Author: Silica Rabbit

In March 2026, AMI Labs, co-founded by Turing Award winner and former Chief AI Scientist at Meta, Yann LeCun, announced the completion of a $1.03 billion seed funding round.

Almost at the same time:

World Labs, founded by Fei-Fei Li, completed a new funding round of about $1 billion

Google DeepMind released the Genie 3 world model

Tesla continues to advance the deployment of the Optimus humanoid robot in factories

These events are not isolated, but together point to a clearer trend: AI is moving from "understanding the digital world" to "understanding and acting in the physical world."

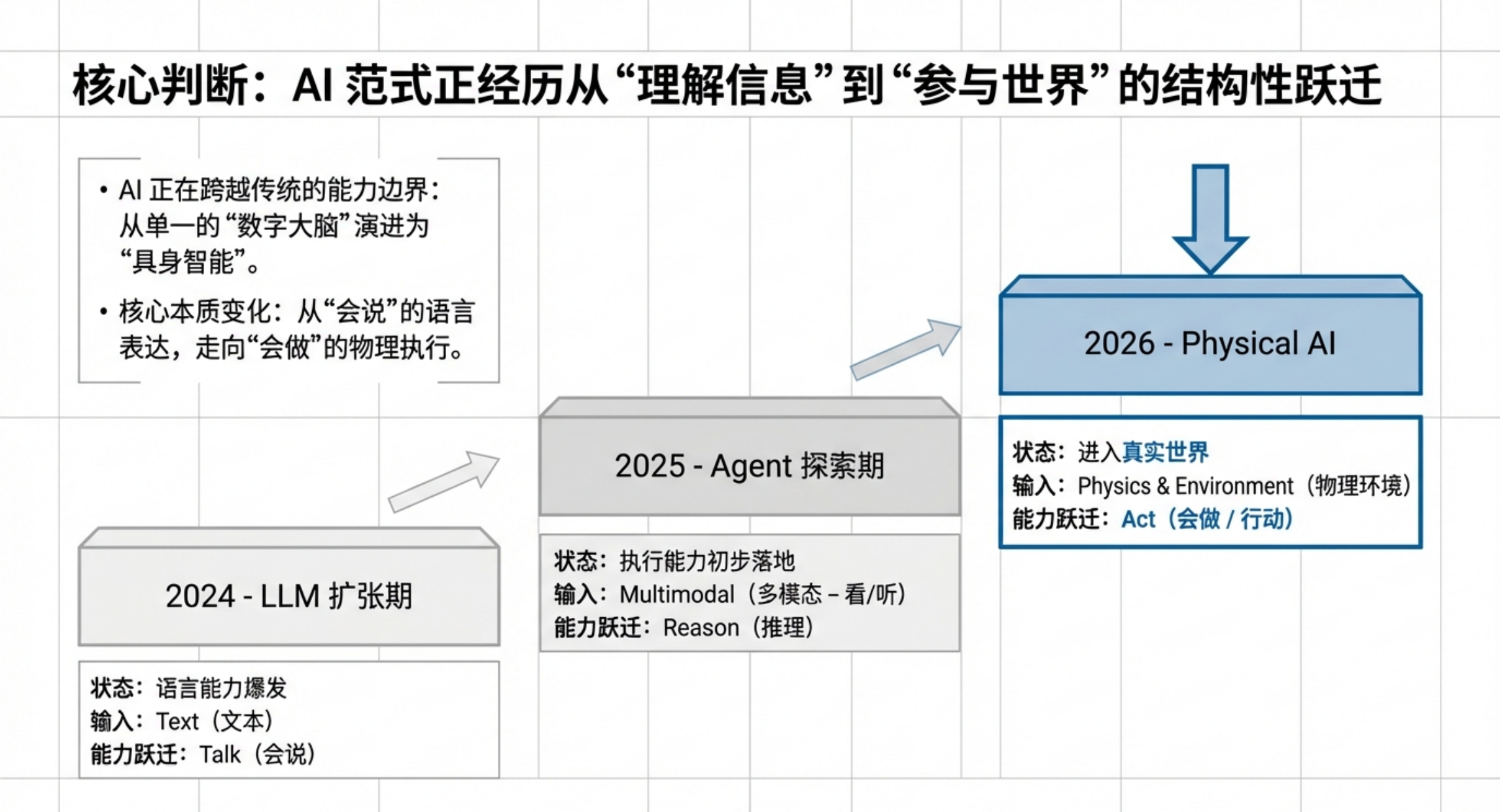

If 2024 is the expansion period for large language models, and 2025 is the exploratory period for agents, then in 2026, the core narrative in Silicon Valley is shifting to a more fundamental question: Can AI truly understand "how the world operates" and perform tasks in reality?

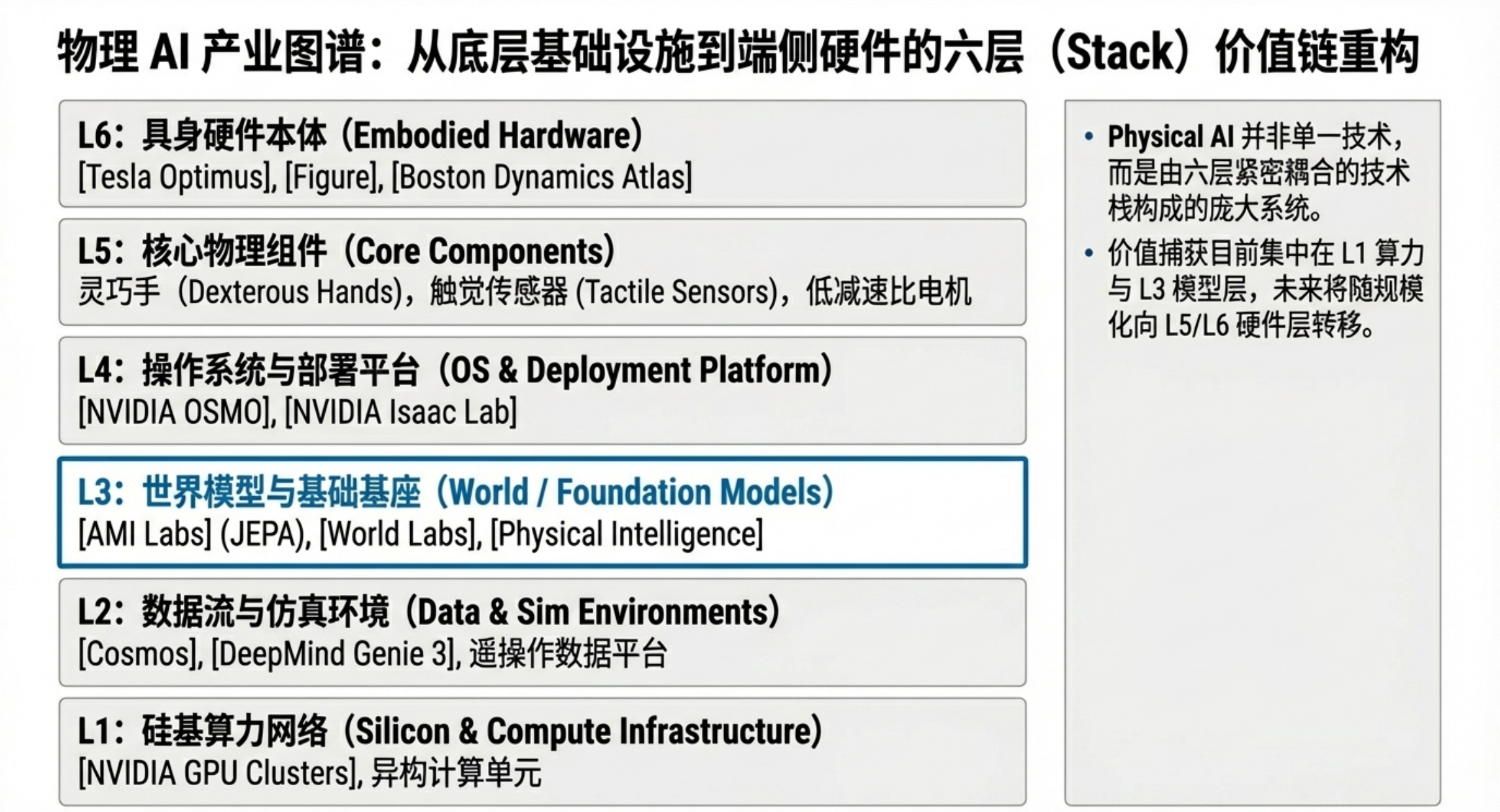

This is not just a change in technical direction; it also means that the industrial value chain is being rewritten. In the past two years, the main battleground for AI competition has mainly focused on a few high-threshold segments such as models, computing power, and data centers; as AI begins to truly enter the physical world, competition will no longer only occur at the model level but will also expand synchronously to the hardware itself, system integration, data collection, simulation environments, supply chain collaboration, and real-world deployment. In other words, Physical AI is not just a breakthrough at a single point but a complete reconstruction of the infrastructure system.

For this reason, this round of changes may represent not only a new wave of technological fervor for the Chinese-speaking world, particularly for Chinese entrepreneurs, engineers, and investors, but also a rare structural opportunity window. Unlike the previous round dominated mainly by large model training resources and super capital, Physical AI inherently relies more on composite capabilities: understanding algorithms and engineering; achieving system collaboration and delving deep into manufacturing, supply chains, and industrial scenarios. Teams that possess both technological depth and hardware collaborative capabilities with Chinese and American industrial perspectives are more likely to occupy key positions in this new cycle.

In other words, Physical AI is not just a new story told in Silicon Valley; it may also be the most important ticket for the Chinese to pay attention to in the next round of global technological infrastructure changes.

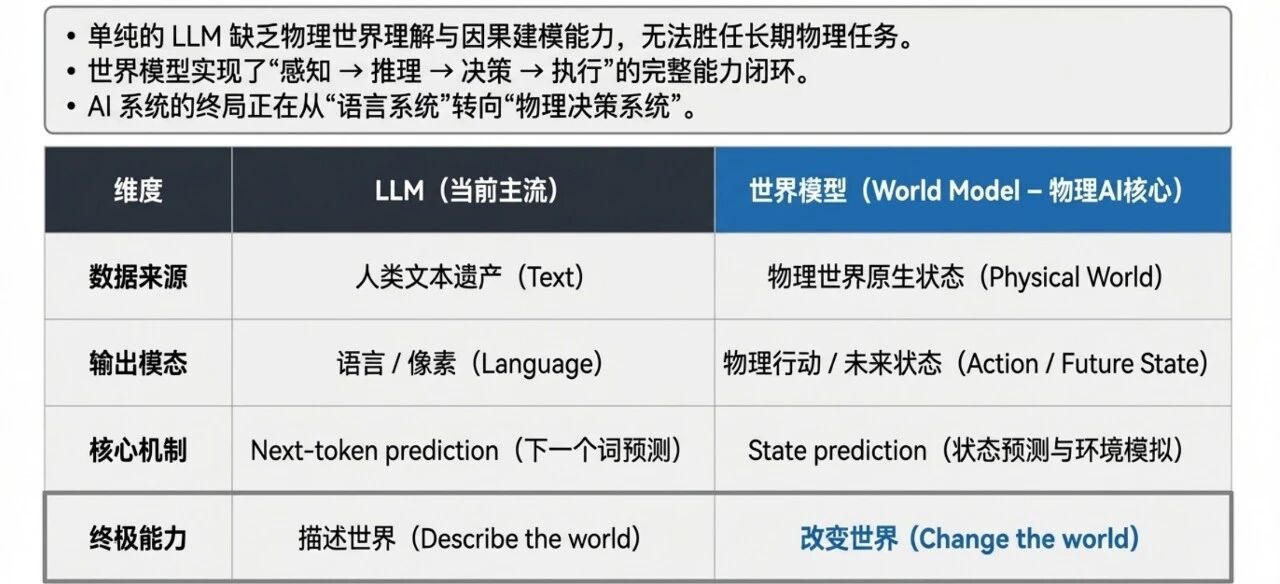

Over the past three years, large language models (LLMs) have dominated the development path of AI, with the core paradigm being next-token prediction based on massive text data. However, the boundaries of this paradigm are gradually surfacing: it can "describe" the physical world but lacks executable understanding; it lacks the ability to model causal relationships and physical constraints; and it performs limitedly in continuous decision-making and long-term tasks.

Thus, a faction represented by Yann LeCun is beginning to promote another path: World Model—predicting "states" rather than "text." The core difference between the two is that the LLM focuses on text as the learning object and uses language as the output form, essentially remaining at the level of "cognition and expression"; while the world model models the state of the physical world, directly aiming at the closed-loop capability of "perception—decision—execution."

This is not just LeCun's judgment alone. In Q1 2026, the world model direction almost simultaneously witnessed several key advancements: AMI Labs clearly bets on a long-term route of "research first, then product" with JEPA as its core framework; World Labs attempts to genuinely understand relationships, occlusions, and physical constraints in the three-dimensional world through "spatial intelligence"; Google DeepMind promotes the generation of dynamically interactive environments through Genie 3 for agent training.

Though the paths of the three companies differ, they point to the same trend: the next leap for AI is not merely about generating better text, but rather about accurately modeling the world and completing actions within it.

The world model addresses the "brain" problem—how AI understands the physical world. But the other half of the Physical AI battlefield is equally intense: Who will build the "body"?

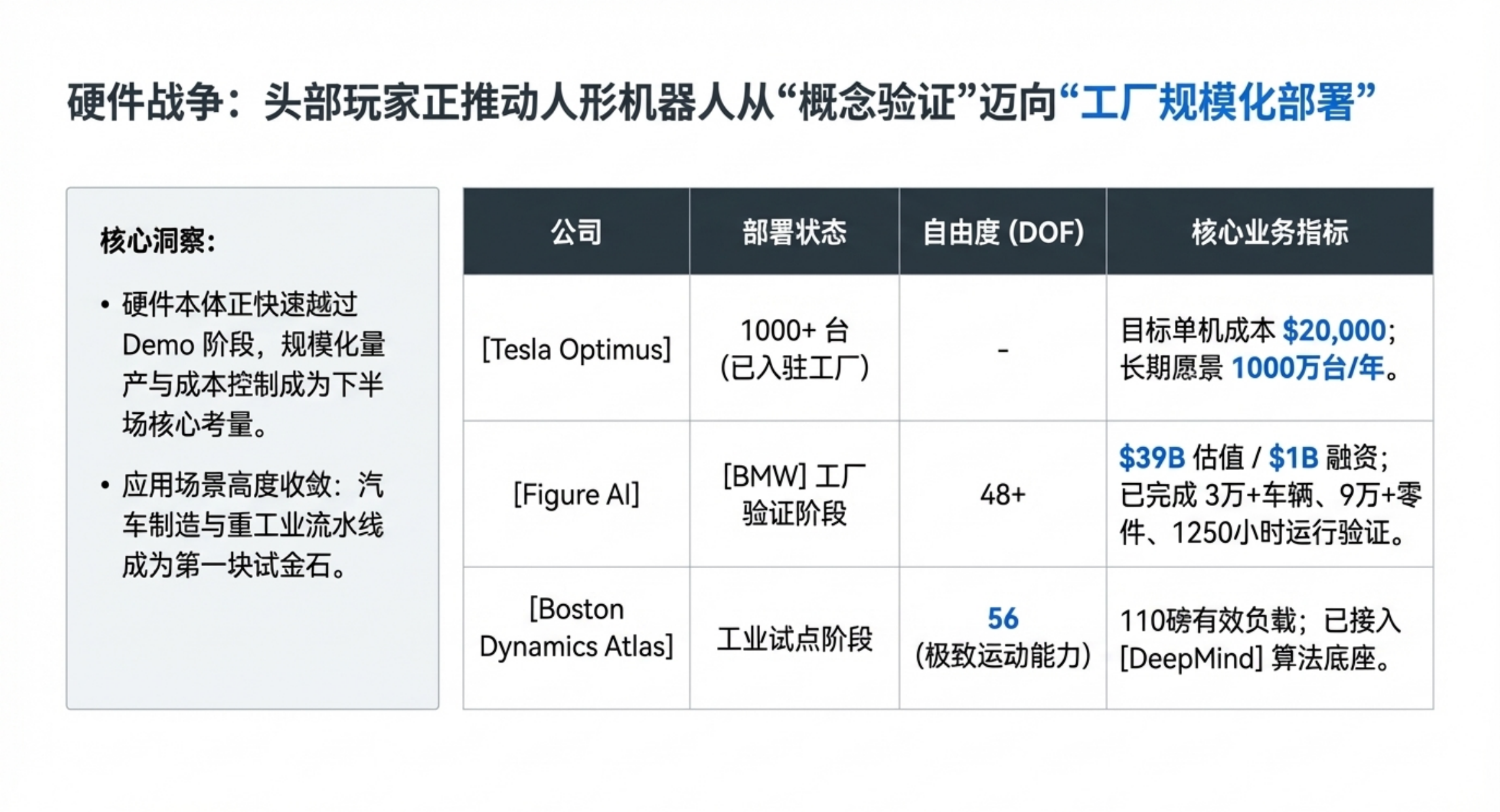

The humanoid robot race in 2026 has shifted from "laboratory demos" to "factory mass production." Here are some key numbers:

Tesla Optimus Gen 3: Over 1,000 units deployed at Gigafactory Texas and Fremont factories for parts handling and assembly tasks. This is the largest deployment of humanoid robots in history. Tesla is building a dedicated factory in Giga Texas with an annual capacity of 10 million units, aiming to reduce the cost per unit to $20,000—two years ago, the industry average was still $50,000 to $250,000.

Boston Dynamics Atlas: The product version of Atlas at CES 2026 stands 6.2 feet tall, has 56 degrees of freedom, and can lift 110 pounds. More importantly, its "soul" is its collaboration with Google DeepMind to integrate cutting-edge foundational models into Atlas. The entire annual production capacity for 2026 has already been reserved by Hyundai and Google DeepMind, with a factory planning for 30,000 units/year underway.

Figure 03: Figure AI raised $1 billion at a valuation of $39 billion, with its Figure 02 involved in the production of over 30,000 BMW X3s during an 11-month trial at the BMW Spartanburg plant, moving over 90,000 parts and accumulating 1,250 hours of operation. Figure 03 has been fully upgraded based on this, equipped with over 48 degrees of freedom and a proprietary Helix AI platform.

Mind Robotics: Just announced a $500 million funding round, focusing on industrial-scale AI robot deployment.

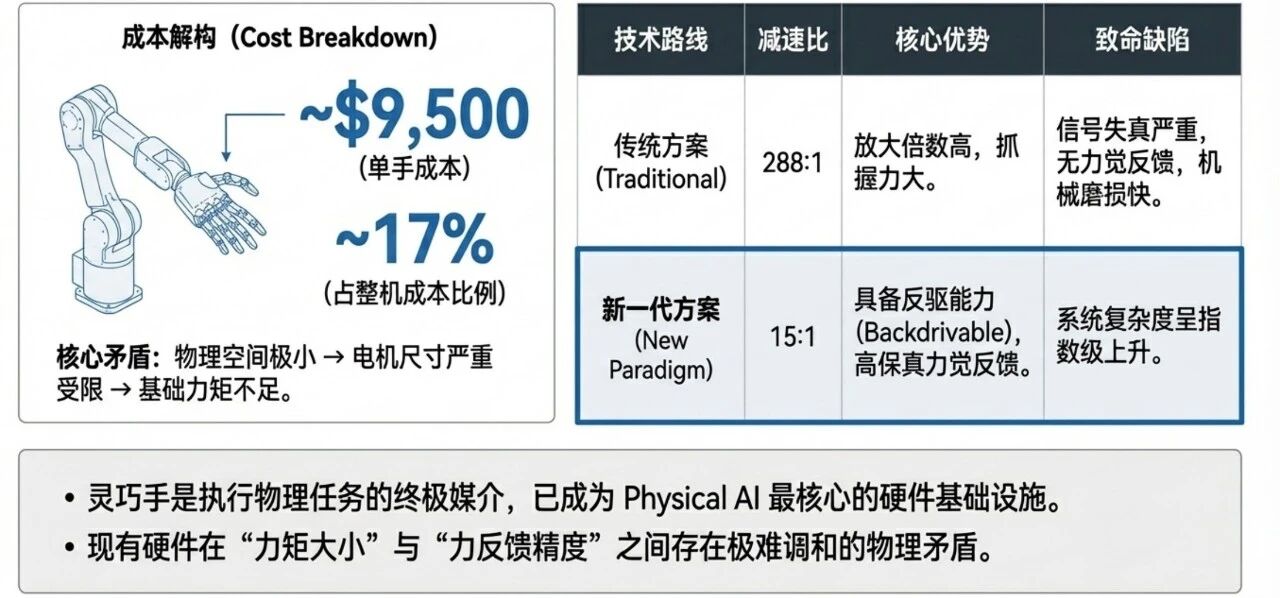

However, in this hardware race, an underestimated link is emerging: the Dexterous Hand.

The legs of humanoid robots solve the mobility problem, and the torso addresses the load-bearing issue, but what truly determines whether the robot can work in complex environments is the hands. For instance, in Tesla Optimus, the hand's cost accounts for 17% of the whole machine, about $9,500—making it the most expensive single component.

The difficulty of the dexterous hand lies in a fundamental contradiction: the finger space is too small to accommodate large motors; small motors do not provide enough torque, necessitating high gear ratio gearboxes to amplify force; however, high gear ratio gearboxes result in inertia distortion, loss of force feedback, and mechanical wear—which can "poison" the AI learning process from a physical standpoint.

A number of new companies are trying to break through this bottleneck. Some adopt an axial flux motor architecture to compress the gear ratio from 288:1 to 15:1, achieving a fully reversible dexterous hand; others utilize synchronized design data collection gloves to transfer human operation data to robot hardware with zero loss. These seemingly small hardware innovations might be among the most critical infrastructure in the entire Physical AI ecosystem.

Every technological wave brings about a "shovel seller."

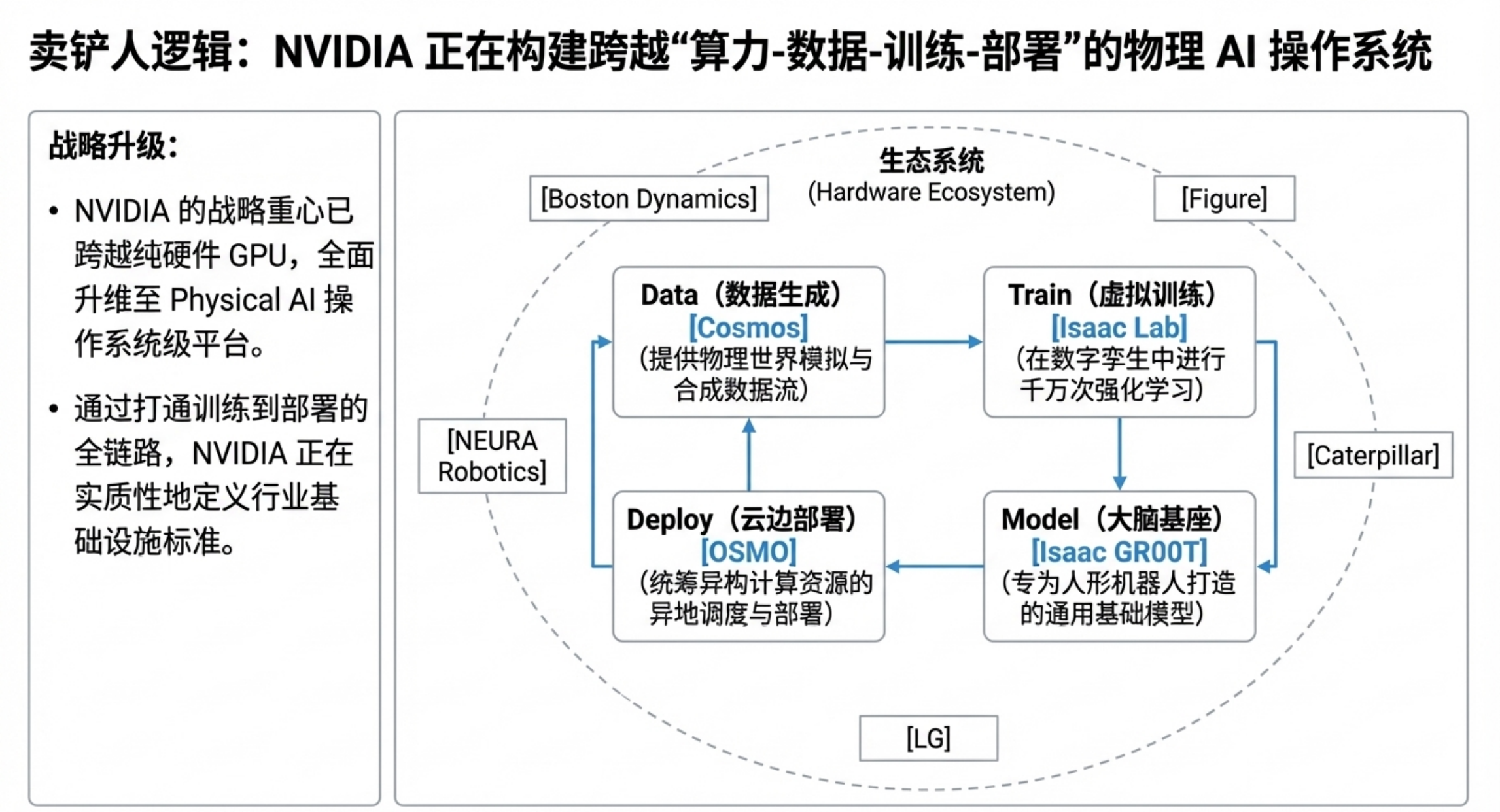

During the era of large models, NVIDIA became the biggest beneficiary with its GPU and CUDA ecosystem; in the Physical AI era, its role is further evolving—not just providing computing power, but attempting to construct a complete infrastructure for the robotics era.

At the GTC conference in March 2026, NVIDIA released a comprehensive suite of platform capabilities around Physical AI: including visual-language-action models for humanoid robots, Isaac GR00T, a series for generating large-scale synthetic data, and a toolchain covering training, evaluation, and deployment (such as Isaac Lab and OSMO). These capabilities are not standalone tools, but gradually form a complete development and operational system.

Multiple robotics companies, including Boston Dynamics, Caterpillar, Franka Robotics, LG, and NEURA Robotics, have already built next-generation systems on the NVIDIA platform.

Its strategy is also very clear:

Not to directly participate in end products, but to become the underlying standard for the entire industry.

If Physical AI is a city under construction, then NVIDIA is simultaneously providing cement, steel, and electricity.

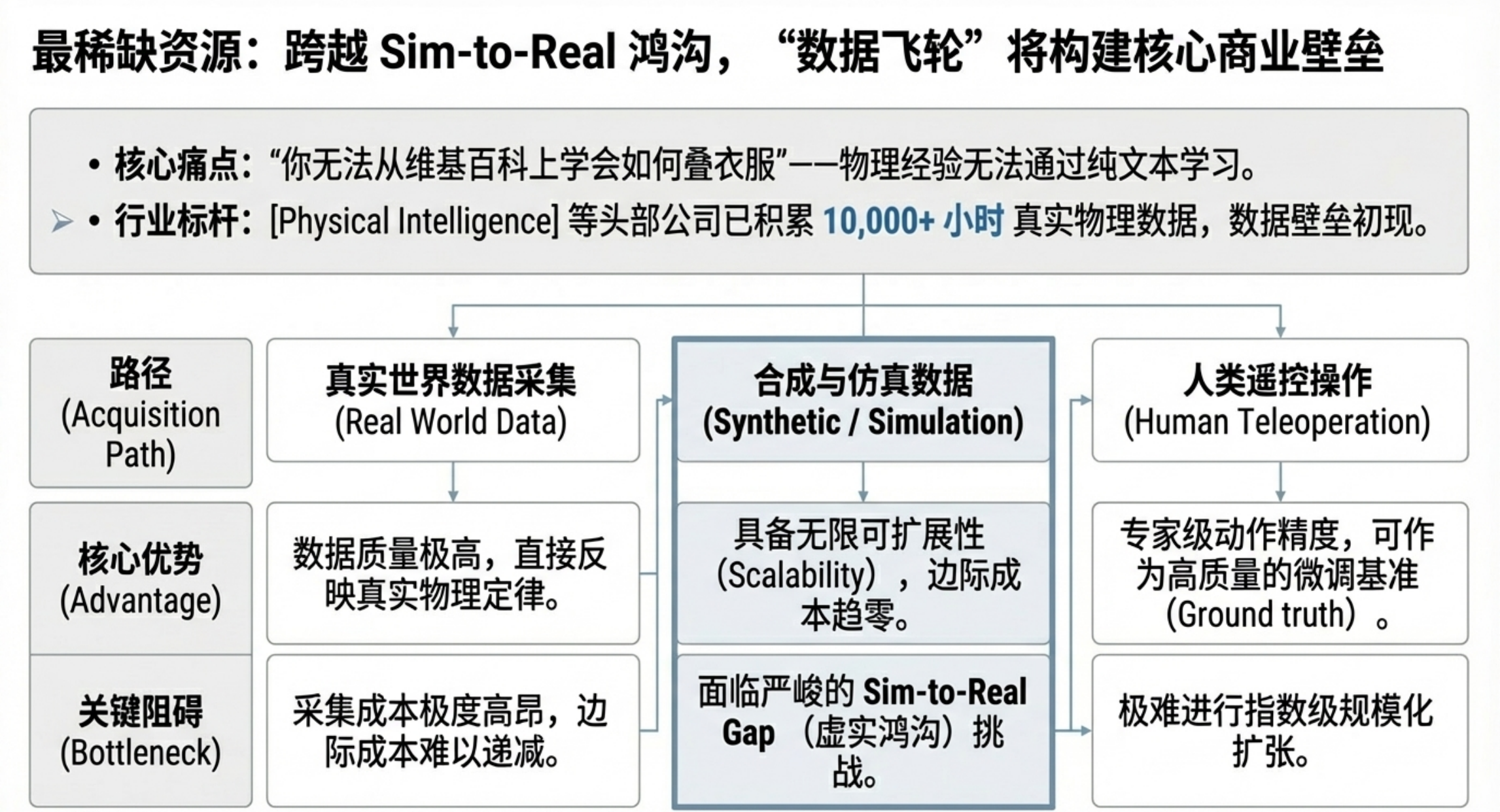

In the world of large language models, the internet provides almost unlimited text data. But in Physical AI, a more fundamental problem emerges:

Real-world manipulation data is extremely scarce.

This makes data one of the most crucial and rare resources across the entire industrial chain.

Currently, the industry is mainly exploring three paths.

Real data route. Represented by Physical Intelligence, its π0 model is trained on over 10,000 hours of real robot operation data covering various robot forms and task types, capable of executing complex operations (like folding clothes, assembling boxes, etc.). Its open-source approach essentially provides the industry with a "manipulation pre-training foundation."

Synthetic data route. Google DeepMind's Genie 3 and NVIDIA's Cosmos attempt to generate large amounts of simulated environments through world models, completing training in virtual worlds before migrating to the real world. The core challenge of this path is the sim-to-real gap, but as simulation accuracy improves, this gap is gradually narrowing.

Human teleoperation route. Using data collection gloves and other devices to directly map human operations onto robotic systems. This method offers the highest data quality, but there are still limitations in terms of cost and scalability.

Tesla is trying a mixed approach: continuously collecting human operation behaviors through factory video to train the motion capabilities of Optimus.

In the long run, the competitive landscape of Physical AI may not depend on whose model is the best, but on who possesses the most and highest quality real-world interaction data. Once the data flywheel starts turning, its barriers will increase exponentially.

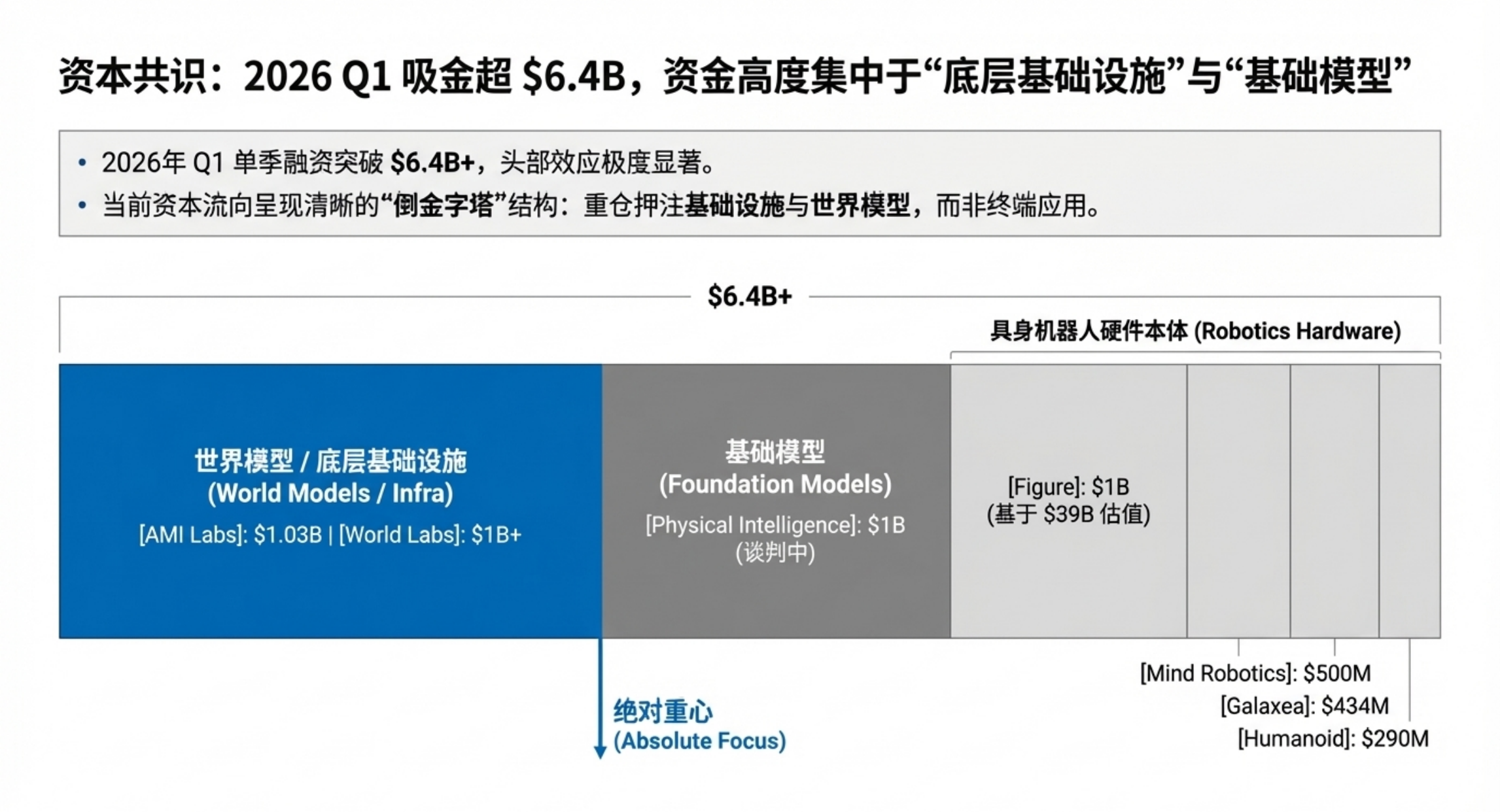

The numbers do not lie. Here are the key financing events in the Physical AI field for the first quarter of 2026:

[World Model Layer]

· AMI Labs (LeCun)— $1.03 billion seed round, valuation of $3.5 billion

· World Labs (Fei-Fei Li)— $1 billion new round, Autodesk invests $200 million

[Foundational Model Layer]

· Physical Intelligence— negotiating for a new round of $1 billion, valuation will exceed $11 billion

· RLWRLD— $41 million seed round extension

[Humanoid Robot Complete Systems]

· Figure AI— previously raised $1 billion at a $39 billion valuation (2025)

· Mind Robotics— $500 million, industrial-scale deployment

· Galaxea— $434 million, Series B unicorn

· Humanoid— $290 million seed round, direct unicorn

· Generative Bionics— €70 million seed round

[Infrastructure and Tools]

· NVIDIA— continuing investment in Isaac GR00T / Cosmos platform

· RoboForce— $52 million, Physical AI workforce platform

From the publicly available data alone, Q1 has already exceeded $6.4 billion. This does not include the internal investments made by major companies such as Tesla, Hyundai/Boston Dynamics, and Google DeepMind.

The flow of capital indicates one thing: Physical AI has already crossed the "proof of concept" stage and entered the "infrastructure construction" stage. Investors are no longer asking "Can the robots be used?" but are instead asking "Whose infrastructure can scale robots the fastest?".

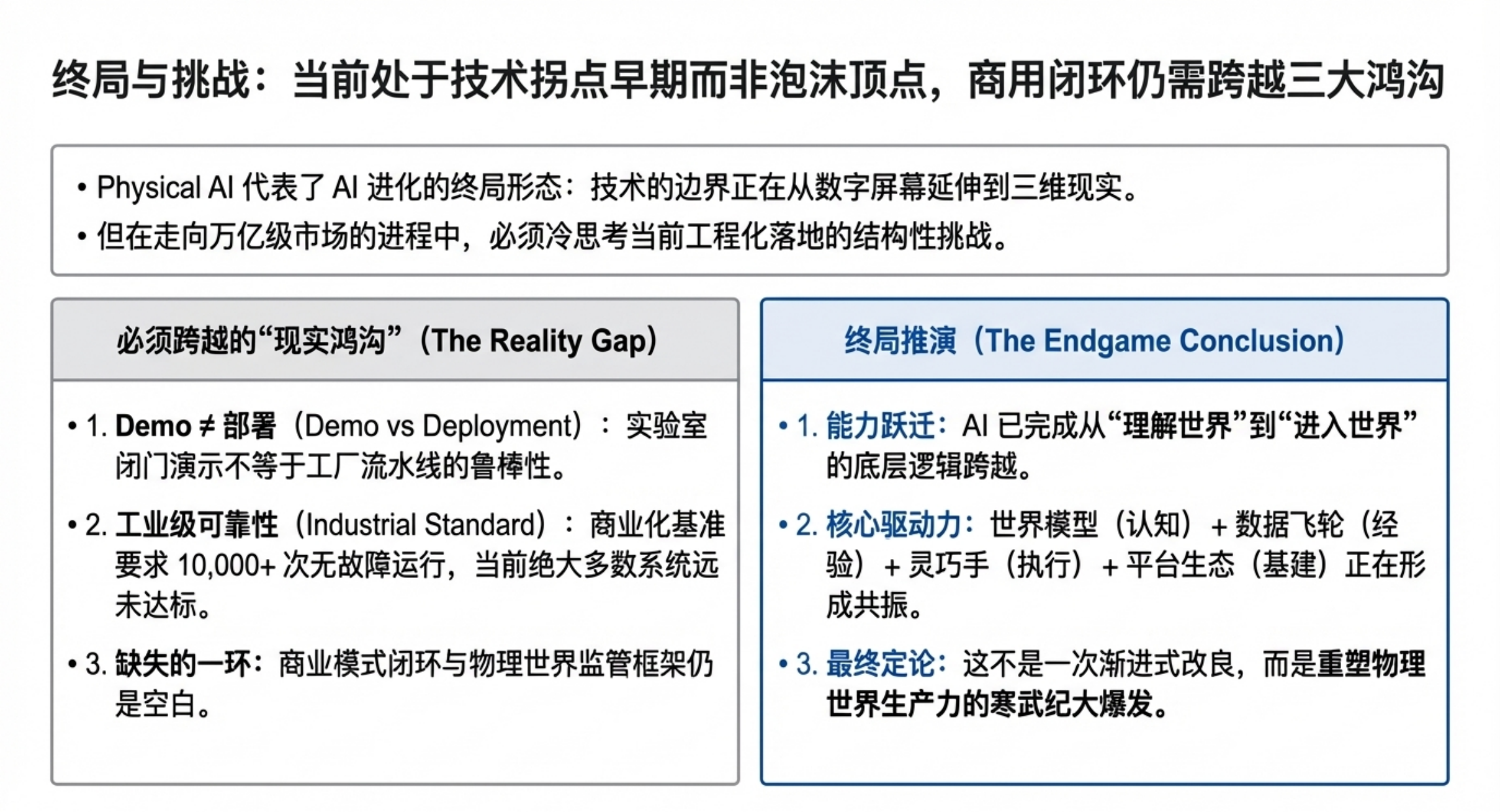

Of course, Silicon Valley is never short of bubbles. In light of the enthusiasm for Physical AI, several calm questions are worth considering:

Demo ≠ Deployment. As industry insiders reached a consensus at Davos 2026: The gap between a brilliant demo and a system that can run 10,000 times without error is much larger than promotional implications suggest. Figure 02 did indeed participate in the production of 30,000 vehicles at the BMW factory, but it was executing relatively standardized parts handling, not dexterous assembly.

Sim-to-real remains a tough nut to crack. The fidelity of world models is improving, but the long-tail complexity of the physical world—lighting changes, material differences, unforeseen collisions—remains the biggest challenge for the synthetic data route.

The business model has yet to work. LeCun himself stated that AMI Labs will only focus on research in its first year. World Labs is experimenting with a free + paid model. Physical Intelligence has open-sourced its core model. Currently, these companies have nearly zero revenue, with capital betting on a paradigm monopoly 3-5 years out.

Safety and regulation are elephants in the room. When thousands of robots with autonomous decision-making capabilities enter factories or even homes, who is responsible for accidents? Currently, the global regulatory framework for Physical AI is nearly blank.

But precisely these questions indicate that we are in the early stages of a technological turning point rather than the top of a bubble. Every true paradigm shift—whether the internet, smartphones, or cloud computing—was accompanied in its early stages by "demos far outperforming products." The key difference lies in whether the underlying technology is genuinely progressing, and not just the presentation.

From LeCun's JEPA architecture, to Genie 3's real-time world generation, to π0's 68-task generalization capability, to the deployment of 1,000 units of Optimus in factories—the advances in Q1 2026 represent substantial engineering breakthroughs, not castles in the air.

Physical AI is not a new track; it is more of one of the ultimate forms of AI.

As AI moves from "understanding the world" to "entering the world," what is being rewritten is not just the boundaries of model capabilities, but also the modes of industrial division of labor and value distribution. Future competition will not only occur in model parameters and computing power clusters, but will also happen in the embodiment of robots, dexterous hands, data collection, simulation systems, industrial scenarios, and supply chain organizational capabilities.

This is also why this round is particularly important for the Chinese.

In the past twenty years, one of the deepest accumulations for the Chinese has never been a single-dimensional technical label, but rather the ability to truly integrate cutting-edge technology, engineering execution, hardware manufacturing, and cross-regional industrial collaboration. Whether entrepreneurs, engineers, or investors and industrial resource organizers, as long as they can catch this opportunity to transition from digital intelligence to physical intelligence, they have a chance not only to participate in the trend but to become part of that trend itself at certain key levels.

In 2026, Physical AI may still be far from maturity; but precisely because it is still in its early stages, the window has just cracked open. For the Chinese, this may not be another round of "following participation," but a new starting point with greater opportunities to deeply engage in the infrastructure layer, platform layer, and key component layer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。