Written by: Prathik Desai

Translated by: Block unicorn

Introduction

At the end of the 1960s, Wall Street faced a problem that was not particularly conspicuous. As securities trading became increasingly popular, trading activities surged, yet the infrastructure supporting these trades remained outdated. Brokers were still settling trades through the physical exchange of stock certificates. Messengers were running around Manhattan delivering envelopes. Back offices were cluttered with various forms. The surge in trading volume once became so severe that the U.S. market had to stop trading every Wednesday for six months to allow firms time to handle the backlog of paperwork.

This eventually evolved into the infamous "paperwork crisis."

Better "runners" or more paper documents could not resolve the issue. Thus, in 1973, they replaced all liquid assets with the Depository Trust Company (DTC). This company dematerialized securities and changed ownership transfers to book updates instead of the physical handover of stock certificates. The modern U.S. securities market we see today is the result of this decision, evolved through multiple iterations.

Today, the DTC holds over 1.4 million securities valued at $87.1 trillion, including securities issued both in the U.S. and over 130 other countries and regions.

We also see similar narratives throughout financial history. When an asset class becomes substantial enough and popular enough, the support for its development is not solely based on bookkeeping strategies; the fundamental drive behind it is always trust. After the launch of the DTC, ordinary investors no longer had to worry about ownership issues because trust in the central authority’s ability to maintain records replaced the need for paper certificates.

A similar problem has arisen in the cryptocurrency space. Over the past two years, driven by Exchange-Traded Funds (ETFs) and other forms of investment (such as digital asset government bonds), the appeal of cryptocurrencies as mainstream assets has steadily increased in the U.S.

This development has prompted back offices to act swiftly, just as the paperwork crisis of the 1960s birthed the DTC.

In cryptocurrency, "paper" refers to private keys, which act more like bearer instruments—whoever controls the private key controls the assets. This has presented familiar issues for financial institutions: operational control, asset segregation, auditability, bankruptcy concerns, governance, and the fact that losing a private key means permanent loss.

Now, a new trust mechanism is being built around these challenges: the trust bank charter. In today’s article, I will explain why numerous companies are racing to apply for cryptocurrency custody bank charters.

The Charters Craze

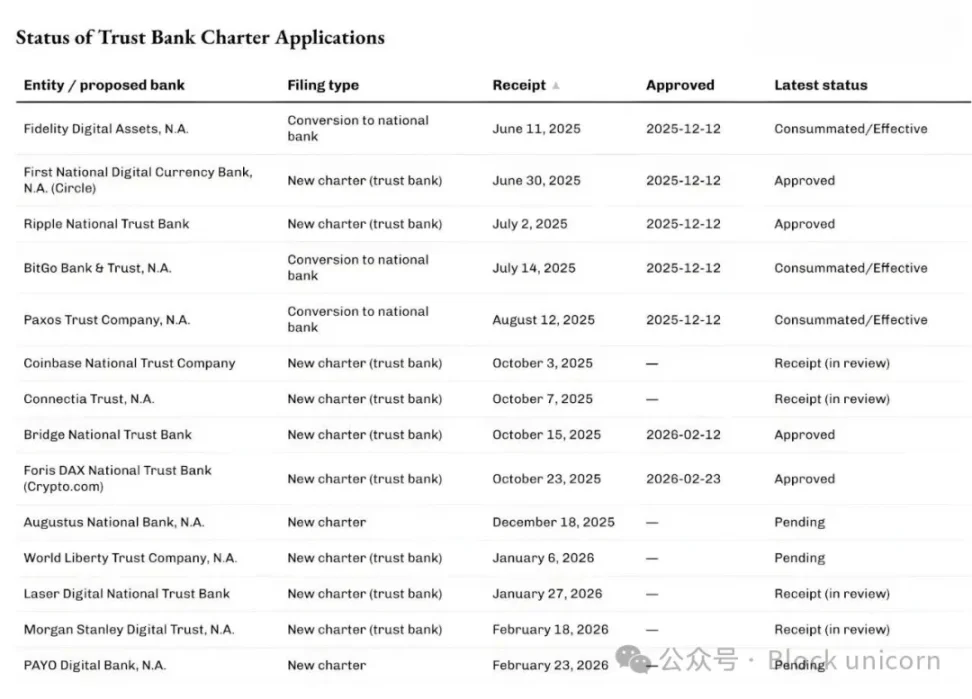

In recent months, the Office of the Comptroller of the Currency (OCC) has been approving and processing an increasing number of applications aimed at becoming national trust banks related to digital asset custody and stablecoin infrastructure.

On December 12, 2025, the OCC conditionally approved five such applications, including Circle's First National Digital Currency Bank, Ripple National Trust Bank, and conversion applications from BitGo, Fidelity Digital Assets, and Paxos. Subsequently, Stripe's cryptocurrency division Bridge and Crypto.com received preliminary approval from the OCC in February 2026.

The queue is not limited to native companies in the cryptocurrency space.

Last week, the world's largest wealth management company, Morgan Stanley, applied to establish a trust bank named Morgan Stanley Digital Trust National Association.

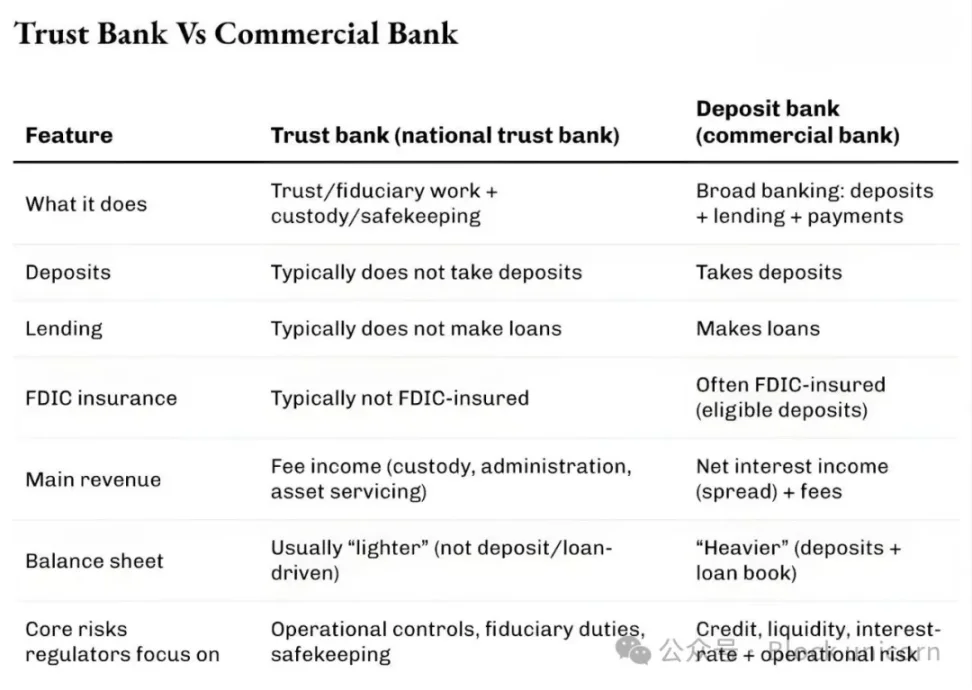

Do you know what the commonality among these applications is? They are not queuing up to become ordinary banks that handle deposits and loans. Unlike regular banks, these national trust banks cannot accept deposits or issue loans and do not have insurance from the Federal Deposit Insurance Corporation (FDIC). They apply to provide custodial, safekeeping, and trust management services. You can think of it as a bookkeeping service specifically for crypto assets.

I believe this is one of the most obvious signs that cryptocurrency is changing the way traditional financial institutions operate, while the rest of the world is busy focusing on the fluctuations in cryptocurrency prices.

Bank charters may sound dull, but like many other financial infrastructure innovations, they redirect our attention to the lessons learned by the financial world from the paperwork crisis. It also underscores that the core of mainstreaming cryptocurrencies lies in custody and control.

Why Now?

The surge in applications for charters is closely related to the OCC's recent clarification regarding national banks' authority in cryptocurrency-related custody operations. In May 2025, the OCC confirmed that national banks and federal savings associations could buy and sell their custodial assets at the direction of clients.

In December 2025, the agency also confirmed that banks could engage in "no-risk principal" cryptocurrency trading by acting as intermediaries without holding inventory.

Last week, on February 27, 2026, the OCC clarified that starting April 1, 2026, national trust banks can conduct non-trust activities that go beyond their narrow fiduciary responsibilities.

Why is this important? If you are a company engaged in custody, settlement, reserve management, and related services, this is crucial.

We have seen similar situations in the financial world.

In the early 2010s, as a wave of fintech companies developed applications on the foundation of partner banks, new types of banks emerged. While these applications made banking more accessible, they also posed some issues. Despite having user-friendly interfaces, the partner banks still controlled deposits, infrastructure, and regulatory powers. When problems arose, responsibility was dispersed across multiple entities, leading to chaos.

The response at that time was similar to what we see now in the cryptocurrency space: controlling risk and returns.

In 2016, the OCC began exploring the issuance of special-purpose national bank charters for fintech companies. Two years later, the OCC started accepting charter applications from non-depository fintech companies engaging in core banking operations.

Though courts rejected the possibility of issuing bank charters to non-depository institutions, fintech companies continued to reduce reliance on partner banks. A few fintech companies then transformed into full-service banks through traditional and more cumbersome routes, sometimes involving acquisitions.

Varo initially was a fintech company and received its full-service national bank charter in 2020. Jiko transformed into a bank through the acquisition of a small national bank. SoFi received conditional approval in 2022 to become a full-service national bank by acquiring an existing national bank.

The current surge in applications for national trust bank charters follows a similar pattern; this time, however, Washington is also establishing a new framework for digital assets.

The legislative backdrop behind all these developments more clearly illustrates why companies are not merely pursuing custody services in the digital asset realm when applying for national trust bank charters.

In July 2025, U.S. President Donald Trump signed the GENIUS Act, establishing a federal framework for payment stablecoins. Multiple companies seeking trust bank frameworks have indicated they plan to operate stablecoin and related reserve businesses within the regulatory framework set out by this act.

Both Bridge and Circle mentioned this in their respective announcements.

This answers the first layer of the question "Why now?" The clarity in regulatory policies has opened new value chains for existing businesses (including traditional firms and crypto-native firms), allowing them to expand their service offerings.

The second layer involves market structure.

Institutional investment in cryptocurrencies has shifted towards vehicles more akin to traditional financial products, such as ETFs, funds, and managed accounts. These vehicles require custodians that meet legal and operational requirements.

If you think that centralized cryptocurrency investment is no longer in demand, you are mistaken. The current development of cryptocurrency ETF infrastructure demonstrates that clearly.

In April 2025, the world's largest asset and crypto fund management company, BlackRock, added Anchorage Digital Bank as a bitcoin custodian beyond its existing partner Coinbase for its iShares Bitcoin Trust fund. BlackRock stated that this move is part of "ongoing risk management" aimed at meeting the growing demands of retail and institutional investors.

What value do financial giants like Morgan Stanley, valued at $9 trillion, see in these charters?

One of the recent indicators appeared less than two weeks ago during a fireside chat at the "Corporate Bitcoin" conference. At that time, Phong Le, CEO of Strategy (formerly MicroStrategy), stated, "If anyone can help the world 'take the orange pill,' it has to be Morgan Stanley." Amy Oldenburg, head of digital asset strategy at Morgan Stanley, responded, "That might be accurate."

What Changes Are Happening?

Once you connect these developments, the surge in trust charters resembles not so much a story of cryptocurrency but more of the evolution we observed during the development of the DTC.

As cryptocurrencies gradually evolve into a financial asset, both retail and institutional investors require a place to store private keys, which must be recognized by lawyers, auditors, and regulatory bodies. Establishing national trust bank charters is one approach to broadly addressing this issue.

Next is the question of the economic benefits of this business line. Custody services initially appear to charge low fees. Starting in the first quarter of 2025, Coinbase has stopped disclosing custody fee revenue as a separate item, instead consolidating it into "other subscription and service revenues." However, the complexity of custody operations goes far beyond what it may initially seem.

Whoever controls custody controls the collateral, which in turn determines the financing capabilities of these institutions. Financing decides leverage, and leverage determines trading volume. Ultimately, trading volume decides earnings.

In 2025, global securities lending income is projected to reach $15.3 billion, with loan balances exceeding $4 trillion. Custody giant State Street reported total revenues of $13.94 billion for 2025, with service revenues accounting for about 40% ($5.32 billion), including services such as custody, accounting and fund administration, record-keeping, and client reporting.

Thus, while custody services alone may not generate substantial revenues, the ancillary services surrounding custody can create repeatable revenue streams.

The DTC became indispensable because it enabled the market to scale without being buried under cumbersome paperwork. Today, the DTC has evolved into a comprehensive system, far beyond mere safekeeping; it also provides settlement services, processes corporate actions, and supports underwriting. This has formed a complete ecosystem built around updating ownership records.

Obtaining cryptocurrency custody licenses can bring similar benefits to these applicants. In addition to becoming a treasury, they can offer authorized ledger interfaces.

This license allows these institutions to provide credibility to their clients in terms of recording, segregating, transferring, and auditing digital asset ownership. They can achieve this without needing to be banks that take deposits, through a more streamlined balance sheet and focused approach.

However, trust charters also have their critics.

Supporters of traditional banking argue that these charters could serve as a "backdoor" into the banking system without requiring the absorption of deposits or the same extensive public obligations. Various banks are debating the delineation of boundaries.

Although the debate continues, regulatory changes are already underway. The OCC's conditional approvals may not represent final endorsements, but they convey an important message: despite adhering to the principle of self-custody, the scale of cryptocurrencies has become substantial enough to emphasize the importance of back-end operations.

I believe that if industry insiders label the surge in trust bank license applications as a phenomenon of the cryptocurrency industry, they are profoundly mistaken. It is more akin to a natural evolution where market participants are continually seeking to create value by addressing inefficiencies in the industry.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。