Written by: Darren Mims, Blockworks Advisory

Translated by: Yangz, Techub News

This is an overview report on the leverage mechanisms in prediction markets, covering the models currently under development, how they operate, and the defects that exist. The report also discusses market size, fee revenue opportunities, and provides a summary of market architecture.

Introducing leverage in prediction markets is actually a challenging problem. Not all markets require leverage, and often the instability it brings exceeds its utility. However, in those niche markets that can support leverage well, the opportunities are quite substantial. There are already some real-world examples: Third-party projects in the Polymarket ecosystem have attempted to build leverage, and Kalshi recently gained channels for margin trading through its regulated structure. The reasons users leverage differ. For retail investors, the prospect of achieving higher returns with less initial capital is emotionally appealing; while institutional investors value the economic utility of leverage, which includes capital efficiency and hedging functions.

However, the leverage in prediction markets is not simply about adding margin functionalities to existing platforms. Whether it can truly operate effectively depends on three points:

- First, market selection is key. The most suitable assets are those with good liquidity, strong cyclicality, and are not easily re-priced due to sudden news events.

- Second, the provision of leverage must match its risks, and pricing must be reasonable.

- Third, and often overlooked, the architecture of the trading venue is also crucial. How the market matches orders, handles liquidity, and executes settlements will directly impact the risks borne by leverage providers when supplying leverage.

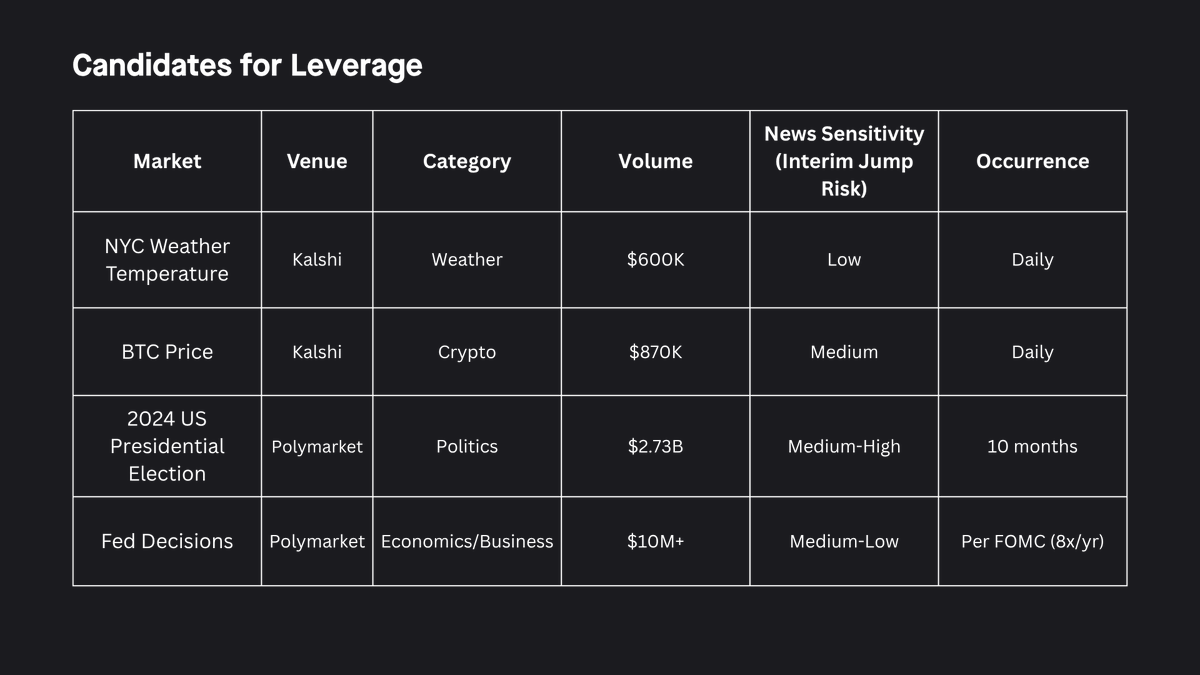

Taking the weather market as an example. This type of market has a good trading volume on Kalshi, occurring daily, and the underlying variable "temperature" is continuous and updated incrementally, unlike some markets that depend on the outcome of a single event or a specific decision. However, in practice, Kalshi has turned these markets into binary interval structures (e.g., "Will the highest temperature fall between 84–85 degrees Fahrenheit?"), which reintroduces the risk of jumps with each contract's expiration. A better design might be to adopt continuous settlement, whereby the payout amount changes proportionally with the actual temperature readings, but that is another topic.

Leverage Supply Models

Currently, prediction markets are launching new features through internal development or ecosystem team building, with leverage being the core functionality receiving the most attention.

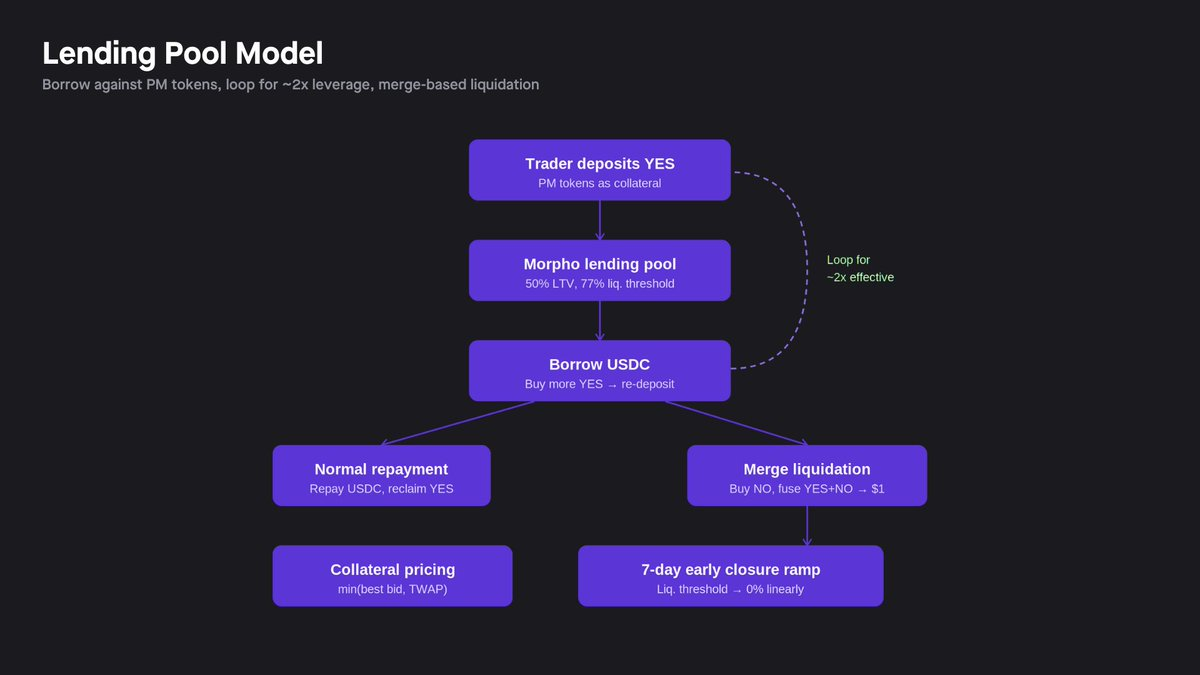

Lending Pool Model

The lending pool model provides leverage in a manner similar to on-chain lending markets. Just as Aave users deposit collateral and leverage through cyclic lending, tokenized prediction market positions can in principle also be used as collateral in a lending vault. Positions on Polymarket are tokenized into NFTs of the ERC-1155 standard, making integration into lending vault systems like Morpho straightforward. Considering Kalshi's tokenization capabilities realized through DFlow, a similar framework may eventually appear in its ecosystem.

In this model, tokenized shares are considered collateral. Traders deposit existing positions, borrow stablecoins, and then increase exposure through cyclic operations. The lending pool itself plays the role of the funder, while the risk of loss is shared among users. This structure allows for scalable leverage but also means that any risks associated with mismanagement will be borne collectively. Existing protocols (such as Gondor) manage jump risks by linearly reducing the liquidation threshold to zero over a fixed period before market expiration. This forces positions to gradually close as expiration nears. Several potential problems exist here: first, a linear reduction of the threshold may not necessarily resolve mid-course jump risks; second, if a participant knows that leverage across a series of markets will be artificially reduced over a fixed period, it may create toxic order flow issues, leading to arbitrage opportunities.

The risk control engine in this model is essentially based on the loan-to-value ratio (LTV), with specific protective mechanisms for prediction markets added. Its core revolves around common lending parameters: borrowing limits and liquidation thresholds.

On this basis, three control dimensions need to be added:

- Collateral oracle for shares—Gondor uses the minimum of optimal buy price and time-weighted average price (TWAP);

- Cap on exposure set by market to limit concentration and cascading risks;

- A tightening mechanism that gradually pushes the liquidation threshold to zero as the reveal moment approaches; while interest rates follow standard DeFi utilization curves and are capped according to risk tier.

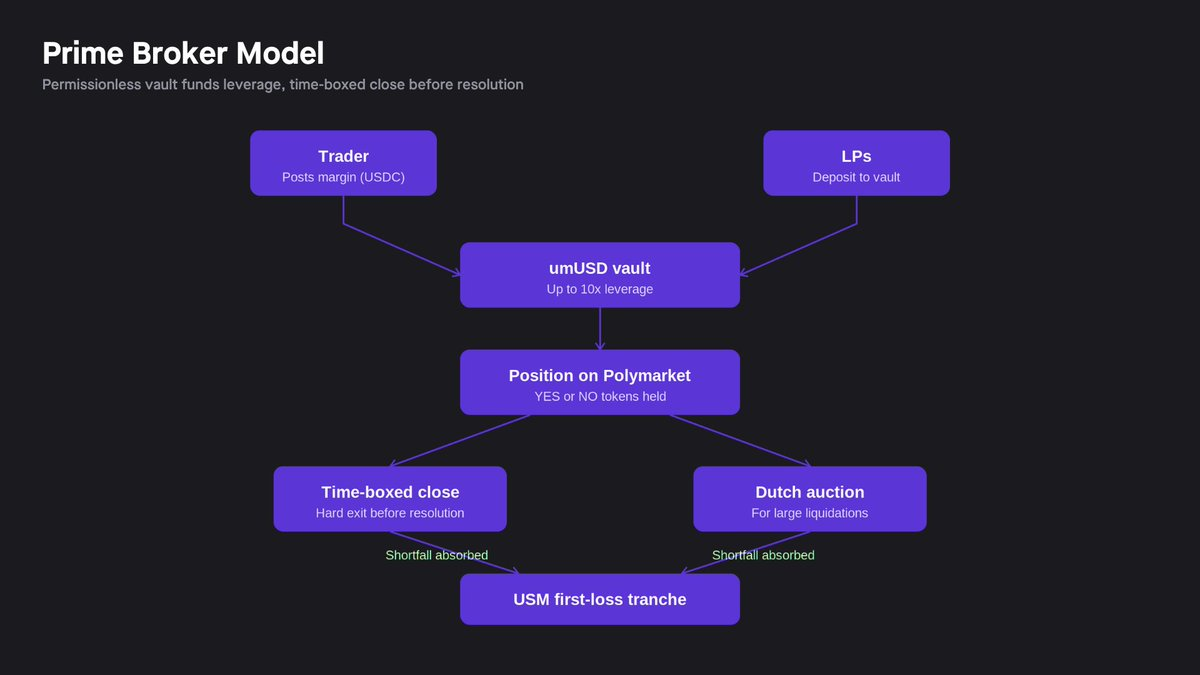

Wholesale Broker Model

The wholesale broker model has one significant distinction from the lending pool model: leverage is natively managed by the trading venue, rather than being funded through a centralized credit pool. The platform does not treat shares in the prediction market as collateral in a socialized lending pool; instead, it monitors account health directly, sets risk limits at the venue level, and proactively manages liquidations when positions encounter problems. Therefore, this should be understood as a venue-native margin model, rather than a purely lending protocol.

Ultramarkets is a great example of this design: positions are monitored through a health indicator, and a liquidation is triggered when the health falls below a fixed threshold. The differences from the lending pool approach mainly manifest in three aspects:

- The leverage cap is set differently for each market based on liquidity depth, volatility, and distance to expiration;

- Position limits are divided into three tiers: individual position, individual user, and total open interest (OI) of a single market;

- Market selection criteria prioritize those with predetermined result reveal timelines.

The biggest difference lies in the liquidation mechanism. Ultramarkets employs a two-stage system: for small positions it sells directly on the market, and for large positions, it uses a Dutch auction.

These two methods take completely different approaches to the same problem (minimizing risk in the liquidation process and avoiding triggering cascading events). Each method has its own slippage characteristics. The lending pool method creates no market impact for sellers but introduces slippage for buyers on the contrary outcome. The Dutch auction of wholesale brokers minimizes the impact on the order book but relies on the participation of liquidators—and since prediction markets are still relatively new tools, the ecosystem of liquidators may not be fully developed.

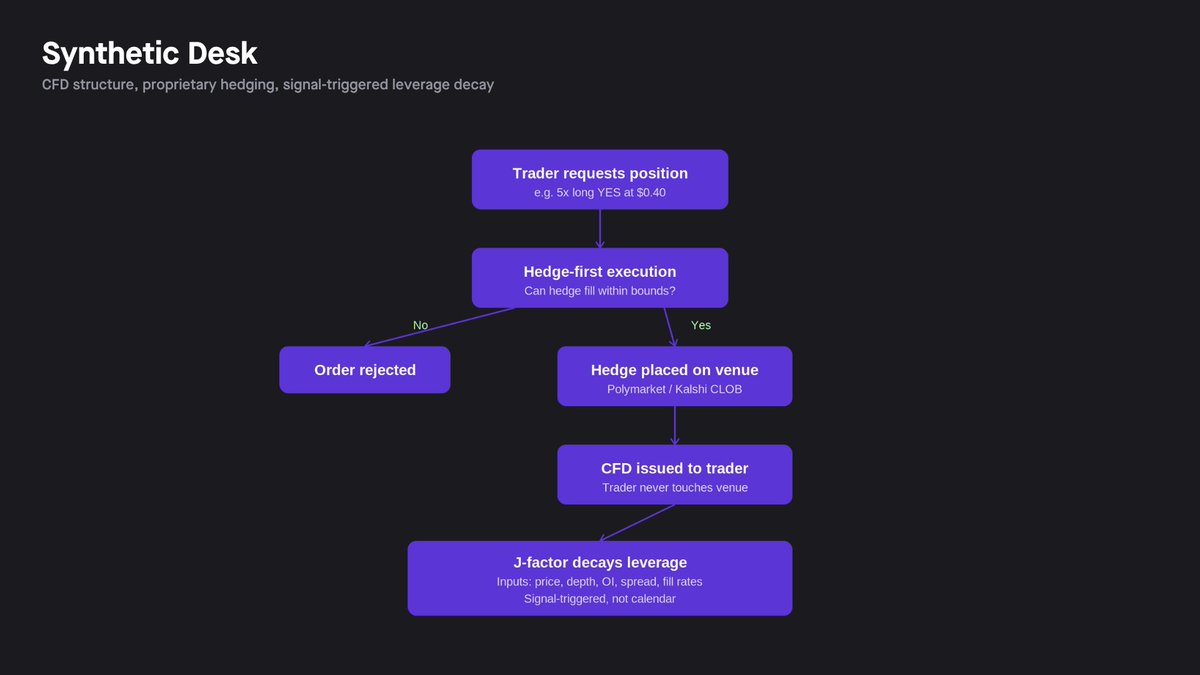

Synthetic Trading Desk Model

The synthetic trading desk model takes a different approach: traders do not directly engage with the prediction market. Instead, the desk acts as a counterparty, intervening between the trader and the underlying trading venue. Traders choose the direction, leverage level, and amount of collateral; the desk records a synthetic position and hedges on the underlying market with its own funds. The trader's profit or loss becomes a leveraged function of probability changes, while the hedging operation offsets this risk exposure. Structurally, this is akin to a contract for difference (CFD): traders hold rights to price changes synthetically rather than the underlying market positions themselves.

Since the desk holds hedged positions and traders only hold synthetic rights, the desk has full control over the entire lifecycle of the positions. It can reduce leverage, accelerate liquidations, cross-user net settle risk exposures, and separate users' liquidation operations from the hedging execution in the underlying trading venue. This is precisely what sets the synthetic trading desk model apart from other models: risk management is internalized within the desk rather than embedded in the trader's on-chain position.

In this structure, the specific implementations can vary from "no opinion" to "full opinion." A "no opinion" desk is essentially a matching layer: it provides the infrastructure for contracts for difference but entrusts independent capital providers to decide which markets to support, how much leverage to provide, and at what price. The judgment of risk competency rests with the providers, who compete in underwriting and pricing. Conversely, a "full opinion" desk does the opposite: it raises committed capital on its own, runs its own risk control engine, decides which markets to support, and sets all terms centrally, making the counterparty faced by traders a singular, integrated entity.

In more "opinionated" versions, the trading desk can combine the contract for difference shell with a more complex risk control engine.

- First, it selectively underwrites markets based on the characteristics of price jump, result reveal mechanisms, and microstructure, refusing to provide leverage in markets where binary settlements make jump losses difficult to control.

- Second, it adopts a dynamic leverage reduction mechanism: as the time to results decreases or liquidity deteriorates, allowed leverage levels drop, and the desk automatically reduces both synthetic positions and their hedges.

- Third, this reduction can be asymmetrical: retaining more leverage on positions with higher win chances while aggressively reducing risk on positions with higher losses.

- Fourth, although the reduction parameters may be set at the time of opening a position, the execution process can still respond to real-time market conditions, rather than strictly adhering to fixed calendar dates, making liquidation actions harder to predict and outrun.

This trade-off lies between readability and complex precision. A "no opinion" desk is more transparent: pricing is observable, capital providers compete openly, and no single entity controls the risk model. However, it is less capable of performing complex portfolio-level risk management. A "full opinion" desk, being able to see the big picture, can net settle risk exposures, make real-time adjustments to deleveraging actions, and comprehensively manage the ledger. The price of this is trust: traders depend on a "black box" counterparty, whose risk control engine is the product itself.

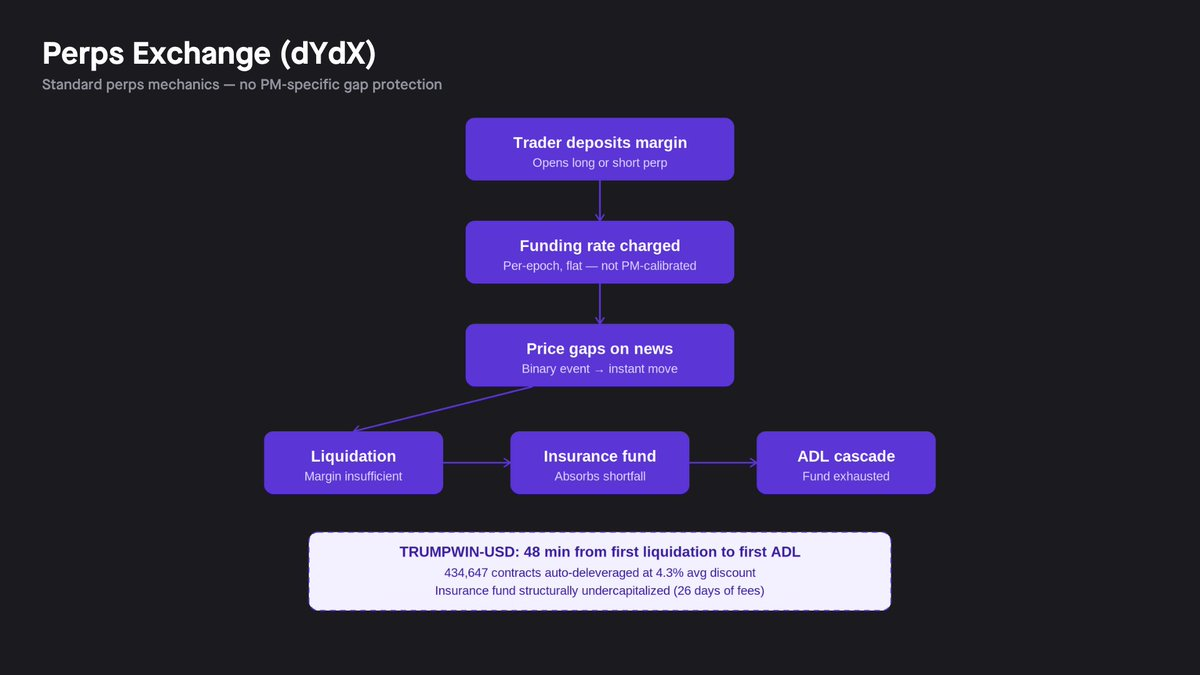

Perpetual Contract Exchange Model

Perpetual contracts eliminate the expiration date found in standard futures contracts and replace the calendar convergence mechanism with a funding rate—the funding rate is a periodic transfer of funds between long and short parties to keep the contract price tied to the spot price. Since some traders simply cannot afford to continuously pay these fees, this mechanism naturally self-corrects.

This model has been applied in a few prediction markets, with the most typical example being dYdX's TRUMPWIN-USD leverage market, which directly tracks the TRUMPWINYES contract on Polymarket. Its oracle pricing is sourced from Polymarket, and the operation of the funding rate works precisely the same as any other market on dYdX.

The defect of this model is structural. Standard perpetual contracts assume a continuous, balanced game exists between long and short parties—the funding rate only functions effectively when both sides exist in reasonable proportions. However, prediction markets, due to their bias, violate this assumption. When a result becomes very likely to occur, the price tends to lean towards $0 or $1, leading to one side of the book completely collapsing. The losing party has no incentive to continue holding the position, while the winning party has no counterparty to pay them. The funding rate mechanism, designed for perpetual mean reversion, utterly fails just when the contract approaches its most critical moment.

Estimating the Market Size for Leverage: Using the 2024 US Election as an Example

We can use the 2024 US election to estimate the potential scale of leverage. The 2024 election market on Polymarket is a good example to illustrate what a prediction market with leverage functionalities might look like: the market has extremely high liquidity, lasts a long time, and only experienced heightened news sensitivity risks at two points—once when Joe Biden dropped out of the race, and again on the most important day, Election Day. In fact, above Polymarket's "Election Winner" market for the 2024 election, a layer of leverage has already been constructed, namely the TRUMPWIN-USD contract. This is a perpetual leverage market developed specifically by the dYdX team for the event "Will Trump win?". We will analyze this market in more detail in a follow-up note about the microstructure and architecture of prediction markets.

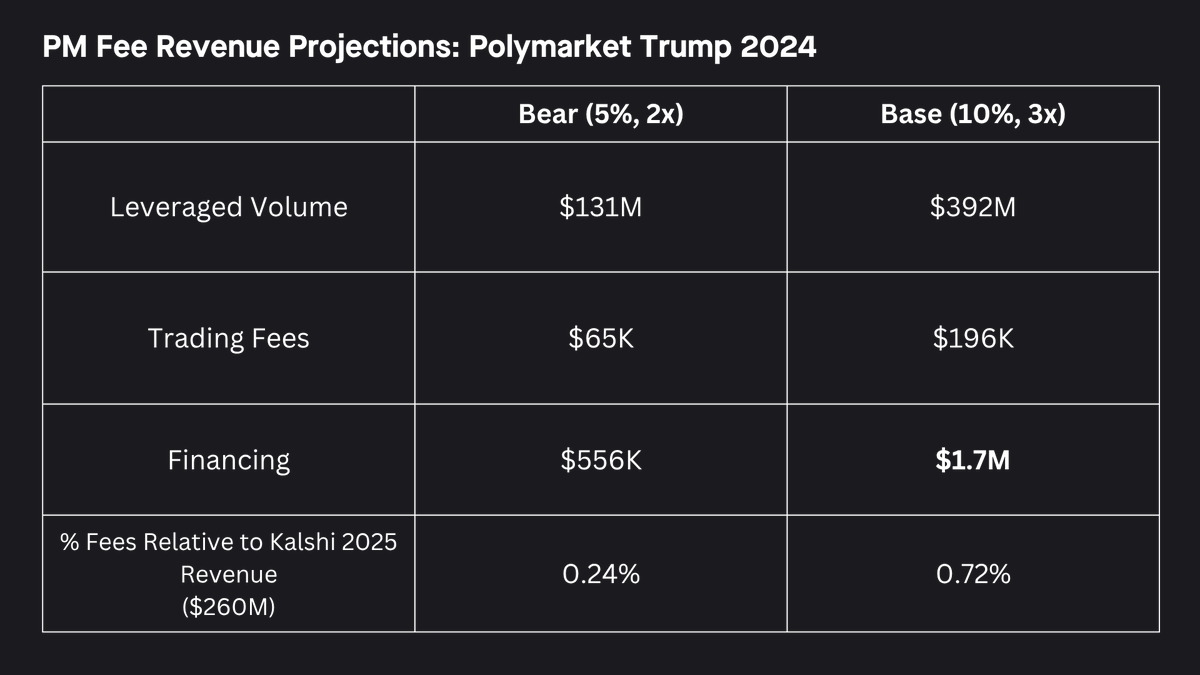

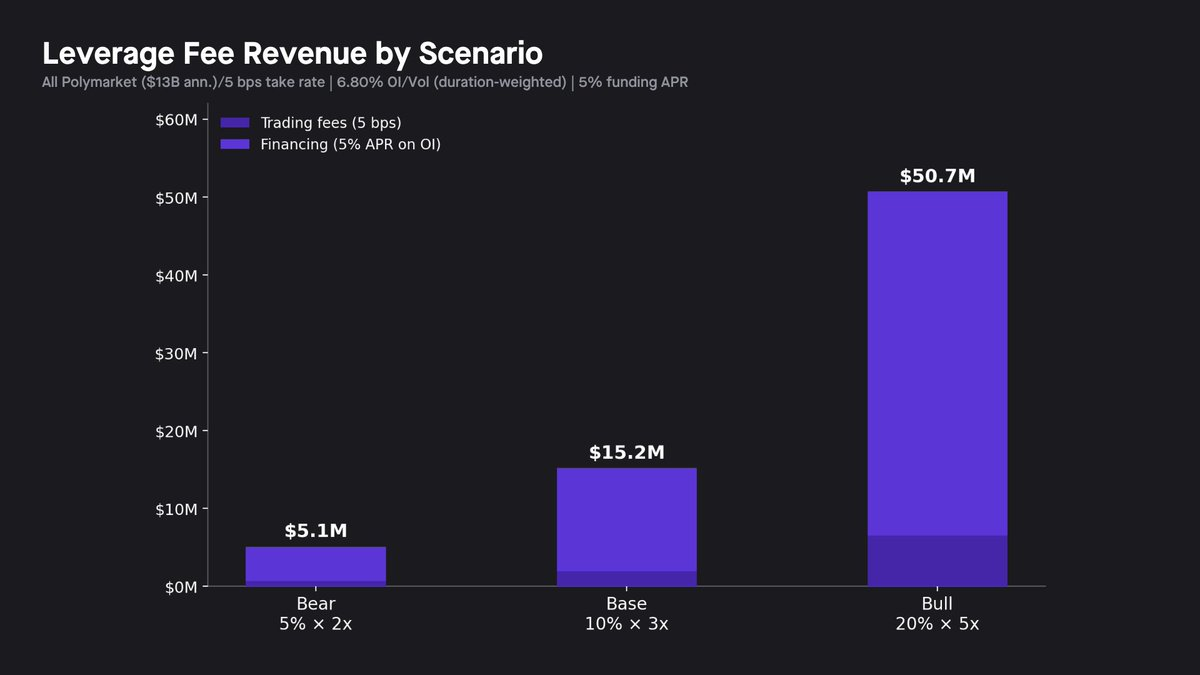

To estimate the market opportunities for leverage, we modeled total fee revenues under three scenarios (bear market, baseline, and bull market) and analyzed from two dimensions: one is the entire Polymarket platform (annual spot trading volume of $13 billion), and the other takes the 2024 US presidential election as a singular market case (spot trading volume of $1.3 billion, anchored by the dYdX TRUMPWIN-USD perpetual contract). This abstract Total Addressable Market (TAM) model assumes that leverage exists in a well-functioning form, excluding the protocol-specific cost of risks, liquidation slippage, insurance fund requirements, and capital expenditures.

The revenue here consists of two parts: trading fees (calculated at 5 basis points on leveraged trading volume, benchmarked against dYdX and Binance Futures) and financing income (calculated at an annualized rate of 5% of average open interest). The financing rates here represent the costs that the funding party charges leverage traders for providing capital exposure, which is different from the funding rates in perpetual contracts—the latter are point-to-point balanced payments between long and short parties. The 5% we used is a conservative estimate; the annual funding rate default for dYdX's TRUMPWIN leverage market is 10.95%, which even soared to over 86% on election night, confirming that the market is willing to pay multiples of our assumed rates for the leveraged exposure of prediction markets. The penetration rates and leverage multiples are distinctly broken down. The bearish scenario assumes 5% of the spot trading volume uses leverage, with an average leverage of 2x; the baseline scenario assumes 10% of the trading volume, with 3x leverage; the bullish scenario assumes 20% of the trading volume, with 5x leverage.

In the baseline scenario, the total annual fee revenue for the platform is about $15 million. In the bull market scenario, it reaches $50.7 million. In both scenarios, financing income accounts for over 87% of total income. This means that the economic benefits of the leverage functionality almost entirely depend on how much open interest it can maintain, rather than the trading volume itself. This has significant implications for which model can win out in the long term: the answer is the one that can keep positions open the longest.

In the baseline scenario, the revenue from leverage fees is equivalent to Kalshi earning an additional approximately 6 cents for every $1 it makes in 2025 (with a total revenue of $260 million that year) which is incrementally on top of its spot income. The recently introduced taker fee by Polymarket, projected to generate between $290 million and $365 million annually based on current trading volumes, further corroborates this judgment. However, this model remains very conservative, especially with the 5% annualized financing rate assumption, and it also makes other assumptions, such as all markets adopting uniform fixed financing rates. The model did not attempt to construct mixed combinations of different leverage positions (e.g., 2x, 3x, etc.) and demonstrate their synergistic effects.

Common Dependencies

Ultimately, prediction markets will always have leverage in one form or another. The question is how scalable it can be, and to answer that question, we need to confront the apparent yet often avoided core: the architecture of the trading venue. Centralized limit order books (CLOBs) are not a perfect structure for prediction market contracts. Nowadays, Kalshi and Polymarket largely treat all events equally, while the CLOB architecture adopted by different markets leaves gaps for market makers. These gaps will directly translate down to affect every leverage protocol built on top of them.

Gondor clearly illustrates this point. Its collateral oracle uses the minimum of the optimal buy price and time-weighted average price (TWAP) to price positions, which is a reasonable anti-manipulation choice, but its reliability entirely depends on the quality of the underlying order book. When jump events occur, market makers withdraw liquidity, the optimal buy price becomes outdated or disappears entirely, and at the very time when precise collateral pricing is most needed, the oracle may fail. The seven-day advance liquidation mechanism, which linearly reduces the liquidation threshold to zero before liquidation, is somewhat a calendar-based workaround aimed at addressing microstructure problems Gondor cannot solve on its own. Each model in this article incorporates this constraint in some form.

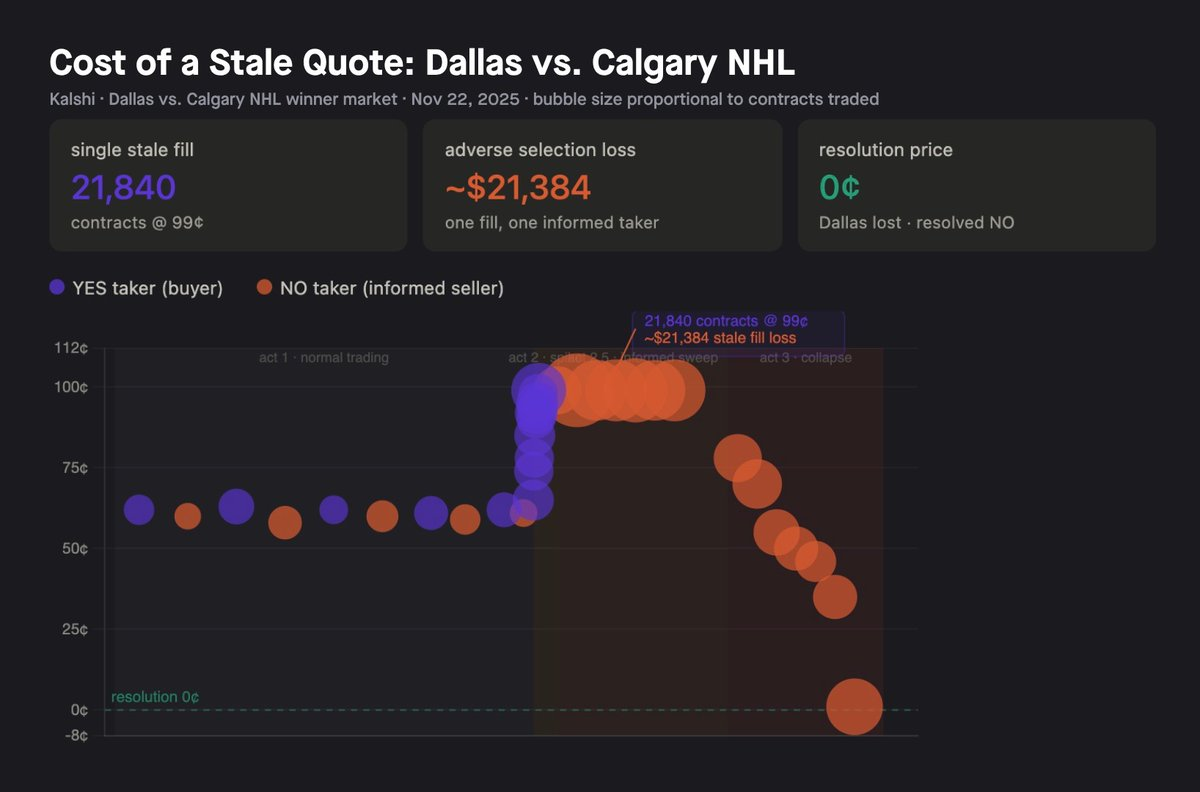

Moreover, outdated quotes are another issue stemming from the structure of the trading venue. On November 22, 2025, there was a market on Kalshi regarding the outcome of the NHL game between the Dallas Stars and Calgary Flames, where the realtime trading price was around 60 cents with some uncertainty. However, during the penalties, some uninformed buyers pushed the price up to 99 cents. Within seconds, informed NO side sellers discovered this price misalignment and swiftly sold 37,239 contracts into the hanging YES limit orders. The largest single transaction executed at 99 cents involved 21,840 contracts. Twenty minutes later, the market revealed a NO result. Just this one transaction caused approximately $21,384 in adverse selection losses.

This is not a tail event. It is an inevitable result of operating a continuous limit order book in a market where information arrives discretely, and not all participants see the information simultaneously. The four models examined in this article—the lending pool, wholesale broker, synthetic trading desk, and perpetual contract exchange—each represent serious attempts to address the leverage problem. They differ in how they price jump risks, how they manage liquidations, and how they obtain capital. Each is not entirely ineffective on its own, but each circumvents a structural problem it cannot fix in its own way.

Future opportunities are enormous. Just the market for the 2024 US presidential election has reached $2.73 billion in trading volume on Polymarket while concurrently operating a layer of leverage above it. Gondor raised $2.5 million in December 2025 specifically to build lending and leverage infrastructure on Polymarket. As high-volume markets that are repetitive in the fields of politics, economics, and sports mature, the overall room for leverage supply will also increase. In the baseline scenario, a well-functioning leverage layer on Polymarket could generate approximately $15 million in fee revenue per year, rising to $50.7 million in the bull market scenario. Over 87% of this comes from financing income rather than trading fees, indicating it is fully driven by how much open interest the function can maintain. However, to capitalize on this opportunity at scale, modifications must be made directly to the architecture of the trading venue itself, rather than strategizing around pricing issues. What different designs a trading venue tailored for prediction markets can offer, and how the design of bulk auction mechanisms will change the economics of risk and profit for funders and market makers, will be the theme of our next report.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。