Abstract

• Gate is the only exchange that achieves full category coverage (stocks, metals, indices, forex, commodities) in perpetual contracts (Orderbook model). For professional users who prefer order book matching, transparent depth, and API trading, Gate provides the most comprehensive trading experience that is closest to the native cryptocurrency contract paradigm.

• Most competitors focus on independent TradFi CFD modules, attracting cross-circle users through a wide variety of underlying assets and low thresholds, while Gate's differentiated advantage leans towards integrating traditional assets into a unified order book perpetual framework, building it as reusable derivative infrastructure, thus creating a significant mechanical gap with competitors at the order book perpetual level.

• As the industry shifts from product stacking to competition in trading infrastructure, the order book model emphasizes open matching, transparent liquidity structure, and reusable trading paradigms, which aligns more closely with the long-term direction of standardizing trading scenarios for RWA. Gate, with its unified order book architecture covering multiple asset categories, provides a stronger scalability space for the subsequent expansion of more complex real asset trading forms.

1. Definition of Market Product Forms

In the TradFi布局 of mainstream cryptocurrency exchanges, the key differences between platforms are not just the number of traditional assets launched, but in what trading forms these assets are introduced to the market. Different product forms determine how transactions are matched, how key price parameters (such as index price/mark price) and risk control mechanisms are anchored, as well as whether trading experiences and strategies can be reused within the framework of cryptocurrency derivatives.

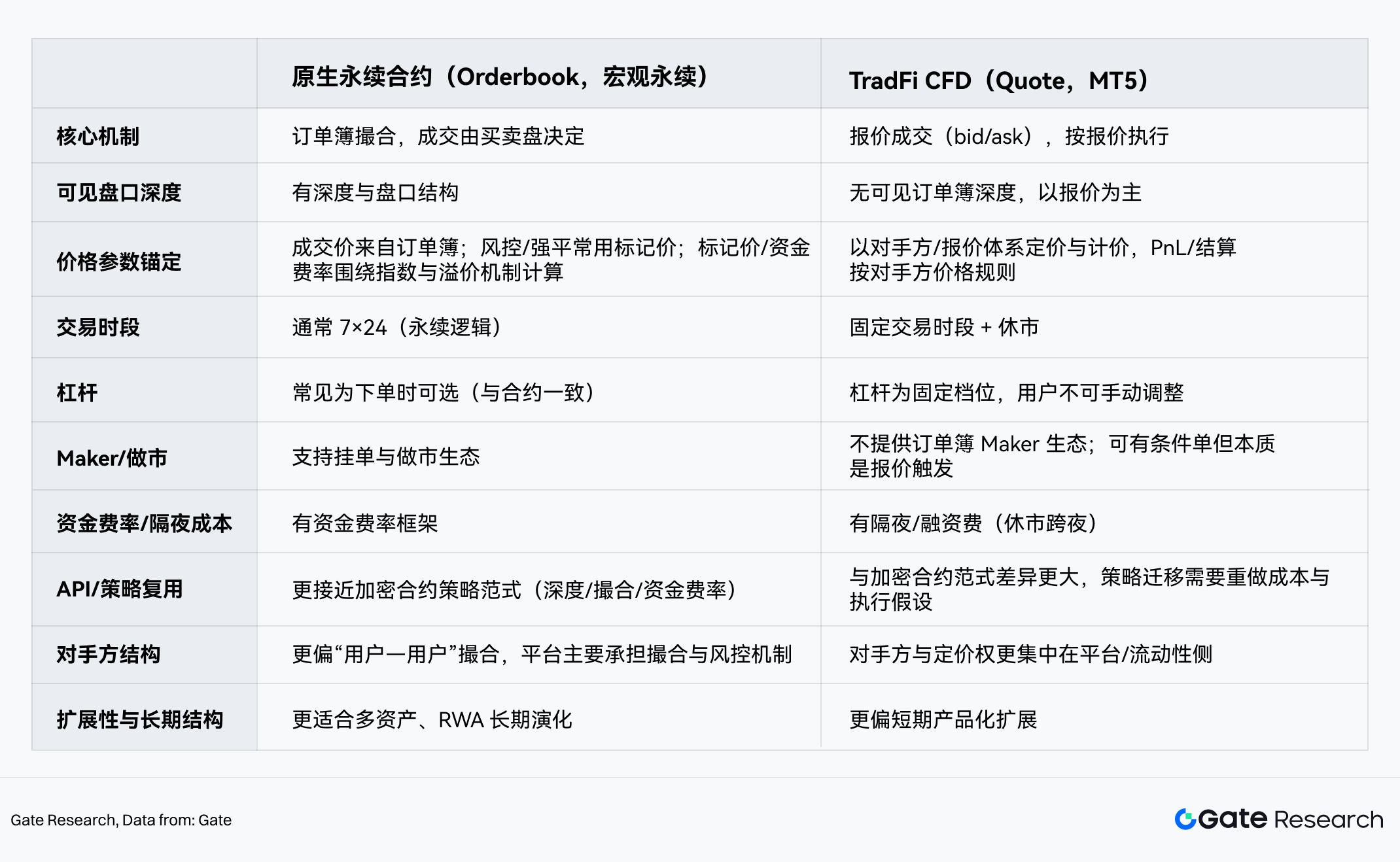

Based on differences in trading mechanisms, current CEX TradFi derivatives can be categorized into two main forms:

• One type is the native perpetual contract (Orderbook) model, which integrates stocks, indices, forex, or commodities into the order book matching system. Transactions are completed through matching buy and sell orders, using frameworks such as funding rates from cryptocurrency perpetual contracts; at the same time, mark prices and funding rates are usually calculated based on external indices or reference prices and premium indices, making TradFi assets closer to the experience of cryptocurrency native contracts in terms of visible depth, order posting/market making, and API consistency, naturally fitting for quantitative institutions and API users.

• The other type is the TradFi CFD (Quote) model, which centers around bilateral quotes from the platform or liquidity providers, where transactions are more reflected as matching according to bid/ask quotes, lacking visible order book depth and Maker ecosystems; its advantage lies in a rich variety of asset types and low barrier to entry, but critical elements such as price formation, spread/commission, overnight fees, and forced liquidation paths rely more on the platform's mechanisms, with relatively limited strategy reuse space, leaning more towards mid-frequency and directional trading.

I. Perpetual Contracts vs CFDs

The differences in product forms and trading mechanisms have led to significant differentiation in the product paths and long-term strategies of various platforms.

2. Core Data Matrix Analysis

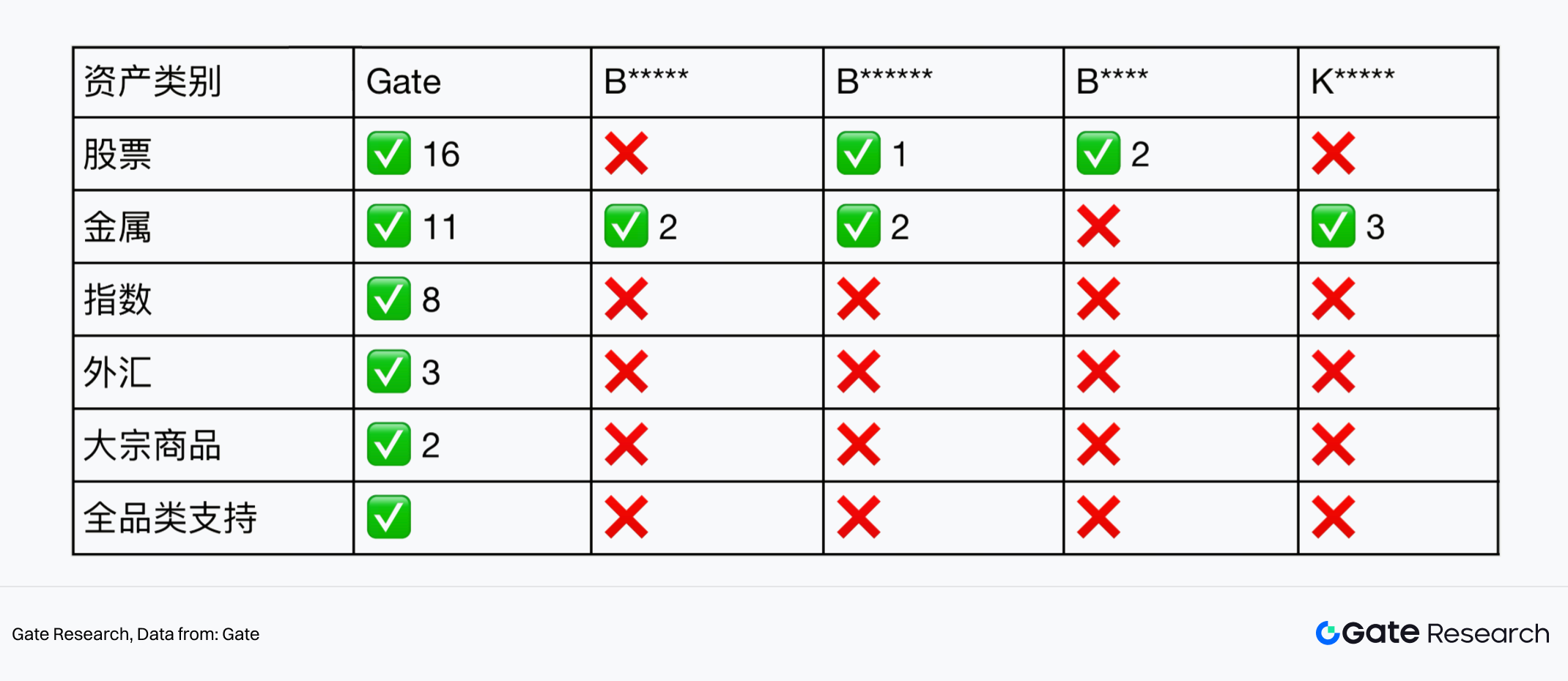

2.1 Perpetual Contract (Orderbook) Coverage Matrix — Gate's Absolute Moat

From the coverage matrix perspective, Gate has already established a very clear leading position in traditional asset Orderbook. Currently, Gate is the only platform that achieves full category coverage of Orderbook, allowing stocks, metals, indices, forex, and commodities to be traded under the same Orderbook system; at the same time, Gate is the only exchange that truly integrates indices and commodities into the Orderbook. Directly placing TradFi assets into the Orderbook, rather than delegating them to CFD quoting systems, essentially chooses a way of trading that is closer to real transactions. In other words, this means that prices are matched by the market, there are real order books, depth, and users can post orders and market make, allowing TradFi assets to be used as directly by quantitative strategies and APIs as BTC and ETH.

II. Coverage of Mainstream Cryptocurrency Exchanges' TradFi Orderbook

Statistical Criteria Note: Only includes perpetual contract products that support the Orderbook mechanism, excluding quoting (CFD / Quote) modules.

In terms of stocks, Gate has launched 16 tradable assets on the Orderbook, ranking among the top within similar platforms. Currently, it covers core tech stocks represented by AAPL, NVDA, and TSLA, as well as high Beta stocks such as COIN and MSTR that are highly correlated with crypto, extending to indices and leveraged ETFs like QQQ and TQQQ. This combination allows professional traders to participate in core stock assets, crypto-mapped assets, and macro index opportunities within the same Orderbook perpetual system, creating a more comprehensive cross-market trading and hedging structure.

In metals, Gate's perpetual contracts cover not only core safe-haven assets like gold and silver but also extend to platinum, palladium, and industrial metals like copper, aluminum, and nickel, forming a complete trading structure for metals and industrial metals. With the context of a strong overall metal market in 2026 and significant volatility, this layered coverage allows metal assets to support hedging, macro, and industrial cycle trading logic within the Orderbook perpetual system, significantly increasing tradability and strategy space.

Moreover, Gate has also established a substantial exclusive first-mover advantage in index perpetual contracts, having launched 8 indices including NAS100, UK100, SPX500, US30, HK50, and JPN225, all operating within the Orderbook system, forming an unreplicable product barrier.

Additionally, the forex and commodity perpetual contracts have also been practically implemented. Although the quantity is still expanding, the technology, risk control, and liquidity models have been validated. Among them, Gate has formed a completely independent differentiated interval for TradFi perpetual contracts in commodities, having launched the perpetual contracts for XTI (WTI crude oil) and XBR (Brent crude oil) for live trading. In the backdrop of escalating geopolitical tensions and significant fluctuations in energy prices in 2026, integrating crude oil as a core commodity into the Orderbook perpetual system enables efficient completion of related risk hedging, directional trading, and cross-asset allocation for the first time within the cryptocurrency-native derivatives framework, further amplifying Gate's first-mover advantage in the TradFi perpetual track.

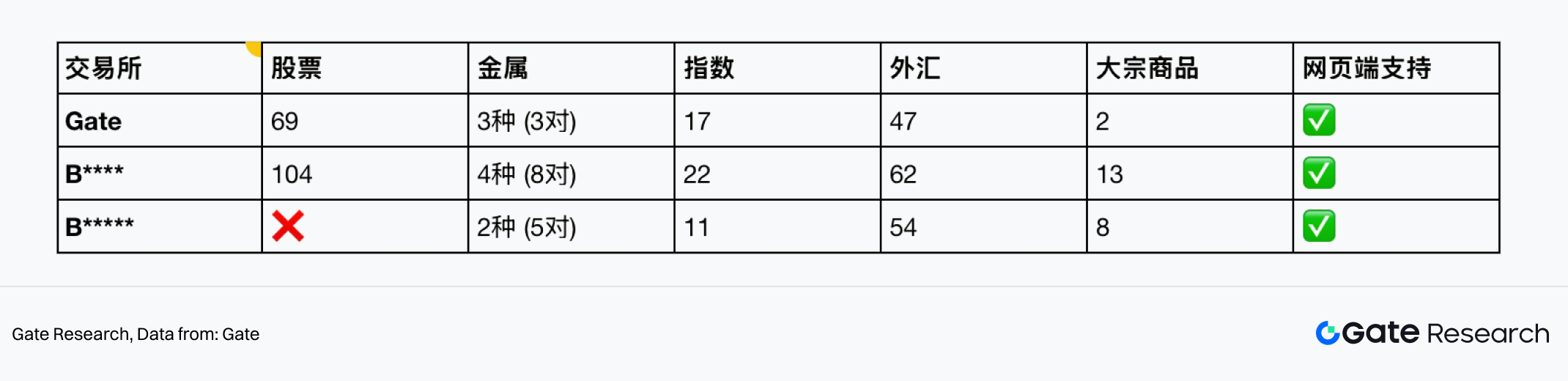

2.2 TradFi CFD Module Comparison — The Main Battlefield for Competitors

In the TradFi CFD module, the market shows a competitive landscape that is completely different from the Orderbook perpetual contracts. This track emphasizes "asset diversity", with the core goal being to lower barriers and quickly accommodate the trading needs of cross-circle users. The product form is primarily quoting-based, often lacking visible order depth, and the trading experience is more akin to traditional forex or CFD platforms, suitable for directional speculation, but not emphasizing deep participation or high-frequency trading.

III. Mainstream Cryptocurrency Exchange TradFi CFD Module Comparison

Statistical Criteria Note: Only counts independent TradFi / CFD quoting modules that exist within exchanges, excluding perpetual contract products.

Within this framework, other mainstream CEXs cover a broader user base through a large number of stock, forex, and index offerings; in contrast, while Gate also provides a certain scale of stock CFD products, its resource investment is relatively restrained. In terms of quantity, Gate's CFD module covers 69 stocks, 17 indices, 47 forex pairs, supported by a small number of metals and commodities, overall possessing basic completeness but serving more as a supplementary role rather than a core focus of the platform.

Overall, for Gate, the advantage is not in how many TradFi assets are listed, but in whether these assets can truly be traded in a manner similar to cryptocurrency assets, such as having real order books, continuous price discovery, the ability to post orders, market make, and be directly used by quantitative strategies and APIs. It is this approach of treating TradFi assets as cryptocurrency-native derivatives that sets Gate apart from other platforms in the realm of perpetual contracts.

3. Objective Facts and User Experience Differences (Qualitative Analysis)

Aside from numerical statistics, product operation, user experience, and fee rates also influence user choices.

3.1 Asset Visibility and Compliance Thresholds

On asset visibility and compliance strategies, different platforms have adopted distinctly divergent paths. Gate adopts a relatively conservative strategy, where TradFi stock trading pairs are only available to logged-in users, preventing guests from directly browsing the order book, which to some extent limits search engine indexing and natural traffic acquisition; simultaneously, Gate conducts clear isolation in naming related assets, emphasizing their synthetic or tokenized attributes through the X prefix or ONDO suffix (e.g., TESLAX, APPLON). This approach helps reduce compliance risks but may also reinforce users' perception of "not being real stocks" in their minds.

In contrast, M*** and B***** employ more aggressive customer acquisition strategies, making related TradFi stock products open to guests across the network, displaying original codes for stocks like AAPL and TSLA, facilitating natural traffic acquisition, with an almost zero user understanding cost, significantly improving first contact and conversion efficiency; similarly, B****** also makes market information externally visible. Such strategies are more advantageous in user growth and cognitive transition but may also come with higher risks related to securities attributes and regulatory compliance.

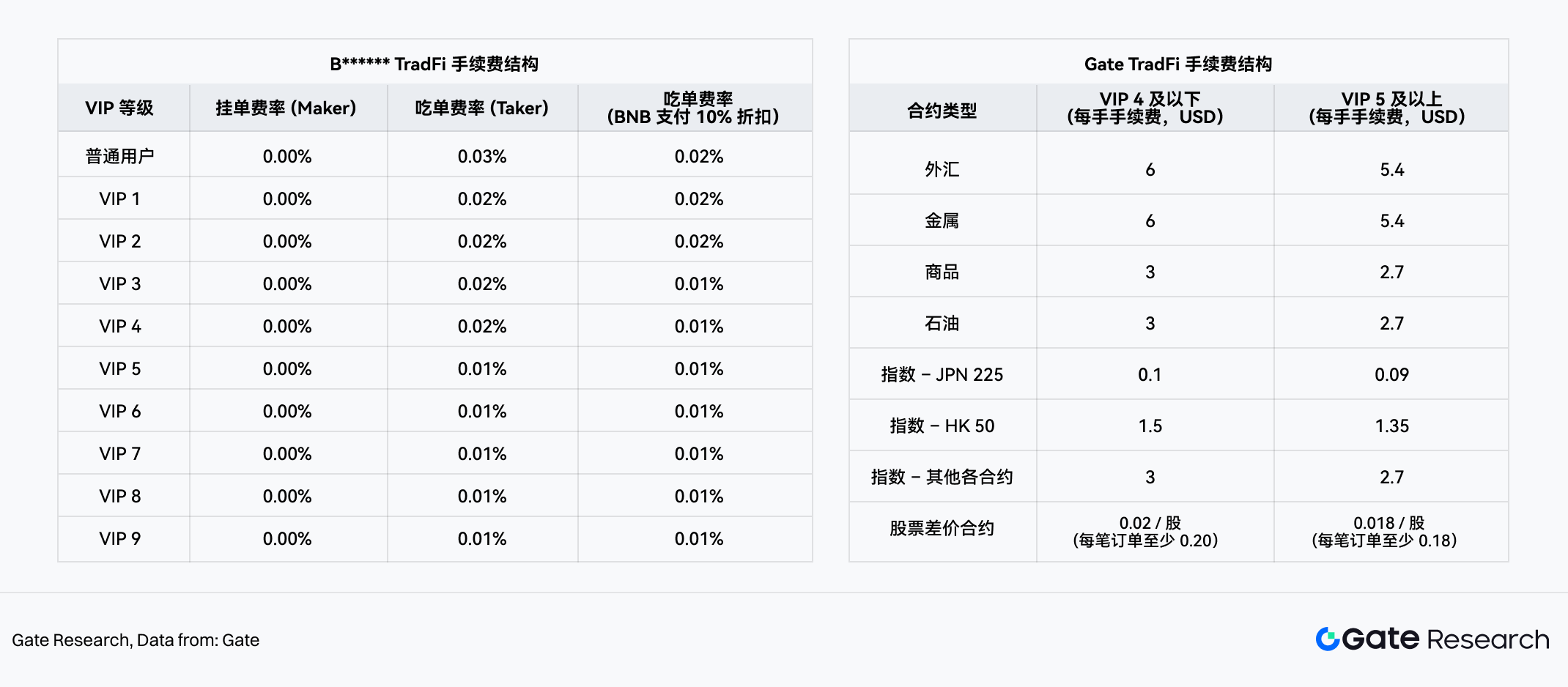

3.2 Fee Rates and Product Operations

In TradFi-related products, Gate and B****** adopt completely different pricing models; Gate maintains a common fixed charging model per contract seen in traditional CFD markets, while B****** TradFi Perps employs a percentage fee model based on nominal transaction amounts for perpetual contracts.

IV. B****** TradFi Fee Structure/Gate /TradFi Fee Structure

Taking gold (XAUUSD) as an example, under the contract specification of 1 contract = 100oz, Gate's metal TradFi contracts adopt a fixed fee per contract: regular users (VIP4 and below) face a per-contract fee of about $6, while higher-level users (VIP5 and above) can reduce it to $5.4. This fee is unrelated to the gold price or nominal transaction amount, and the trading cost can be clearly defined before placing an order, providing high predictability.

In contrast, B******* TradFi Perps continue to employ the percentage fee model of the U-based perpetual contracts. In the original pricing model without considering any temporary discounts, regular users incur a fee rate of 0.05% (0.045% if paid with BNB), while the highest-level users (VIP9) face a fee rate of 0.017% (0.0153% with BNB). In this model, the fee fluctuates linearly with the gold price.

Conducting a comparative analysis under the premise of 1 contract = 100oz, it can be observed that the gold price range corresponding to the equalization of Gate and B******* fees is approximately as follows, where typically, B****** has lower fees:

• Regular users: $120–133/oz

• Highest-level users: $318–353/oz

Considering that the actual gold price has long remained well above this threshold level, in the current market environment, Gate's fees in small to medium position trades are notably more competitive. This is particularly evident in the following trading scenarios:

• Trades primarily involving 1 contract or a small number of contracts, avoiding fee escalation with rising prices

• High-frequency or strategy-based trades that focus more on stability and predictability of per-transaction costs

• TradFi / CFD user migration scenarios where the fixed per-contract charge pricing model is more familiar

In terms of marketing packaging and content supply, Gate's investment in TradFi is more concentrated and sustained. Based on the current app and website statistics, Gate has launched over 10 ongoing or recent operational activities centered around TradFi, including trading rewards, physical gold incentives, exclusive beginner tasks, trial funds, and point incentives, maintaining a high-frequency update pace. Meanwhile, Gate has provided over 10 announcements, tutorials, and informational content centered around TradFi, covering product launch explanations, contract rules, leverage and risk control adjustments, research interpretations, and beginner guides, forming a relatively comprehensive system of activities and educational content.

In product presentation, Gate highlights the TradFi module prominently on the app and website homepage, continuously exposing it as a core business module, reducing user discovery and understanding costs. In contrast, B******'s TradFi-related entry levels are relatively deeper, leaning more towards functional contract supplements, with fewer relevant marketing activities and systematic tutorials overall. Looking at it holistically, Gate provides more frequent operational activities and intense explanatory content, establishing a clearer advantage in user outreach, first conversions, and TradFi user education.

V. Gate TradFi Access

3.3 Strategic Divergence in Trading Models

3.3.1 Model Selection of Various Platforms

In the TradFi space, the trading model choices of various platforms for traditional assets directly reflect their strategic positioning and product architecture differences:

•B****'s Pure CFD Strategy: B**** does not support traditional assets within its perpetual contract products. All trading of traditional assets is conducted within an independent TradFi CFD module. This effectively separates crypto users and traditional trading users into two different systems, with trading logic and matching mechanisms not interfering with each other.

•B*****'s Hybrid Model Strategy: B***** supports stock and metal assets within its perpetual contract products, but other asset classes (indices, forex, commodities, etc.) still need to be traded through its TradFi CFD module. Users must log in or authenticate again when transitioning from the main site to the TradFi interface, indicating costs associated with interface and session state switches.

•Gate's Multi-Asset Orderbook Perpetual Contract Strategy: Gate uses the Orderbook order matching mechanism for perpetual contracts across five categories of traditional assets: stocks, metals, indices, forex, and commodities, rather than relying on independent CFD quoting products to carry out transactions. This means that relevant TradFi assets enter the matching market in the form of standardized derivatives on Gate, where prices are determined by supply and demand from bid and ask orders in the order book, providing users with market liquidity rather than platform counterparty quotes. Although different asset classes are located in their respective trading segments, their underlying matching framework, order book logic, and trading rules remain consistent, allowing for a unified market structure and strategy reusability in multi-asset trading.

3.3.2 Strategic Implications Behind Model Selection

These three designs represent different strategic thoughts. B**** and B***** have taken a relatively "pragmatic" path by isolating the trading systems for crypto and TradFi assets, optimizing for different user groups and market demands. This architecture can quickly launch products within a short duration to cover market demands.

On the other hand, Gate opts for a unified Orderbook infrastructure to cover all asset classes. This not only standardizes trading logic but also positions the platform as a neutral matcher. In the Orderbook model, the platform does not directly act as a counterparty, and its income is sourced from trading fees, which are not directly linked to users' profits and losses; while in the CFD model, the platform typically acts as a counterparty, where its income may exhibit some relationship with user trading results. Gate's adherence to the Orderbook model for TradFi conveys a concept: that trading TradFi assets should maintain a matching thought consistent with cryptocurrency assets.

For users seeking trading transparency, a clear liquidity structure, and controllable counterparty risk, this consistency in trading experience is clearly appealing.

3.3.3 Long-term Strategic Intent

From the perspective of trading structure and risk-bearing mechanisms, different trading modes exhibit essential differences in long-term scalability. Under the Orderbook architecture, the platform merely assumes the matching function, where users are counterparts to each other, and the platform itself does not need to intervene in price formation or assume directional risks. This design enables the platform to continuously focus on liquidity building, matching efficiency, and trading depth optimization, without being constrained by the structural burdens introduced by the expansion of asset classes, making it more suitable for supporting multi-asset, long-term evolving trading systems.

From the long-term perspective of the RWA space, genuinely mature RWA trading forms should possess clear price discovery mechanisms, transparent liquidity structures, and reusable trading infrastructures, rather than relying on singular product forms or closed pricing models. The public matching and market-oriented pricing emphasized by the Orderbook model are naturally closer to this goal. Gate currently employs a unified Orderbook structure for TradFi perpetual contracts, essentially laying the groundwork for future more complex and standardized trading forms of real assets.

4. Conclusion: Gate is Transitioning from Multi-Asset Expansion to Trading Infrastructure Upgrade

Through a comprehensive analysis of product forms, data matrices, and platform paths, a clear conclusion can be drawn: Gate's true differentiation in the TradFi space does not lie in "whether or not to provide stocks, indices, or forex," but in "what trading structure carries these assets." While most platforms in the industry are still in the product expansion stage for TradFi, Gate has already entered the stage of competition in trading mechanisms.

The current mainstream practice in the market is to incorporate traditional assets into independent CFD quoting systems, using the quantity of asset coverage and low threshold experience as core competitive points; while Gate chooses a path that leans more towards fundamental structural evolution — directly integrating TradFi assets into a unified Orderbook perpetual matching system, keeping price formation, order book structure, matching logic, and API rules consistent with cryptocurrency-native contracts. This means that what Gate is doing is not merely an extension of traditional TradFi products. Its true direction is building a multi-asset unified matching derivatives trading infrastructure.

From the perspective of trading structure, the core value of the Orderbook model lies in public matching and market-oriented price discovery. Once TradFi assets enter this system, prices are formed by real buy and sell orders, allowing users to post orders, market make, and engage in deeper structures, making the trading experience much closer to an open market rather than a quoting-driven closed trading model. For quantitative institutions and API traders, the key value brought by this mechanism is the reusability of strategy paradigms: cross-asset hedging, macro-linked strategies, event-driven trading, and even high-frequency market making can all be completed under the unified matching logic without needing to rebuild execution and risk control assumptions for different asset classes. This structural consistency allows Gate's TradFi trading to naturally integrate into the cryptocurrency-native derivatives ecosystem.

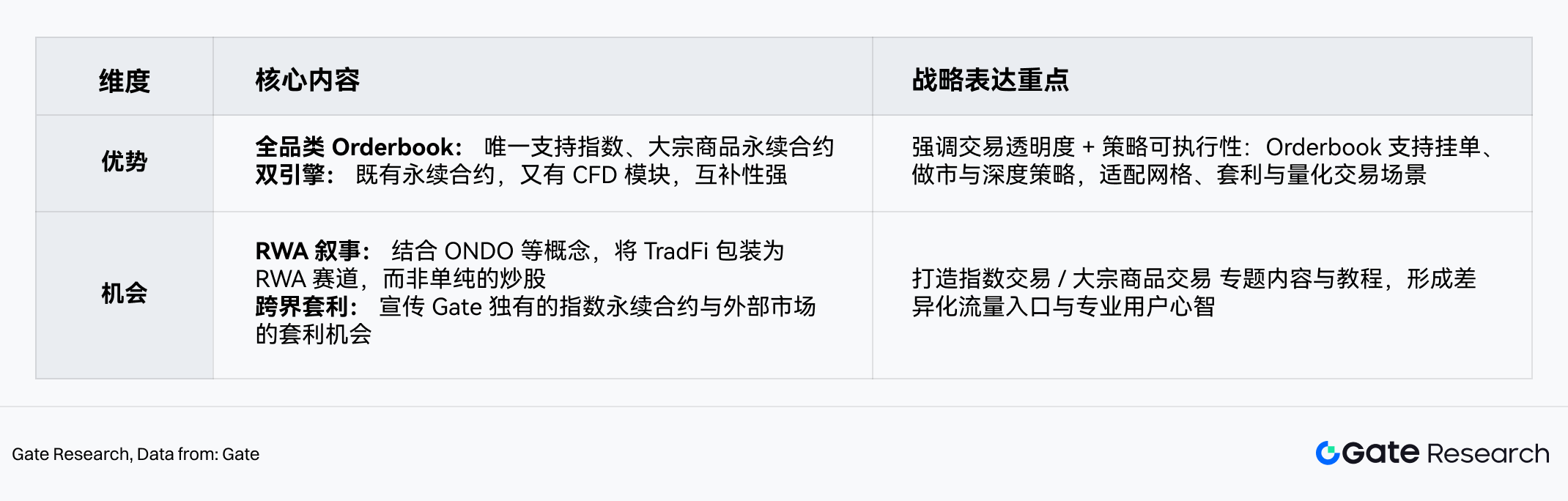

Based on the above trading structure and platform positioning analysis, Gate's structural advantages and strategic opportunities under the TradFi Orderbook route can be distilled into the following strategic positioning matrix:

VI. Gate TradFi Orderbook Strategic Positioning Matrix

On this structural foundation, Gate's platform role and long-term expansion path also present a clearer direction. From the perspective of platform role and long-term scalability, Gate's Orderbook architecture reinforces its neutral matcher positioning. The platform focuses on matching and liquidity organization as core functions, not needing to assume directional price risk, allowing it to continuously invest resources in liquidity depth, matching efficiency, and market structure optimization. This mechanism does not introduce structural risk burdens when expanding asset classes, thus being more suitable to support the future long-term evolution of multi-assets. As the industry gradually shifts from "competition of product numbers" to "competition of trading mechanisms", this structural advantage will serve as a continuous source of technological and liquidity moats.

From a longer-term perspective, this path is highly aligned with the evolution direction of RWA trading forms. A mature RWA market requires transparent price discovery mechanisms, public liquidity structures, and reusable trading interfaces, wherein the Orderbook model is the core foundation of such standardized trading forms. Gate's current utilization of a unified Orderbook architecture for TradFi perpetual contracts essentially establishes an expandable framework in advance for the standardized trading form of real asset chaining in the future. This gives Gate a natural structural capacity and first-mover advantage as the RWA trading infrastructure gradually matures in the next stage.

Based on the structural positioning mentioned above, Gate is advised to upgrade its external strategic expression from "TradFi asset expansion" to "multi-asset trading infrastructure upgrade." The core narrative should revolve around the following directions:

• Emphasize the unified Orderbook perpetual structure as a mechanism-level positioning rather than merely asset quantity: Gate's differentiation does not lie in "how many traditional assets are online," but in the fact that these assets operate under a standardized derivative market with the same matching logic.

• Highlight real order book depth and market-oriented price discovery: By visualizing order book structures, depth distributions, and order posting ecosystems, letting users intuitively understand that these assets operate in a market environment where participation in market-making is possible, rather than in a closed trading model driven by quoting.

• Strengthen professional trading scenario narratives: Gate's TradFi Orderbook is more suitable for binding cross-asset hedging, macro-linking, event-driven, and quantitative strategies based on depth structures, rather than the traditional sense of a "cross-circle wealth management entry." This narrative will help the platform establish a clearer mechanism cognition within professional trader groups.

Finally, on the long-term narrative side of the industry, gradually establish a logical extension from "traditional asset Orderbook perpetual" to "future RWA standardized trading interfaces," positioning Gate in the market mind not only as a TradFi innovator but also as an early infrastructure builder for standardized trading forms of real assets on-chain.

Overall, Gate represents not just a trading platform that provides more traditional assets in the TradFi space, but rather one that has taken the lead in creating a multi-asset order book trading infrastructure. As the industry shifts from the stage of asset expansion to upgrading trading mechanisms, the long-term value of this path will continue to amplify. The core strategic significance of Gate is reflected in its laying the groundwork for a multi-asset, standardized, and reusable future trading system through its unified Orderbook architecture.

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform, providing readers with in-depth content, including technical analysis, hot insights, market reviews, industry research, trend forecasts, and macroeconomic policy analysis.

Disclaimer

Investment in the cryptocurrency market involves high risks, and users are advised to conduct independent research and fully understand the nature of assets and products purchased before making any investment decisions. Gate assumes no responsibility for any losses or damages resulting from such investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。