Original Title: The Return of Rimland

Original Author: ALEXANDER CAMPBELL

Translation: Peggy, BlockBeats

Editor's Note: The conflict surrounding Iran has not subsided with ceasefires, blockades, and tariff threats; instead, it continues to spill over. From the Strait of Hormuz to the Red Sea, from energy channels to trade order, the core of the situation is no longer localized military confrontation but a systematic game about "who controls the flow."

This article, tracing the strategic concept of "rimland," points out that the United States is trying to push the conflict from a regional issue to a global topic through maritime blockades and the restructuring of energy pathways, implicating China as well. As sanctions and interception measures escalate, the confrontation originally centered around the Middle East is transforming into a structural shock affecting global energy, supply chains, and financial systems.

Moreover, the market has not yet fully absorbed this "chain reaction." The immediate fluctuations in oil prices are just the first step; the transmission of these effects to liquidity, technological investment, household consumption, and even agricultural supply is only just starting to show. After the reevaluation of energy prices, the real test will be how the global economy can withstand the second round of shocks that follow.

This implies that the current issue is no longer whether the conflict will escalate but along which paths its impact will spread and when the market will begin to price these unpriced risks.

Below is the original text:

Well, the situation is clear now.

The tensions we identified last Wednesday have proven to be irreconcilable.

Iran wants nuclear weapons and control over the Strait; both points are unacceptable to Trump. How far is the distance between these two "target circles"? So far that Israel's war against Lebanon wasn't even included in the discussion agenda.

I won't claim my judgment is precise, but we may indeed have entered the "mid-game." This is not a conflict that can be called off in an afternoon. The core of the issue is very straightforward: Who will control the most important waterways in the world? And will Iran's willingness to threaten its neighbors be enough to gain leverage for negotiating nuclear weapons?

This is the key.

What is now becoming clearer is a whole set of strategic pathways. Readers who have followed along from "Fighting for the Dollar" to "Don't Take the Bait," then to "Awakening the Hegemon" and "Fragile Peace," should be able to see the pattern.

Trump is executing a "rimland" strategy.

Intercepting shipping. Threatening to impose a 50% tariff on all countries supplying weapons to Iran. Rather than attacking the heartland directly, controlling maritime channels for energy transport and drawing China into this game. For every mine Iran lays or for every tanker it attacks, it retaliates with tenfold actions—seizing their vessels, controlling tankers, directly selling their crude oil.

Settling in dollars.

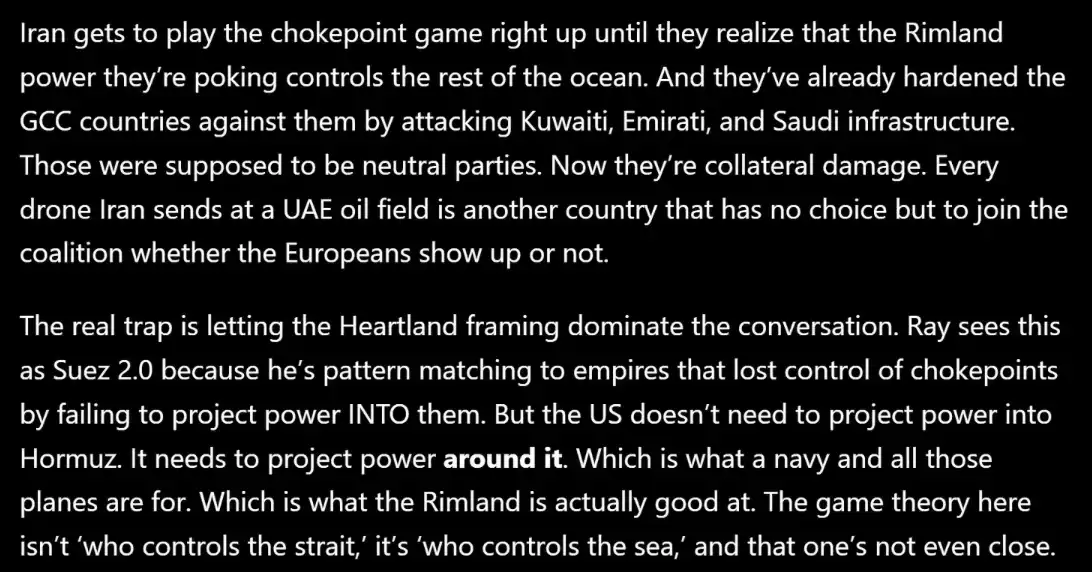

The screenshot mainly states that Iran is trying to use "choking the strait" as a bargaining chip, but this misjudges America's advantages strategically (control of the seas rather than control of nodes), and tactically pushes more neutral countries toward the opposing side.

Then there is the Abraham Accords. Saudi oil flows to Haifa via Jordan; the Trans-Arabian Pipeline has been reactivated. A corridor constructed of physical infrastructure is connecting coastal countries into an energy network, completely bypassing the "heartland." This is a "rimland alliance" built with pipelines and steel.

In my view, the reason we have reached this point largely stems from this very process—Iran (and China) set off a crisis in Israel through Hamas on October 7, thereby interrupting the normalization of relations; had this process continued, it could have formed an alternative trade route bypassing the Strait of Hormuz and even the Belt and Road Initiative.

Trans-Arabian Pipeline

This also explains the divergence between Washington and Brussels. The U.S. feels the weight of responsibility; whereas Europe seems to believe it can negotiate its own energy channels privately while allowing the "older brother" to bear the costs of the conflict. France has, on one hand, blocked relevant resolutions in the UN Security Council, while on the other, negotiated bilateral passage arrangements through the strait with various parties and called for the formation of an "independent national alliance." This reflects a typical "heartland" mindset: trading with inland powers, avoiding direct confrontations, as if maritime routes would maintain operation on their own.

Trump has just plugged this loophole—thus turning America's problem into the world's problem.

As of writing, oil prices have risen over 6%, and the stock market has dropped about 1%, making last week's gains from the ceasefire very likely to be quickly erased. I bought some VIX call options last weekend, so you could say I have a bit of a stake.

How the situation progresses next depends on a series of more fundamental questions:

· Can the ceasefire last another week, or is it heading toward a breakdown due to "reverse deduction"?·

Trump has indicated he will intercept ships that have paid a "toll" to Iran, does this include Chinese vessels? What will happen when they try to load crude oil from Kharg Island?

· He has also reiterated the threat of imposing a 50% tariff on any country supplying weapons to Iran—does this mean the trade war is back on the table?

Then there is Iran's countermeasure: it could activate the Houthis, who still have the capacity to disrupt passage through the Bab el-Mandeb Strait. Notably, most tankers transporting Saudi oil via the "East-West" pipeline are ultra-large crude carriers (VLCCs) that cannot pass through the Suez Canal. Once the Houthis escalate their actions, it would not only impact shipping in the Red Sea but also force these giant tankers carrying the most critical oil to take longer routes.

The main line here is that this conflict continues to escalate in its scale and spillover.

By escalating actions to intercept all vessels that pay "tolls" to Iran and reiterating the tariff threats, Trump has clearly drawn China into this game. Beijing has been stockpiling crude oil for years to prepare for similar scenarios. But given the economic strain from real estate, how much longer can the Chinese market maintain its "composure"? How likely is it to choose to escalate conflict to ensure energy supply?

From Venezuela to Iran, the sequence of these actions increasingly resembles a deliberately designed strategy.

The "rimland" is making a comeback.

Next, there are the chain issues at the market level:

· How bad will Monday's opening be? The first round of declines is primarily from short-term funds and retail investors buying put options. When will long-term funds start to think volatility is uncontrollable, forcing them to sell off or hit risk limits?

· Last week, hedge funds quickly covered their positions on "going long on AI hardware and shorting software." But with rising oil prices, falling bonds, tightening liquidity, and compounded by Gulf helium supply chain risks (key raw material for chip manufacturing), will these be enough to reprice expectations for the AI acceleration cycle?

· Before the conflict, the U.S. economy showed nearly zero growth in the first quarter. With energy prices soaring, disposable income is being consumed by gasoline, heating, and aviation fuel—will households cut back spending or further leverage?

· The Federal Reserve minutes show the policymakers have begun discussing tightening policy to cope with energy-driven inflation pressures. A new round of discussions on "how to deal with negative supply shocks" is unfolding. In the face of such a large-scale energy shock, can the Federal Reserve still "choose to ignore"?

Ultimately, these questions point to a larger "chain reaction."

The "rimland" strategy addresses the problems of energy and the dollar but does not resolve the entire system supported by energy. The market is currently only pricing for the "first node" and has not transmitted to the "second node." Oil prices can be rapidly revalued due to news, but agricultural production cycles do not follow suit. Urea prices remain at $700, and the USDA projects wheat planting acreage will hit a new low since 1919—this will not reverse just because two diplomats shake hands. Those farmers who couldn't afford fertilizer in March cannot "replant" in April.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。