products. The development of yield-bearing stablecoins enables stablecoins to possess both payment attributes and yield attributes. A borrowing, yield splitting, structured products, and asset management market formed around reserve earnings is constructing a new layer of yield assets on-chain. This suggests that stablecoins may not just be a digital mapping of dollars but could also become significant underlying assets in the global digital asset market.

New scenarios such as AI Agent payments are opening new demand spaces. When machines start autonomously purchasing APIs, data, content, or computing resources, stablecoins inherently have advantages in programmable payments and real-time settlements. Although this market is still in a very early stage, its long-term potential merits attention.

Compliance is transitioning from a limiting factor to a growth driver. Since 2025, the U.S. Congress has been continuously advancing digital asset-related legislation such as the GENIUS Act and the CLARITY Act. Regardless of how the final details of the bills adjust, their common significance lies in providing clearer regulatory expectations for the stablecoin industry. The establishment of a compliance framework indicates not only increased regulatory constraints but also that stablecoins are receiving a “license” to enter the mainstream financial system.

In the long run, the greatest opportunity for stablecoins is not to replace traditional finance but to become a new infrastructure layer connecting traditional finance and on-chain finance.

5.2 Risks: Attention to Real Constraints Beyond Growth Narratives

Although the long-term outlook is broad, the development of the stablecoin industry is not linear, and its risks should not be overlooked.

Regulatory and compliance risks: Stablecoins inherently link fiat currency systems, payment networks, and capital markets, placing them at the core of regulatory attention. As bills like the GENIUS Act and CLARITY Act progress, the future stablecoin market may gradually shift from its current dominance by crypto-native institutions to a market jointly participated in by banks, payment institutions, and large fintech companies, thus constricting the survival space of some small and medium issuers and increasing market concentration, with some projects likely exiting the market for failing to meet new compliance requirements.

Yield model risks: The current profitability of mainstream stablecoins heavily benefits from the high-interest environment in the U.S. When reserve assets can provide higher yields, issuers can earn considerable interest income. However, if the future enters a rate-cutting cycle, reserve earnings may decline significantly, placing pressure on business models that rely on high yields. This impact is likely to be more pronounced for yield-bearing stablecoins.

Data bubble risks: Stablecoin trading volumes have rapidly increased in recent years, but on-chain trading volumes do not necessarily equate to growth in real economic activity. A significant portion of trading may stem from arbitrage, market making, bot activities, and funds cycling between protocols. Rather than the trading volume itself, the real scales of payments, corporate adoption, and long-term user growth are better indicators of the industry's actual development level. If the market overly relies on short-term data narratives, it may overestimate the actual penetration speed of stablecoins.

Changes in competitive landscape: The stablecoin market has historically been dominated by crypto-native institutions, but in the future, banks, payment companies, internet platforms, and fintech firms may all become significant participants. As the barriers to issuance lower, competition may evolve from stablecoin-to-stablecoin competition to ecosystem competition among payment networks, financial institutions, and tech platforms. For existing issuers, maintaining liquidity advantages and network effects will become a long-term challenge.

Systemic concentration risks: Currently, market liquidity and user scales are still highly concentrated among a few leading stablecoins. Should any primary issuer, reserve asset, or key infrastructure face problems, it could trigger a domino effect across the entire industry. Hence, as the industry continues to expand, risk diversification and infrastructure resilience construction will become increasingly important.

In a sense, the stablecoin industry has already entered a new phase of “regulation-driven growth.” In the past, the liquidity and network effects determined the competitive landscape; in the future, what truly deserves attention is not just who issues more stablecoins but also who can continually connect real money flows, real users, and real economic activities within regulatory frameworks. Only by simultaneously mastering issuance, settlement, yield, and compliance capabilities can one establish a genuine long-term advantage in the next phase of competition.

VI. Outlook and Conclusion: Where is the Endgame for Stablecoins

In recent years, the most frequently mentioned scenarios in discussions about stablecoins have been trading, cross-border payments, and remittances. These scenarios have indeed driven the rapid growth of stablecoins, but from a longer-term perspective, they may represent only the first steps in the development of stablecoins rather than their final form. A question worth pondering is: if all dollars could circulate on-chain in the future, who would stablecoins be truly competing against? The answer may not be another stablecoin but today’s bank account system. For the past century, the issuance, circulation, and settlement of dollars have primarily relied on commercial bank networks. Bank accounts fulfill the functions of storing funds, payment settlement, earnings management, and credit creation. Stablecoins are gradually replicating and reconstructing this system: issuers are responsible for creating on-chain dollars, payment networks facilitate value transfers, yield-bearing stablecoins undertake cash management functions, and on-chain lending protocols are beginning to assume part of the credit mediation function.

From this perspective, the direction of stablecoin development may not be to become a new payment tool but to evolve into a new dollar account system. What users hold will no longer just be a stablecoin balance, but an on-chain dollar account that possesses payment, yield, lending, and asset management capabilities. Meanwhile, the gradual improvement of regulatory frameworks will also accelerate this process. The significance of legislative advancement lies not only in regulating industry development but also in promoting the transition of stablecoins from crypto-native markets to mainstream financial systems. In the coming years, banks, payment institutions, internet platforms, and asset management companies may all become important participants in the stablecoin market.

The endgame of stablecoin competition may not be for one type of stablecoin to replace another, but rather to form a layered structure similar to the banking system: a few foundational currency layers with regulatory licenses and reserve capabilities, alongside a large number of scenario-specific distribution layers aimed at payments, corporate treasury, AI Agents, and financial applications. True competition in the future will no longer just be about issuance rights, but rather who can command user entry points, settlement networks, and the distribution of reserve earnings.

About Us

Hotcoin Research, as the core research institution of Hotcoin Exchange, is committed to transforming professional analysis into your practical tool. We analyze market trends for you through the "Weekly Insights" and "In-depth Reports"; leveraging the exclusive column “Hotcoin Selections” (dual screening by AI and experts), we identify potential assets for you to lower trial-and-error costs. Each week, our researchers also engage face-to-face through live broadcasts, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate the cycles and seize value opportunities in Web3.

Risk Warning

The cryptocurrency market is highly volatile, and investing itself carries risks. We strongly advise investors to make investments based on a complete understanding of these risks and under a strict risk management framework to ensure the safety of funds.

Website: https://www.hotcoin.com/zh_CN/learn/index/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。