Written by: RWA Research Institute

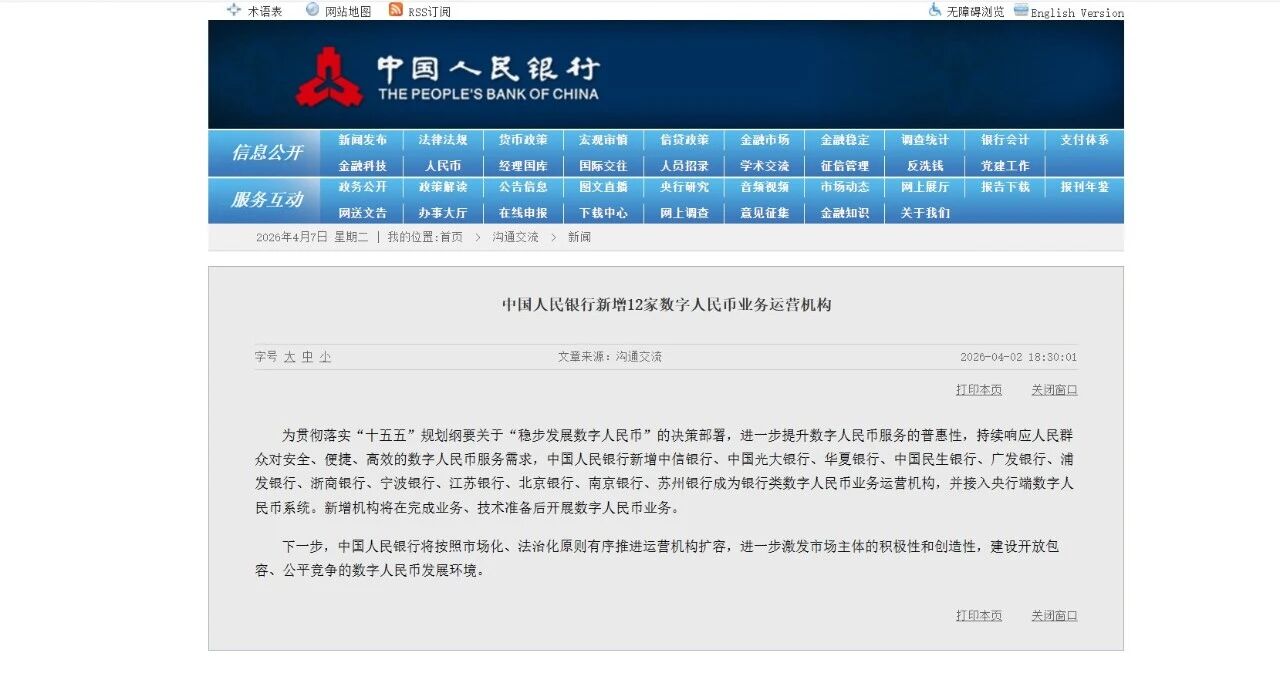

On April 2, 2026, the website of the People's Bank of China issued a message: 12 new banking institutions for digital yuan operations were added, and connected to the central bank's digital yuan system. Once the news was released, the number of digital yuan operating institutions increased from 10 to 22. This seems merely like an official announcement, but behind it lies a key turning point towards the large-scale popularization of China's legal digital currency.

Twelve banks, thousands of engineers, and billions of system inputs—a silent transformation in digital finance is quietly occurring in the machine rooms and backend code of system development.

Let's rewind time to over two months ago. On January 1, 2026, the new generation digital yuan measurement framework, management system, operation mechanism, and ecosystem officially began implementation. Lu Lei, vice governor of the People's Bank of China, pointed out in an article that according to the institutional arrangement, the digital yuan in commercial bank wallets is based on accounts as commercial bank liabilities, marking the transition of digital yuan from cash-type version 1.0 to deposit currency-type version 2.0. The change from "digital cash" to "digital deposit currency" signifies a substantial transformation in the legal and economic attributes of digital yuan.

The digital yuan train has moved from 1.0 to 2.0, and now, the tracks have been laid for more banks.

1. From "Digital Cash" to "Digital Deposit Currency":

A complete identity reshaping

To understand the significance of this expansion, we must first comprehend the complete identity reshaping brought about by digital yuan version 2.0.

The research and development of digital yuan dates back to 2014. Over more than a decade of pilot exploration, digital yuan has been positioned as "digital cash" (M0), with no interest payments. This positioning is theoretically rigorous, but in practice has led to two significant problems: insufficient user holding willingness, as holding cash yields no returns; and severely lacking promotional motivation for banks, as promoting digital yuan effectively "expels" deposits from the bank's balance sheet, with banks investing substantial human and material resources without economic returns.

In December 2025, the People's Bank of China issued the "Action Plan on Further Strengthening the Digital Yuan Management Service System and Related Financial Infrastructure Construction" (hereinafter referred to as the "Action Plan"), which mechanismatically clarified that digital yuan will transition from the digital cash era to the digital deposit currency era. According to the "Action Plan", banking institutions may pay interest on customers' real-name digital yuan wallet balances, adhering to self-disciplinary agreements on deposit interest rate pricing. Furthermore, banks can autonomously carry out asset-liability management for digital yuan wallet balances, with deposit insurance legally providing security equal to that of deposits.

What does this mean? When digital yuan starts to earn interest, it no longer remains a "pocket change wallet" stored in a smartphone, but instead transforms into a genuine deposit. From a user perspective, holding digital yuan comes with revenue incentives; from a bank's perspective, digital yuan deposits become a fund source available for utilization, significantly enhancing the intrinsic motivation for commercial promotion.

This is a fundamental institutional change. Digital yuan has upgraded from a mere payment tool to an interest-bearing, manageable currency form that can be incorporated into the financial safety net, beginning its institutional embedding into the banking system and monetary finance structure. This arrangement not only promotes the innovative development of digital yuan but also effectively prevents potential financial risks, highlighting a prudent monetary governance approach.

2. A promise from ten years ago, fulfilled a decade later

This expansion is not a sudden policy surprise. As early as October 27, 2025, Pan Gongsheng, president of the People's Bank of China, had already issued a clear signal at the 2025 Financial Street Forum Annual Meeting: The People's Bank will further optimize the digital yuan management system, research and improve the positioning of digital yuan within monetary levels, and support more commercial banks in becoming digital yuan operating institutions.

A mere six months later, twelve banks officially "entered the scene."

From the initial 10 to the current 22, this number reflects the institutional evolution of the dual-layer operating system for digital yuan. Reportedly, there were previously 10 designated operating institutions for domestic digital yuan, comprising six state-owned large banks (Industrial and Commercial Bank of China, Agricultural Bank of China, Bank of China, China Construction Bank, Bank of Communications, Postal Savings Bank of China) and two joint-stock banks (China Merchants Bank, Industrial Bank), as well as two internet banks (WeBank, MyBank). The newly added 12 banks—China CITIC Bank, China Everbright Bank, Huaxia Bank, Minsheng Bank, Guangfa Bank, SPD Bank, Zheshang Bank, Ningbo Bank, Jiangsu Bank, Beijing Bank, Nanjing Bank, Suzhou Bank—include 7 national joint-stock banks and 5 leading urban commercial banks.

It is noteworthy that among the 12 newly added institutions, 5 are based in Beijing, namely China CITIC Bank, China Everbright Bank, Huaxia Bank, Minsheng Bank, and Beijing Bank. A relevant official from the Beijing Municipal Financial Office stated that Beijing will coordinate with the People's Bank of China to promote the system construction of newly added operating institutions and develop digital yuan application scenarios, continually supporting the construction of the digital yuan operation management center, and enriching the digital yuan ecosystem.

From "national team leadership" to "multi-party co-construction", this represents not just an expansion of the digital yuan ecosystem's radius, but a clear declaration of the direction of market-oriented reform.

3. The "last mile" of the dual-layer architecture

As of the end of November 2025, the digital yuan handled a total of 3.48 billion transactions, with a cumulative transaction amount of 16.7 trillion yuan; through the digital yuan App, 230 million personal wallets were opened, and 18.84 million digital yuan unit wallets were established. Compared globally, these figures show a leading position among central bank digital currency projects. However, the other side of the coin is that under the coverage of 10 operating institutions, the reach of digital yuan has not truly penetrated local governmental affairs, small and medium-sized enterprise settlements, or the "capillary" level of inclusive finance.

Industry insiders believe that the current push for expansion primarily aims to streamline the dual-layer operating system, incorporating more joint-stock banks and city commercial banks to address previous issues of insufficient participation and promotional motivations. Chief economist Dong Ximiao of China Merchants and CMB analyzed that the digital yuan adopts a "central bank–operating institution" dual-layer architecture. Previously, only a few institutions served as operating entities, so this inclusion of some joint-stock commercial banks and leading city commercial banks is timely and necessary.

Joint-stock banks and city commercial banks have large customer bases, local governmental cooperation resources, and differentiated service capabilities. Their addition will help improve the dual-layer operating structure of digital yuan, forming a richer ecosystem and service capabilities. Some experts believe that from a financial structure perspective, the deep involvement of joint-stock and city commercial banks will extend the issuance layer of digital yuan from state-owned large banks to a broader network of small and medium-sized banks, benefiting the construction of a multi-tiered liquidity allocation and exchange system and significantly enhancing the inclusiveness and resilience of the payment system.

This is akin to the transportation network of a city, where high-speed rail handles rapid transport, while buses and community shuttles ensure passengers reach their final destination. Previously, digital yuan operating institutions were concentrated among state-owned large banks and two internet banks, analogous to having only the "main lines"; now, with the addition of 12 new members, "capillaries" leading to neighborhoods and alleys are being laid. Without those capillaries, digital yuan would always be on the way; but with the capillaries, it can truly enter the pockets and lives of the people.

4. After entering the field: Opportunities come with challenges

The news of the expansion is exciting, but being added to the operating institution list does not mean immediate commencement of business. The People's Bank of China has made it clear that the newly added institutions will commence digital yuan operations after completing business and technical preparations.

This statement carries significant weight. For the 12 newly qualified banks, it means completing a series of full-process construction tasks, including system development, joint debugging tests, acceptance check, production launch, and customer-facing operations. More critically, the core change in stage 2.0 is that wallet balances are included in the bank's balance sheet liability management; thus, the digital yuan system needs to transition from a traditional "channel access layer" to an "asset-liability management layer," and this is not a simple new system build.

Developing digital yuan business represents a comprehensive elevation involving technical capabilities, business models, and organizational collaboration for operating institutions. In the short term, the focus is on system access and scenario construction; in the medium term, it is on ecological operation and value transformation; and in the long term, it is on strategic layout deeply integrated with digital financial infrastructure. Commercial banks need to systematically advance from the perspectives of strategic awareness, capability development, in-depth scenario cultivation, and organizational transformation.

The promotion of digital yuan has experienced a shift from "voluntary promotion" to "endogenous drive." Previously, some experts pointed out that promoting digital yuan usage to customers would not only reduce users' deposits in banks but also involve substantial financial and human costs, causing commercial banks to lack intrinsic economic incentives. After the positioning of digital yuan shifts from M0 in 2.0 era, it can break some previous policy bottlenecks, releasing greater potential on the supply side for more innovative explorations in areas such as corporate services and cross-border payments. This also provides a broader commercial imaginative space for newly included operating institutions.

For banks, having operational qualifications and real business return space will significantly enhance their enthusiasm; for the overall development of digital yuan, the expansion can substantially broaden the service coverage, accelerating the transition from pilot phases to regular popularization and laying an important foundation for subsequent ecosystem improvement and large-scale application.

5. Fair Competition and Ecological Prosperity

The central bank explicitly stated in the announcement that, in the next step, it will orderly promote the expansion of operating institutions according to market-oriented and rule-of-law principles, further stimulating the initiative and creativity of market participants, and building an open, inclusive, and fair competitive environment for the development of digital yuan.

This statement is worth careful reflection. "Market-oriented, rule-of-law" and "open, inclusive, fair competition"—these expressions indicate that the development of digital yuan is transitioning from the "pilot promotion" phase to the "institutional construction" phase. Future expansions of operating institutions will not be a one-time action, but a continuous process; the central bank will evaluate institutions based on their risk management levels, technological strength, retail business capabilities, etc. This implies that in the future, more qualified banks may join, and the openness of the digital yuan ecosystem will continue to increase.

When competition between operating institutions shifts from "pilot compliance" to "scenario competition," the breadth of user scenario coverage and service experience will become the key to differential competition. The process of digital yuan transitioning from "usable" to "easy to use, loved to use" will be accelerated by the inclusion of more participants.

In broader fields such as smart contracts, cross-border payments, and corporate settlements, the imaginative space for digital yuan is opening up. Smart contracts will first achieve "penetrating" applications in scenarios requiring high trust and automation, such as prepayment fund supervision, fiscal subsidies, and supply chain finance, forming replicable commercial closed loops. In terms of cross-border payments, leveraging the multilateral central bank digital currency bridge, digital yuan is expected to achieve point-to-point, low-cost real-time settlement in trade settlements. The multilateral central bank digital currency bridge has cumulatively handled 4047 cross-border payment transactions, with a total transaction value equivalent to 387.2 billion yuan, in which digital yuan accounts for about 95.3% of the transaction value across various currencies.

From 10 to 22, it appears to be just a change in numbers, but behind it lies a qualitative change from institutional design to ecological landing of the dual-layer operating structure. As Dong Ximiao puts it, "This is a concrete measure to implement the '14th Five-Year Plan' outline regarding the 'steady development of digital yuan,' which will further enhance the inclusiveness of digital yuan services."

After 22, we are not just looking forward to digit growth. When more banks transform from "bystanders" to "participants," digital yuan can truly move from the top-level blueprint into the pockets of the people.

This is just the beginning.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。