Trader Jez today announced his new protocol PaperTrade developed on HyperEVM, sparking enthusiastic discussions in the English crypto community.

Jez is a long-time advocate of perpetual contracts, having heavily invested in Hyperliquid in its early days, with his account ranking high on the airdrop leaderboard of Lighter and Variational. This time he has personally stepped in to create a Perp DEX with no fees, no slippage, and no funding rates.

Ancient Casino Exile on Chain

The mechanism of PaperTrade has an unsavory predecessor in financial history. The bucket shops of American small towns in the early 1900s displayed signs of brokerage firms and wrote real-time quotes from the New York Stock Exchange in chalk behind the counter, but the clients' orders never left the drawers of the shop owners. Essentially, it was a gamble between the clients and the shop owners. This business was banned by legislation in New York State in 1909 and essentially disappeared by the 1920s.

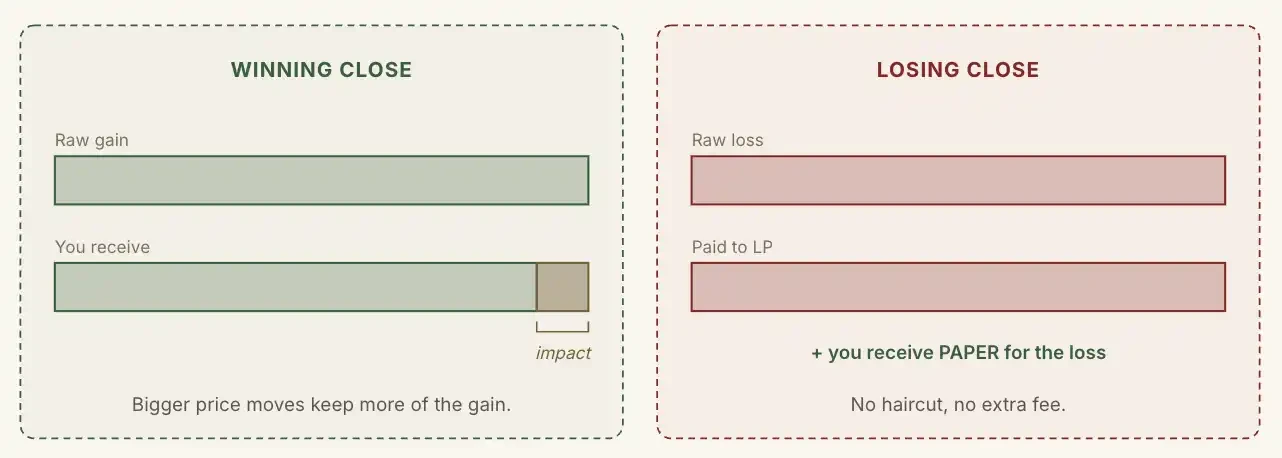

When users open or close positions on PaperTrade, the platform directly reads the order book prices from Hyperliquid and settles the difference between opening and closing directly against the public LP pool. Throughout this process, no orders enter the matching system of Hyperliquid, nor is there any actual turnover of perpetual contracts. The trading parties are always the users and the LP pool, with no third-party counterparties.

Perpetual Contracts + P2P + DeFi Ponzi

PaperTrade also draws from models of DeFi mining and P2P lending.

User losses on PaperTrade are directly deposited into the protocol's LP pool, while user profits are skimmed by the platform. The smaller the price fluctuations, the more profit is taken. In other words, the more users earn, the less the protocol extracts.

Unlike HLP, the LP pool of PaperTrade has no pre-stored team funds, no VC investments, and does not accept any form of external deposits at all. Its only source of funding is the margin losses of users.

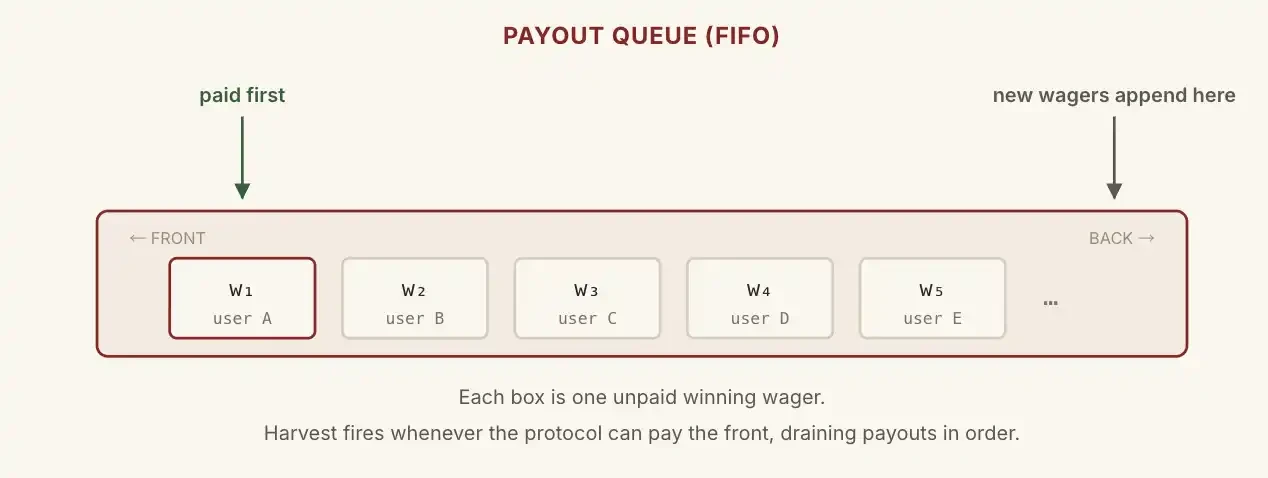

Here comes the question: If there is only $100 in the LP pool, but a user earns $5000, how does the protocol pay?

PaperTrade transfers the credit queue of traditional P2P lending on-chain.

This $5000 will enter an orderly on-chain queue, waiting for the next losing order to come in and fill the gap, paying out the queue in order from the front. The user’s principal is always refunded first, and only the profit portion gets queued.

Theoretically, the LP could "go bankrupt" at times, but every winner will ultimately be paid, unless the losses of the losers cannot cover the profits owed to the winners by the platform.

If it ended here, the project would be doomed because if the LP pool runs out of money, it would mean winners might wait a long time to get their profits, naturally resulting in no motivation to trade, leading traders to leave, and even the losers would be gone, making the platform’s debts to winners become bad debts.

The essence of PaperTrade is its token PAPER.

For every dollar the user loses, the protocol will mint a certain amount of PAPER according to a curve.

When the LP balance is below $2 million, the minting rate is fixed at 100 PAPER for every $1 lost; after the LP exceeds $2 million, the rate begins to decline, and the more the LP balance, the less PAPER minted.

Horizontal axis: number of PAPER obtained per unit of loss; vertical axis: LP balance (one unit is $1M)

Staking PAPER can yield two parts of dividends: one is the protocol's skimmed income; the other is when the balance exceeds $5 million, all excess will be allocated entirely to stakers.

In other words, the scale of the LP pool has been designed with a $5 million ceiling; beyond this scale, user losses will be fully returned to PAPER holders. This creates a closed-loop where "losers gain equity in the platform, winners take the losers' money, and the platform skims the winners to subsidize the losers."

Therefore, a reasonable participation strategy can be summarized as: betting on losing money to mint PAPER when the LP pool's TVL is low, and staking PAPER to collect dividends when the LP pool's TVL is high.

Pressure Test of HyperEVM

The author believes that the greatest uncertainty of PaperTrade lies in its deployment of HyperEVM.

PaperTrade merely uses the quotes from Hyperliquid as a free native oracle, while all other logic resides in the contracts of HyperEVM.

This means that any high-performance chain with similar capabilities, willing to connect to an external price oracle, can replicate all mechanisms of PaperTrade on its chain. Replicators can even provide things that HyperEVM cannot do: lower gas, higher TPS, more generous early subsidies, and more aggressive token incentives.

During the meme season of HyperEVM in Q1 last year, there was a period with slow on-chain speeds and high gas fees, making the launch of PaperTrade another test for HyperEVM.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。