Author: Decentralisedco

Translated by: Bilingual Blockchain

The commonality among all these platforms is that they are capital-intensive businesses.

Unlike products that can be built with a few lines of code on a Saturday afternoon, they require the coordination of patient capital willing to accept the risks posed by these platforms. In some cases, complex supply-side networks help these protocols build a moat.Jupiter’s integration network is difficult to replicate overnight.

Because blockchains are primarily tools for moving funds and verifying whether transactions adhere to the rule sets created by developers—they are only valuable when they can participate in capital-intensive operations. Perpetual contract trading platforms are able to repeatedly put large amounts of capital into productive use on a daily basis. Lending platforms extract a small portion from the substantial revenues generated.

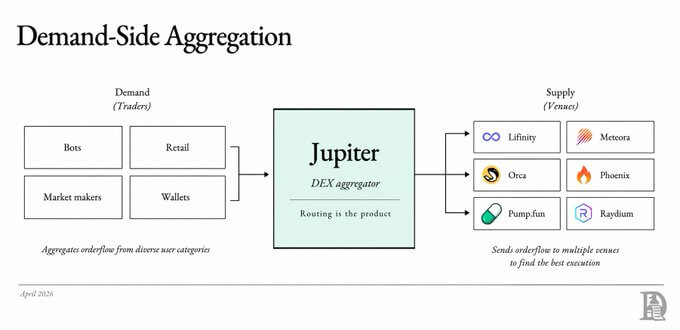

For example, Aave earned about $123 million from approximately $920 million in revenue generated over the past year. But such aggregators can only dominate when they possess three key elements:Supply (liquidity), demand (users), and distribution channels.

In this regard, Hyperliquid is a unique case. It has paid nearly $100 million in builder fees, but the vast majority of its revenue comes from its own native frontend. It is able to retain its highest-quality users while expanding the coverage for new users to interact with the protocol.

But what is the logic behind this?

One theory suggests that distribution channels are the tollways of Web3. Large protocols tend to own and retain their highest-quality users. When you notice the revenues generated by decentralized exchanges compared to on-chain aggregators routing orders, you realize this.

Overall, builder fees account for only about 6% of the total revenue of Hyperliquid, which is around $1.1 billion. MetaMask’s tight integration on Ethereum brought it $184 million in swap fees last year. Phantom generated nearly $180 million, but considering this is a small part of a massive economy of scale ecosystem.Retail products aimed at distribution can only drive value towards them when built on a single protocol that possesses both liquidity and economic activity.

Vertically integrated aggregators can attract and retain users because they have deep available liquidity. From this perspective—capital in the crypto space is no longer a commoditized product. It is the most necessary component. Vertical integration of capital provides participants with more reasons to stay within the ecosystem. In such systems, capital can generate liquidity because it can be put into productive use.

Capital itself is not a moat. It is a result of the vertical integration you build. Vertical integration is the moat; capital is merely a byproduct.

Having a large TVL (Total Value Locked) does not guarantee success. In an economy, idle or underutilized capital can become a burden when it suffers a hack. This is why you see protocols trying to differentiate based on the economic output they can generate from niche use cases.@USDai_Official, the company behind $chip, has issued nearly $100 million in loans this quarter and has $1.5 billion in reserve projects underway, expected to generate nearly 16% APY for its riskier tiers within the year.

The highest-risk pools on @maplefinance generate approximately 15-20% APY, comparable to the current 12.6% APY of the USDC pool on Aave or higher. It aggregates borrowers who can use protocol liquidity to create economic output.

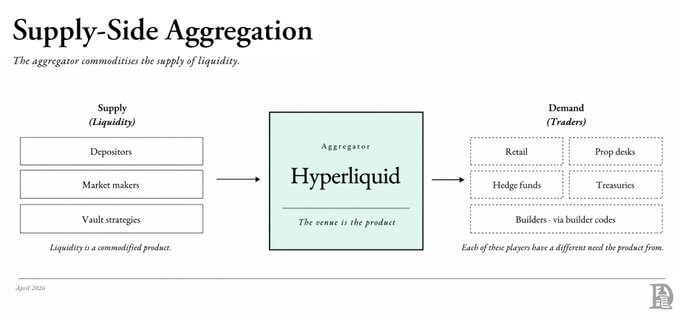

Naturally, Hyperliquid is the best example of a supply-side aggregator that can put capital to meaningful use. Last year, Hyperliquid achieved approximately $942 million in revenue, with an average TVL of about $3.5 billion. Based on some rough calculations, for every $1 deposited in the protocol, it turns over about 285 times a year, generating around $0.30 in fees for every $1 TVL. In contrast, Aave generates approximately $0.05 in fees for every $1 TVL in its lending market.Yes—I am comparing the TVL yield of Hyperliquid (a trading platform protocol) with Aave (a lending avenue). However, in a market where consumer preferences are not predetermined and investor loyalty is shallow, capital will flow to where the best outcomes can be generated. Considering the risks of hacks, investors will demand a premium for the risks involved.

As it stands, perpetual contract trading platforms are the only places that can utilize idle capital and repeatedly use it on-chain to generate fees.Vertical Integration in the Crypto Space

Protocols have slowly begun to execute the same logic.

In Web3, without vertical integration that makes it easier to use, capital providers can be seen as commodities. Unless ecosystems are integrated into user experiences that do not exist anywhere else, users will not have loyalty.For Maple, such integration involves years of experience collaborating with hedge funds and market makers. For @centrifuge, its integration involves receiving nearly $1 billion from @grovedotfinance for its JAAA bond issuance from Janus Henderson. They do not capture loose, abstract parts of the economy but rather vertically integrate to provide better products to end users. By doing so, they create moats that are difficult to replicate overnight.

Maple’s years of underwriting experience or Centrifuge’s moat as a trusted capital coordinator are all features of a world where capital and relationships have become the only things that are difficult to replicate.

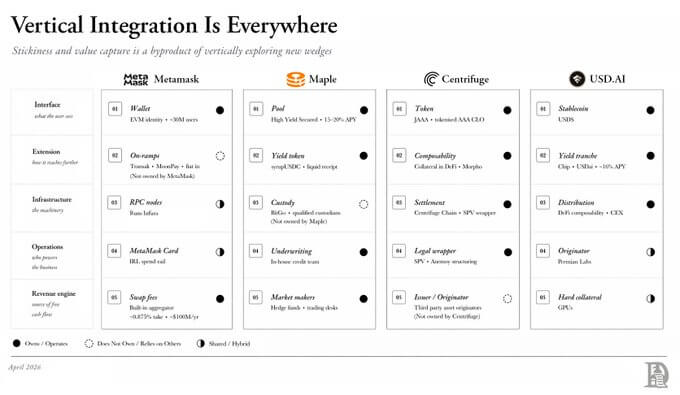

Companies engaging in vertical aggregation might regularly let parts of the stack go to third parties. Part of the reason for this is the lack of economic efficiency. For example, compared to the capital generated in swap and credit underwriting, holding custody or MetaMask issuing its own cards may not yield huge profits.However, when companies scale up, having the entire stack is necessary to establish a competitive advantage. This is partly why the industry is undergoing mergers and acquisitions.

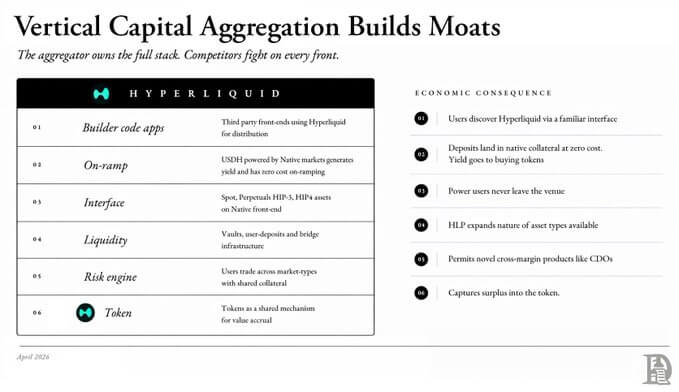

When a company implements vertical integration, you are not competing on single products but rather on the overall experience users have within it. On Hyperliquid, once HIP-4 goes live, users will be able to deposit for free (through @nativemarkets), participate in predictive market positions, and trade that position as collateral on their perpetual contract product. Its risk engine supports this experience. It’s worth noting that, even in today’s traditional finance, this would not be possible without the assistance of investment bankers.

The tweet below is an example of what happens when products undergo vertical integration within an ecosystem:

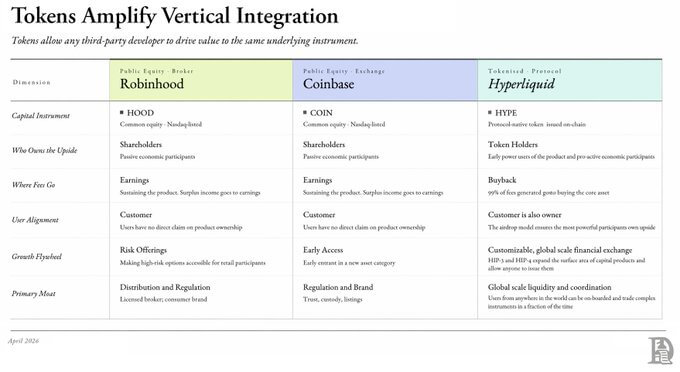

Hyperliquid has users, deposit channels, risk engines, trading interfaces, liquidity, and issues Tokens. Competing with it as a new business means fighting on six different fronts at the same time.

For newly launched applications, being able to capture a small slice of that holds far greater significance than building on new protocols like Monad—the total derivatives trading volume of all five perpetual contract protocols on Monad is around $2.6 billion.

Integrated ecosystems like those on Hyperliquid can attract developers, more integrations, headlines, and satisfied Token holders. (Or like me, a writer obsessed with studying how these things work).Trading platforms have also seen this shift. Coinbase acquired Deribit, which has custody operations, jointly issues currency (USDC) with Circle, gains revenue from reserves, has a substantial wallet infrastructure, and deposit channels in over 100 countries. It has also launched its own blockchain to pursue a vertically integrated user experience. Admittedly, Coinbase may be pursuing retail users who clearly do not want to "publish content" on a blockchain or use Farcaster too early.

Coinbase's integration exists in a loose form but is hidden beneath layers of bureaucracy, regulatory hurdles, and internal priorities. This may be a major distinction between an open-access integrated system and a walled garden. With a market cap of about $60 billion, Coinbase has little incentive to pursue edge developers.

In contrast, Hyperliquid benefits from developing its core pathway into the best marketplace while creating an ecosystem that drives value for the underlying Token.

In this context, Token is part of the integration, as it is what keeps these integrations active and valuable as a shared underpinning. This is where you see the industry getting confused between tokenized protocols and tokenized businesses. The premise of tokenized protocols is that it is easy for third-party developers to build on them. It incentivizes people to drive value (down) towards the Token—often in the form of repurchases from the market.

Companies like Robinhood and Coinbase are powerful economic players, but they cannot replicate Hyperliquid’s core owner-operator network.

The protocol's airdrop ensures that those who hold it are individuals contributing to its economy. They own enough Tokens and are willing to drive value for it. Hyperliquid practices this goal by foregoing 99% of revenue to repurchase Tokens from the market. Imagine a public company repurchasing ESOP from employees with 100% of their income. We might see people more accepting of capitalism.

This is what you see in the evolution of the industry, whether we like it culturally or not. Solana focuses on immutability. Ethereum focuses on censorship resistance and open-source. But if you closely observe where the traffic goes, you will see the industry adjusting its ideology based on commercial realities.

Compromise with Chaos

A vertically integrated stack will ultimately demand the sacrifice of complete decentralization for economic progress.This is not a new story on the internet. In the late 1990s, there was great hope for an open internet that allowed free speech without the concerns of repercussions. Nazi memorabilia was auctioned on Yahoo until a French court intervened in 2000. Tim Wu explored this topic deeply in his book "Who Controls the Internet?". The story of the internet, or perhaps the story of all human business networks, is that complete decentralization gives way to a diluted version that sacrifices control for economic interaction.

We accept the diluted version of the original so that business can scale, for without dilution, chaos would ensue.This tremendous expansion of energy is reflected in the way we describe those epochs. “The Wild” West. The internet “bubble”. Perhaps crypto is also experiencing a similar expansion of energy and dilution.

What does this mean for founders? Look at the data for Metamask and Phantom. These businesses are earning more than most L2s because they are downstream of ecosystems that produce enormous economic output. Building bridges to nowhere and for underserved trading platforms is no longer a business model—especially when the associated pain includes hacks. You should build where liquidity and users are today.

Imitating a vertically integrated product overnight is impossible. But you can build on top of it.

Operating systems have also seen similar patterns. When Blackberry fell and iOS became the dominant player—developers had to choose where to build. We have seen similar situations in the crypto space. Only this time, the capital incentives might keep developers blind for longer.Do you remember I mentioned Cubbon Park? I often think about why it has remained so clean and well-maintained during my decade in Bangalore. Part of the reason is that there are rules. For instance, being in the park after 6 PM is not allowed. Or holding events in the park may be met with scorn. Sometimes the rules can be strict. But the rules keep the place functioning properly.

Platforms and protocols on the internet are very similar. We may not like the rules surrounding them, but the rules keep them functioning.In an era of vertical integrators, we may find ourselves agreeing more and more with the rules so that our funds stay with us, and the economies of the people spending time in them can continue to scale. The trends point in this direction. Stablecoins, RWA (Real World Assets), perpetual contract trading platforms with closed-access risk engines, lending platforms with unknown risk underwriters, and off-chain RFQ products like @DeriveXYZ all point to the same trend.

That is vertical integration capital aggregators willing to forgo the dream of complete decentralization for progress.This article link: https://www.hellobtc.com/kp/du/04/6297.html

Source: https://x.com/Decentralisedco/status/2046961963385925865

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。