Original | Odaily Planet Daily (@OdailyChina)

Author | Ding Dong (@XiaMiPP)

Shanzhai coins are dead, which is almost a consensus that cryptocurrency users have been unwilling to admit over the past year, yet are forced to face. Even former blue chips, under the continuous decline of the market, have all fallen into prolonged sideways movement or downward trends, showing little improvement.

However, amidst this overall stagnation, MORPHO tokens have rebounded from a low of $0.96 in early February to the range of $1.8-1.9, doubling against the trend. From the daily chart, this rebound has basically formed a rounded bottom pattern, which could indicate a bottom reversal signal. Is this increase driven by a brief market sentiment boost, or a trend initiation resonating from fundamentals and structural variables?

When the Old Dynasty Begins to Consume Itself

Morpha is a lending protocol launched in 2021. Initially, it operated similarly to lending protocols like Aave and Compound, but in 2023, Morpha began to roll out Morpho Blue (the current main version), completely transforming into an independent, permissionless lending foundation layer, firmly positioned at the forefront of the Ethereum ecosystem lending track.

However, in the lending track, Aave remains the largest and strongest brand leader, which is an undeniable fact. Recently, Aave has fallen into serious governance disputes due to a $51 million "Aave Will Win" funding framework proposed by founder Stani.

This funding was originally planned to support new product development, and the proposal clearly stated that future related brand revenues would 100% return to the DAO treasury—which seemed like an ideal operation of the project party "handing over control, sharing profits with the community," but unexpectedly ignited long-standing contradictions within the DAO.

The reason is that DAO governance representative and ACI founder Marc Zeller publicly released an "audit" report on February 25, accusing Labs of low capital utilization, claiming that approximately $86 million had been taken from the DAO over the past few years without transparent disclosure. Meanwhile, DAO core developer BGD Labs announced it would exit by April 2026 due to governance friction. The founder's high voting power once dominated controversial proposals, further dragging the entire DAO into a public tug-of-war over power and capital allocation. As early as December last year, cracks had already appeared within the Aave community, detailed in "Can AAVE, embroiled in opposing sentiments after a significant sell-off, still be bought?".

Now, as Aave slows its pace due to governance friction, Morpho's governance model of "simplicity" has drawn attention. Aave can be regarded as the first-generation lending governance paradigm of "DAO-led, global parameter adjustment," where all risk parameters (such as collateral factors and liquidation thresholds) are determined by DAO global votes. Although this design ensures overall robustness, it is easy to fall into governance bottlenecks—any parameter adjustment requires broad consensus from the community, and any disagreement may lead to delays, especially during controversial periods when decision-making can be paralyzed.

In contrast, Morpho follows a modular, market-driven second-generation path: the protocol itself is highly permissionless, allowing anyone to create isolated markets at any time. The risk parameters of each market (such as LTV, interest rate curves, liquidation incentives) are set by independent professional risk managers (curators), rather than relying on global DAO votes. This means risk is strictly localized within individual markets, responsibility is distributed to specific curators, and decision-making speed is significantly improved without waiting for global consensus, allowing curators to quickly iterate parameters based on actual market conditions. The advantage of this design is a significant reduction in governance friction and decision delays.

When the old dynasty begins to wear itself down, it may be the opportunity for new forces to overtake.

Data Validation: Does It Deserve This Window?

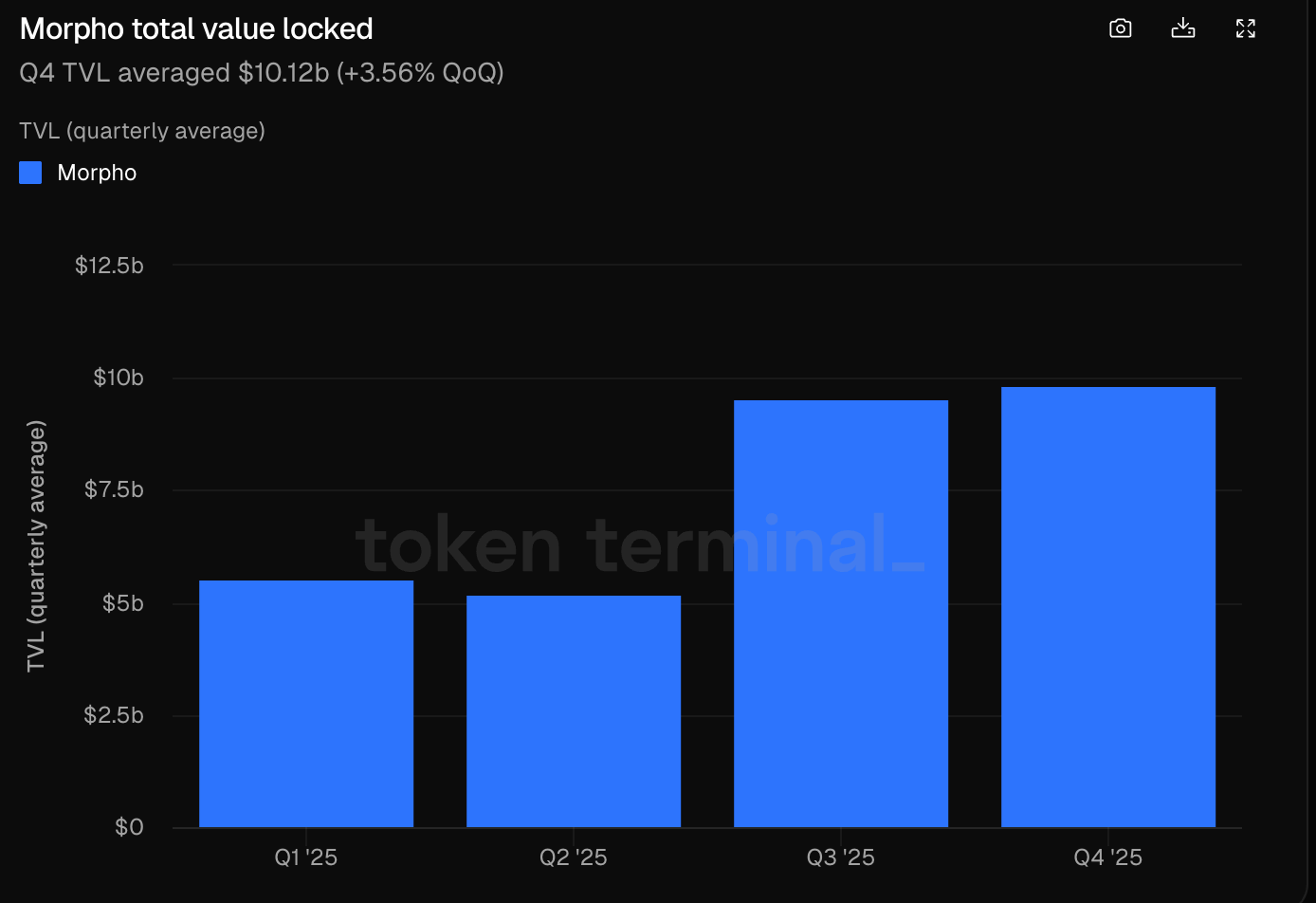

Let’s take a look at the fundamentals of Morpho to see if it has the potential to challenge Aave's lending throne. According to Tokenterminal data, in Q3 and Q4 of 2025, Morpho's protocol TVL (Total Value Locked) consistently maintained above $9.5 billion, growing approximately 80% compared to the previous half-year;

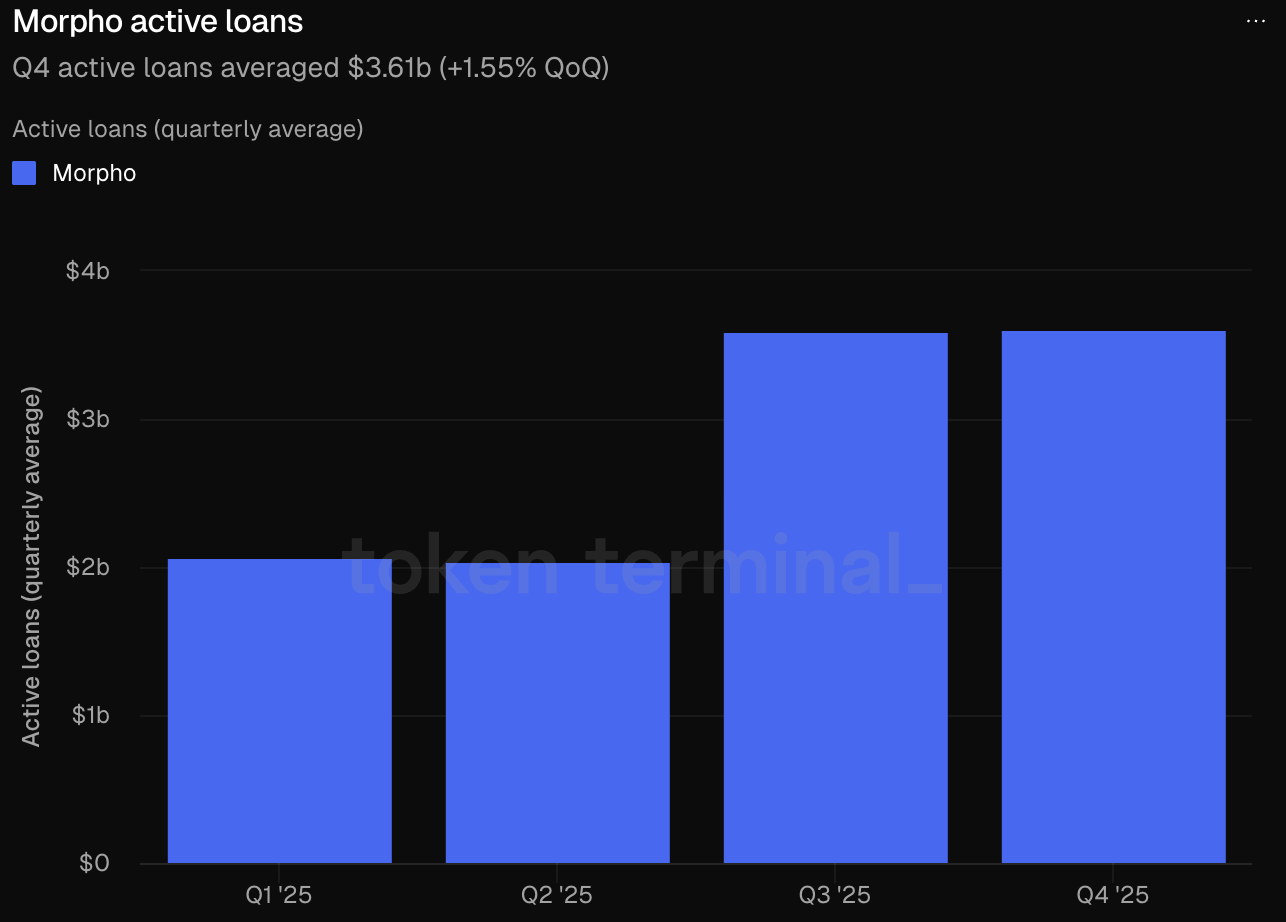

The scale of active loans within the protocol also exceeded $3.5 billion in both Q3 and Q4, with a year-on-year growth rate of about 80%.

In terms of one of the core metrics for DeFi protocols—protocol revenue—except for a relatively weak performance in Q2, other quarters have basically stabilized around $50 million.

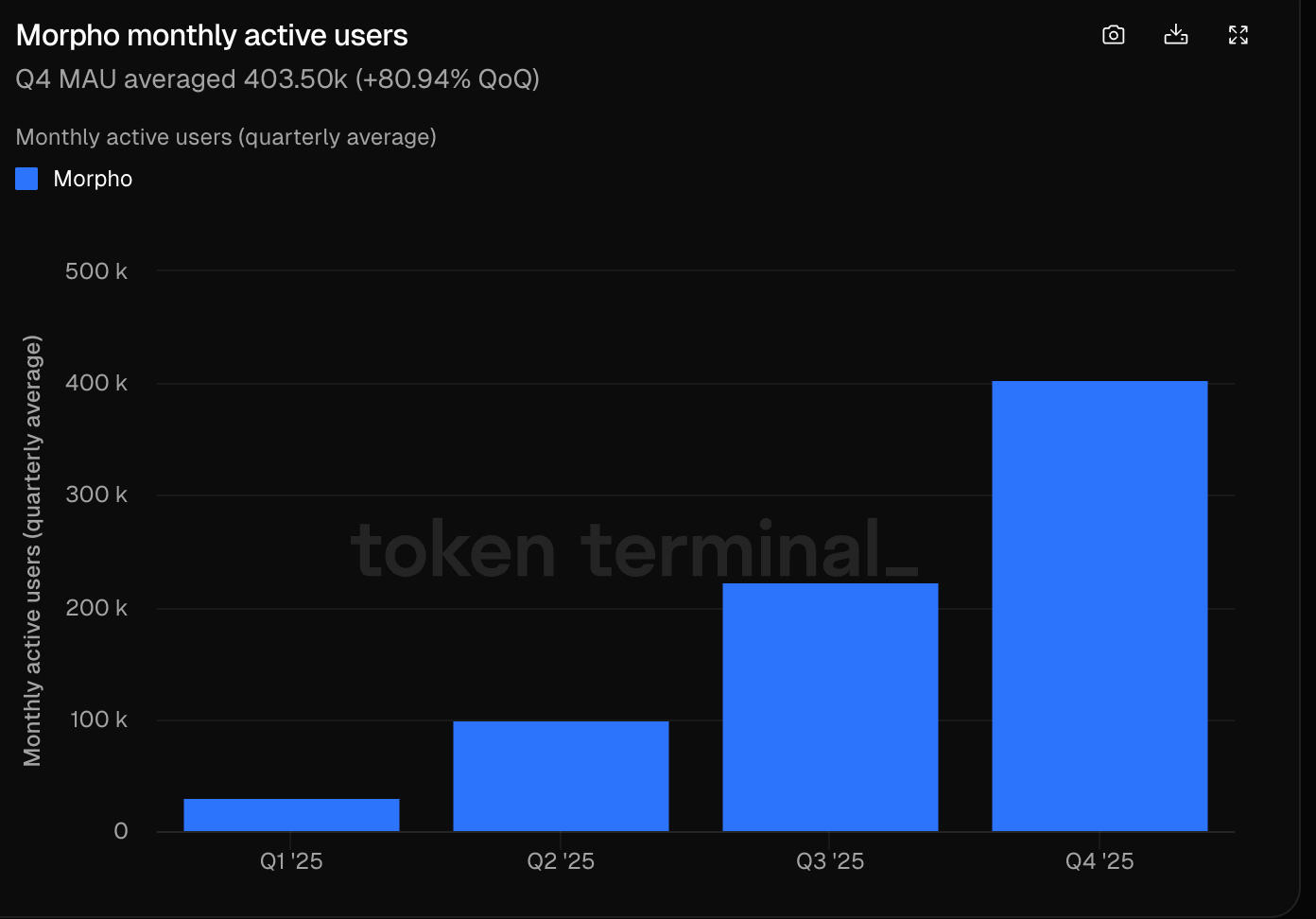

User growth is even more intuitive; the number of quarterly active addresses expanded rapidly from about 30,000 in Q1 to around 400,000, demonstrating strong organic growth momentum.

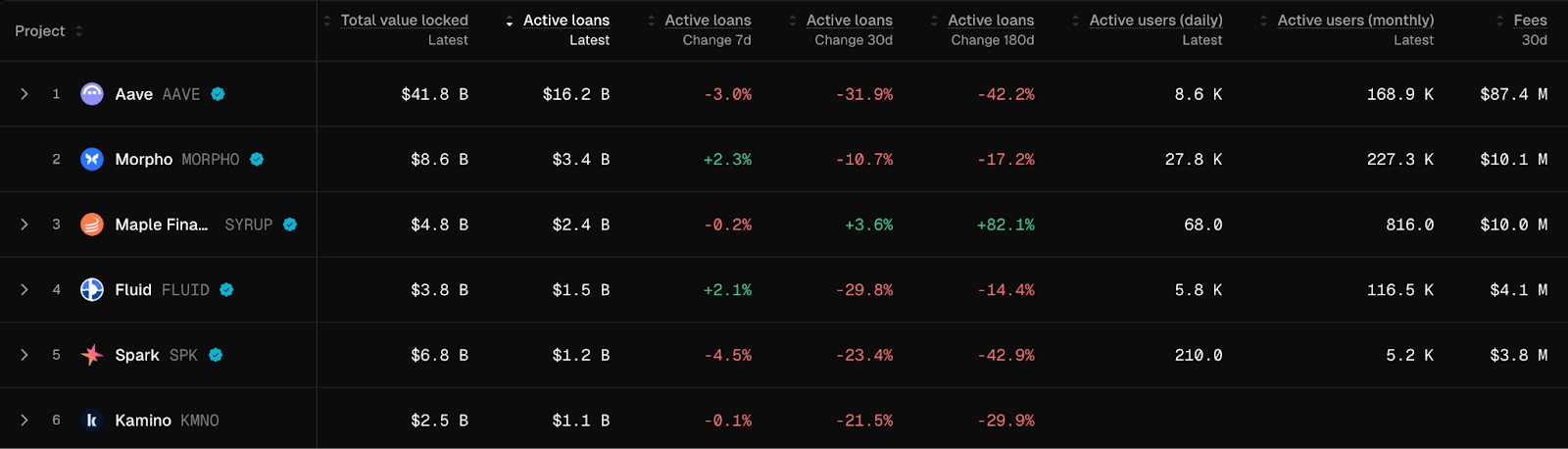

Although Morpho's current TVL and active loan scale still do not match Aave, its user growth rate has made it one of the most formidable "dark horses" in the lending track. Especially in the context of the entire DeFi landscape facing pressure and experiencing growing pains in 2025, Morpho’s performance can be regarded as achieving high growth against the trend, sufficient to prove its product model has withstood the market test. Moreover, protocols that can consistently attract funds and users during bear markets often possess stronger explosive potential in the next cycle.

Institutional Variables: When Traditional Capital Begins to Bet

Strong fundamentals can only prove that this protocol has a solid foundation, but the bigger catalyst that truly changes the market capitalization curve is the entry of traditional financial giants.

On February 13, Wall Street asset management giant Apollo Global Management signed a significant collaboration agreement with Morpho's nonprofit organization Morpho Association, planning to gradually acquire up to 90 million MORPHO tokens over the next 48 months, equivalent to about 9% of Morpho’s total supply, valued at approximately $160 million at the current price of $1.8.

If viewed purely from a trading perspective, this will bring sustained buying demand for MORPHO. However, if you are familiar with Apollo, you would understand that this may be more like a strategic infiltration into DeFi.

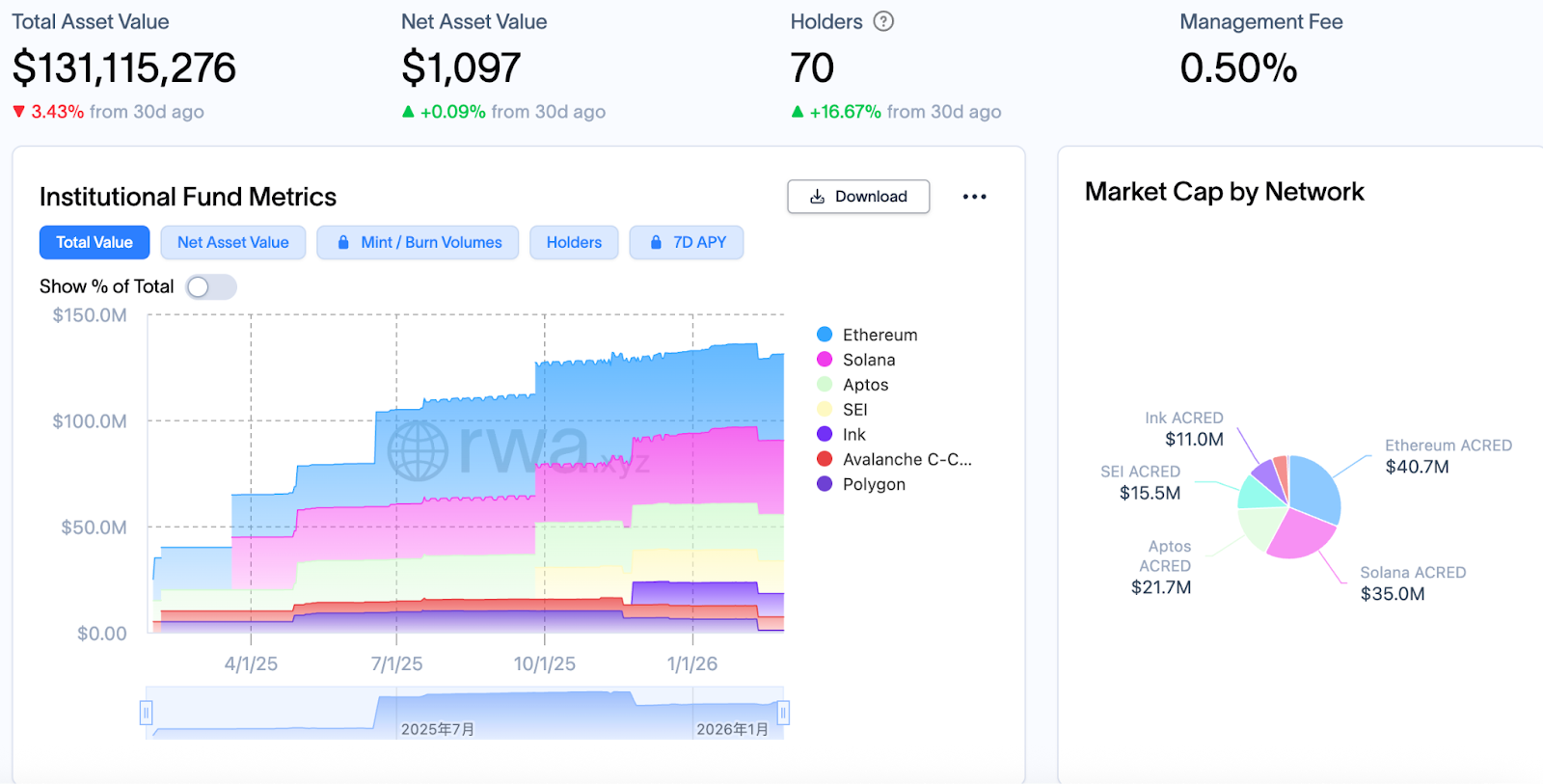

Apollo manages nearly $940 billion in assets, and its private credit business is known for pursuing high returns, while the on-chain world provides opportunities for leverage amplification and global instant liquidity. Since 2024, it has been testing the cryptocurrency industry, using RWA (Real World Assets) as its main battlefield, partnering with Securitize to tokenize its diversified credit strategy into ACRED, currently reaching a scale of $130 million.

However, the core issue after RWA is on-chain has never been issuance, but liquidity release. Assets can be tokenized, but without an efficient lending market and leverage environment, their return potential cannot be released. From Apollo’s layout, it is reasonable to speculate that it likely aims to utilize Morpho’s lending market to amplify the returns of its credit products. Because Morpho’s modular lending structure provides a natural fit for RWA—isolated markets, independent risk parameters, customizable leverage environments; these mechanisms are far more attractive to institutions than parameter games under unified governance.

This assumption is not without basis, as although Morpho is highly permissionless, key parameter options still need to be expanded through Morpho DAO governance. If Apollo holds a substantial amount of MORPHO tokens, it will gain corresponding voting rights, potentially pushing for the addition of RWA-friendly parameters. If Apollo's intentions come to fruition, Morpho’s modular design could attract a faster influx of institutional funds, making it a crucial infrastructure for amplifying institutional credit products on-chain. This level of institutional endorsement would not only strengthen Morpho's competitive advantage but also narrow the gap with Aave—especially as Aave finds itself deeply mired in internal governance quagmires.

Conclusion

Aave's governance crisis may continue to drag down its market value and liquidity in the short term, while Morpho is quietly rewriting the competitive landscape of the lending track by leveraging its structural advantages and institutional catalysts. However, whether Morpho can truly shake Aave's throne remains to be seen as it continuously pursues TVL growth and more TradFi players enter. But at least for now, this power transition of the "second generation of lending" has already begun.

Risk Warning: The MORPHA token will welcome a large unlock in March, belonging to Morpho DAO, Morpho Association reserves, and core contributors, with short-term liquidity shocks needing to be monitored.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。