There is a reason why private credit adapted to on-chain earlier than most RWAs.

Written by: Bryan Daugherty

Translated by: Block unicorn

There is a reason why private credit adapted to on-chain earlier than most RWAs

It inherently possesses the elements that can be priced in an on-chain market: returns.

This makes its development path clearer than that of private equity, venture capital, or real estate.

Those categories primarily involve acquisition channels, packaging, or long-term investments.

Private credit provides a more direct path.

Cash flows can be allocated, financed, and ultimately reused within the crypto market.

Source: DefiLlama

What matters is not that private credit is tokenized

But that private credit is starting to function on-chain.

Many tokenized assets are still in the issuance phase.

- They are packaged.

- They are distributed.

- They are stored in wallets.

Private credit goes further.

It starts to appear as collateral in the lending market and in strategies that allow users to borrow against the asset without completely exiting.

This is far more significant than mere tokenization.

The market has begun to distinguish between acquisition channels and usability

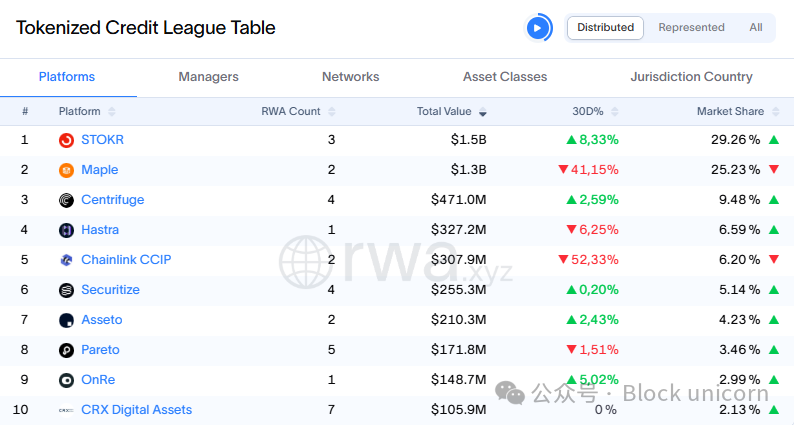

A strong signal from the report is that most of the active private credit market capitalization is concentrated in permissionless products.

Source: rwa.xyz

This indicates some important information.

Users want more than just exposure to private credit.

They want private credit that behaves more like crypto assets:

- Transferable

- Usable in decentralized finance (DeFi)

- Easier to finance

- Easier to transfer between different places

This is starkly different from the tokenized fund interest that remains fundamentally unchanged.

The fastest-growing products come from those built for crypto infrastructure (Crypto Rails)

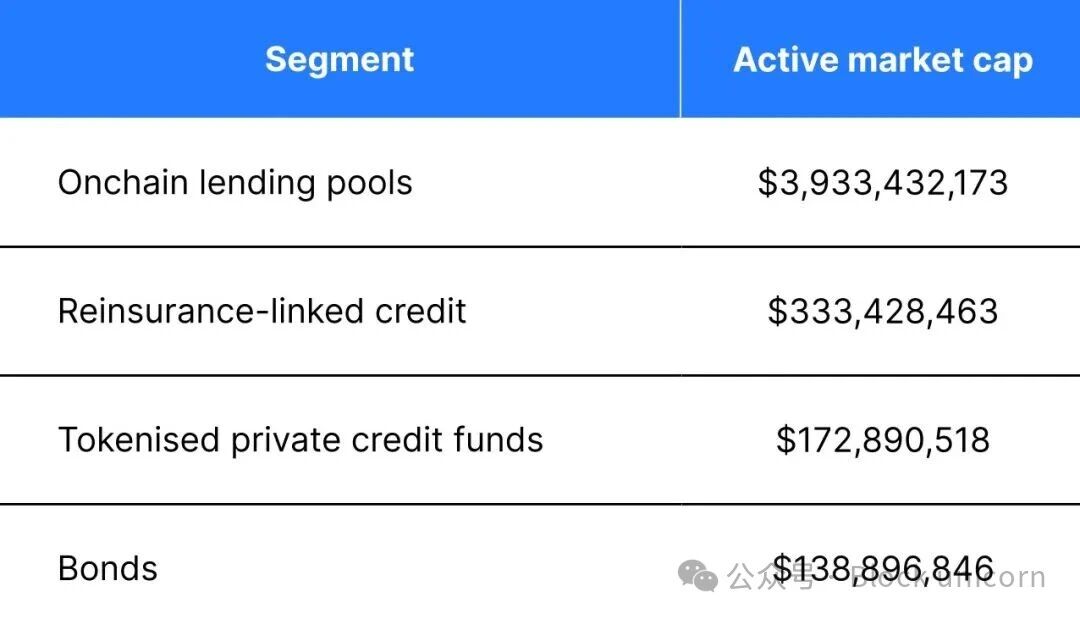

Another prominent point is where the capital actually resides.

Source: DLResearch

The largest share of on-chain private credit is not in tokenized fund wrappers.

Instead, it comes from on-chain lending pools.

This is crucial because it indicates that the market rewards structures specifically designed for on-chain use, rather than merely repackaging traditional products to fit new channels.

The more powerful the product is in the crypto market, the more likely it seems to attract demand.

Why private credit developed first

Private credit solves two problems simultaneously.

For traditional asset managers, tokenization improves distribution.

For on-chain markets, it introduces a new type of productive collateral.

This combination remains rare in RWAs.

Real estate can be tokenized, but liquidity and valuation are still difficult to achieve.

Private equity and venture capital can be tokenized, but largely remain passive holdings.

Carbon credits benefit from better tracking, but their usability in decentralized finance (DeFi) is not high.

Private credit is one of the first categories to tokenize while improving acquisition channels and financial use.

None of this eliminates the inherent risks

It is still private credit.

Underwriting is still important.

The borrower's qualifications are still important.

Recovery value is still important.

Liquidity is still important.

Putting assets on-chain does not solve any of these issues.

It merely makes products easier to distribute and, in some cases, easier to finance.

This is useful.

But it is not the same as reducing potential risk.

The true revelation of RWAs

Private credit is important because it illustrates what the market rewards.

Not just tokenized assets.

But those assets that become more useful once they are on-chain.

This might be a clearer way to think about the next phase of RWAs.

Industry leaders will not be those assets that are the easiest to package.

They will be those that gain real utility from being part of the on-chain financial system.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。