Our updated deck for our “An Honest Conversation about the R Word” report is now live.

Since our original publication on March 22, there has been no sign that the ongoing conflict in the Persian Gulf is set to end quickly. Despite this, implied recession probabilities across assets have actually fallen over the past two weeks.

Our recession framework is simple: Fragile Conditions + Trigger = Recession.

The conditions are in place. Fiscal impulse is negative and set to worsen as most benefits from the OBBBA are front-loaded into the first half of this year. Global easing is fading, with central bank policy breadth already rolling over. Liquidity offers little margin of safety for anyone to backstop a selloff. And supply-driven inflation is rising again.

The trigger is here. Roughly 20 to 30% of crude, LPG, LNG, and refined products flow through the Strait of Hormuz. Even an immediate ceasefire would take months to normalize flows and prices.

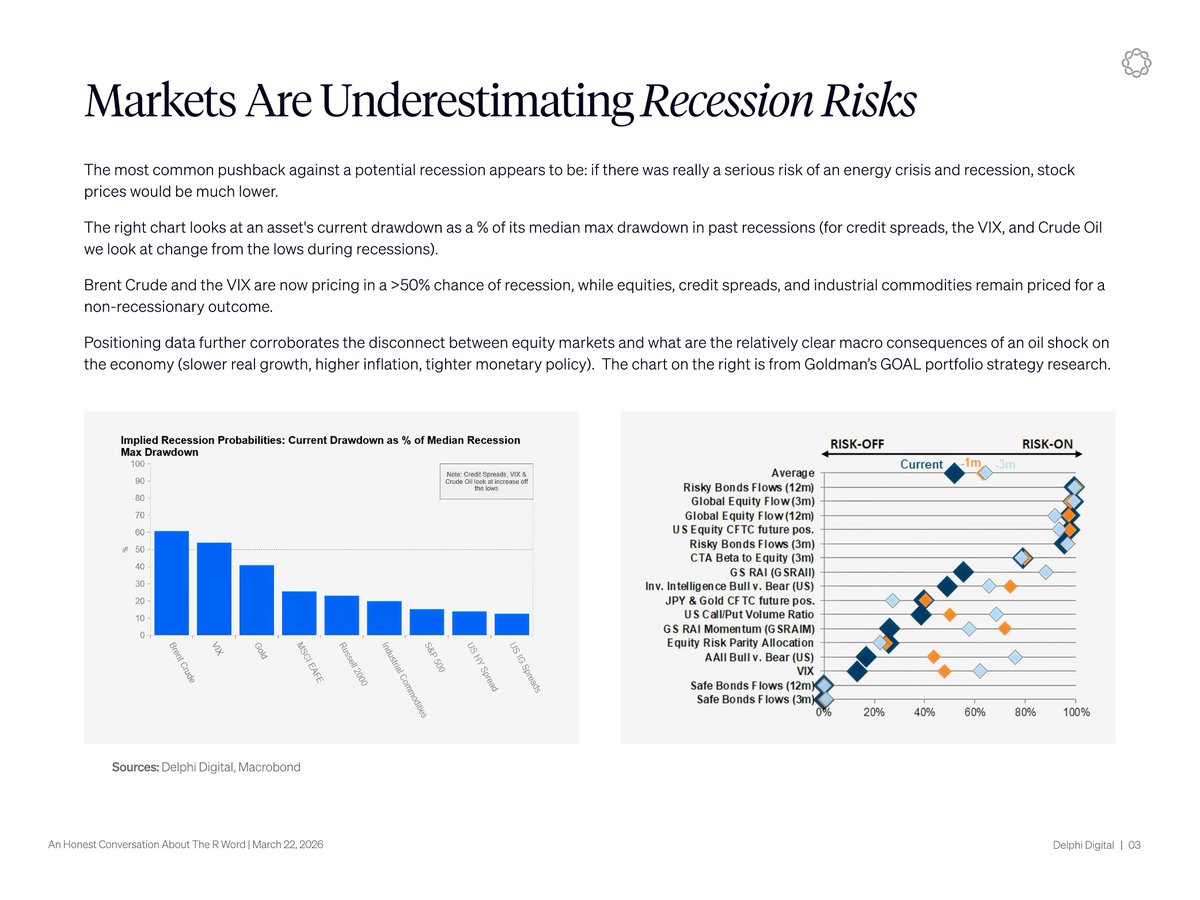

Yet recent BofA fund manager survey's had just 5% expecting a hard landing. Equity positioning has barely pulled back. Markets have a well-documented inability to price tail risks until they become the base case.

The recession probability is now at least a coin flip and rising every day. The largest hit to risk assets has always come at the beginning of recessions - the part markets refuse to price until it's too late.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。