While dealing with the Iran war, Trump placed 3,642 orders in his US stock account.

This is Trump’s Q1.

Meanwhile, he was also handling tariffs, negotiating trade agreements, and signing executive orders. Last Thursday, the US government's Office of Government Ethics released a 113-page document on its official website. A handwritten line on the cover stated that the declarant paid a late fee. The most closely watched transaction disclosure in the world has finally been published.

In the same week, the US Congress was advancing a bill to prohibit officials from trading stocks. According to Axios, the relevant proposal has been co-sponsored by more than 120 members of Congress, with versions in both houses, and a poll support rate of over 70%.

However, the biggest loophole in this bill is that it does not apply to the president.

The White House's response is also familiar. The president's assets are managed by his children, and transactions are executed by account managers, fully complying with all requirements of the US officials' stock trading disclosure law, with no conflicts of interest. This statement has been repeated many times over the past year. Whenever new details emerge, it gets stated again. After many repetitions, it has become information in itself.

A person who can influence tariffs, trade, industry subsidies, cryptocurrency regulation, and market sentiment, while maintaining a large US stock account.

The disclosure document states that the transactions are compliant. What the market really wants to see is what he bought, how much he earned, and whether these stocks align with his policy direction.

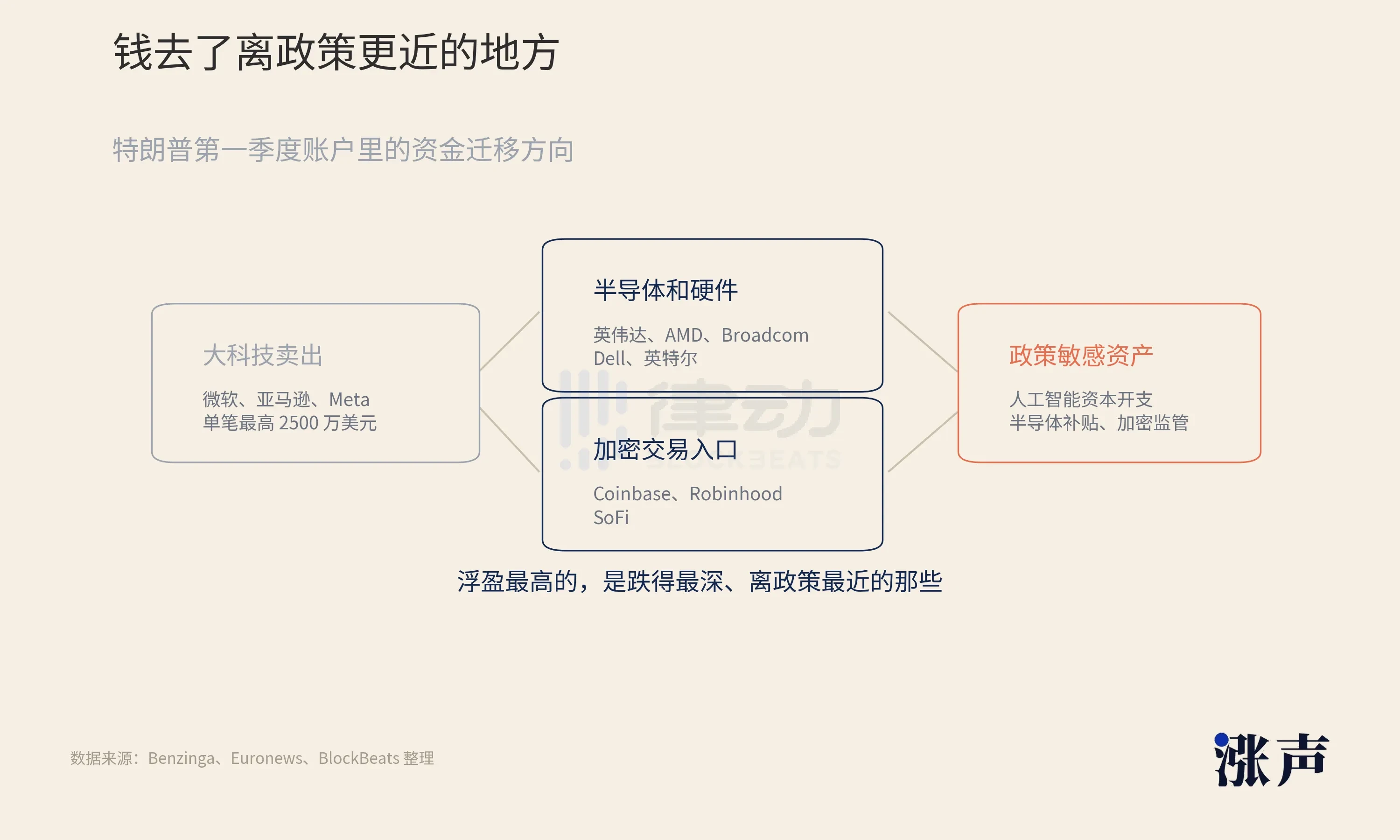

Money moving out of big tech to places closer to policy

Federal disclosure rules only require a range of amounts, not exact prices or actual gains and losses.

Benzinga estimated, after cross-referencing Trump’s scanned documents page by page, that Nvidia was bought for about $2.4 million to $6.6 million, Microsoft for about $2.4 million to $8.1 million, Amazon for about $2.5 million to $8.3 million, and Oracle for about $2.2 million to $10.6 million.

Big tech had another set of moves.

Microsoft, Amazon, and Meta had the largest sell order amounts, with individual orders reaching up to $25 million. In the same batch of companies, holdings were established in the early part of the first quarter, with sales occurring in the latter part, and buying and selling alternated on the bills. Money moved out of big tech into the semiconductor and AI hardware chain.

Nvidia, AMD, Broadcom, Dell, and Intel are among the most frequently appearing names in this chain. Also included are Coinbase, Robinhood, and SoFi. The timing of establishing positions coincided with discussions about the federal Bitcoin reserve and the initiation of the "Trump Account" retirement plan.

Euronews reported that if the positions were maintained until the disclosure date, targets with paper profits exceeding 100% included AMD, Intel, Marvell, SanDisk, Seagate, and others.

The ones with the highest paper profits are those that have fallen the furthest and are closest to policy.

In this group of transactions, big tech remains the foundation. Microsoft provides enterprise software and cloud services; Amazon has cloud computing and advertising; Meta has advertising cash flow and AI recommendation efficiency; Oracle has databases and cloud infrastructure. They are the easiest names for US stock funds to return to risk assets.

The incremental changes are within the hardware chain.

Nvidia is the center of graphics processor supply; AMD is the second option; Broadcom makes custom chips and data center networks; Dell delivers AI server systems. For every graphics processor that cloud vendors buy, one more order comes from companies in this chain. The money from big tech is betting on the valuation logic of platform companies, while the money from the hardware chain is betting on the first batch of people to receive cash when AI capital expenditures are realized.

In contrast, Dell is the cleanest case in this timeline.

On February 10, 2026, the Trump account established a position in Dell, with an amount ranging from $1 million to $5 million. On May 8, Trump publicly praised Dell's hardware products at a White House event, and Dell's stock rose by about 12% that day. Six days later, the transaction was disclosed.

There is also a background on this same line. The Dell family had previously promised to invest $6.25 billion into the "Trump Account" retirement plan. Each segment looked legal when viewed separately, confirmed by the US officials' stock trading disclosure law.

Moreover, no one is under investigation.

This is also where the Trump account differs from ordinary politicians' trades. In a regular official's stock disclosure, readers look for whether they have aligned with a policy direction. Trump's disclosure adds another layer. He is not just betting from the sidelines of the market; his public activities, policy projects, and industry relationships themselves also become part of market pricing.

The line with Dell is short and complete.

The account buys first, then the White House speaks, the company’s stock rises on that day, and family money enters Trump’s policy projects. It does not need to prove that any segment is illegal; it is enough for the market to treat it as a sample of a politician's trade.

Intel bought into a "US state enterprise"

There is a transaction in the US stock account that is not in Trump's personal account.

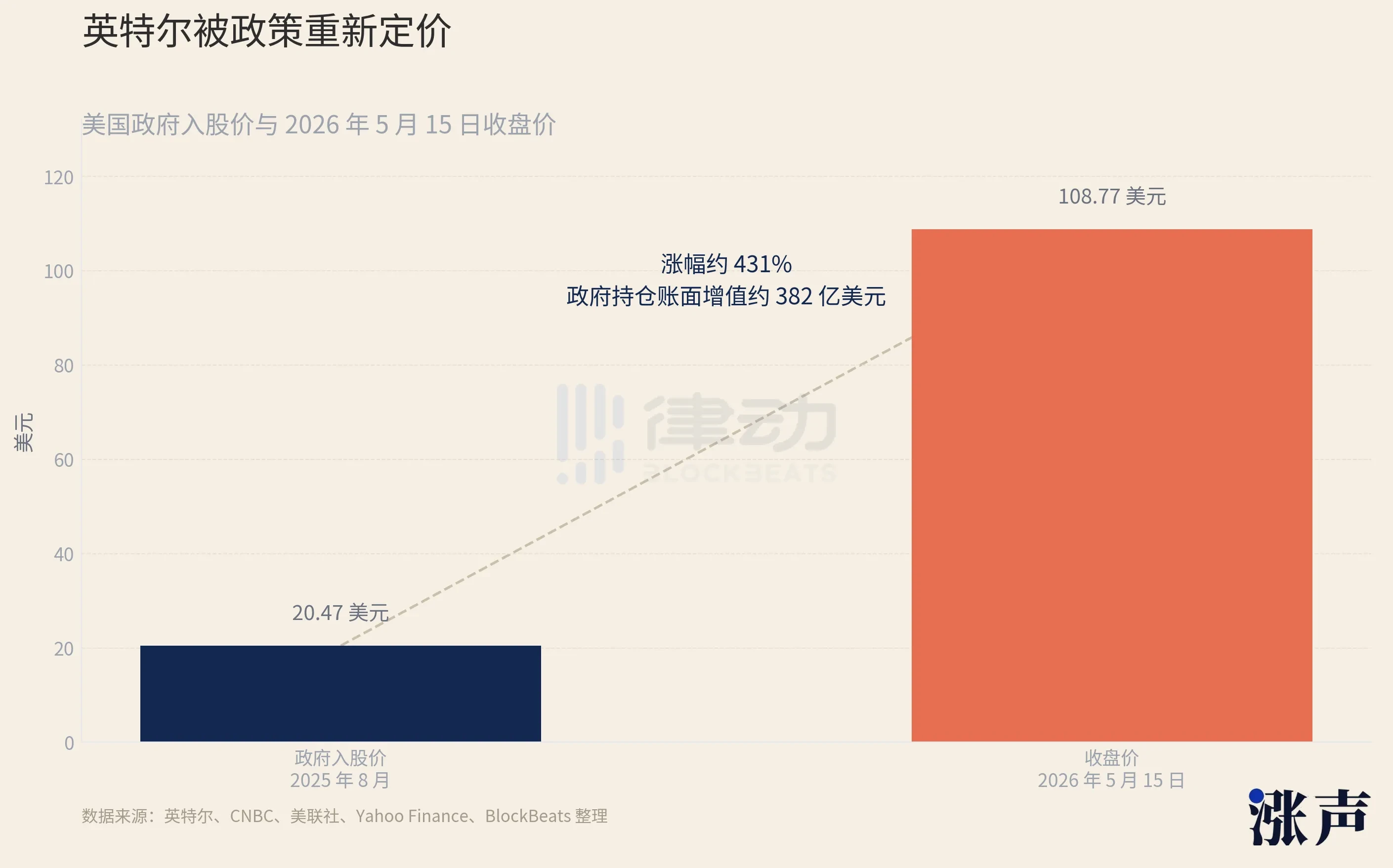

In August 2025, the CHIPS and Science Act still had $5.7 billion in subsidies for Intel that had not been disbursed, plus $3.2 billion for the “safe harbor” project, totaling $8.9 billion.

The Trump administration converted this subsidy into equity. 433.3 million shares of Intel common stock, at $20.47 per share, acquiring about 9.9% equity. The US government became Intel's largest shareholder, classified officially as a "passive investor," without requesting a board seat.

This was a clause not included in the design of the CHIPS and Science Act. The subsidy was intentionally designed as a non-equity form for a clear purpose: the government would give out money without intervening in corporate governance. Receiving money is allowed, but holding shares is not, as holding shares would give the government financial interests in the future of the company, making it difficult to maintain neutrality.

Trump changed the rules.

Before this transaction occurred, Intel's stock price had languished below $20 for nearly a year, with revenue continuously declining and process technology lagging; the market judged it to be a company that had lost competitiveness. After the government stepped in, a new variable entered Intel’s valuation—the US government would not let this company fail.

This judgment does not fit into cash flow discount models, but the market will price it.

Chip manufacturing is a national strategy; the largest shareholder would not sit idly by, and Intel's tail risk was cut off from this moment forward. Trump's personal account's position in Intel appeared in early March 2026, six months after the government completed its acquisition.

At this time, Intel had exceeded earnings expectations for six consecutive quarters, driven by demand for AI inference, with orders for central processing units recovering. Rumors about Apple’s contract manufacturing continued to grow, and the fundamental repair story began to make sense. By May 15, 2026, Intel closed at $108.77. From the government’s purchase price of $20.47, the increase was approximately 431%, and the government’s stake had appreciated by about $38.2 billion.

First using taxpayers' money as a safety net, then following up with personal funds. This statement sounds harsh, but the sensitivity of the Intel case lies here.

Public information already exists, and Trump’s personal account buying Intel may not actually involve any non-public information. The issue is that when the government has already pushed a company to the center of national strategy, and the president’s personal account appears next to the same company, the market finds it hard to see it as a simple investment.

The community calls Intel a "US state enterprise," and behind the joke is a realistic judgment.

It is different from traditional state-owned enterprises, but when the government buys a large stake with $8.9 billion, Intel is placed within the policy framework of American manufacturing, supply chain security, AI computing power sovereignty, and semiconductor subsidies. Investors are buying not only Intel's next quarter profits but also the expectation that the US government will not let it exit.

This is also why Intel is more important than Dell.

Dell represents a clear timeline for an individual stock.

Intel represents an institutional timeline. It commences with the transition from subsidy to equity, linking industrial policy, government financial interests, personal holdings, and market pricing.

In the past few years, the market has tracked the Pelosi family’s trades with a consistent logic: policymakers knew in advance what was happening, and thus bought early. That is a one-way causal relationship—policy generates information, information creates trading opportunities, and officials act ahead.

Intel is different. Here, the key has surpassed simply knowing details of a policy in advance; the government itself directly becomes part of the trade. Subsidies, equity, manufacturing return, AI computing power, personal accounts, all fall under the same company.

This case explains why the batch of AI hardware and semiconductor assets in the Trump account is important.

Nvidia and AMD are computing chips; Broadcom is for networking and custom chips; Dell is for entirety of servers; Intel is the domestic manufacturing bolstered personally by the US government.

These targets may seem dispersed but point in the same direction. The US market is buying AI capital expenditures, the US government is buying domestic semiconductor capabilities, and the Trump account emerges alongside these assets.

Closed loop: Positions and policies pushing each other

Tracking the stock accounts of politicians has been practiced in the market for many years.

The Pelosi family’s trades have been tracked for years, and the logic has remained simple: policymakers knew something in advance, hence they bought early. Policy generates information, that information brings trading opportunities and officials profit from time differences.

This logic has a legal framework; the US officials' stock trading disclosure law was created for this reason.

Trump’s US stock account has an additional layer, and it is harder to deal with.

If he holds Intel, there are financial incentives to maintain semiconductor subsidies. Holding Coinbase and Robinhood creates incentives to promote cryptocurrency legalization. Holding AI hardware chains provides motivation to continue expanding capital expenditures in data centers. Holding broad market index funds and big tech adds to the motivation to maintain risk appetite in the overall US stock market.

When the account and policy align, the two can reinforce each other. Over a long time, it becomes difficult for outsiders to discern which one is pushing the other.

Policy influences holdings, and holdings in turn influence policy leanings, which then pushes up the value of the holdings. Once it begins, it becomes challenging for outsiders to determine whether financial interests played a role in any specific decision and how significant that role was.

Previous presidents have insisted on using blind trusts, and the core meaning lies here: money goes in, the individual does not know what they hold, so there’s no financial bias when formulating policy. Cutting off this feedback loop is a basic assumption of institutional design.

Trump does not have this setup.

The CHIPS and Science Act initially designed the subsidies as non-equity to avoid the government becoming a shareholder and losing its neutrality afterward. Trump altered it to equity, and the government took a 9.9% stake. Six months later, his own account also invested in Intel. Now, the direction of semiconductor subsidy policy and the market value of his two accounts point in the same direction.

The US officials' stock trading disclosure law regulates officials trading using non-public internal information.

Most of the information here is public. The problem is that decision-making power and financial interests are tied to the same person, and current rules do not have means of constraint on such ties, only requiring them to report the results.

On April 9, 2025, he tweeted that it was a great time to buy. Less than four hours later, Trump announced a suspension of tariffs, and the S&P 500 rose by 9.5%. Afterward, Washington University law professor Kathleen Clark said, "He is sending a signal; he can recklessly manipulate the market."

A year later, the account emerged.

The Dell family invested $6.25 billion into the "Trump Account," Trump built a position in Dell in Q1, publicly endorsed Dell in Q2 at the White House, Dell rose about 12% that day, and six days later the transaction record entered public documents.

Everyone in this chain got what they wanted.

The market received a story that could explain the stock price. The company received exposure from the White House. The Trump account realized paper gains. The policy project secured funding from business families.

The 113-page disclosure document tells you what he bought, but does not convey the fact that policy influences holdings, and holdings, in turn, affect the policy.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。