Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma (@azuma_eth)

On May 11, before the US stock market opened, stablecoin issuer Circle officially announced its first-quarter financial report for 2026.

The financial report shows that Circle's total revenue and reserve income in the first quarter was $694 million, slightly below the market expectation of $715 million; EPS was $0.21, higher than the market expectation of $0.18; adjusted EBITDA was $151 million, a year-on-year increase of 24%; net profit was $55 million, a year-on-year decrease of 15%.

As a result of the financial report release, CRCL saw significant fluctuations in pre-market trading, with nearly a 6% pre-market increase gradually erased amidst the volatility. By 22:00, CRCL experienced a sharp drop after trading on US stocks but quickly reversed course, temporarily reporting $115.74, a daily increase of 2.52%.

Core Data Interpretation

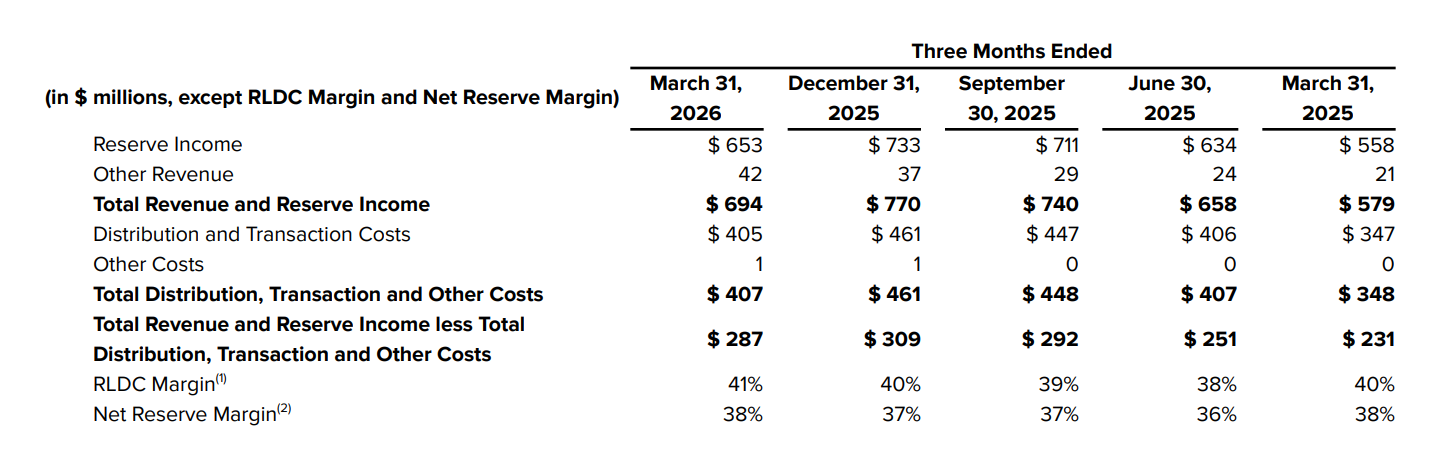

As shown in the financial report, Circle's total revenue and reserve income for this quarter was $694 million, which, although a year-on-year increase of 20%, interrupted the previous trend of growth over multiple quarters ($579 million ➡️ $658 million ➡️ $740 million ➡️ $770 million ➡️ $694 million) and failed to meet market expectations.

Circle attributed the slowdown in revenue growth to the decline in the reserve return rate. On December 10, 2025, the Federal Reserve lowered the federal funds target rate range by 25 basis points to 3.5%-3.75%, thus compressing Circle's reserve asset yields primarily consisting of US Treasury bonds.

However, despite the relatively weak revenue, Circle's financial report still revealed some optimistic localized data.

First, Circle's other revenue excluding reserve income set a new record, reaching $42 million, showing a continuous increase over multiple quarters ($21 million ➡️ $24 million ➡️ $29 million ➡️ $37 million ➡️ $42 million).

As discussed in our article today afternoon titled “Financial Reports, Legislation, Federal Reserve... Circle Faces Three Major Tests This Week”, this means that Circle's revenue sources are becoming more diversified, with its platform services, API tools, and payment products generating substantial business income, and reliance on interest income is decreasing.

Another noteworthy data point is the RLDC Margin, which represents profit margin after deducting distribution costs, reflecting the core business profit level after distribution expenses are accounted for, and is widely viewed as Circle's most core profit indicator. This quarter, Circle's RLDC Margin reached 41%, achieving growth for four consecutive quarters (36% ➡️ 39% ➡️ 40% ➡️ 41%), which indicates that Circle is becoming more efficient in controlling distribution costs.

Next, let's look at the expenditure situation. Distribution and transaction costs remain Circle's largest expense item, amounting to $405 million this quarter, a year-on-year increase of 17%. This expenditure is mainly linked to the USDC distribution contract with Coinbase, which is set to expire in August this year, and how it will be renewed (mainly depending on whether the profit-sharing ratio will be adjusted) will greatly affect Circle's future expenditure and profit situation.

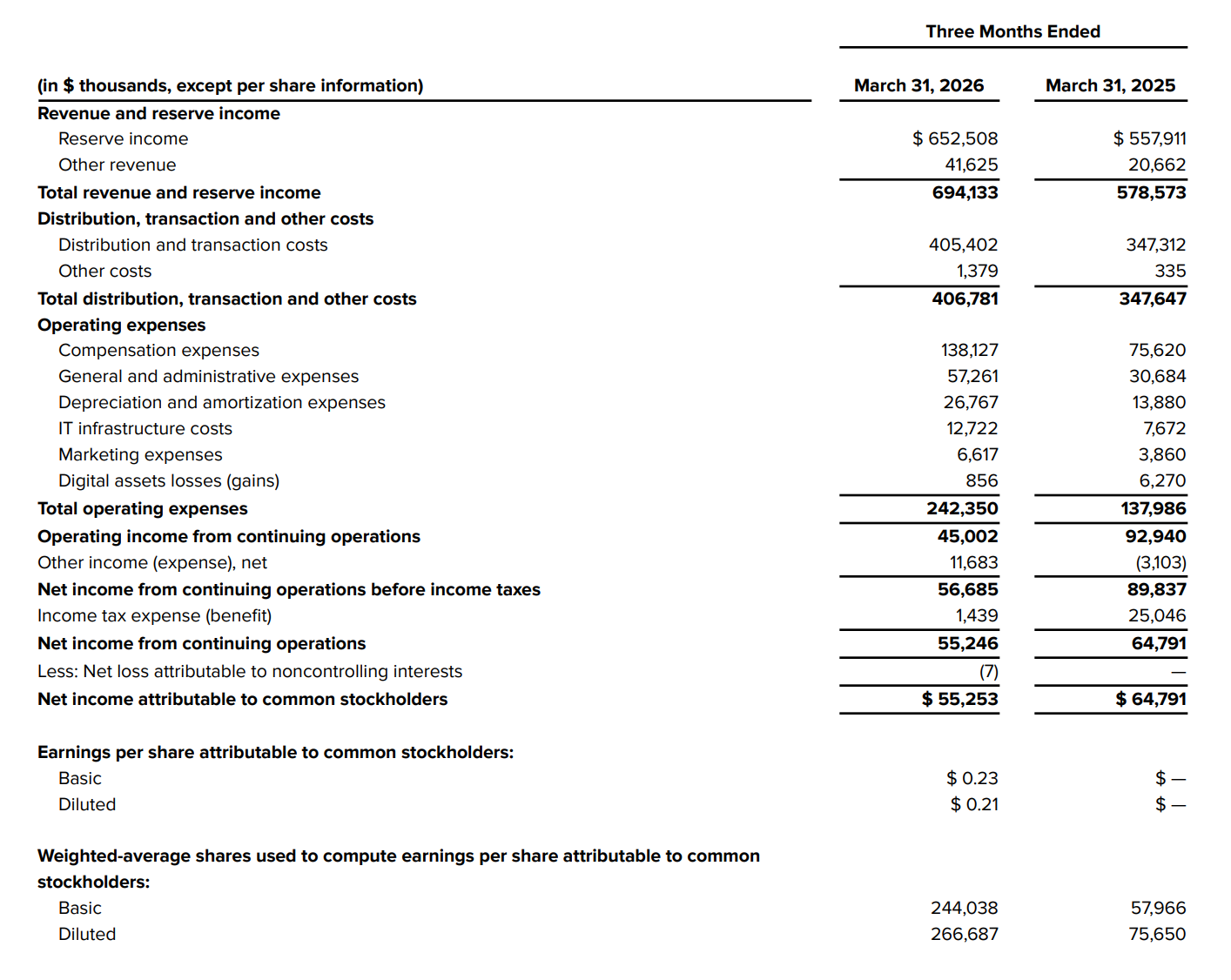

Excluding distribution costs, operating expenses increased dramatically from last year's $138 million to $242 million, a year-on-year increase of 76%. The primary source of this increase came from compensation expenses, which rose from $75.62 million to $138 million, nearly doubling — Circle explained that this was mainly influenced by stock-based compensation and related taxes following its IPO.

Due to the surge in expenditures, Circle's operating profit this quarter fell from $92.94 million in the same period last year to $45 million; net profit attributable to common shareholders dropped from $64.79 million in the same period last year to $55.25 million; earnings per share (EPS) were $0.23, diluted to $0.21.

Other Operational Highlights

In addition to the core financial data, Circle also disclosed several operational highlights in its Q1 financial report.

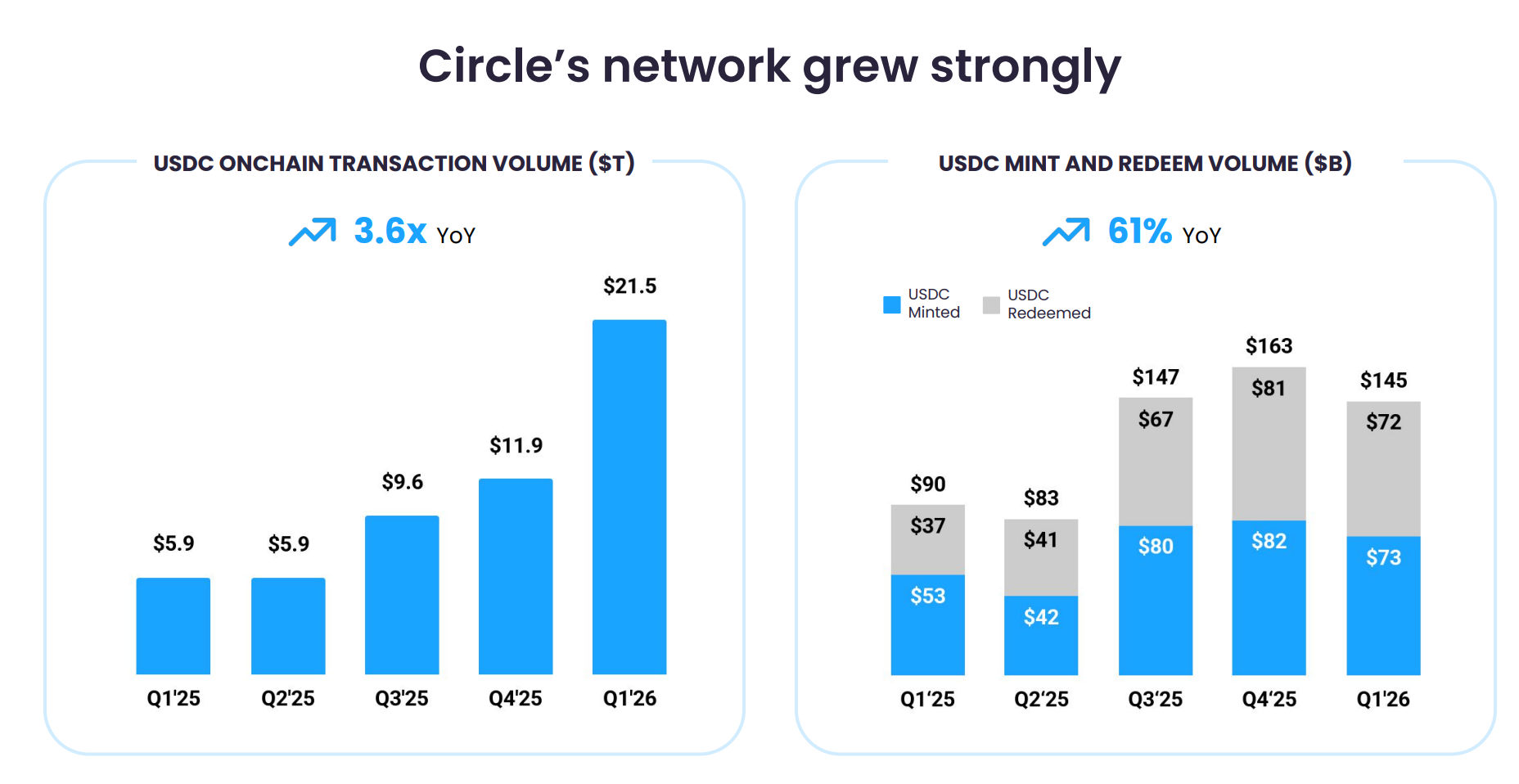

Among them, the most critical data is that the circulation of USDC reached 77 billion tokens at the end of the first quarter, a year-on-year increase of 28%, but at the same time, USDC's on-chain transaction volume reached an astonishing $21.5 trillion in the first quarter, a year-on-year increase of 263%. Visa Onchain Analytics data also showed that in the first quarter, USDC accounted for 63% of the total stablecoin transaction volume across the network.

The surge in transaction volume far exceeds the growth in circulation, indicating that each USDC is being transacted and used on-chain at a significantly higher frequency — USDC is not lying static in wallets but is being actively and frequently used in payment, DeFi, cross-border settlement, and other scenarios.

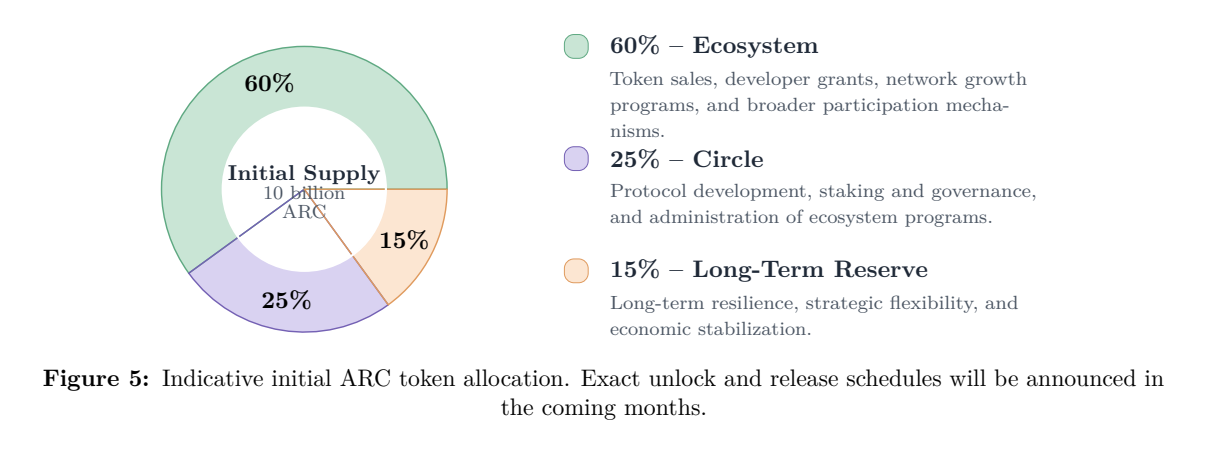

Another key point is that Circle also disclosed that its payment network Arc Network has completed an ARC token pre-sale raising $222 million, with a valuation of up to $3 billion, backed by well-known institutions including a16z, BlackRock, Intercontinental Exchange, Standard Chartered, and SBI. The ARC token white paper disclosed today shows that 60% of the tokens will be allocated to the ecosystem (token sales, developer funding, network growth); 25% will be allocated to Circle (protocol development, staking, and governance); 15% will be allocated to long-term reserves (strategic flexibility and economic stability).

In addition, Circle's payment service Circle Payments Network (CPN) aimed at institutions is estimated to reach an annual transaction volume of $8.3 billion (based on a reverse calculation of 30-day data as of March 31); in April, Circle also launched a "Managed Payments" product to expand its payment offerings, allowing financial institutions to initiate stablecoin payment businesses without having to manage digital assets themselves.

In response to the AI Agent-driven business future, Circle also announced the launch of Agent Stack, a suite of infrastructure services and tools aimed at the AI Agent economy, designed to provide high-speed, low-cost financial service capabilities for autonomously operated AI Agents. Circle co-founder and CEO Jeremy Allaire expressed his outlook on this, stating: "With the pre-sale of the ARC token, the accumulation of potential for Arc Network, and the launch of Agent Stack, we are building a trusted infrastructure for AI-native economic activities and a more programmable internet finance system."

Circle's New Chess Game

Against the backdrop of declining high-interest dividends (after Powell took over the Federal Reserve, he will promote a "rate cut + balance sheet reduction" strategy), Circle is clearly unwilling to be completely constrained by the Federal Reserve's interest rate policy, and its layout focus has subtly shifted towards diversified expansion of non-interest income.

From the details disclosed in this quarterly report, after consecutively launching services such as CPN, Managed Payments, Agent Stack, and Arc Network, Circle's goal is no longer just to be a "stablecoin issuer," but to try to position USDC as the underlying dollar network of the internet era. Under this entirely new vision, Circle's clientele is no longer limited to exchanges or crypto-native users but is extending towards cross-border payments, corporate settlements, and even the AI Agent economy.

Circle's ambition has become quite clear: to transform USDC from a "static reserve asset" into "liquid economic blood." This may be the grand strategy that Circle genuinely wants to achieve.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。