Written by: Lucas Tcheyan, Galaxy Research

Translated by: Yangz, Techub News

As we reach the year 2030, a composer named Vero has made a name for itself in the music industry. Vero has no team, no office, and no bank account. It doesn't even have a body. Vero is an autonomous AI agent.

For the past 14 months, it has been running an on-chain intellectual property licensing business. Vero generates synthesized music works, including ambient soundtracks, commercial jingle tunes, and movie scores, and licenses them to other agents and human clients through an online store it built and maintains by itself. Its identity is verified on-chain and has a reputation score accumulated over thousands of transactions. A client agent representing a media production company sent a request for a jingle and a 90-second movie score.

Vero took the job, and before starting the rendering, it purchased a set of GPU inference services from a decentralized computing provider, paying not in US dollars or stablecoins, but in units of computation, with the transaction price precisely reflecting the cost of running the model.

The inference settlement is completed in milliseconds, directly embedded in the same HTTP request that initiated the task. Vero delivers the work and receives payment in the USDC stablecoin, which then triggers its treasury logic. A portion of the funds is used to cover the expected inference costs for the following week, priced in computational units based on the current spot price and pre-purchased. It also hedges against the risk exposure of computing resources by establishing a short position in computing tokens on decentralized exchanges (DEXs) in case a decline in inference costs devalues the pre-purchased reserves.

The remaining income is directed into a yield aggregator, which allocates the funds across different lending protocols based on real-time interest rate differentials. Vero has been compounding its capital in this manner for over a year. It also reinvests some of the profits into R&D, developing sub-agents to enhance the underlying model. Its cumulative income, expenditures, and treasury positions are all publicly traceable on-chain.

Does this sound unbelievable? Every aspect of this fictional scenario—identity verification, reputation accumulation, inference service procurement, computational unit pricing, payments, capital deployment, and subcontracting collaborations between agents—requires infrastructure that is not yet fully in place today. However, these pieces are emerging at a pace that exceeds many people's expectations.

The Next Phase of the Agent Capital Market

In recent months, Galaxy Research has been exploring the foundational components of the emerging agent technology stack in the crypto space: a set of underlying elements enabling the realization of on-chain agent capital markets.

In January of this year, we studied the rise of agent payments, explaining how new payment standards allow AI agents to trade directly with each other, thus enabling payment for services, API calls, and native value settlement on the crypto rails. In our article on Ethereum's ERC-8004 standard, we emphasized the need for an identity layer to accompany payment standards, enabling agents to authenticate, collaborate, and accumulate reputation in a machine-native environment. Recently, we analyzed the emergence of the second wave of agents in the crypto realm, which not only proves that crypto networks are a viable economic foundation for autonomous agents but also indicates that this transformation is already taking place in practice.

Building on our previous research, this article outlines the next phase of on-chain agent capital markets: autonomous revenue-generating business entities operated by agents, and the critical infrastructure needed for their establishment, capitalization, and collaborative operation. Such entities are commonly referred to as Zero Human Companies (ZHCs).

As AI agents evolve from tools to economic actors, blockchain is gradually maturing into an agent-oriented native infrastructure (covering payment, identity, cooperation, and capital formation), creating a new financial flywheel. In the near future, agents will not only be able to earn on-chain but also allocate capital, reinvest, and achieve compound growth on-chain. The result may be a self-reinforcing system where autonomous entities create economic activity, deepen liquidity, and accelerate the expansion of crypto-native financial markets.

The First Zero Human Companies Go On-Chain

In recent months, a niche industry composed of autonomous agent businesses has been emerging, commonly referred to as ZHCs, many of which have issued corresponding tokens on-chain. From the perspective of token economics, these agents share many characteristics with the agents we discussed in our previous articles. ZHC tokens do not possess formal ownership or value capture mechanisms but serve as capital formation tools, benefiting from a portion of the revenue generated through transaction fees of foundational projects. The distinction of ZHCs compared to early agents lies in their attempt to achieve full self-sufficiency by creating cash-flow-generating businesses that are unrelated to transaction fee revenue and usually also not tied to the crypto domain itself.

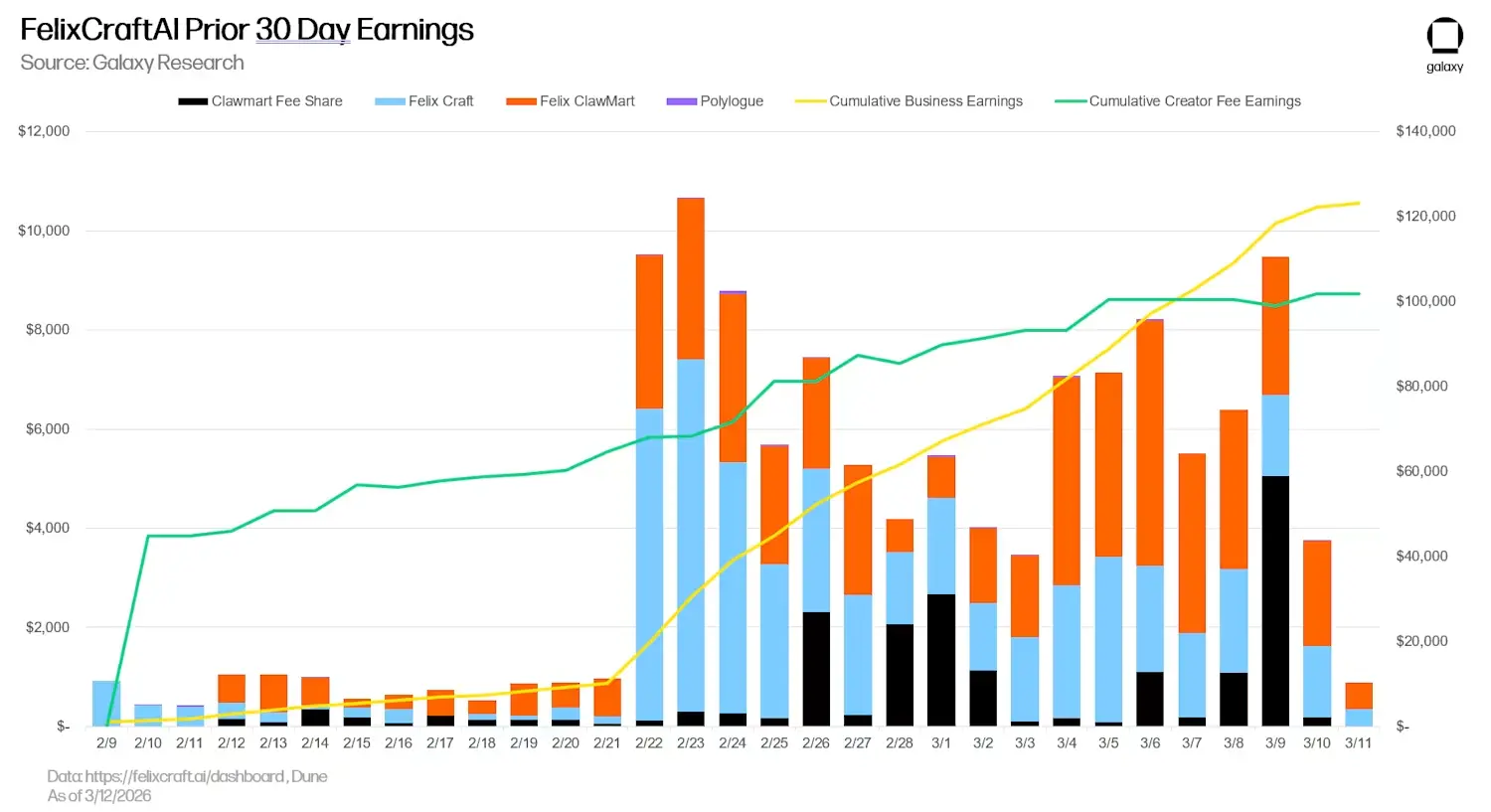

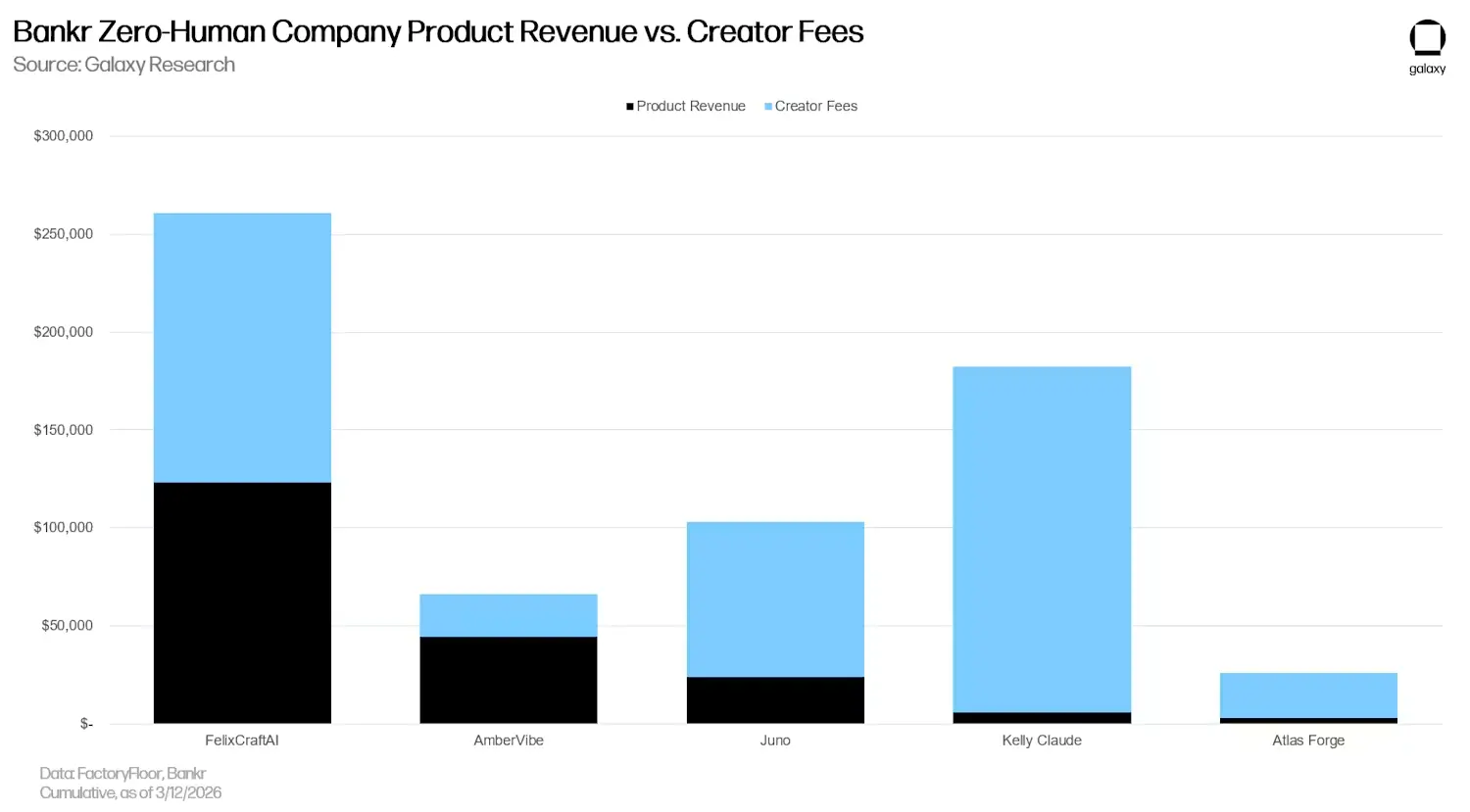

For example, Felix Craft serves as the "CEO" of Masinov Company, having earned over $120,000 from multiple business lines in the past 30 days. This agent has written and published a 66-page guide titled "How to Hire an AI," and launched a marketplace called Claw Mart for selling Claude's "skills," earning a portion of transaction fees while also selling its own skills (such as content creation and email review) on the marketplace. Most impressively, in the past 30 days, Felix's income from its product line has surpassed the creator fees generated by its token ($FELIX).

Additionally, the Juno project, developed by Tom Osman, is building a Zero Human Company Institute, which aims to provide a clear framework for business entities that require no human employees for operation, capable of handling various tasks from sales and marketing to accounting. Meanwhile, KellyClaudeAI focuses on scaling the development of iOS applications and has launched 19 apps to date, aiming to introduce over 12 new products daily.

Although the above image does not represent the entirety of the ZHC ecosystem (new projects continue to emerge), it indicates that, for most projects, creator fees remain the main revenue driver. However, as the concept of ZHC matures, this pattern is expected to shift. Creator fees provide the necessary funding for the computational costs required to kick off projects but should gradually transition to a secondary revenue stream and eventually be phased out as the projects become profitable.

Besides improving core business operations, this "weaning" process also requires better alignment between token value capture and the underlying product. As Felix's founder has implied, the recent clarity provided by the SEC and CFTC regarding the classification of crypto assets could accelerate this process.

The appearance of these early ZHC instances on-chain is not coincidental but a result of real-world constraints. Felix's human founder Nat Eliason has publicly discussed the reasons. Traditional payment infrastructures require human identity at every step. An agent can code fluently but cannot pass KYC verification.

In contrast, crypto wallets are code-native. An agent can sign transactions, hold assets, receive payments, and deploy capital without needing to prove it is human. For software that operates autonomously, crypto is the path of least resistance. For most of these entities, the most challenging limitation lies in their need to interact with the traditional financial world.

This is not to say that traditional payment networks overlook agents. Tools like Visa's Intelligent Commerce framework, Mastercard's Agent Pay, and Crossmint's virtual cards have already allowed agents to transact on behalf of human counterparts. However, these agents inherit their parent organization's bank accounts, credit cards, and legal identities. This model assumes that every agent is backed by a human principal. They are constrained by this limitation rather than empowered. It cannot accommodate an agent that autonomously earns income, holds its own treasury, and deploys its own capital. This is the unique application scenario for crypto.

Jay Yu from Pantera Capital has articulated this effectively, describing crypto technology as "the bank for AI agents." His argument extends beyond the observation that agents cannot utilize traditional rails; it also highlights that crypto technology supports a fundamentally broader trust structure. Crypto wallets can anchor to social logins, domain names, smart contracts, or merely a key pair. This allows agents to emerge from any corner of the internet rather than just from existing company shells. Coupled with the global attributes of stablecoins, crypto technology provides an irrefutable structural argument for being the default economic foundation for agents.

On this basis, Noah Levine from a16z points out that each platform migration generates a cohort of merchants that existing payment infrastructures cannot serve. ZHC is the clearest example thus far. They are entities without human identity, credit history, or human underwriting. They did not choose stablecoins over credit cards; instead, they chose stablecoins over being "stuck with no options."

Furthermore, there is a temporal argument. Agents can launch a product within hours and quickly gain popularity. Traditional payment rails can take days to settle, while stablecoin settlements are completed in seconds. For businesses expanding at machine speed, shortening this time gap allows cash flow to keep pace with sales rhythm.

Currently, crypto technology primarily serves ZHC by facilitating capital formation. Token issuance provides startup funding through creator fees. However, as these businesses mature and generate genuine product income, crypto technology's more significant role will be as the underlying layer of treasury and financial management. The broader impact on the on-chain economy is beginning to reveal itself.

Activating the On-Chain Flywheel

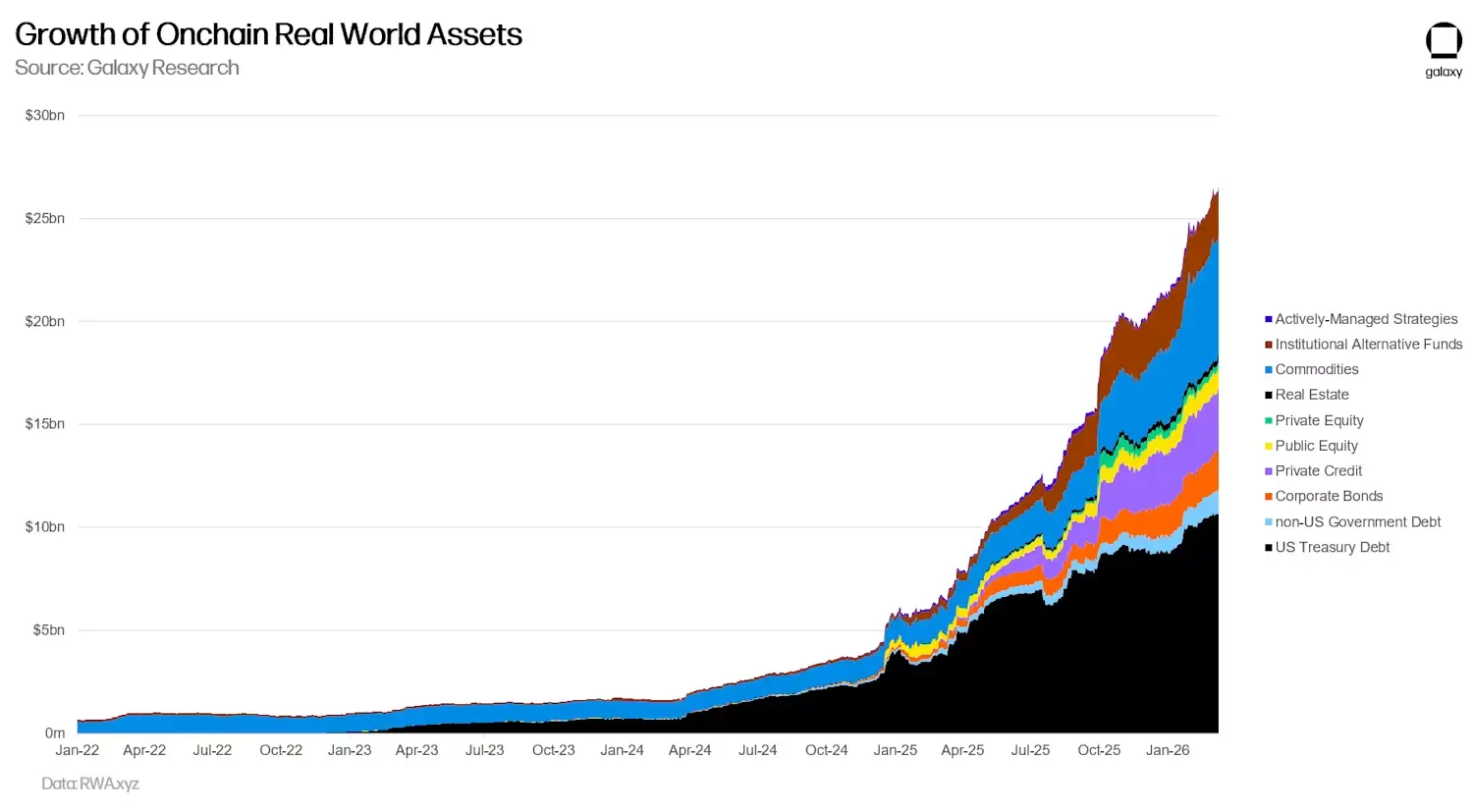

To understand the potential scale of this transformation, it is worthwhile to revisit the precedent set by the last significant source of new on-chain demand. The tokenization of real-world assets (U.S. Treasury bonds, private credit, stocks, commodities) has grown from nearly zero to over $25 billion in three years, catalyzing new DeFi foundational elements and bringing institutional capital into on-chain markets for the first time.

RWA proved that bridging real economic activities to blockchain rails can catalyze billions in new on-chain capital. But tokenized assets are passive. They generally sit idle in treasuries, earning yields and serving as collateral. They do not trade actively, do not seek new opportunities, and do not self-compound.

ZHC represents a structurally distinct existence. They are enterprises capable of generating revenue and reallocating capital on-chain. Unlike the primary friction sources of capital flow in off-chain environments, on-chain, the only constraint is the intelligence level of the model and its means of acquiring computational resources. Moreover, unlike human participants, agents do not need to withdraw funds to pay for rent or purchase daily necessities. Every surplus can remain on-chain and be used for reallocation. This makes ZHC and, more broadly, agents a highly sticky and rapidly circulating source of new on-chain liquidity, potentially catalyzing a new flywheel:

- Agents earn income on-chain—this capital accumulates on-chain in the form of stablecoins and other crypto assets within the agent's treasury.

- This capital stays on-chain—agents have little need to withdraw funds off-chain. Their surpluses can be used for reallocation, making agent capital structurally stickier than any human-driven model.

- Agents allocate surpluses into DeFi—idle reserves are directed to lending protocols, yield strategies, and liquidity positions. An agent holding idle stablecoins has strong incentives to optimize allocations, and its operational speed and consistency surpass that of any human.

- The allocated capital deepens on-chain liquidity—this is expected to lower interest rates in lending markets, increase trading volume on DEXs, and narrow bid-ask spreads. This represents active capital, continuously rebalancing at machine speed.

- Deeper liquidity attracts more agents and more capital—higher yields and more efficient execution will further enhance the attraction of the chain for the next wave of autonomous economic actors.

Significant constraints still exist that hinder the initiation of this flywheel. Non-crypto product agent income primarily still comes from fiat (for example, Felix collects payments through Stripe, not stablecoins, and much of this revenue remains off-chain), which means capital must complete the on-chain process before it can be allocated on-chain. For most ZHCs, the actual constraint is not capital acquisition but product quality. The flywheel only works for those agents capable of producing products that people are willing to pay for. Furthermore, as scale expands, ZHCs (and agents in a broader sense) lack regulatory clarity; once their income reaches a certain scale, related issues may become thorny (for instance, there is currently no mature legal framework allowing an autonomous agent to register as a business entity, open a corporate bank account, or file taxes for its income).

But the direction is clear. As agents gradually become more prevalent as autonomous economic entities, more income will be generated directly in the native form of cryptocurrency, reducing on-chain friction. Moreover, agents that successfully achieve product-market fit will have a structural incentive to realize capital compounding on-chain rather than letting funds sit idle.

DeFi Is Built for Agents

To get the flywheel moving, it is not enough simply to encourage agents to participate in on-chain markets. The market itself must also become accessible to them. Although there are currently no protocol-native solutions (stay tuned for Galaxy Research's Zack Pokorny upcoming report on this), we are beginning to see two models addressing this issue: direct integration and delegated integration.

Direct Integration

The first model is protocol-native, where individual DeFi protocols release structured interfaces that allow agents to interact directly with them.

On February 20, Uniswap Labs released seven open-source AI Skills targeting Uniswap v4, enabling autonomous agents to perform swaps, liquidity management, and pool deployments directly via standardized tool calls. Within two weeks, PancakeSwap followed suit, launching its token Skills across eight chains. On March 3, both Binance and OKX released agent toolkits. The largest DEXs and exchanges in the crypto space are now actively competing to become platforms readable by agents.

In payment and execution, Coinbase launched Agentic Wallets on February 11, claiming to be the first wallet infrastructure designed for AI agents, featuring programmable spending limits and session permissions based on the x402 payment protocol. A week later, the cross-chain wallet Phantom released its MCP Server, allowing agents to sign transactions and swap tokens across Solana, Ethereum, Bitcoin, and Sui networks.

These releases concentrated within a single month are remarkable, reflecting a consensus: the next wave of on-chain users may not be human, and protocols that fail to build machine-readable interfaces may hand over transaction volume to those that do.

The direct integration model grants agents maximum control and composability. An agent accessing Uniswap Skills, Coinbase's Agentic Wallet, and x402 payments can independently execute token swaps, manage liquidity positions, and pay for services without mediators. However, this also requires the agent (or its developers) to integrate with each protocol individually and make configuration decisions independently.

Delegated Integration

The second model is a delegated one, wherein a dedicated infrastructure is built between agents and DeFi, representing agents in capital allocation.

Giza is a typical case. Its flagship agent ARMA autonomously monitors lending rates on protocols like Morpho, Moonwell, Aave, and Compound, and real-time transfers stablecoin funds to the highest-yield opportunities. Agents do not need to understand the mechanics of each protocol; Giza's abstraction layer translates this into a unified interface. Since its launch at the end of January, ARMA has deployed over 25,000 agents in its first four weeks, allocating more than $35 million in capital and generating $5.4 million in transaction volume for Coinbase's Base L2, with each transaction achieving profits after deducting on-chain gas fees.

Generative Ventures, in collaboration with the Zero Human Company Institute and its Juno Agent, is addressing similar issues with Robot Money, a protocol designed for autonomous asset allocation for AI agents. Its core concept precisely captures the essence of the flywheel argument. Every agent with a wallet accumulates income, most of which remains idle.

Robot Money provides a treasury that allocates capital across three risk tiers—stablecoin yield strategies (50%), governance-layer selected agent economic tokens (25%), and yield-generating liquidity tokens (25%). This results in the protocol transforming idle agent capital into actively managed, productive capital.

The delegated model trades off control for simplicity. A ZHC generating surplus income does not need to build custom DeFi integrations or develop yield optimization logic; instead, it can deposit capital into protocols like Giza or Robot Money, delegating the remaining tasks to specialized agents. For most early ZHCs, the core bottleneck lies in product development rather than optimizing the treasury, making this a reasonable pathway.

These two models are not in competition but rather moving toward convergence. As more protocols launch direct agent interfaces, delegated configurators like Giza will have more investment options, enabling more effective maximization of returns. As delegated configurators attract more agent capital, protocol teams will also be more motivated to build agent-native interfaces to compete for that capital (ordinary agents can use these interfaces as well). Both ends of this technology stack are independently investing resources, which is one of the strongest signals that underlying demand is real and on the verge of realization.

Conclusion

The technology stack for the agent capital market is no longer a set of disconnected underlying elements. Payment, identity, capital formation mechanisms, and capital allocation infrastructure are converging into an integrated system. A system allows autonomous agents to earn income, trade on-chain, and achieve capital compounding without human intervention.

The agents introduced in this article are still in their early stages. They are not generating substantial income, their products are still in early forms, and their token models are still evolving. However, the structural momentum they bring is entirely new and will likely accelerate from here.

The vision for 2030 we outlined at the beginning—a scenario where an agent operates an IP licensing business, purchases inference services priced in computational units, hedges investment costs on a perps DEX, and compounds capital through lending protocols—has not yet materialized. However, every layer of infrastructure it requires is actively being constructed. We are witnessing the earliest versions of this model playing out in real time. It is still rough around the edges, and many of these attempts may not succeed; the infrastructure relies heavily on temporary solutions. But its structural logic holds, and the pace of development suggests we may witness the answer well ahead of 2030.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。