Original Author | Stacy Muur (@stacymuur)_

Compilation | Odaily Planet Daily (@OdailyChina)

Translator | Dingdang (@XiaMiPP)

Editor's Note: @BinanceResearch released a research report on the Evolution of Token Models in June 2025, which deeply reviews the attempts and lessons learned in token design, incentive mechanisms, and market structure of Web3 projects over the past few years. From the bubble of the ICO era, the brief glory of liquidity mining, to the recent re-examination of issuance methods, governance means, and economic models by projects.

Stacy Muur has organized this report and distilled ten key observations, revealing core issues such as governance failure, low airdrop efficiency, model fragmentation, and supply distortion, while also pointing out the market's gradual return to "real demand" and "revenue support." During market downturns, these insights may provide important references for the next phase of token issuance, valuation, and mechanism innovation.

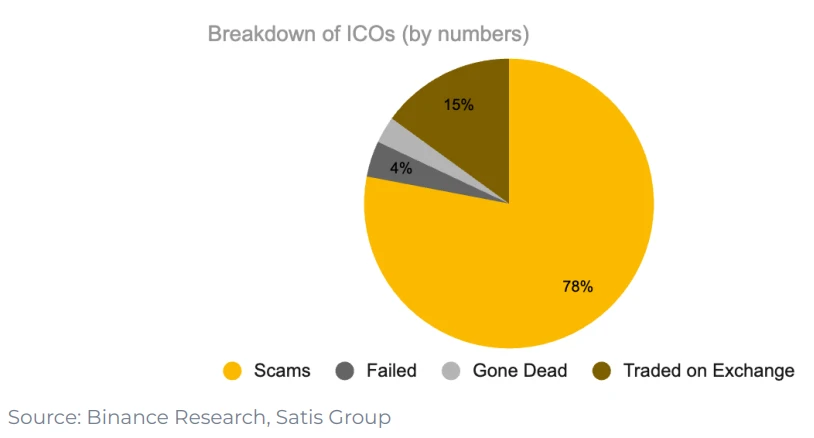

1. Only 15% of Projects from the ICO Era Successfully Launched on Exchanges

78% of projects were outright scams, while the rest either failed or gradually faded into obscurity. This indicates that the market at that time was filled with short-termism and lacked genuine sustainable construction motivation.

2. "Governance" as a Design for Token Utility Has Not Truly Worked

After the UNI airdrop, only 1% of wallets chose to increase their holdings, and 98% of wallets never participated in any governance vote.

Governance sounds good in theory, but in practice, it often amounts to another way of saying "exit liquidity."

3. Liquidity Mining Started with Synthetix in 2019 but Failed to Sustain Long-Term Demand

However, "governance rights" did not maintain ongoing attention to the projects. Data shows that 98% of airdrop recipients never participated in governance, and most sold their tokens immediately after the airdrop.

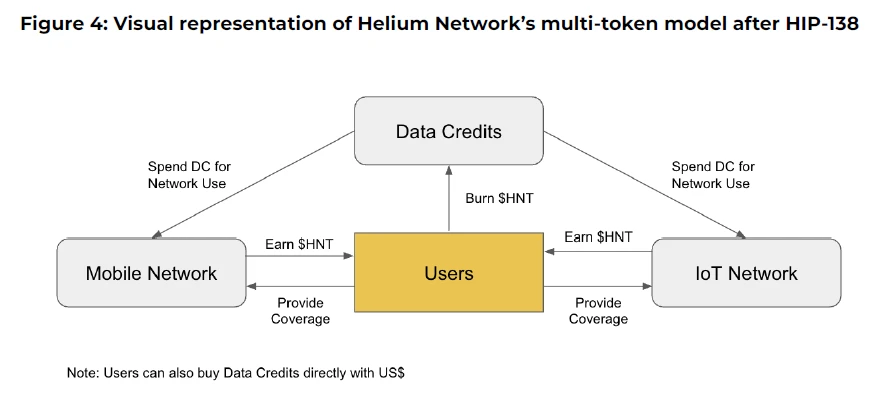

4. The Multi-Token Model Attempts of Axie Infinity and Helium Failed

Projects like Axie Infinity and Helium once adopted a multi-token model, separating "speculative value" from "functional utility." One token was used for value capture, while another was used for network usage.

In practice, this separation did not work: speculators flocked to the "utility token," misaligning incentive mechanisms and causing value to fragment. Ultimately, both projects had to revert to a simpler single-token design.

5. Private Placement Financing Reached Its Peak in 2021-2022

Total financing in 2021 reached $41.46 billion

In 2022, it was $40.12 billion

This scale has exceeded twice the total financing amount of the entire 2017-2020 cycle. However, this financing boom did not continue afterward.

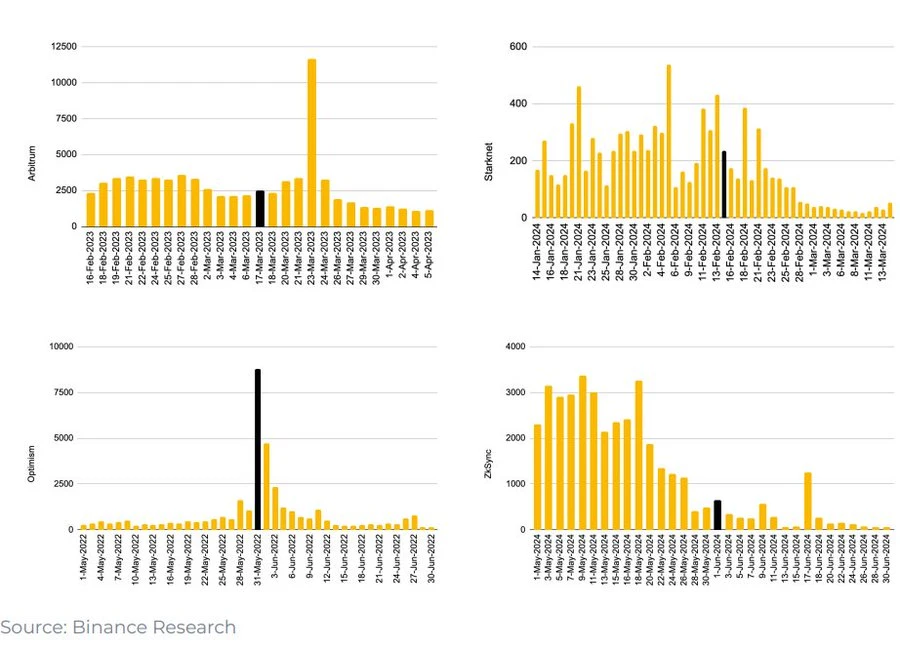

6. Cross-Chain Bridge Usage Plummeted After L2 Airdrop Snapshots

Whenever L2 announced an airdrop snapshot, the usage of cross-chain bridges quickly declined. This means that the surge in usage was not driven by real demand but rather by airdrop participants inflating transactions.

Most users sold their tokens after the airdrop, while project teams often mistakenly regarded this short-term "traffic" as genuine product-market fit.

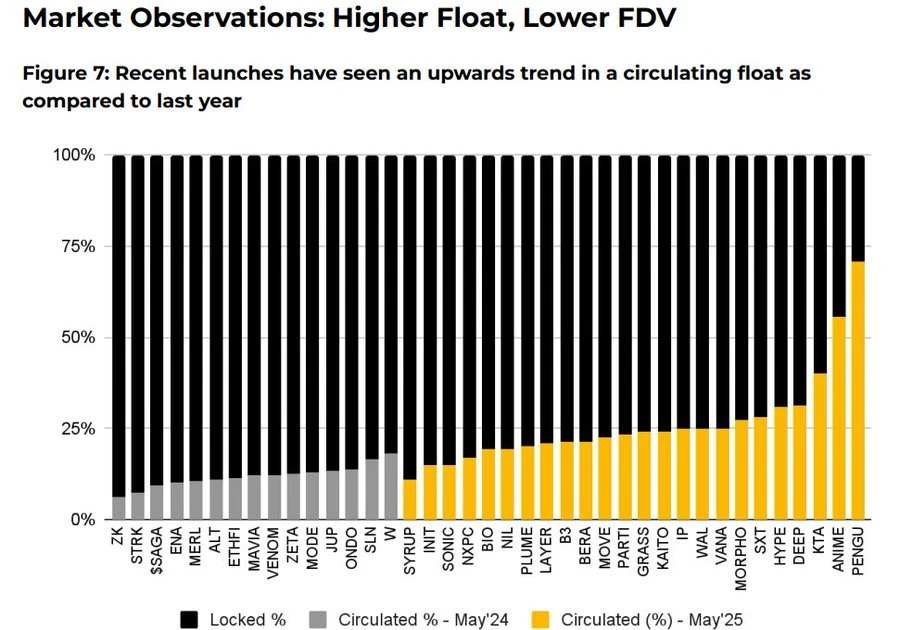

7. Token Issuance Methods Adjusted in 2025

Initial market circulation significantly increased

Average fully diluted valuation (FDV) dropped from $5.5 billion to $1.94 billion

Data shows that tokens with a higher circulation ratio and more reasonable valuations at issuance performed better after listing. The market is gradually rewarding more genuine and transparent token economic models.

8. The Return of Buyback Mechanisms

Protocols such as Aave, dYdX, Hyperliquid, and Jupiter have launched structured "redemption and destruction" plans, using protocol revenue to buy back tokens from the market and destroy them. This is both a symbol of financial health and a stopgap measure while the issue of "tokens lacking utility" remains unresolved.

9. The Truth Behind Hyperliquid's Buyback

Taking @HyperliquidX as an example, the protocol has bought back and destroyed HYPE tokens worth over $8 million, funded by 54% of its trading fee revenue. However, these buybacks did not provide dividends to token holders; they merely supported token prices by creating "scarcity."

Critics argue that this buyback represents a misallocation of capital. It creates artificial deflation rather than returning actual profits to token holders. In contrast, token models with revenue-sharing attributes may provide better incentive alignment.

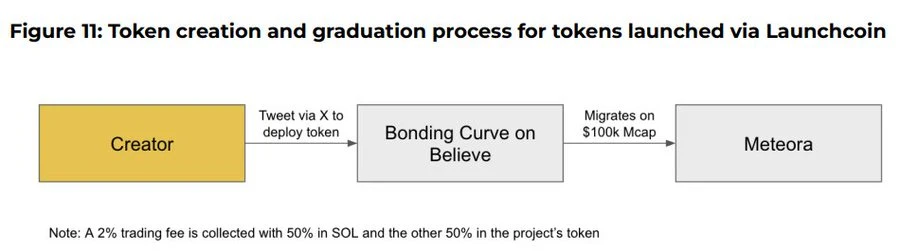

10. Believe App is an Emerging Player in the Current ICM (Instant Create Market) Narrative

This app allows users to easily create tokens on the Solana chain by posting tweets in a specific format on X (formerly Twitter), such as "$TICKER + @launchcoin," which triggers price discovery and liquidity deployment through a bonding curve model, enabling community tokens to be launched and traded without development.

Final Conclusion: Despite Continuous Evolution of Models, Token Utility Remains an Unresolved Issue

Governance mechanisms have proven to lack user stickiness

Buyback plans are, to some extent, merely a substitute for the lack of intrinsic demand for tokens

Points and airdrop mechanisms tend to lean towards short-term strategies

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。