Written by: Nancy, PANews

"It’s time to move beyond Bitcoin and MEME coins; the market is shifting towards 24/7 on-chain trading and real assets with actual utility." This statement by Robinhood CEO Vlad Tenev, made after the official announcement of tokenized stock trading, depicts the current craze for tokenized stocks and reveals the profound changes the crypto market is undergoing.

With platforms like Robinhood, Kraken, and Coinbase sequentially venturing into tokenized stocks, the crypto world is witnessing a restructuring of market dynamics and capital flows. Some voices believe that tokenized stocks, as a significant innovation in the crypto space, are expected to expand the overall market capital scale, helping the crypto ecosystem transition from the margins to the mainstream. Others argue that the introduction of quality assets may pose a severe impact on altcoins that rely on narrative-driven value. Currently, tokenized stocks are still in their early stages, facing multiple challenges such as insufficient liquidity and regulatory hurdles that need to be overcome.

Are Altcoins Heading Towards Marginalization?

As traditional quality assets like U.S. stocks gradually become "on-chain," the flow of capital in the crypto market is quietly changing.

Some market perspectives suggest that tokenized traditional quality assets, backed by clear business models, compliant regulatory frameworks, and stable real returns, are becoming the new favorites for on-chain capital, creating a siphoning effect on the altcoin market. In particular, tokens that lack real revenue models, have immature products, and rely solely on narratives to support their market value are facing liquidity exhaustion and survival pressure.

For instance, crypto KOL BITWU.ETH posed a sharp question: "When traditional quality assets are tokenized and can be traded on-chain, do crypto-native assets still hold value? Investors can directly purchase highly liquid, stable, and clearly valued assets like Apple and Tesla on-chain; why gamble on an altcoin that 'might' develop a product?" He believes that the structural differentiation of altcoins has officially begun, with more high-quality real assets appearing on-chain, while narrative-driven altcoins may be directly marginalized and face extinction.

Of course, this trend also signifies that the crypto market may bid farewell to an era driven solely by narratives, moving towards a more rational, value-oriented development path. Crypto analyst Crypto_Painter pointed out that altcoins may not necessarily disappear; they are just becoming increasingly difficult to sustain. In the crypto market, each new quality asset diminishes the value of those assets that rely on consensus to maintain their price. The only way forward for altcoins is to generate real application value, and it must be value that can bring actual income. All tokens that cannot materialize and rely solely on narratives for survival will gradually enter a death spiral. There may still be altcoin seasons, but the era of widespread price increases across thousands of coins is unlikely to return; simple models should be a thing of the past.

However, Qiao Wang from Alliance Dao believes that tokenized stocks will not kill altcoins; perpetual contracts for stocks will. Because they possess a continuous stream of new narratives combined with high volatility adjusted for leverage.

Colin Wu, editor-in-chief of Wu Says Blockchain, expressed a similar view. He pointed out that merely buying spot assets seems meaningless; the perpetual contracts for stock tokens may be the real game-changer. Traditional CEXs may find it somewhat challenging, but decentralized platforms like Hypeliquid could effectively provide stock perpetual contracts. The difficulty lies not only in regulation but also in the relatively long educational process required for traders of cryptocurrencies and stocks to engage with such hybrid products.

Cross-Border Invasion of Traditional Finance

Regarding the popular trend of tokenized stocks, many crypto practitioners and KOLs have expressed optimism, believing that bringing stocks on-chain is not just an innovation in trading tools but could fundamentally change the ecology and landscape of securities trading, as well as enhance the scale and depth of the crypto market.

The market environment, user demographics, and infrastructure that the synthetic asset protocol Mirror Protocol (which uses stablecoins to synthesize stock-like assets) operated in years ago are not on the same level as today. Crypto KOL Chen Mo CM pointed out that earlier, some questioned whether Hyperliquid would be the next dYdX, and now they say that tokenizing stocks is the next Mirror and FTX. In fact, the right thing may not succeed the first time, but success is a matter of time. The key lies in how well stocks become integrated as on-chain assets within the ecosystem; merely buying and selling is just the tip of the iceberg. The most significant change compared to before is the shift in regulatory attitudes. The U.S. stock tokens from Mirror were once not allowed to appear on the trading front of Uniswap, let alone the integration of multiple chains and ecosystems, which cannot be compared.

Crypto KOL Blue Fox added that a major feature of crypto technology is lowering trading barriers, which can promote trading freedom. For example, users in some regions who previously could not purchase securities now have the opportunity to do so. Even shares of some popular companies that are not publicly traded can circulate through tokenization. While these developments have not yet materialized, they are beginning to take shape. At the same time, a harsh reality will emerge: behind free trading, a concentration effect will occur, where some leading assets and currencies will gain increasingly larger opportunities, while relatively weaker currencies or assets will gradually become marginalized due to the loss of protective barriers. Of course, new assets with narrative capabilities will also have more opportunities. The true impact of crypto technology is just beginning. From an investment perspective, new opportunities and new traps will continuously emerge.

Crypto KOL @Cody_DeFi emphasized that directly purchasing U.S. stocks within DeFi protocols is a significant leap for tokenizing stocks, meaning stocks can also be priced through AMM and can engage in Loop and Yield Swap. These financial derivatives would be very complex and lengthy if done through traditional finance, as they require a cumbersome back-office support system. When stock assets can flow smoothly on-chain like tokens, it makes the simplicity and elegance of DeFi more intuitively evident. In simple terms, the core function of blockchain in finance is encapsulated in six words: "payment and settlement." This cannot be achieved in any traditional financial network with scale effects. Once "payment and settlement" are realized, even if U.S. stocks cannot be traded 24/7, tokenized U.S. stocks can, and the core of trading lies not in infrastructure but in liquidity matching. Under the conditions of payment and settlement, OTC can also possess capabilities comparable to exchange counters.

From a more macro perspective, BroLeon from Australia pointed out that the issuance of stock tokens signifies a cross-border invasion from traditional financial platforms to blockchain infrastructure, marking the beginning of a fusion between traditional finance and crypto assets as the compliance process for crypto assets progresses. Traditional CEXs should feel the arrival of strategic competition from another dimension and are likely to begin counterattacking soon; "stock tokens" should also soon become widespread across major CEXs. The tokenization of private equity in companies like OpenAI and SpaceX and their sale to retail investors is a global first, resembling the previous IEO model. This opens up a compliance precedent for the tokenization of non-public company assets, and once the ice is broken, it may trigger a wave of similar innovations (such as tokenization of new potential companies, real estate, and even artworks).

"In the future, there will be many innovations regarding equity tokenization, such as the exploration of perpetual equity contracts. These innovations could change the industry landscape. The U.S. SEC is now encouraging experimentation, which makes companies bolder and less fearful of legal risks or regulatory suppression." Galaxy Digital founder Mike Novogratz stated in a recent interview that Galaxy is currently working with the SEC and may soon tokenize Galaxy's stock as a first step.

Ash, head of the Aptos Foundation ecosystem, bluntly stated that tokenized stocks present an arbitrage opportunity for users in emerging markets and serve as an entry point to attract a larger scale of retail users to engage with cryptocurrencies. If this trend truly emerges in the next 2-3 years, it would be a significant boon.

Still Facing Multiple Challenges of Insufficient Liquidity and Compliance

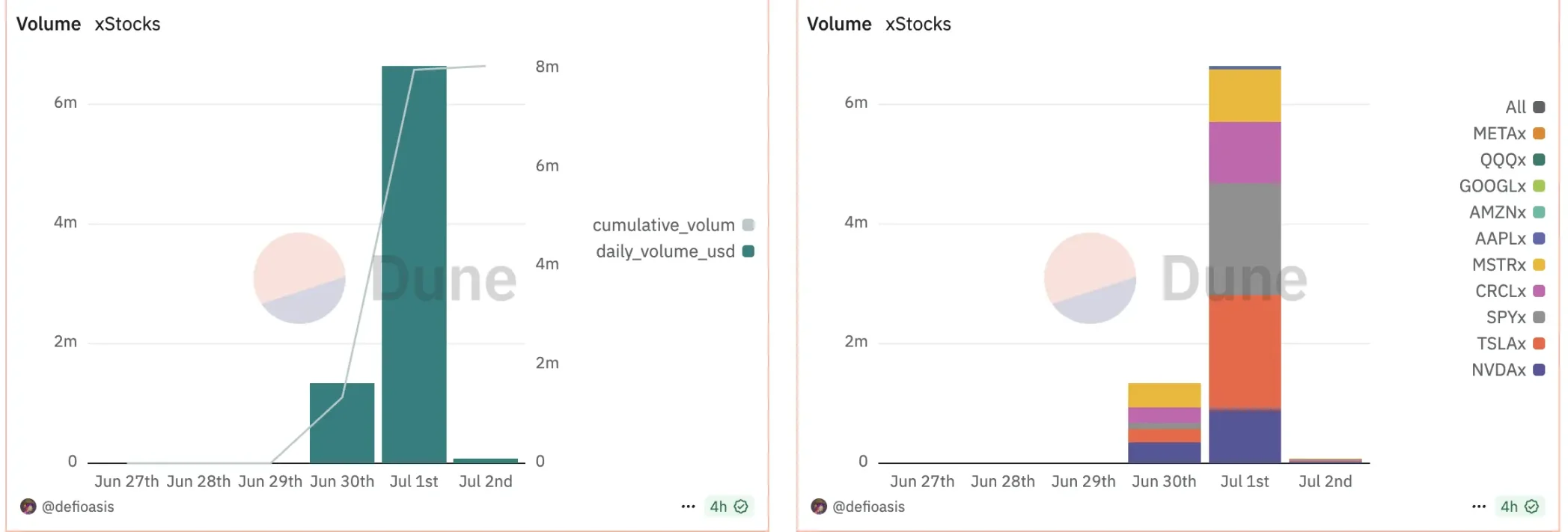

Despite the growing popularity of the concept of tokenized stocks, the overall market is still in its early stages, far from forming sufficient market depth. For example, according to xStocks data, Dune data shows that its total trading volume is only about $8.05 million, with fewer than 8,000 users, and only three stock tokens (SPYx, TSLAx, CRCLx) reached a trading volume of one million dollars within 24 hours. It is evident that actual liquidity on-chain remains quite limited.

Velocity Capital investor DeFi Cheetah also referenced early attempts like Mirror Protocol and Synthetix, pointing out that their failures were primarily due to a lack of meaningful liquidity. Simply tokenizing stocks is not difficult; the real challenge is having sufficient liquidity to support global-scale trading, which is still hard to match with traditional markets at this stage.

Dragonfly partner Rob Hadick also highlighted the structural flaws in current tokenized stock products, noting that the market's expectations for tokenized stocks are too high while lacking in details. He believes that most platforms currently rely on SPVs (special purpose vehicles) to purchase equivalent real stocks as collateral, but they can mostly only buy during U.S. stock market hours. This means that all after-hours/weekend trading requires market makers to bear the price risk themselves. However, these price fluctuations are difficult or nearly impossible to hedge in traditional finance. Moreover, even for redemptions, market makers must bear fees as high as 25 basis points (bps), which is a significant cost for them. Additionally, any DeFi protocol or market maker that inadvertently provides this token trading service to U.S. users will face compliance risks far exceeding those of other crypto assets. This means that weekend and after-hours trading is generally unsuitable for professional traders, and price fluctuations are highly coupled with official opening prices, making such products not user-friendly for most.

Despite the various challenges currently faced, Rob remains optimistic about the long-term potential of tokenized stocks. In the long run, when the primary market truly goes on-chain, collateral shifts to tokenized stocks, and traditional institutions upgrade their outdated technological frameworks, we will ultimately see: stocks appearing on-chain in the form of large-scale liquidity; smooth on-chain trading, accurate pricing, and active institutional participation; and the accelerated integration of infrastructure between crypto and traditional finance. Only then will be the inflection point for the explosion of tokenized stocks. The current products will merely be a small disappointing transitional product on the road to the future, potentially bringing some discussion and experimental value, but they will not be the endgame.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。