In the early morning of March 9, the situation in Iran escalated. CME was closed, ICE was closed, and major global futures exchanges were all closed. The next official quote for crude oil prices would not come until the Monday morning session, several hours later.

However, the crude oil contract CL-USDC on Hyperliquid did not wait. That day, the trading volume of this on-chain perpetual contract soared from the usual $21 million to over $1.2 billion. Traders used an on-chain protocol to achieve real-time pricing of geopolitical risks during the window when traditional markets were closed.

This event was spread in the crypto circle as another victory for DeFi. But few people asked a more fundamental question: when external markets are closed, where does the price of this on-chain exchange come from?

Where does the price come from when there are no external quotes?

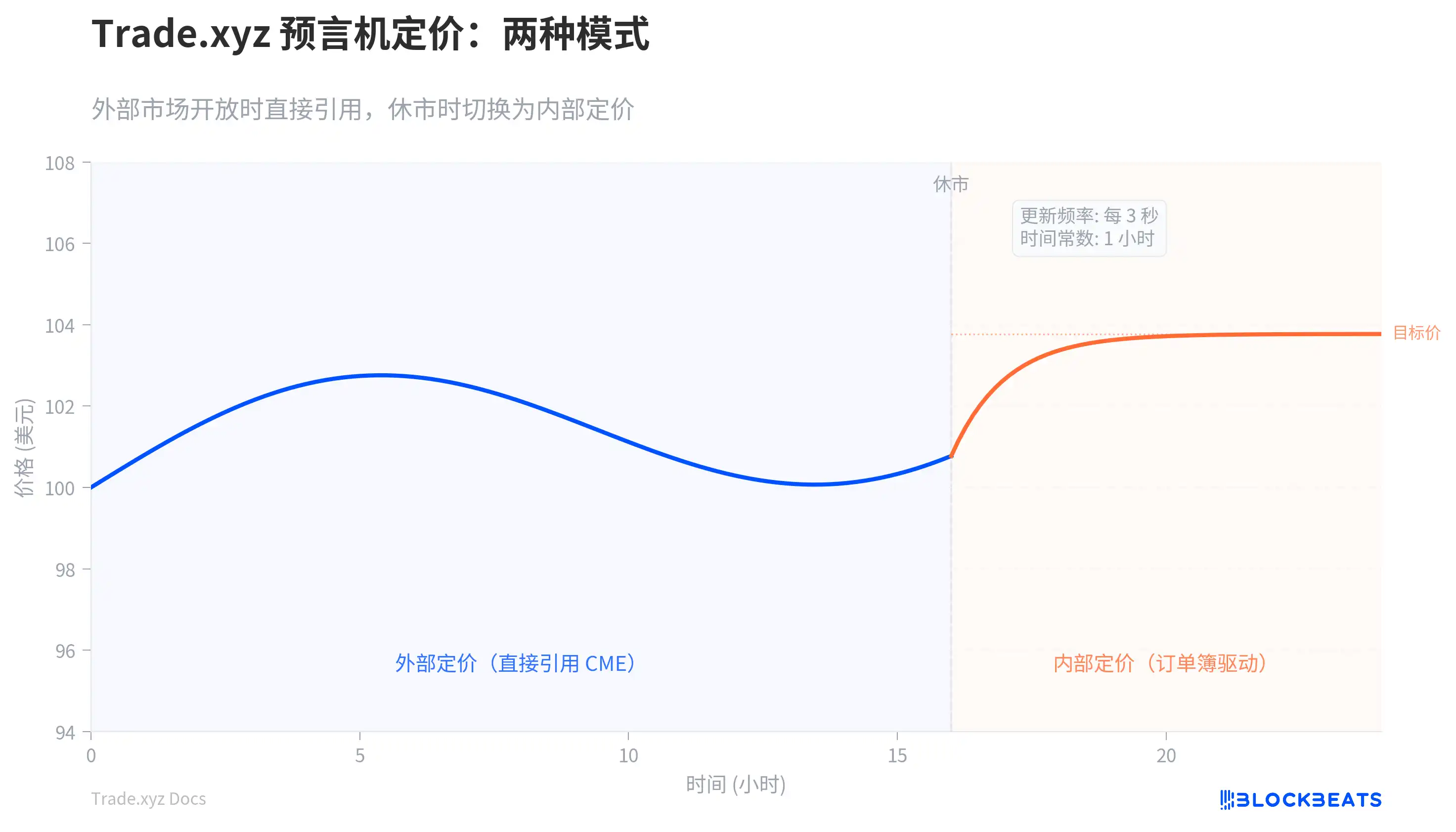

Trade.xyz is the largest provider of traditional asset perpetual contracts on Hyperliquid, operating on the HIP-3 protocol and accounting for 90% of the total open interest in HIP-3. The S&P 500, NASDAQ 100, WTI crude oil, gold, silver, and Korean stocks can all be traded 24 hours a day, 7 days a week. However, the pricing logic for perpetual contracts is entirely different from spot trading. The price on spot exchanges is determined directly by matching buy and sell orders, while perpetual contracts require an "anchor" to tether the contract price to the real price of the underlying asset. This anchor is the oracle.

In the traditional futures market, the pricing anchor is the exchange itself. The price of crude oil futures on CME is the price of crude oil and does not require an additional reference. However, the contracts on Trade.xyz run on the Hyperliquid chain and have no direct connection to the matching engine in Chicago. When CME is open, the oracle on Trade.xyz directly references CME's quotes, which is not technically challenging. The real challenge arises when CME is closed.

Trade.xyz's solution is to extract information from its own order book. The system calculates a “shock price difference,” which simply means: if someone wants to buy a large amount right now, how much higher will the average transaction price be than the current price? If someone wants to sell a large amount, how much lower will it be? This discrepancy reflects the imbalance of buying and selling forces in the order book. The oracle adds this discrepancy to the current price to get a "target price," and then uses a decay function to gradually bring the current price closer to the target price.

The key word is "gradually." The oracle updates every 3 seconds, but each time it only moves a small portion of the gap between the current price and the target price. This movement speed is controlled by a time constant. The larger the time constant, the slower the oracle, making it harder to manipulate, but also less able to reflect real market sentiment.

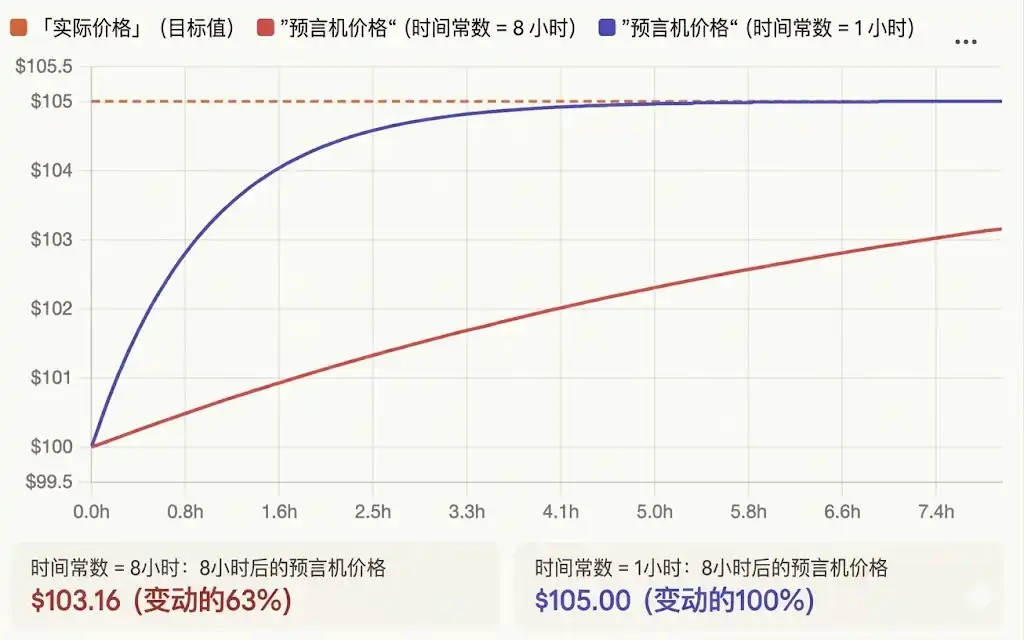

In the initial phase of Trade.xyz, this time constant was set to 8 hours. In November 2025, this parameter was reduced to 1 hour. The reason for the decrease is related to traders’ real capital: Trade.xyz settles funding rates every hour. The oracle was too slow in tracking the real price, and profitable traders would constantly be drained by the funding fees.

As shown by the red line in the figure below, if you went long on crude oil and got the direction right after 8 hours, but the oracle took 8 hours to catch up to the real price, during those 8 hours the price never reached your target (the real price), and your profits were significantly eroded by funding fees.

After the parameter was reduced to 1 hour, the price reached your expected position (blue line) in just 5 hours, enabling the price to confirm your judgment faster and saving on funding fees compared to before.

But a faster oracle also brings new risks. If the oracle stops for 6 hours due to a failure and then suddenly recovers, it would jump to the target price at 99.7% according to the formula. This sudden price jump could trigger large-scale liquidations. Trade.xyz's solution is to add a safety valve: regardless of how long actually passed, each update's effective time difference counts for at most 6 minutes. Even if the oracle recovers after downtime, the price can only catch up a little step at a time.

Cages, re-anchors, and the Monday opening gap

Oracle pricing solved the problem of “how to quote on weekends.” But another question arises: to what extent can prices move freely?

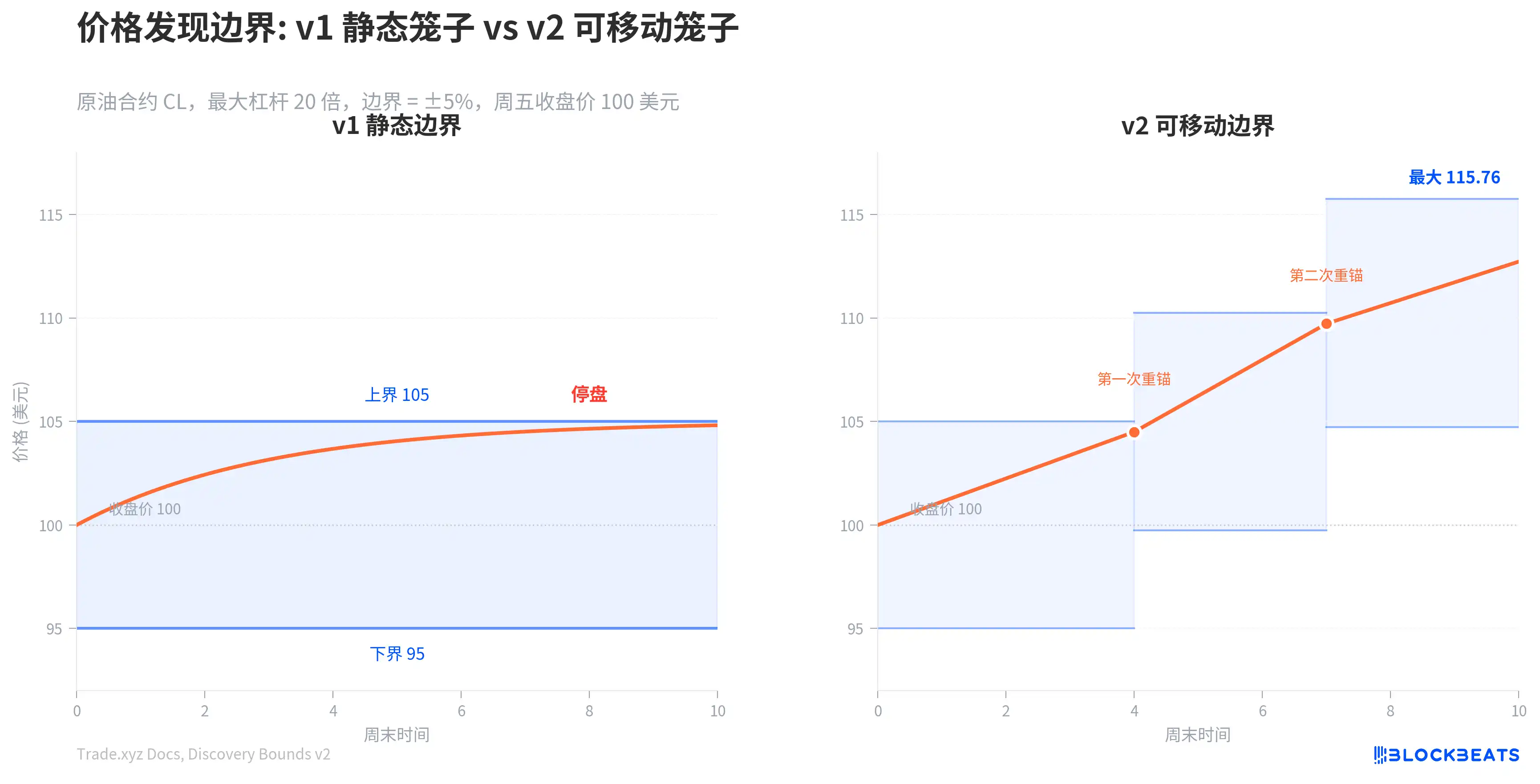

Trade.xyz drew a "cage" for each contract. The marked price is restricted within a certain percentage above and below the last external closing price. This percentage is equal to the inverse of the maximum leverage. The maximum leverage for crude oil contracts is 20 times, so the cage is 5% up and down from the closing price. If crude oil closes at $100 on Friday, the marked price over the weekend can only fluctuate between $95 and $105. If it touches the boundary, trading is halted.

Crude oil contracts halted on weekends in early March

During a normal weekend, this mechanism works well. A 5% range is enough to absorb most overnight fluctuations. However, events of the magnitude of March 9 can push prices directly to the cage boundary. All market information gets suppressed, and when CME opens on Monday, if the real price jumps by 8%, a huge gap will be formed. Short sellers will be liquidated instantly, and market makers will incur losses because they cannot hedge gradually.

In March 2026, Trade.xyz deployed the "Price Discovery Boundary v2" on the crude oil contract. The core change: the size of the cage remains the same, but the cage can move. When the oracle price touches the current boundary at 90%, the system re-anchors the center of the cage to the boundary value, drawing a new cage of the same size around the new anchor point. Up to two re-anchors can occur in each direction.

To put it in concrete numbers: the initial cage is from $95 to $105. When the oracle rises to $104.50, it triggers a re-anchor, and the new cage becomes $99.75 to $110.25. After another trigger, it becomes $104.74 to $115.76, which is the endpoint. From the start of $100, the maximum discoverable range expands to about $115.76.

This design keeps the instant volatility range at 5% at all moments, meaning that market makers' risk models do not need to change. At the same time, re-anchoring means the system "acknowledges" the price movements that have already occurred, reducing the gap at Monday's opening. But the costs are also clear: a liquidation price at -8% for a long position is absolutely safe under v1 (because the price cannot reach -8%), but under v2, it may enter the liquidation zone after a downward re-anchor. Trade.xyz has chosen to deploy v2 on two crude oil contracts first and stated it will decide whether to expand based on the observed effects.

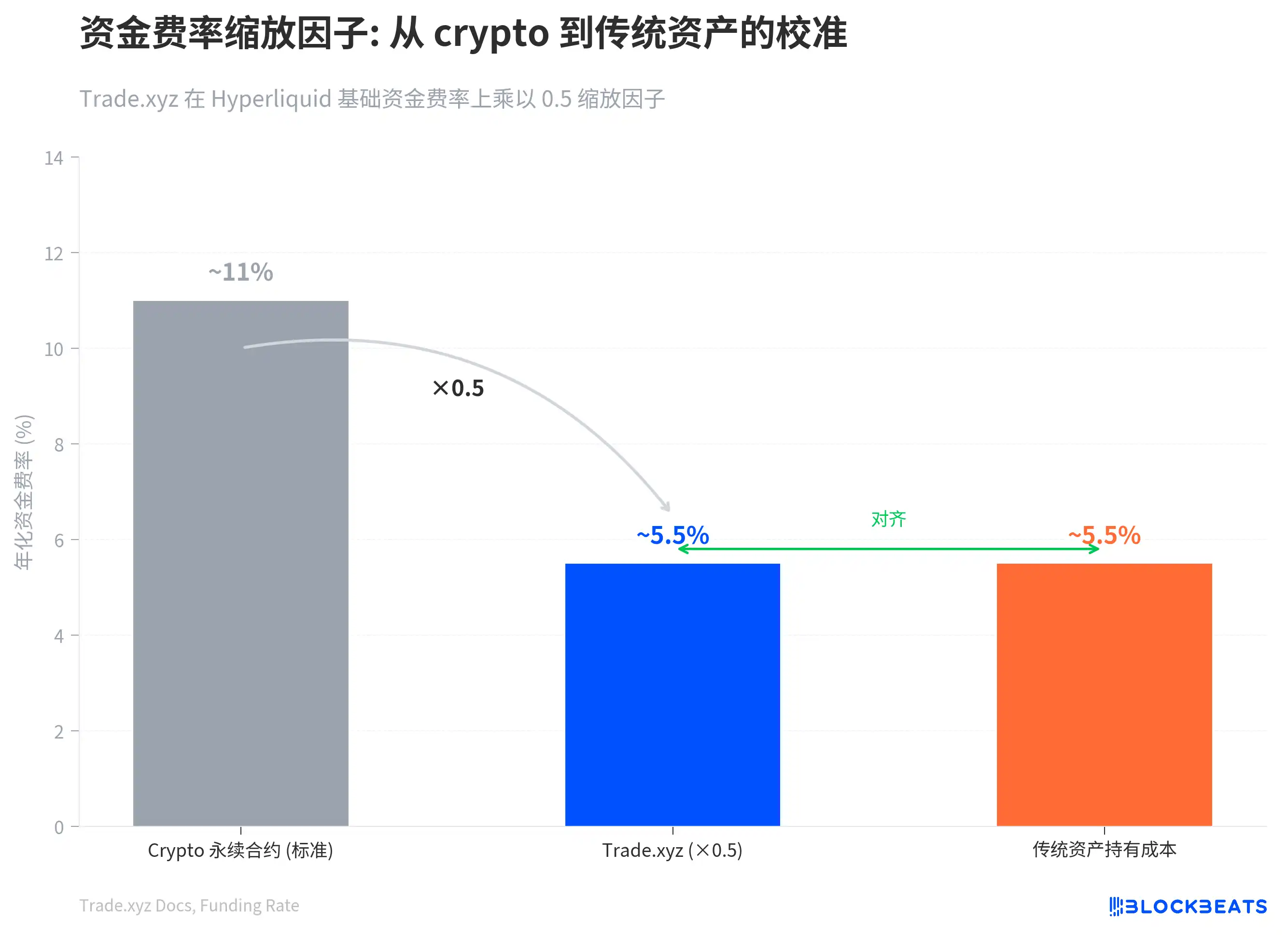

Another key component of the pricing system is the funding rate. The funding rate is the rubber band that tethers the perpetual contract price to the oracle price: if the marked price is above the oracle, longs pay shorts; if it’s below the oracle, shorts pay longs. Trade.xyz’s funding rate formula is similar to those of most crypto exchanges, but it has a scaling factor of 0.5 multiplied at the front.

This 0.5 is a calibration for traditional assets. The basic annualized funding rate for crypto perpetual contracts is about 11%, reflecting the pure holding cost of leverage, which is reasonable for assets like Bitcoin that do not pay dividends. However, for stocks and commodities, the real holding costs are closer to SOFR plus 1 to 2 percentage points, about 5% to 6%. Multiplying by 0.5 reduces the basic annualized rate from 11% to about 5.5%, aligning it with traditional assets. This is especially critical over weekends: the scaling factor directly halves the funding rate over the weekend, and combined with the 1-hour time constant oracle, allows traders with correct direction to retain most of their profits.

Different assets, different processing pipelines

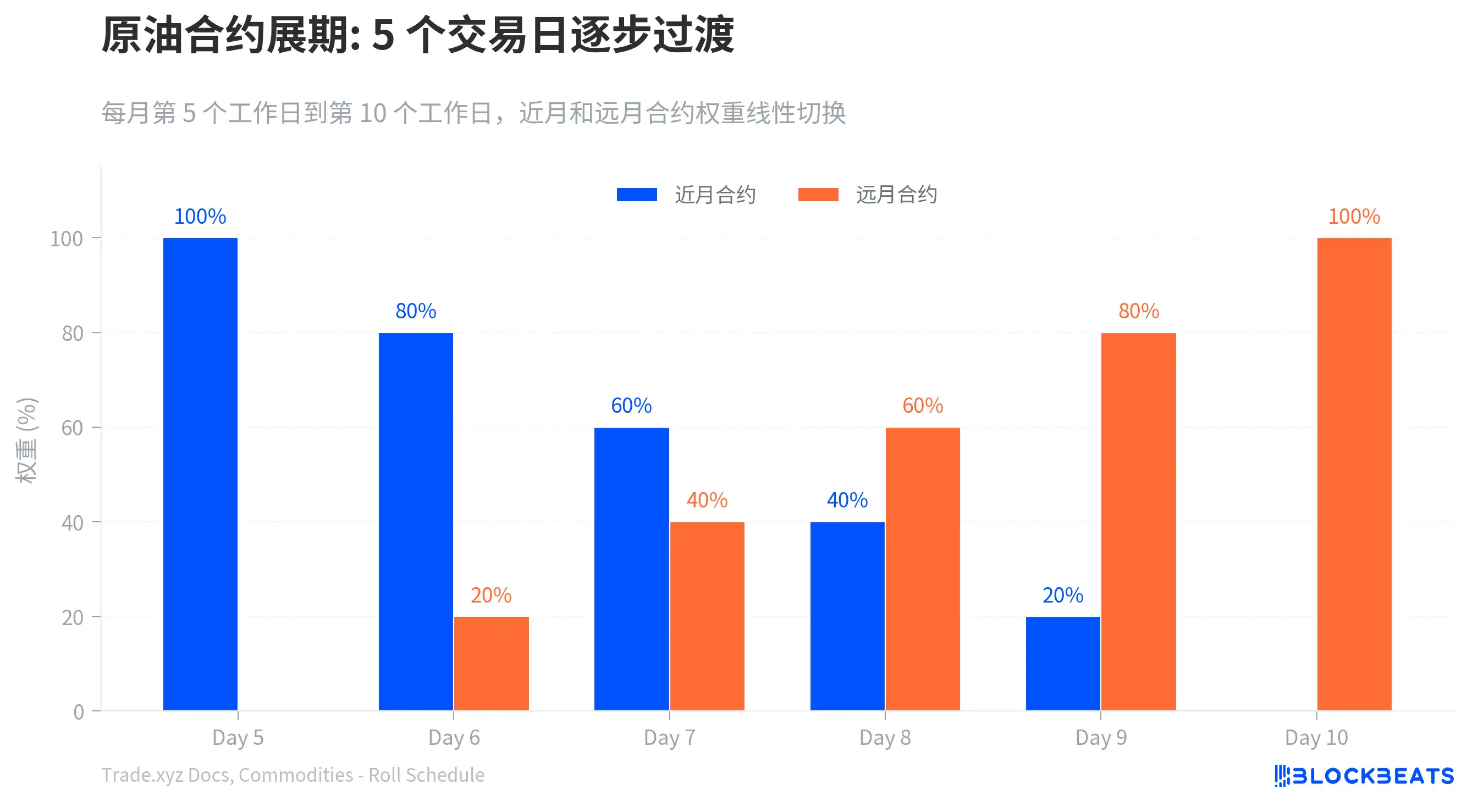

Precious metals have an active global spot market. The external prices of gold, silver, platinum, and palladium are directly derived from spot quotes, with no futures roll-over issues. However, crude oil and industrial metals do not have unified spot quotes, so Trade.xyz can only use CME futures contracts as the pricing basis. Futures contracts have expiration dates, and the system needs to switch from the current month contract to the next month contract every month. The problem is that the prices of the two contracts are often different. Storage costs and supply-demand expectations can cause the far-month contract price to be higher than the near-month contract. If the price jumps during the switch, the holder’s profit and loss can show unrealistic fluctuations, possibly triggering unwarranted liquidations.

Trade.xyz’s approach is to transition gradually over 5 trading days: from the 5th to the 10th business day of each month, the oracle price is the weighted average of the near-month and far-month contracts, with the weights changing linearly each day.

The pricing of index contracts is more complex. XYZ100 tracks the NASDAQ 100, but CME's NASDAQ futures trade almost all day (5 days × 23 hours), providing a pricing reference longer than that of the spot. Initially, Trade.xyz used futures prices to backtrack spot prices, fixing a 4% discount rate to strip away holding costs. However, this fixed value deviates when the Federal Reserve raises rates. The v2 solution launched in February 2026 switched to dynamic calculation: at the opening of U.S. stocks, the actual spot index value is directly used, while the implied discount rate is derived from the spread between futures and spot; after-hours trading uses this discount rate to backtrack the spot price.

There is also a special case: Korean stocks. Trade.xyz has listed Samsung Electronics, SK Hynix, and Hyundai Motor, which are quoted in South Korean won on Korean exchanges. The oracle needs to add a layer of USD/KRW exchange rate conversion on top of the original quotes. The profit and loss of holders reflect both stock price fluctuations and exchange rate fluctuations.

Who is responsible for the consequences of parameter choices?

All these pricing mechanisms are based on a premise: there are enough market makers willing to continuously provide liquidity. Hyperliquid's HLP liquidity vault provides liquidity for native BTC and ETH perpetual contracts but does not cover third-party contracts deployed on HIP-3. The liquidity on Trade.xyz completely relies on the voluntary participation of external market makers. In extreme market conditions, if there are no counterparties to take the positions being liquidated, the system will not be underwritten by the HLP vault as on Hyperliquid's main site but will directly trigger ADL (Automatic Deleveraging), forcibly liquidating the most profitable counterpart positions based on profit ranking.

The brilliance of this pricing system lies in the fact that it creates a self-sustaining pricing environment without external quotes using a set of mutually balancing parameters—the tracking speed of the oracle, the boundaries of price discovery, and the scaling factor of the funding rate. On March 18, S&P chose to authorize Trade.xyz, possibly viewing this infrastructure that has proven to operate during real geopolitical crises.

However, this system also comes with its costs. The oracle extracting information from the order book means that during thin liquidity periods (such as late-night Korean stock contracts), a small number of orders can significantly move the oracle. The Price Discovery Boundary v2 has expanded the liquidable range over weekends, requiring leveraged traders to reassess their safety margins. ADL means that even if your judgment is correct, you could still be forcibly liquidated in extreme conditions.

Trade.xyz has chosen a completely different path from traditional exchanges: it has shifted the pricing power from a centralized matching engine to a set of on-chain parameters. Traditional exchanges close because clearing, risk control, and market making require a manual intervention window. Trade.xyz cannot be closed because on-chain contracts do not have a concept of "closing time." It must provide a price at all times. The crude oil event on March 9 proved that this system can operate under pressure. But it also exposed a deeper issue: when letting on-chain protocols assume the pricing function of traditional financial infrastructure, who is responsible for the consequences of parameter choices?

The adjustment of the time constant from 8 hours to 1 hour is a parameter decision made by the Trade.xyz team. Upgrading the price discovery boundary from v1 to v2 is also one of these decisions. These decisions affect every holder's liquidation line and funding rate. In traditional exchanges, such rule changes require regulatory approval and a public notice period. In the on-chain world, a parameter update can be accomplished in an instant.

In a system that has no HLP backing, no regulatory arbitration, and relies entirely on parameter design to maintain order, understanding how these parameters affect your position is tantamount to understanding the actual risk you bear.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。