Written by: FinTax

1 Introduction

As cryptocurrency assets move from the fringes to the mainstream, the global tax regulatory "net" is accelerating its weave. Following the official release of the 2025 version of the digital asset broker information reporting form (Form 1099-DA, referred to as 1099-DA) and its accompanying operational guidelines, the Internal Revenue Service (IRS) recently updated two detailed rules. This move clarifies the mandatory reporting obligations of digital asset brokers and further refines the exemption threshold for small transactions (De Minimis) through supplementary rules, while innovatively providing optional reporting methods for stablecoins and designated NFTs (Specified Non-fungible Tokens). This is more than just an update of a form; it demonstrates that regulatory granularity has been refined to a per-coin penetrative level. While ensuring tax transparency, regulatory authorities are reducing compliance costs for market participants through differentiated rules. This article dissects the recent update of Form 1099-DA to analyze the current regulatory trends and core implications of the IRS, providing compliance references.

2 Origins and Background: Contents and Background of Form 1099-DA

2.1 Overview

Form 1099-DA is the information reporting form that digital asset brokers use to report profits and losses from digital asset transactions to the IRS and clients. The 1099-DA is not just a patch for the existing system; it is a specially designed reporting form tailored to the native properties of digital assets.

According to the latest guidelines for 1099-DA (Instructions for Form 1099-DA (2025)), starting January 1, 2025, brokers must record and report the gross proceeds of each transaction. Notably, the IRS does not require the reporting of cost basis and nature of gains and losses in 2025, instead granting brokers a grace period for voluntary reporting and clarifying that there will be no penalties for reporting errors during this period. The mandatory reporting obligation for cost basis and the nature of gains and losses is postponed until 2026 (for "covered digital assets" acquired after January 1, 2026), allowing brokers a one-year system adjustment period to address historical challenges related to asset title confirmation and cost tracking.

Additionally, the latest guidelines for 1099-DA impose more refined requirements on data reporting granularity, primarily reflected in two dimensions: the "uniqueness" of asset identity, affirmatively introducing the standardized DTIF (Digital Token Identifier Foundation) identification code to eliminate the ambiguity of token naming; the "structuring" of transaction nature, implemented by isolating reporting of specific asset flows to distinguish between primary sale profits and investor transfer gains and losses. Specifically, the IRS introduced Box 11c, which isolates the original minting profits of specified NFTs creators from the secondary market transfer profits for the first time, enabling the IRS to receive more granular reporting data.

Digital Assets: According to 1099-DA, digital assets refer to any value represented in a digital format, recorded on a cryptographically secured distributed ledger (such as blockchain or any similar technology), regardless of whether each specific transaction involving the digital asset is actually recorded on that distributed ledger; at the same time, the asset is not classified as cash (i.e., it is not issued by the government or central bank as dollars or any convertible foreign currency). Therefore, the IRS's definition of digital assets is broad, encompassing any value digitally represented recorded on a cryptographically protected distributed ledger, including cryptocurrencies, tokenized securities, and designated NFTs.

Qualifying Stablecoins: A digital asset qualifies as a stablecoin if it meets the following three conditions:

(1) The digital asset is designed to track a single convertible currency issued by a government or central bank (including dollars) at a 1:1 ratio;

(2) The digital asset adopts an effective stabilization mechanism;

(3) The digital asset is widely accepted as a means of payment by entities other than the issuer.

Regarding the reporting entities, 1099-DA primarily targets brokers and digital asset intermediaries.

Brokers: According to the revised provisions under Section 6045 of the Internal Revenue Code, brokers are defined as any person prepared to execute digital asset sales on behalf of others in the ordinary course of business. In terms of digital asset sales, an entity is considered a broker if it meets the following conditions:

(1) Regularly proposes to clients the redemption of digital assets it has created or issued; or

(2) Acts as an agent, dealer, or digital asset intermediary to carry out the disposal of clients' digital assets.

Digital Asset Middleman: Individuals who facilitate digital asset sales and can identify the seller's identity and the nature of transactions.

Entities that qualify as digital asset intermediaries include:

(1) Accepting or processing digital assets as a means of payment for stocks, commodities, regulated futures contracts, security futures contracts, forward contracts, foreign currency contracts, debt instruments, options, or security futures contracts;

(2) Real estate reporting individuals who are actually aware of or should generally be aware that real estate buyers are using digital assets for payment;

(3) Accepting digital assets as remuneration for brokerage services;

(4) Owning or operating one or more digital asset vending machines; or

(5) Digital asset payment processors (PDAP).

Entities that do not qualify as digital asset intermediaries include:

(1) Solely engaging in providing proof of work (PoW) or proof of stake (PoS) distributed ledger verification services (staking/mining), without offering any other functions or services; or

(2) Solely providing hardware or software (through sales, licensing, or other means) that allow users to control private keys to access digital assets on a distributed ledger (such as non-custodial wallets), without offering any other functions or services.

In summary, digital asset intermediaries include not only traditional CEX (centralized exchanges) but also extend to custodial wallet providers, payment processors (PDAP), and digital asset vending machine operators.

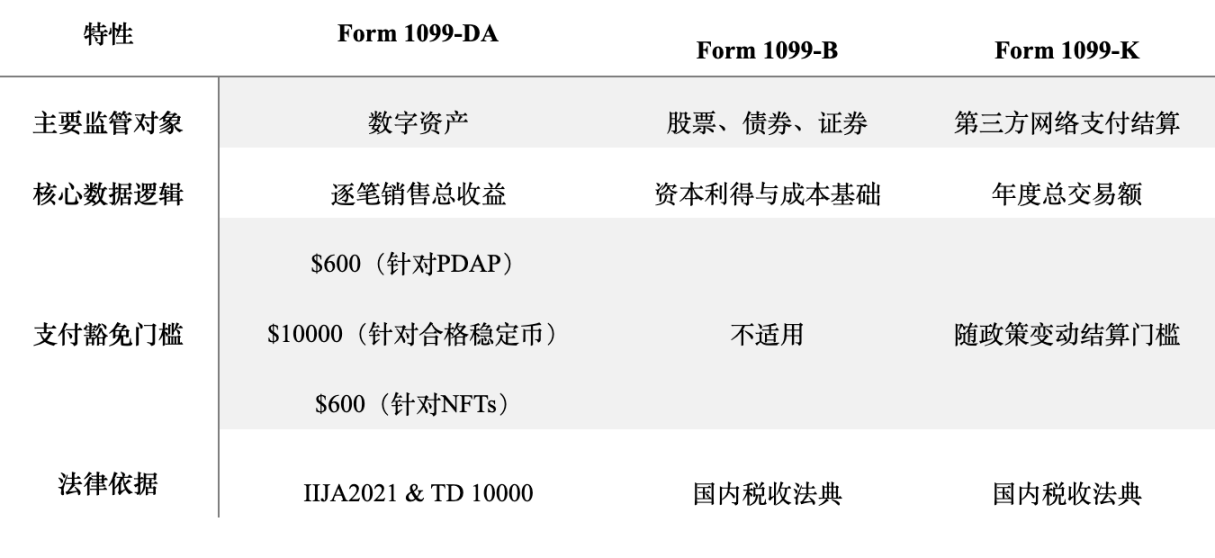

To visualize the uniqueness of 1099-DA, the table below compares it with the reporting forms in traditional finance and payment sectors.

2.2 Core Content

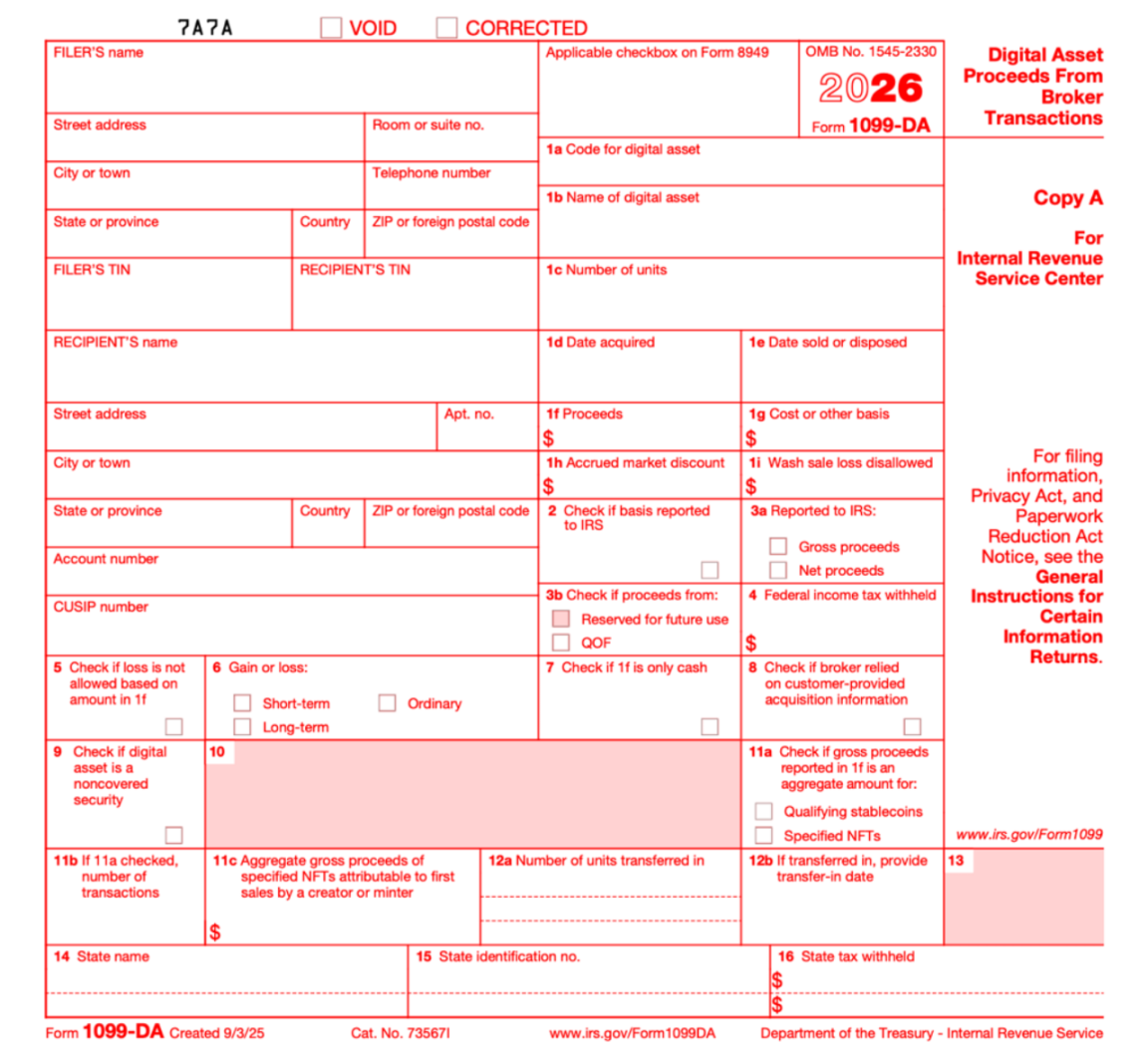

The structure of the 1099-DA form corresponds to the traditional securities 1099-B but adds several detailed boxes to account for cryptocurrency characteristics:

- Box 1a & 1b (Digital Asset Code and Name): Mandatory introduction of DTIF coding; if a certain token lacks a DTIF code, it must be marked as "999999999" (alphanumeric identifier). If utilizing the optional summary reporting method for specified NFTs, Box 1a also requires "999999999", and Box 1b should state "Specified NFTs"; for the qualified stablecoin optional summary reporting method, Box 1a should indicate the DTIF identifier of that stablecoin, and Box 1b should specify the stablecoin's name.

- Box 1f (Total Amount Received): May include cash and the fair market value of the services, digital assets, or other properties received.

- Box 1g (Cost Basis): Although voluntary for reporting in 2025, it will become crucial for calculating gains and losses in the future.

- Box 11a & 11b (Summary Reporting Flags): Special paths designed for stablecoins and specified NFTs, recording whether the optional reporting method was used and the number of transactions covered.

- Box 11c (Primary Market Sale): Specifically used to capture the original minting profits of specified NFTs creators, distinguishing it from secondary market transfers.

2.3 Background of Form 1099-DA

2.3.1 Within the United States

In August 2021, the Infrastructure Investment and Jobs Act (IIJA) was passed by the Senate and signed into law in November of the same year. This act amended Section 6045 of the Internal Revenue Code, explicitly including "digital assets" within the legal definition of "brokers" for reporting purposes, aiming to enhance tax transparency through a third-party automatic reporting system.

After two years of professional consultation and public discussion on policy details, on July 9, 2024, the U.S. Department of the Treasury and the IRS officially released Treasury Decision 10000 (Gross Proceeds and Basis Reporting by Brokers and Determination of Amount Realized and Basis for Digital Asset Transactions), effective September 9, 2024, which precisely defines the constituent elements of a broker in legal terms, clarifies the types of transactions required for reporting, and thoroughly outlines the methodology for calculating cost basis.

TD 10000 stipulates that 1099-DA will officially come into effect in 2026, and each box setting is legally supported by TD 10000, requiring brokers to report digital asset profit and cost basis information from January 1, 2025.

2.3.2 Outside the United States

It is noteworthy that the introduction of 1099-DA represents not only a unilateral upgrade of tax regulatory frameworks for digital assets within the United States but also resonates with the global trend towards tax transparency. At the end of 2022, the Organisation for Economic Co-operation and Development (OECD) officially released the Crypto-Asset Reporting Framework (CARF), aimed at establishing a standardized automatic exchange of tax information concerning crypto-assets worldwide. On November 10, 2023, the United States and over 40 other countries issued a joint statement committing to accelerate the implementation of the CARF framework. On July 30, 2025, the U.S. will release a white paper proposing the implementation of CARF. On November 14, 2025, the IRS submitted a proposal to the White House regarding CARF: US Broker Digital Transaction Reporting, aimed at implementing CARF, and the White House is currently reviewing this proposal. If the United States implements CARF, it will allow the IRS to obtain key information regarding U.S. tax residents' overseas cryptocurrency accounts and exploit this information for tax enforcement.

Although the United States has not yet signed the CARF multilateral agreement, nor initiated automatic exchanges of crypto-asset tax data based on CARF with other jurisdictions, the formal implementation of 1099-DA marks that the U.S. has proactively built a mature underlying data collection system, laying a technical foundation for future automatic exchange of tax data with other countries.

3 Riding the Wave: Recent Policy Interpretation of 1099-DA in the U.S.

Recently, the IRS has significantly accelerated its regulatory pace regarding crypto-assets, demonstrating that its policy output is no longer confined to macro compliance requirements but has evolved into concrete standards with execution power and efficiency.

3.1 Small Transaction Exemptions and Summary Reporting Details

While maintaining strict regulation, the IRS has shown a degree of flexibility in the new rules, forming a burden-reducing system through nested small transaction exemption rules (De Minimis Rules) and optional reporting methods, filtering layers to avoid regulatory redundancy.

Specifically, brokers first determine whether a transaction applies to the "optional reporting method" based on the nature of the asset. Once the optional reporting method is selected, the IRS provides corresponding "small transaction exemption thresholds" that only require reporting on 1099-DA if the transaction amount exceeds the specific threshold; otherwise, reporting is exempted.

The optional reporting method determines "how to report": For qualified stablecoins with minimal value fluctuations and consumer attribute designated NFTs, under the conditions of the optional reporting method, the new rules allow brokers to simplify or be exempt from transactional reporting and instead use aggregate reporting.

The small transaction exemption rule determines "whether to report": To avoid excess impact on the tax audit system from a massive amount of retail consumption data (such as using cryptocurrency to buy coffee or making everyday small payments), the IRS has set differentiated small transaction exemption thresholds based on different transaction types and reporting methods:

- Digital Asset Payment Processor (PDAP) Sales Threshold: $600

If a digital asset payment processor (PDAP) processes total payments of $600 or less for the same customer within a year, there is no need to report on Form 1099-DA.

- Qualifying Stablecoin Optional Reporting Threshold: $10,000

For qualifying stablecoins reported under the optional method, if the total specified sales proceeds (after deducting relevant transaction costs) do not exceed $10,000 for the year, the broker may be exempt from reporting.

- Designated NFTs Optional Reporting Threshold: $600

For designated NFTs transactions reported under the optional method, if the total sales proceeds from all designated NFTs (after deducting transaction costs) do not exceed $600 for the year, the broker may be exempt from reporting.

3.2 Exclusion of Joint Reporting Programs

Additionally, another recent technical development is that the IRS has clarified that the 1099-DA for the 2025 tax year will not participate in the "Federal/State Joint Filing Program (CF/SF)," meaning brokers can no longer complete state tax data reporting in one click through the federal system, or must submit data individually to local tax authorities per state law.

4 Conclusion

In the face of the multiple challenges posed by 1099-DA, high-net-worth investors, project parties, and Web3 organizations and related market participants urgently need to adapt to the new reporting rules. For Web3 practitioners, the governance of transaction data is not only for meeting the IRS's reporting requirements and audits but also to perfect their clear financial mapping. In this wave of transparent regulation, those who can first complete the upgrade from "chaotic accounts" to "tax compliance" will be the ones able to win long-term certainty in the increasingly competitive global Web3 landscape.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。