Based on Ethena's current yield levels, holders can obtain very competitive returns.

Written by: Jonaso

Translated by: Tim, PANews

Recently, we have witnessed the explosive growth of ENA, not only with its price skyrocketing but also attracting significant attention, rising at an astonishing speed.

However, what most people do not realize is that the main catalyst has yet to appear, which is the fee switch.

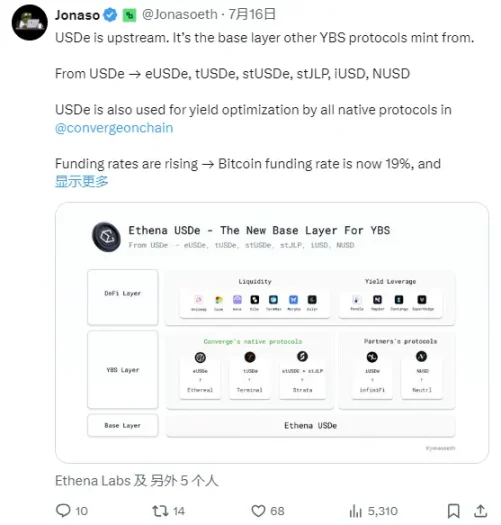

The Rise of a New Stablecoin Giant

In less than a year, the supply of USDe has surged from 0 to over $6 billion, surpassing DAI to become the third-largest decentralized stablecoin, only behind USDT and USDC.

The annualized yield of sUSDe has reached 10%, making it the highest sustainable yield in the current crypto space. The surge in yields is driving the development of aggressive circular arbitrage strategies on Aave and other decentralized platforms.

Financing rates are continuously rising, with the current Bitcoin financing rate at 19% and Ethereum at 12%, marking the first time in six months that both have simultaneously broken the 11% benchmark.

Ethena's revenue reached $7.8 million this week, with an annualized expected income exceeding $400 million. Conservative estimates still indicate room for growth, as Ethena has currently transferred 41% of its stablecoin reserves into higher-yield perpetual contract strategies, while the market average funding rate has reached 14%.

A higher annualized yield simultaneously meets the key condition for enabling the ENA fee switch: the yield of sUSDe must be at least 5% higher than the current Sky savings rate (currently at 4.5%), a milestone that has now been confirmed.

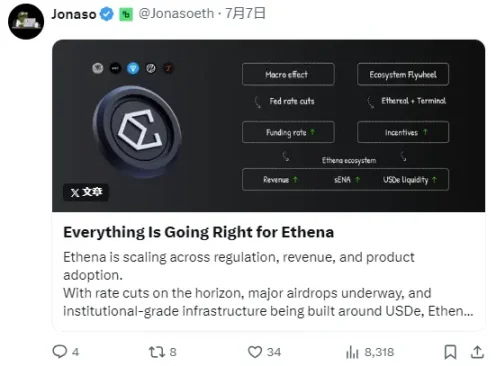

Market Macro Perspective: Federal Reserve Rate Cuts and Ethena's Stablecoin Strategy

Ethena's business model is derived from market volatility and the high funding rates of perpetual contracts.

Unlike traditional stablecoins (such as USDC or USDT) that rely on government bond interest, Ethena's yield comes from its neutral hedging strategy: going long on spot while shorting perpetual contracts.

When funding rates are high, Ethena can generate more income. For this reason, many expect that if the Federal Reserve begins to cut rates as predicted at the end of 2025, Ethena will see even greater returns.

In fact, after the most recent rate cut in December 2024, Ethena set a record for monthly revenue, reaching $12 million.

Ecosystem Growth and Strong Metrics

Ethena has rapidly risen to become one of the top DeFi protocols by TVL, currently surpassing $6 billion in TVL while achieving nearly $400 million in revenue, placing it among the most profitable DeFi projects today.

Three flagship products are helping expand the Ethena ecosystem:

Ethereal: A decentralized perpetual contract exchange with a TVL of approximately $712 million.

Terminal: A liquidity hub focused on tokenized assets, currently with a TVL of nearly $129 million.

Strata: A structured yield product with a TVL of $13 million.

Meanwhile, Ethena is undergoing multi-chain expansion.

The trading volume of USDe on Bybit has surpassed that of USDC ($540 million vs. $444 million).

On the TON network, the TVL of the stablecoin USDe has reached $87 million in just six weeks.

Institutional Capital and Token Buyback

Recently, Ethena announced a partnership with the asset management company StablecoinX. StablecoinX plans to list on the Nasdaq under the stock code USDE.

This round of financing attracted participation from well-known crypto VCs such as Pantera, Dragonfly, and Wintermute, raising a total of $360 million.

Of this, $260 million will be used for ENA buybacks in the open market over the next six weeks, absorbing nearly 8% of the circulating supply of the token.

StablecoinX will permanently include ENA on its balance sheet for long-term holding, aiming to reduce the market circulation of the token to support the long-term development of the protocol.

Fee Switch: The Real Catalyst

While the above factors have driven the rise of ENA, the true catalyst has yet to appear, which is the fee switch.

Despite strong market performance, the ENA and sENA tokens currently lack a mechanism to directly capture that value.

To address this issue, the Wintermute governance team has submitted a proposal to initiate the fee switch mechanism, aimed at allowing token holders to share in the revenue.

This mechanism will enable sENA holders to receive a share of the protocol's income. In other words, it will create real value for token holders, allowing ENA to transcend being merely a governance token.

To activate the fee switch, Ethena must meet five conditions. As of July 2025, four of the five conditions have already been met:

USDe supply exceeds $6 billion

Cumulative revenue exceeds $250 million

1% reserve fund of total supply

Interest spread ≥ 5%

The only remaining condition is to list USDe on Binance or OKX (the token is already listed on Bybit, MEXC, and Bitget).

Once this final step is completed, the fee switch can be activated, at which point sENA holders will begin to receive a portion of the Ethena project's revenue.

Based on Ethena's current yield levels, holders can obtain very competitive returns.

Conclusion

Once the fee switch is activated, ENA will take off.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。