In today's analysis, I will show everyone how Galaxy plans to combine the development of both businesses rather than separating them, and how this will help the company achieve stability that is difficult for other companies to reach.

Written by: Prathik Desai

Translated by: Block unicorn

Introduction

The cryptocurrency trading volume of Galaxy Digital continued to decline in the first quarter of 2026, but its operational business is starting to decouple from the cryptocurrency cycle. The company believes that combining both is the right strategy. In the first quarter of 2026, the price of Bitcoin fell by more than 20%, and the price of Ethereum dropped by about 30%. However, Galaxy's trading volume remained stable. This is the first sign of Galaxy's business decoupling from market cycles.

In previous analyses of Galaxy's profitability, I pointed out that the Helios data center could serve as a hedge against the fluctuations of the cryptocurrency cycle. However, this argument is forward-looking and assumes that the company can complete construction on schedule and fulfill the cash flows from contracts that have not yet begun.

In April this year, Galaxy delivered its first data centers in Texas to CoreWeave, indicating that the company is gradually diversifying its overall business and shifting towards a high-margin, non-cyclical data center business. Although the revenue from its data center business is currently negligible, an improvement in its financial situation is expected to begin in the second quarter of 2026.

In today's analysis, I will show everyone how Galaxy plans to combine the development of both businesses rather than separating them, and how this will help the company achieve stability that is difficult for other companies to reach.

TL;DR:

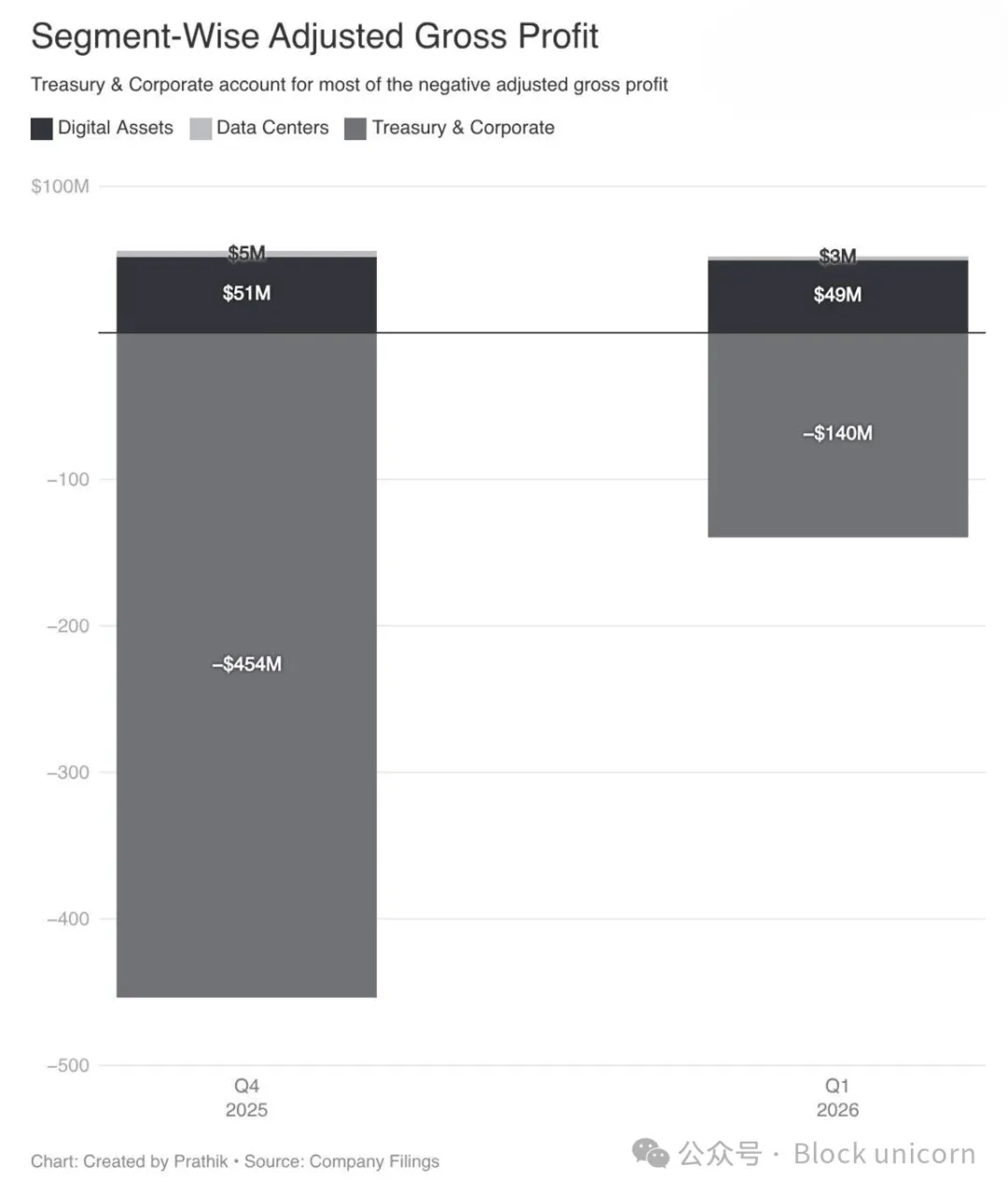

- Despite a drop of about 25% in cryptocurrency prices, Galaxy's digital asset division recorded an adjusted gross profit of $49 million, roughly the same as in the fourth quarter ($51 million).

- Galaxy's trading volume remained stable while the entire industry's trading volume declined by over 20%.

- Helios delivered its first data hall to CoreWeave, marking the completion of its construction milestone and starting to generate operational revenue.

First Signs

Galaxy's financial situation is not significantly different from other cryptocurrency companies. Its adjusted EBITDA for the first quarter was negative $188 million, almost entirely due to an adjusted gross loss of $140 million from the financial and corporate divisions. This loss is primarily attributed to unrealized impairments in its net digital asset exposure. As of March 31, 2026, Galaxy has reduced its digital asset holdings to $667 million, down 27% from $920 million at the end of the year.

The digital asset segment is responsible for cryptocurrency trading, lending, asset management, and infrastructure construction, posting an adjusted gross profit of $49 million. Despite a rise in cryptocurrency prices in the fourth quarter, this segment's gross profit remained nearly flat compared to $51 million in the fourth quarter. The price drop led to a loss of participants, a sharp reduction in trading volume, and a hit to Galaxy's business. This also reduced the collateral on loans that Galaxy relied on to earn interest.

The trading activity of Galaxy's trading desk also reflects this trend. Its trading volume remained flat quarter-over-quarter, while the entire industry's trading activity shrank by more than 25%.

But what hindered Galaxy's operations during the market crash?

Stable Pillars

By diversifying its product and customer base to spread risk, Galaxy was able to survive when its peers faced the shocks of a market crash.

Over the past 18 months, the company has gradually increased fee income and recurring revenue in its trading department. Although the asset management scale decreased from $11.4 billion to $8 billion due to the revaluation of existing holdings, the asset management business still recorded a net inflow of $69 million. Shortly after the end of the quarter, Galaxy secured a $75 million single-client mandate, one of the largest commissions in its history. Despite a 20% shrinkage in loan scale due to falling cryptocurrency prices and natural maturities of loans, Galaxy continued to attract new clients and diversify its counterparties.

In May of this year, the company will launch a fintech hedge fund, investing in companies building tokenized infrastructure. At the same time, the company will open its consumer-facing trading app GalaxyOne to enterprises, allowing institutional users to trade, manage digital custody, finance, stake, and access cryptocurrency research materials. These two businesses are expected to generate recurring revenue regardless of Bitcoin or other cryptocurrency price fluctuations.

The next step is strategic positioning.

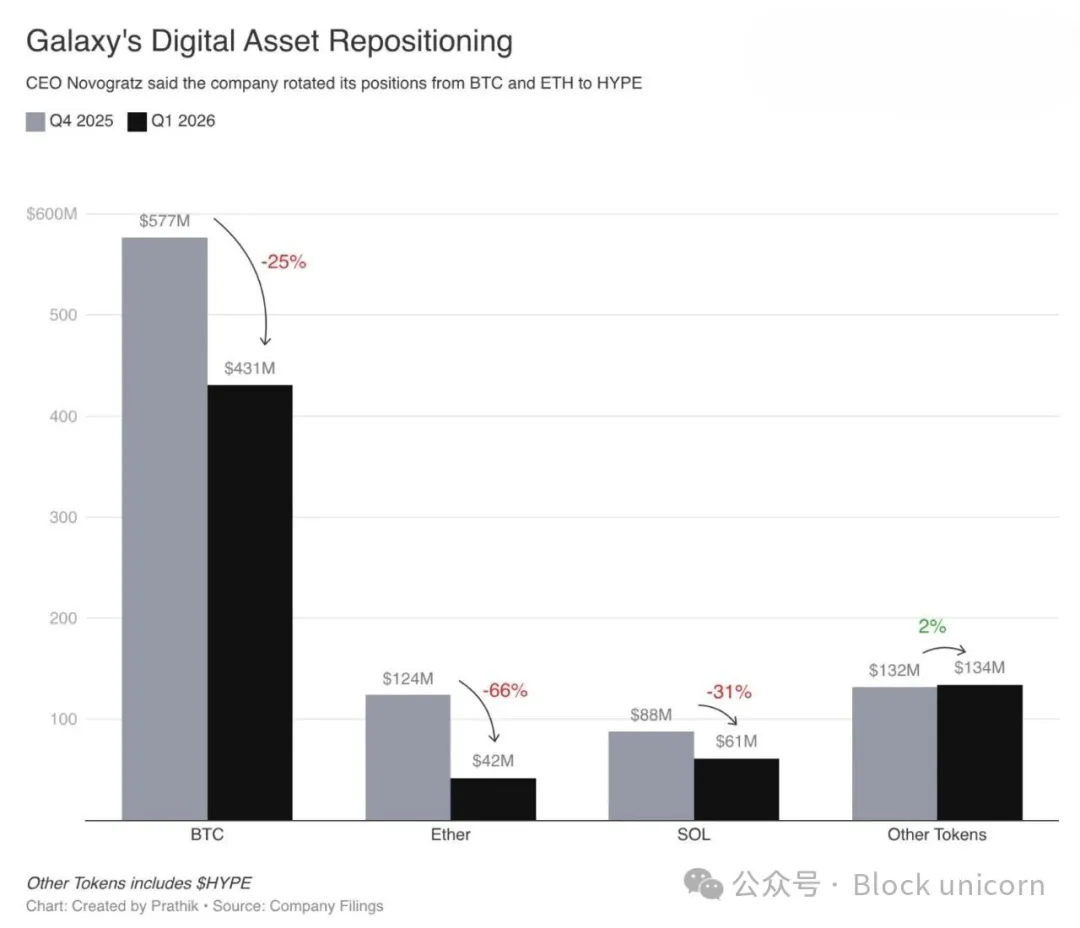

Galaxy has reduced its investment in Bitcoin and redirected a significant portion of its balance sheet towards Hyperliquid.

This rotation has enabled the balance sheet's performance to exceed the returns achievable through a purely beta strategy.

But for Galaxy's investors and analysts, the biggest takeaway will be: the lights in Texas have finally turned on.

Lights, Camera, Data Centers

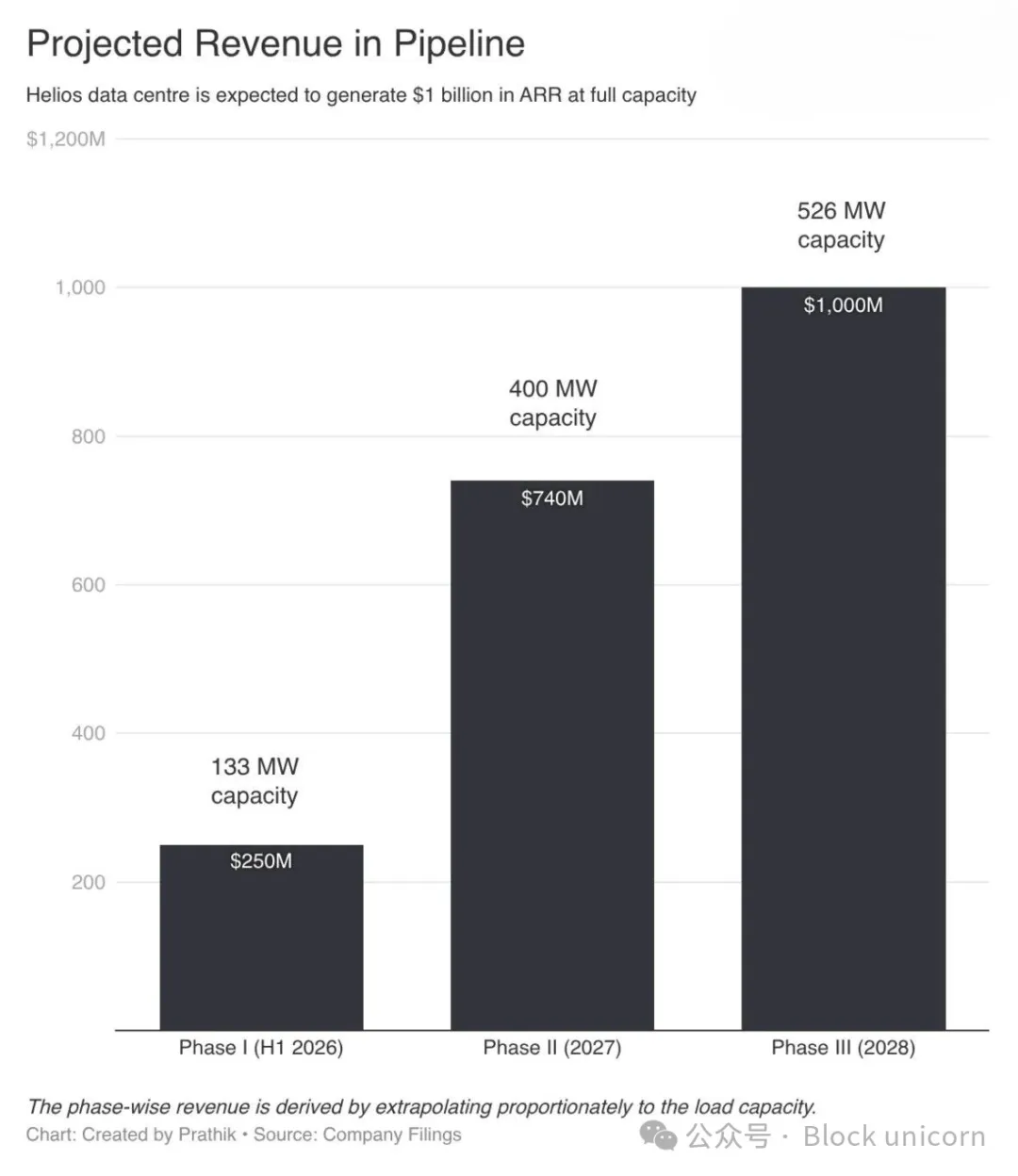

Galaxy's Helios data center delivered its first batch of server rooms to CoreWeave in the first quarter, and it is expected to generate $1 billion in revenue annually after full deployment by 2028.

The facility, originally planned for Bitcoin mining, has now been transformed into a fully functional AI data center equipped with real-time power distribution, cooling, and networking.

Although the revenue from the data center business is only $3 million, the company is still advancing its 133-megawatt phase one project as planned. The three aspects of this business segment that excite me the most are: profit margins, immunity from seasonality, and contract duration. These contracts provide cash flow for 15 years, with an EBITDA profit margin of about 90%. The phase one project is expected to be fully operational in the second half of 2026, with an annualized revenue of $250 million, completely unrelated to digital asset prices.

For reference, the adjusted gross profit from the digital asset business segment for this quarter is $49 million, with an annualized recurring revenue (ARR) of $200 million. The Helios phase one project alone has the potential to generate higher operating profit, with an ARR of $250 million and an EBITDA profit margin of up to 90%.

Galaxy has also received approval from the Electric Reliability Council of Texas (ERCOT) to increase its generation capacity by 830 megawatts.

Besides CoreWeave, the company is actively negotiating with other tenants for expansion. But why seek new tenants?

Galaxy does not want to repeat the mistakes of the past by becoming overly reliant on a single business or customer. This may be why its president, Christopher Ferraro, wants the company to focus on a multi-tenant, multi-park strategy.

However, how will it fund these multiple sites? Each site requires capital-intensive computing power, cooling equipment, and other infrastructure.

In the Helios data center phase one project, CoreWeave's ultimate client—a publicly traded company with a market capitalization of several trillion dollars—will use its GPUs. This credit rating will directly affect the financing terms for Galaxy's future data center projects.

Galaxy's Dual Business Model

Galaxy Digital's two business segments are evolving, with different capital needs, profit models, and prospects. There seems to be little synergy between them, and no apparent reason to continue operating under the same entity. So why not split them up?

The company is not convinced that these business segments will always remain unrelated.

Most people may view Galaxy as an ordinary cryptocurrency company about to spin off its data center business. But they overlook the connection between its cryptocurrency trading and data center operations. When Galaxy's data center business reaches an annual revenue of $1 billion with an EBITDA margin of 90%, it will be fully capable of operating its cryptocurrency infrastructure business robustly during a bear market.

The data centers cover fixed costs, while the cryptocurrency business generates profits during market fluctuations. In this model, the total cost of capital for Galaxy's two businesses decreases, as they can mutually reduce risks. The cryptocurrency business itself does not need to generate sufficient profits to handle economic downturns. As long as it can cover its variable costs, it can help the company maintain operations, as seen in the first quarter of 2026. Data centers can operate independently of token prices, as their demand comes from large-scale data center operators competing to secure computing power. However, sharing a balance sheet with a cryptocurrency business that can generate cash flow allows Galaxy to flexibly bear early development costs and accelerate the construction of new sites faster than an independent data center startup.

Currently, these conclusions are not definitive. This is merely the first quarter's signs of decoupling, and is for reference only. To prove this is a general rule, the conclusion needs to be validated in the next two to three quarters.

However, there is no disputing that the direction of the architecture that Galaxy is building is correct. Its data center business provides high-margin, contractually fixed and predictable revenue, while its trading business offers low-margin, high-volume cryptocurrency trading that is highly cyclical.

Novogratz said if this performance continues for another three quarters, he will celebrate.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。