Funeral expenses lost in cryptocurrency 36 million! Nearly half of the funeral companies in South Korea are insolvent, and regulatory vacuum has led to a disaster.

Written by: Korea Economic Daily

Translation: AididiaoJP, Foresight News

Translator's note: The South Korean funeral industry heavily relies on prepaid mutual assistance programs, similar to insurance or installment financial products. Companies raise customer funds in advance (often through installments) to secure future funeral services and prices.By 2026, approximately 10 million people (nearly 20% of South Koreans) are expected to join such programs, with a market size of about 11 trillion won. Customers sign contracts with mutual aid companies (or funeral service providers) for specific prepaid methods, paying in installments (usually around 10 years, 20,000-30,000 won per month) or a lump sum. This secures specific services (such as body handling, ceremonies, coffins, burials, etc.) and avoids future price increases.

Image source: Korea Economic Daily

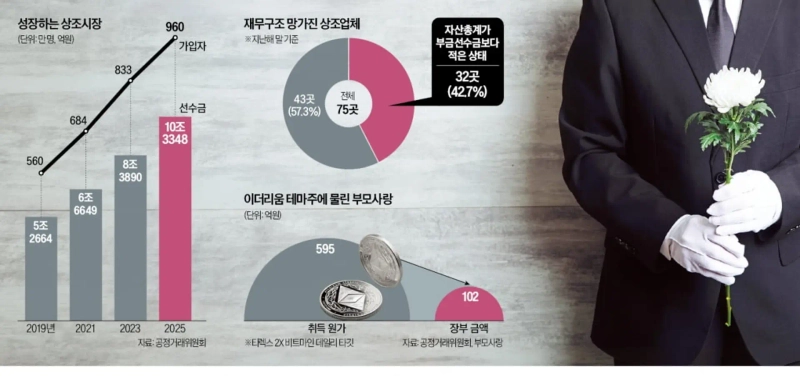

The Korea Economic Daily found that nearly half of the funeral service companies in South Korea have total assets less than the prepaid funds owed to customers. Losses from cryptocurrency-related investments and poor asset management (including operators treating the company as a private treasury for major shareholders) are the main reasons.

A review of the 2025 audit report for 75 national funeral service companies released by the Korea Economic Daily on May 18 showed that 32 companies (42.7%) had total assets lower than their customers' prepaid balances. This means that if all customers request to cancel contracts simultaneously, these companies would not have enough funds for refunds.

The reduction in assets highlights the severe moral hazard in the industry. The seventh-largest operator, Bumo Sarang, invested 59.5 billion won (about 43 million USD) in a leveraged ETF tracking Bitmine (Ethereum-themed stock) that offers double daily returns, recording a loss of 49.3 billion won (about 35.6 million USD) at book value.

The funeral service business is similar to insurance and other financial sectors because it raises and manages customer funds over the long term. However, prepaid funeral operators face almost no regulation regarding financial soundness and management of customer prepaid funds. They are classified legally as prepaid installment transaction businesses, governed by the Fair Trade Commission rather than financial regulatory authorities. Experts say the market size has grown to about 10 trillion won (about 7.2 billion USD) and should be subject to appropriate financial regulation.

Regulatory vacuum leads to "zombie" funeral companies surviving by consuming customer funds

No solvency or asset management regulation, nor restrictions on lending to major shareholders.

Last year, Bumo Sarang invested 59.5 billion won (about 43 million USD) in a leveraged ETF linked to Bitmine. With the cryptocurrency market crash, the product's book value fell to 10.2 billion won (about 7.4 million USD) by the end of the year.

Mideumui Gajok recorded a net loss of 500 million won (about 361,000 USD) last year, accumulating losses of over 2.3 billion won (about 1.7 million USD) over the past 18 years. In the past two years, customers paid only 2.39 million won (about 1,730 USD) in prepaid funds while incurring expenses of 93 million won (about 67,000 USD) due to contract cancellations.

Regulatory vacuum formed because they are not classified as financial companies

As of May 18, according to the Fair Trade Commission, regulation on the management of prepaid funds and financial soundness of funeral service companies effectively does not exist. Unlike insurance companies that must meet solvency ratio requirements set by financial regulatory authorities, funeral service operators have no capital adequacy ratio standard and no provisions allowing authorities to compel major shareholders to inject capital. The role of the Fair Trade Commission is mainly limited to publishing financial indicators such as solvency and liability ratios on its website.

If an insurance company's financial situation deteriorates to the point of being as severe as Mideumui Gajok's, the Financial Services Commission can require it to take corrective measures, including injecting capital. If the company fails to comply, the regulatory authority can designate it as a problematic financial institution and replace the major shareholder.

Banks must comply with higher capital ratio requirements during investments in high-risk assets, as mandated by the Bank for International Settlements standards. Funeral service operators lack similar regulations. Even if they manage customer funds, the only requirement is to retain 50% of the prepaid balance. If they join a mutual aid association, pay fees, and obtain payment guarantees, they can even operate with more than 50% of the funds.

The absence of solvency and asset management rules stems from this industry's legal status outside the financial sector. In 2010, the government amended the Installment Transactions Act to classify funeral service operators as prepaid installment transaction businesses. As a result, regulatory authority was shifted from financial authorities to the Fair Trade Commission.

Another long-standing issue is the lack of restrictions on credit support for major shareholders, leading some funeral service companies to effectively become the owner's private treasury. Industry insiders say this practice is common not only in small companies but also large operators routinely lend customer funds to major shareholders and related parties. Sono Station, ranked third in prepaid balances, holds 1.4531 trillion won (about 1.05 billion USD) and was scrutinized in 2024 for providing 50 billion won (about 36.1 million USD) to its affiliated company Sono International for the acquisition of T'way Air.

In some small operators, loans to major shareholders and related parties even exceed the customer prepaid balance. Hanyang Sangjo, which has a prepaid balance of 570 million won (about 412,000 USD), lent 2.2 billion won (about 1.6 million USD) to its CEO. Jeju Ilchul Sangjo, with a prepaid balance of 450 million won (about 325,000 USD), lent 1.6 billion won (about 1.2 million USD) to its major shareholder.

Some companies cannot refund customers requesting to cancel contracts

The funeral service industry argues that a company cannot be labeled as distressed solely due to high debt ratios or negative net assets. The prepaid balances are recorded as liabilities and are only recognized as revenue when actual services such as funerals are provided. Prior to that, losses accumulate and erode equity, according to the industry.

Some operators have achieved good performance through diversified investments in bonds, real estate, infrastructure, and corporate finance, including The-K Yedaham operated by the Korean Teachers Credit Union. However, warning signals are increasing among small companies. The Daeno Welfare Foundation had total assets of 40.7 billion won (about 29.4 million USD) at the end of last year, below its prepaid balance of 70.6 billion won (about 51 million USD), rendering it unable to refund when customers requested to cancel contracts.

As of March, the total unpaid cancellation claims reached 1.3 billion won (about 93,900 USD). The Daeno Welfare Foundation stated it plans to pay canceled customers through additional borrowing. Bumo Sarang officials said these losses are short-term unrealized losses caused by global market fluctuations and are manageable within the company's financial buffer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。