Written by: FinTax

1. Introduction

On May 21, 2025, the Hong Kong Legislative Council officially passed the "Stablecoin Bill" (hereinafter referred to as the "Stablecoin Ordinance"), which was published in the Gazette on May 30, 2025, and will be implemented within the year. Following the progress of the Legislative Council, the Hong Kong Monetary Authority (hereinafter referred to as the HKMA) released two consultation documents (drafts for public consultation) on May 26: the "Consultation Document on Proposed Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT) Requirements for Regulated Stablecoin Activities" (hereinafter referred to as the "AML Consultation Document") and the "Draft Guidelines for Regulating Licensed Stablecoin Issuers" (hereinafter referred to as the "Regulatory Guidelines Consultation Document"). The former clarifies the anti-money laundering and counter-terrorist financing obligations that licensed stablecoin issuers must fulfill, while the latter covers regulatory standards for reserve asset management, information disclosure, cybersecurity, and financial soundness, aiming to standardize the operational framework for licensed issuers. The Stablecoin Ordinance marks a milestone in the regulation of virtual assets in Hong Kong, and together with the future officially released AML Consultation Document and Regulatory Guidelines Consultation Document, it will form the legal foundation for Hong Kong's stablecoin market.

Not long before this, the "Guiding and Establishing National Innovation for U.S. Stablecoins Act" (hereinafter referred to as the "GENIUS Act") was passed in the U.S. Senate with a vote of 66 in favor and 32 against. This indicates that both the U.S. and Hong Kong, as major global financial centers, are engaged in a regulatory competition surrounding stablecoins and even the international monetary system. Can Hong Kong leverage its geographical advantages, mature financial system, and open stance towards innovative technologies to become a practical model for the global stablecoin market? This article will focus on analyzing the institutional highlights and legislative process of Hong Kong's Stablecoin Ordinance, and through a comparison of the stablecoin bills in the U.S. and Hong Kong, assess their potential impact on the crypto industry.

2. Overview of Hong Kong's Stablecoin Legislative Process

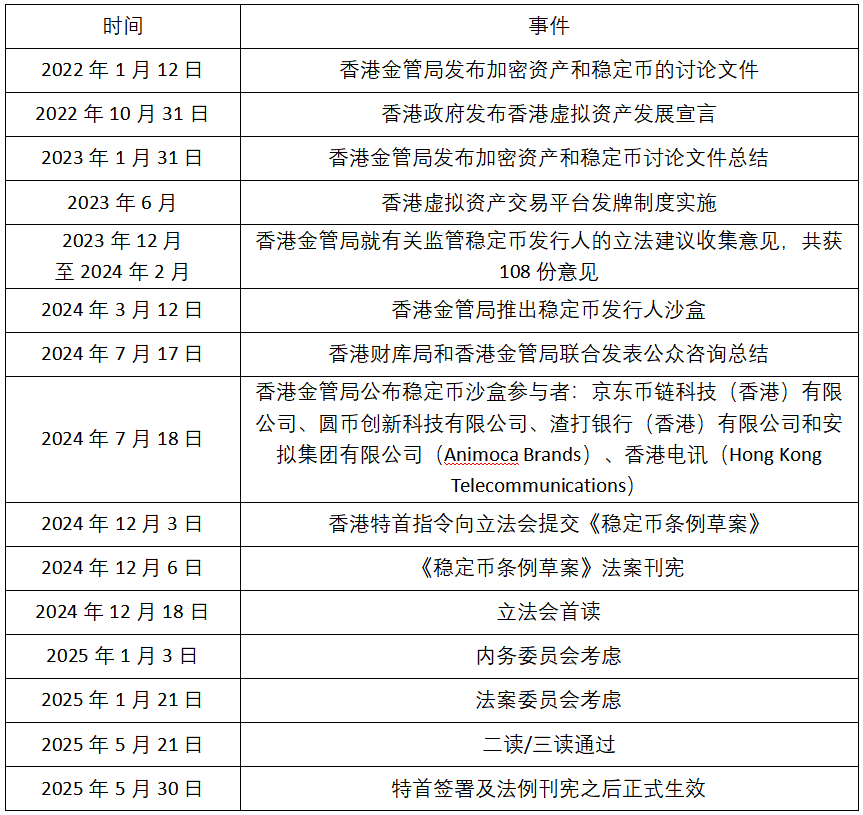

This section summarizes the legislative process of Hong Kong's stablecoin in the table below:

From the discussion document on crypto assets in early 2022, to the implementation of the licensing system for virtual asset trading platforms in 2023, and the completion of sandbox testing to verify technical feasibility in 2024, culminating in the third reading of the legislation in May 2025, it is evident that the Stablecoin Ordinance, which has preempted the GENIUS Act, is not a hasty initiative but rather a product of a comprehensive legislative process spanning three and a half years.

3. Main Content and Highlights of the Stablecoin Ordinance

3.1 Main Content

The Stablecoin Ordinance consists of 11 parts with a total of 175 articles, providing detailed explanations on the definition of stablecoins, licensing system, obligations of licensees, powers of the HKMA, criminal offenses and penalties, and supervisory mechanisms. We will outline the main content framework of the Stablecoin Ordinance from three aspects: the definition of stablecoins, reserve asset requirements, and issuer requirements.

3.1.1 Definition of Stablecoins

In terms of regulatory targets, the Stablecoin Ordinance defines stablecoins as "cryptographically protected digital forms of value" that meet five key criteria: (1) expressed in a unit of account or as a store of economic value; (2) used or intended to be used as a medium of exchange for payment, debt settlement, or investment; (3) capable of being electronically transferred, stored, or traded; (4) operating on a distributed ledger (which must meet the four characteristics of transaction record retention, network sharing, consensus verification, and node synchronization); (5) intended to maintain stable value by referencing a single asset or a group/basket of assets.

The aforementioned definition of stablecoins is relatively broad; however, only stablecoins that anchor to a certain standard value are subject to regulation under the Stablecoin Ordinance (defined as "designated stablecoins"). Article 4.1 of the Stablecoin Ordinance stipulates that designated stablecoins must fully reference "one or more official currencies" (such as the U.S. dollar or Hong Kong dollar), or reference "the unit of account or economic value storage form specified in the HKMA Gazette," or a combination of the above, and must maintain stable value through an asset anchoring mechanism. Therefore, algorithmic stablecoins that lack backing by physical assets, even if they meet the aforementioned definition of stablecoins, are excluded from the regulatory scope of the Stablecoin Ordinance due to their inability to satisfy the asset anchoring mechanism.

Additionally, the HKMA reserves the right to expand the scope of stablecoins. Article 4.2 of the Stablecoin Ordinance grants the Financial Commissioner the authority to include other digital forms of value in the scope of "designated stablecoins" through Gazette announcements, allowing the HKMA to dynamically adjust the regulatory scope in response to new types of cryptocurrencies.

3.1.2 Reserve Asset Requirements

As mentioned earlier, the Stablecoin Ordinance specifies two types of assets that stablecoins can anchor to: official currencies and assets designated by the HKMA. The HKMA has further detailed the requirements for reserve assets in the Regulatory Guidelines Consultation Document established under the Stablecoin Ordinance.

First, according to Article 2.1.1 of the Regulatory Guidelines Consultation Document, stablecoin issuers must ensure that their anchored reserve assets are fully covered. Issuers must maintain the market value of reserve assets at all times not less than the total face value of circulating stablecoins and must set buffers based on the risk characteristics of the assets (e.g., credit bonds require over 15% collateralization) to cope with market fluctuations. All assets must be denominated in the reference currency of the stablecoin (Hong Kong dollar stablecoins are exempt from holding U.S. dollar assets due to the linked exchange rate system). If currency mismatches are necessary, prior written approval from the HKMA must be obtained, along with the implementation of risk mitigation measures such as over-collateralization.

Second, reserve assets are limited to highly liquid, low credit risk statutory financial instruments, corresponding to Article 2.2.1 of the Regulatory Guidelines Consultation Document: bank deposits maturing within three months; tradable debt securities with a remaining maturity of no more than one year (must be issued or guaranteed by sovereign governments, central banks, qualified international organizations, or multilateral development banks, and must meet the 0% risk weight standard as stipulated in Articles 55-58 of the Banking (Capital) Rules, while absolutely prohibiting the holding of debt instruments issued by financial institutions and their affiliates); cash receivables from overnight reverse repurchase agreements guaranteed by high credit-rated counterparties; investment funds specifically established for managing reserve assets and other assets recognized by the HKMA.

Finally, Article 2.4.4 of the Regulatory Guidelines Consultation Document stipulates that reserve assets must be completely separated from the issuer's own assets through a statutory trust structure. The validity of the trust must be confirmed by a legal opinion from an independent lawyer and updated in the event of significant changes. The trust must be custodied by a licensed bank or an institution recognized by the HKMA, and the custody agreement must explicitly prohibit deductions from the reserve account to ensure priority repayment to stablecoin holders in the event of bankruptcy.

3.1.3 Issuer Requirements

According to Article 14 of the Stablecoin Ordinance, the issuer of stablecoins must be a legally registered entity, including local Hong Kong companies or qualifying foreign companies, and must have a substantial business presence in Hong Kong. On this basis, the Regulatory Guidelines Consultation Document proposes additional risk control measures. For example, if the issuing entity is a subsidiary of a group, its parent company must possess financial business qualifications and be subject to unified supervision at the group level. Banks can act as special issuers but must comply with both banking regulatory requirements and stablecoin-related regulations.

Regarding the amount of reserves, different entities have different reserve requirements. Non-bank issuers must maintain a paid-up capital of at least HKD 25 million or its equivalent in freely convertible foreign currency, ensuring that the capital is entirely independent for stablecoin business operations and prohibited from flowing to related parties. Bank-type issuers are exempt from this minimum capital requirement but must still meet the capital adequacy standards stipulated in Article 5.1.3 of the Regulatory Guidelines Consultation Document, and the capital used for stablecoin business must be strictly separated from the bank's other assets.

It is noteworthy that Article 7 of the Regulatory Guidelines Consultation Document imposes restrictions on corporate governance and personnel qualifications. The issuing entity must establish a governance structure with checks and balances, where at least one-third of the board members must be independent non-executive directors (INEDs). The appointment of the CEO, head of stablecoin business, and other key executives must receive prior written approval from the HKMA and undergo a "fit and proper" comprehensive assessment, covering professional competence, criminal record, financial soundness, and conflict of interest review. Information on managerial personnel must be filed with the regulatory authority, and their qualifications must continuously meet performance requirements. All key personnel involved in stablecoin business must undergo regular compliance training and behavioral supervision.

3.2 Highlights of Hong Kong's Stablecoin Regulation

As countries accelerate the implementation of stablecoin legislation, the Hong Kong Stablecoin Ordinance still has two major highlights.

First, the cross-border regulation of stablecoins is a key highlight of the Stablecoin Ordinance. Based on the traditional financial regulatory principle of "territorial jurisdiction," any designated stablecoin issued locally in Hong Kong must apply for a license to ensure that local financial activities are controlled. Hong Kong's innovation lies in breaking geographical limitations by extending regulation to stablecoins issued overseas. Specifically, if an overseas-issued stablecoin is pegged to the Hong Kong dollar or actively promoted to the Hong Kong public, it will be required to apply for a license. When the issuance of a certain stablecoin may affect "the monetary stability, financial stability, or the function of Hong Kong as an international financial center" or "involves significant public interest," the Financial Commission also has the authority to regulate it and require compliance with licensing obligations. The Stablecoin Ordinance imposes strict cross-border regulations on stablecoin issuance, aiming to guide overseas issuers targeting Hong Kong to apply for licenses and accept regulation, ensuring the safety of Hong Kong's financial system and the sovereignty of its currency.

Second, the diversification of pegged fiat currencies reflects Hong Kong's openness as an international financial center. As mentioned earlier, Hong Kong's designated stablecoins can reference one or more official currencies to maintain stable value, and due to the existence of the linked exchange rate system (the Hong Kong dollar to U.S. dollar exchange rate remains stable between HKD 7.75 and HKD 7.85 to USD 1), the reserve assets of designated stablecoins pegged to the Hong Kong dollar can be denominated in U.S. dollars. Correspondingly, Hong Kong stablecoins must comply with international anti-money laundering (AML) and counter-terrorist financing (CFT) standards to reduce the regulatory complexity brought about by multi-currency anchoring. The multi-currency anchoring mechanism not only reduces the devaluation risk of a single pegged fiat currency but also attracts international investors pegged to mainstream currencies such as the U.S. dollar and euro, enhancing the competitiveness of Hong Kong's stablecoin market. Compared to stablecoins pegged to a single currency or a specific sovereign asset, Hong Kong stablecoins clearly offer a richer selection and institutional guarantees.

4. Comparison with the GENIUS Act

Although the Stablecoin Ordinance provides Hong Kong with a comprehensive regulatory framework for stablecoins, the value anchoring mechanism of crypto assets is not native to it. Stablecoins like USDT and USDC, pegged to the U.S. dollar, have already gained ample practical opportunities in the global trading and settlement system. With the end of the Biden administration's high-pressure cycle on crypto assets, the GENIUS Act, led by the Trump administration, may provide an alternative policy path for global stablecoin regulation.

4.1 Core Content of the GENIUS Act

4.1.1 Scope of Application

The act clearly defines "payment stablecoins" as a type of digital asset issued through distributed ledger technology, whose core function is to serve as a payment or settlement tool, and requires issuers to commit to redeeming at a fixed currency value. Notably, national currencies, deposits (including blockchain-recorded deposits), and securities (as defined by the Investment Company Act of 1940) are explicitly excluded.

On the technical level, the act adopts a "technology-neutral" principle, allowing the issuance of stablecoins based on innovative forms such as blockchain and smart contracts, but mandating independent custody of their reserve assets and prohibiting the commingling of reserve assets with the issuer's own assets to prevent the risk of fund misappropriation.

4.1.2 Regulatory Hierarchy

The bill establishes a layered regulatory framework of "federal leadership + state-level supplementation":

At the federal level: Institutions such as the Federal Reserve and the Office of the Comptroller of the Currency (OCC) review and issue licenses to national issuers with a market capitalization exceeding $10 billion, requiring regular disclosure of reserve asset details, acceptance of stress tests, and compliance with the Bank Secrecy Act and anti-money laundering (AML) regulations.

At the state level: Small and medium-sized issuers (market capitalization ≤ $10 billion) can choose a state regulatory framework but must ensure that it is "substantially consistent" with federal standards (certified by the Treasury Department).

4.1.3 Issuer and Compliance Requirements

The bill sets strict entry thresholds for issuers and explicitly states that stablecoins must not offer interest returns:

Three categories of qualified issuers:

Subsidiaries of deposit-taking institutions (requiring Federal Reserve approval);

Federally approved non-bank entities;

State-approved entities (as mentioned above, mandatory inclusion in federal regulation after exceeding $10 billion in market capitalization).

For foreign issuers, the bill requires them to register in the U.S. and demonstrate that "the regulatory framework of their home country is substantially comparable to that of the U.S.," while also possessing the technical capability to execute "legal orders" from U.S. courts or government (such as asset freezes).

4.1.4 Reserve Asset and Transparency Requirements

The bill imposes mandatory provisions on the allocation and transparency of reserve assets:

Reserve assets must be highly liquid: Reserves must cover 100% of the circulating volume, limited to cash in U.S. dollars, government bonds maturing within 93 days, repurchase agreements backed by government bonds, and other low-risk assets, with prohibitions on re-pledging or reusing.

Disclosure and auditing: Issuers must publicly disclose the size, structure, and custody location of reserve assets monthly, subject to review by a registered accounting firm, with the CEO/CFO endorsing the accuracy of the data. Non-public companies with a circulating volume exceeding $50 billion must submit audited financial statements to ensure financial transparency.

4.1.5 Consumer Protection and Cross-Border Coordination

The bill safeguards consumer rights and prevents systemic risks through the following provisions:

Redemption and fee transparency: Issuers must clearly outline timely redemption procedures, with no delays in redeeming at face value.

Prohibition of political endorsement: It is prohibited to imply government endorsement in names or marketing, and any member of Congress or senior executive branch official is barred from issuing payment stablecoin products during their public service.

Bankruptcy priority: Claims of stablecoin holders take precedence over other creditors, with reserve assets independent of the issuer's bankruptcy estate, ensuring the safety of holders' funds.

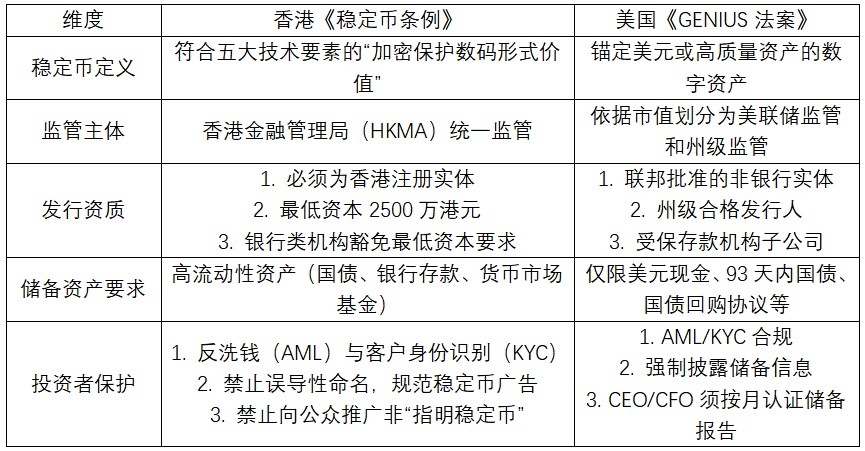

4.2 Comparison of the Stablecoin Ordinance and the GENIUS Act

Both the Stablecoin Ordinance and the GENIUS Act focus on the regulation of stablecoins linked to fiat currencies or other assets, requiring 100% asset coverage and reserve asset isolation protection, while complying with international anti-money laundering (AML) regulations to avoid criminal risks. However, there are many differences between the two in various dimensions, which are summarized in the table below:

5. Potential Impacts of the Two Major Bills

During the Biden administration, the Hong Kong SAR government worked to fill the regulatory gaps in the crypto asset sector, attracting over 200 Web3 companies to establish or expand their businesses in Hong Kong, initially forming a crypto asset ecosystem cluster. However, compared to the high-pressure regulation of crypto assets during the Biden administration, the Trump administration's open policy stance on crypto assets seeks to reconstruct U.S. leadership in this field. Although the implementation of policies remains uncertain, Trump's strong support for crypto assets further reinforces market expectations for regulatory easing, which will inevitably squeeze the space for Hong Kong's stablecoin market. In the face of the constantly changing international policy environment, Hong Kong can leverage its unique institutional arrangements granted by "one country, two systems" to actively participate in the formulation and practice of global crypto asset rules.

In terms of reserve asset management, the Stablecoin Ordinance offers a diversified path. The GENIUS Act strictly limits the types of reserve assets, requiring them to be concentrated in the highest quality liquid assets, effectively forming a strategy primarily based on U.S. Treasury securities. Due to their perfect balance of safety, yield, and liquidity, U.S. Treasuries become the inevitable choice for issuers, deeply binding the U.S. Treasury market with the cryptocurrency ecosystem. In contrast, the Stablecoin Ordinance provides global investors with a more diverse range of value storage and payment options. The diversified reserve assets position Hong Kong to establish a stablecoin system that is controllable in risk and accommodates multi-currency demands.

From a political positioning perspective, Hong Kong is backed by the vast real economy of mainland China. The long-term value of crypto assets should not be limited to financial speculation; serving the real economy and the digitization of real assets is also an important avenue. Mainland China possesses the world's most complete industrial system, providing rich application scenarios for the payment functions of stablecoins. From international logistics and supply chains to digital asset rights confirmation, there are numerous high-value assets with tokenization potential. Hong Kong can fully leverage its institutional advantages as an international financial center and its global resource allocation capabilities to create a world-leading platform for the issuance and trading of real-world asset tokenization (RWA), facilitating the efficient and compliant value transfer of high-quality assets from the mainland and globally in the Hong Kong market, thereby promoting the integration of traditional assets in the mainland with the crypto financial system and constructing a more diverse crypto asset ecosystem.

At the same time, it is essential to recognize the objective trends in the current international crypto ecosystem. On one hand, the U.S. has significant advantages in underlying fields such as public chain technology, crypto protocols, and development tools. If some startup projects and developers continue to choose the U.S. as their headquarters or R&D center, it will inevitably divert talent and capital resources from Hong Kong in the Web3 field. On the other hand, after more than a decade of evolution, the global crypto ecosystem has gradually transformed from the early "de-dollarization" to a "dollarization" pattern centered around the U.S. dollar, with the issuance, circulation, and settlement systems of mainstream stablecoins like USDT and USDC almost entirely dominated by the U.S. In this context, the exploration of Hong Kong's stablecoin system can provide the market with different institutional paths, helping to promote compliance practices for stablecoins in cross-border payments and asset tokenization.

6. Conclusion

With the implementation of Hong Kong's Stablecoin Ordinance and the U.S. GENIUS Act, the global regulatory landscape for stablecoins has officially entered an era of institutional competition. Hong Kong's regulatory framework, centered on "diversified reserves + prudent regulation," not only provides the market with alternative choices outside the U.S. dollar system but also promotes exploration in emerging directions such as RWA (real-world asset tokenization), further broadening the application possibilities of stablecoins in the real economy. In the future, as more countries introduce stablecoin regulatory bills, if Hong Kong can continue to play a pivotal role as a hub connecting the mainland and the international community, it may become a key node in the new order of global digital finance, providing international capital with richer value storage and payment options.

At the same time, the U.S. GENIUS Act establishes a multi-layered regulatory framework centered on the federal level, strengthening control over the operational risks of stablecoins through reserve asset requirements, auditing disclosure mechanisms, and issuer qualification settings, while its technology-neutral principle leaves room for future innovation. Although the regulatory paths of Hong Kong and the U.S. differ, they both reflect a common pursuit of orderly and compliant development in the stablecoin market.

In summary, the gradually clarifying stablecoin regulatory system helps to restore and amplify overall confidence in the crypto market, while the interaction between regulation and the market is driving the global crypto ecosystem into a new stage of compliant development.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。