Written by: Nunchuk

Compiled by: AididiaoJP, Foresight News

Self-custody is changing the way inheritance planning is done. A good Bitcoin inheritance plan must protect your Bitcoin while you're alive, and allow designated individuals to smoothly retrieve these assets after your passing.

Bitcoin grants individuals a rare ability: to hold wealth without relying on banks, brokers, or custodians. This is one of its greatest advantages.

But this very aspect also makes inheritance incredibly difficult.

For traditional assets, there is usually an intermediary. Banks can freeze accounts, verify documents, cooperate with courts, and transfer control. Bitcoin is completely different. The network does not recognize heirs, death certificates, or probate documents, nor does it handle customer service requests. It only recognizes keys and spend conditions.

This brings up a simple yet severe question: the characteristics that make Bitcoin difficult to steal also make it hard to inherit.

Why Bitcoin is Different

Bitcoin inheritance is essentially a "retrieval design" problem: who can access Bitcoin under what conditions, and through what safeguards.

The first challenge is the contradiction between security and accessibility. While you are alive, you need strong protections against theft, coercion, and operational errors; after you die or lose capacity, you want trusted individuals to have a clear recovery path. These two goals often conflict.

The second challenge is complexity. Many powerful Bitcoin solutions (especially multisig) are clear to their designers, but can be completely incomprehensible to spouses, children, trustees, or executors who do not frequently use Bitcoin. A solution that only a cool-headed technician can operate is likely to fail when it is genuinely needed.

The third challenge is privacy. Inheritance planning exposes sensitive information: who owns Bitcoin, how much there is approximately, and who will inherit. A poorly designed plan can expose both owners and heirs to unnecessary risks.

The fourth challenge is time. A true inheritance plan needs to be effective even years or decades later. This means evaluating a plan involves not only whether it is usable today, but also whether it can outlive devices, assumptions, or even the companies that established it.

This point is more important than many realize. An inheritance plan that relies on a company existing forever may be convenient, but is certainly not sustainable.

Six Crucial Questions to Ask

Every Bitcoin inheritance plan involves trade-offs. The simplest way to compare them is to ask six questions:

- Autonomy: Does it allow you to retain full control over the assets, or does it require reliance on some company, custodian, trustee, or legal process to operate?

- Security: While you are alive, can it effectively prevent Bitcoin from being stolen, coerced away, or lost accidentally?

- Heir Experience: Can your designated heir truly retrieve the funds without confusion or committing fatal mistakes?

- Privacy: How much sensitive information about you or your family does this plan expose?

- Flexibility: Is it easy to update the plan if beneficiaries, timelines, or family circumstances change?

- Legal Compatibility: If necessary, can it work with wills, trusts, or fiduciary systems?

No plan can excel across all dimensions, but these six questions can clarify the trade-offs.

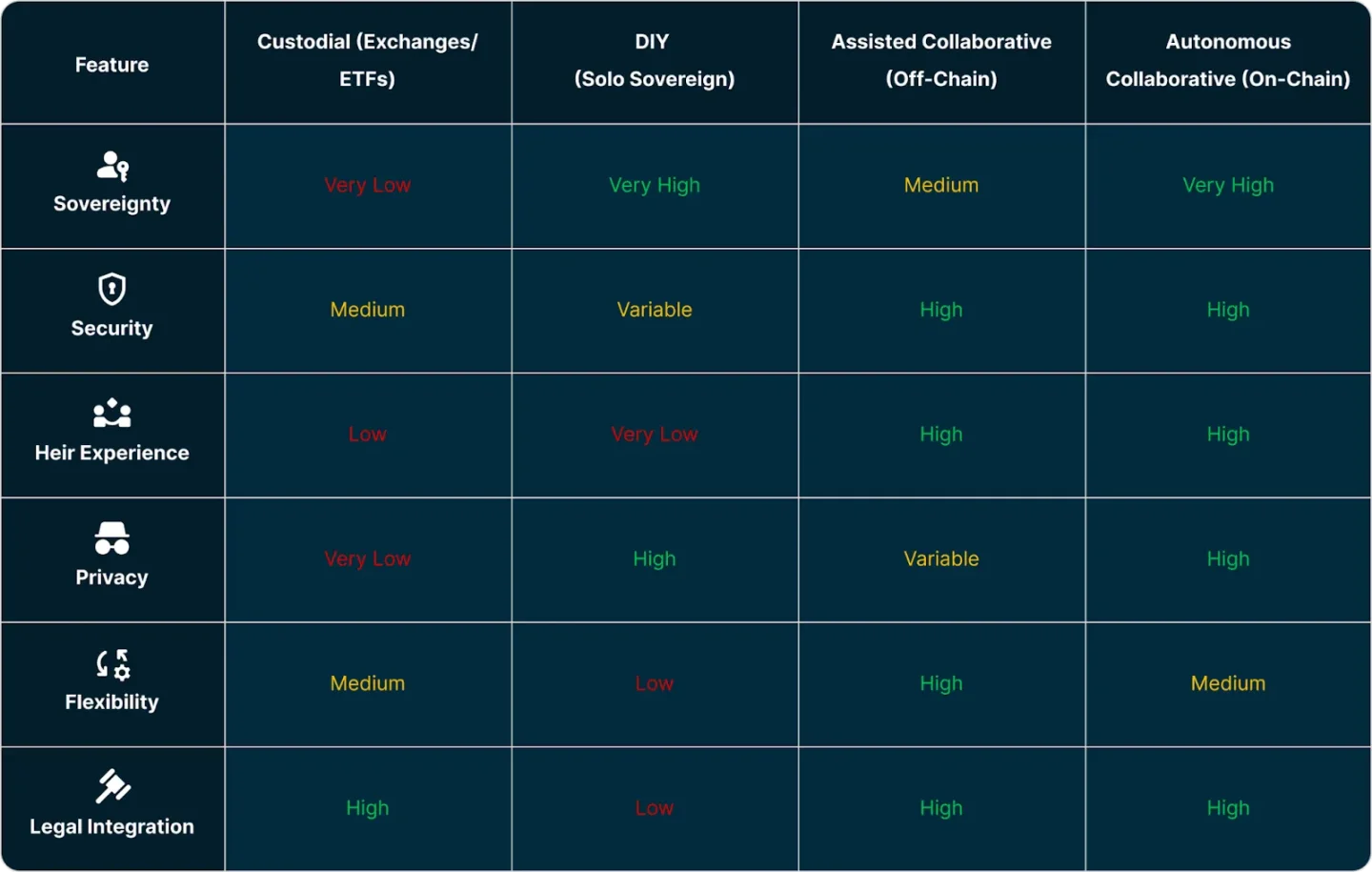

Four Common Solutions

1. Custodial Inheritance

The most traditional approach is to put Bitcoin in exchanges, ETFs, brokers, or other custodians, allowing the traditional legal system to handle transfers.

Its appeal is obvious: accounts and identities are linked, there are statements, customer service is available, and there is a relatively clear legal process for heirs.

But the cost is also clear: the institution holds the private keys. This means whether assets can be withdrawn depends on the policies, compliance processes, jurisdiction of the institution, and whether it can survive in the long term. Heirs may face the dual barriers of both the legal system and the trading platform. A large amount of sensitive client data centralized in one place also brings privacy and security risks that do not exist in self-custody scenarios.

This approach is feasible, but the way it addresses the inheritance problem effectively relinquishes the core value of self-custody of Bitcoin.

2. DIY Inheritance

DIY inheritance covers a broad spectrum. On the simplest end is single-signature transfer: directly leaving mnemonic phrases, hardware wallets, or complete recovery backups to heirs. On the complex end are multisig and time lock solutions built with open-source tools.

These two should not be confused.

From a security perspective, the weakest option is the simple single-signature transfer. For each additional backup of a mnemonic phrase, there is another target for theft, especially if one person or one location can unlock the entire wallet. If the complete recovery materials are stored in a home safe, office drawer, or bank safe deposit box without additional protection, the risks are even higher.

While adding BIP39 passphrases can improve this situation, it introduces new risks: errors in transcription are undetectable without a checksum; short passphrases can be brute-forced; long and complex passphrases may render owners or heirs unable to accurately reproduce them years later, locking themselves out of the wallet.

On the other end, a well-designed DIY multisig or time lock solution can be very reliable. Many experienced Bitcoin users choose this path for good reason. But the trade-off lies in the operational level: the responsibility for setup, maintenance, and recovery falls entirely on the owner and their heirs, with often no one to turn to for help when things go wrong.

If executed well, DIY can provide strong autonomy and security, but it also raises the bar for everyone involved.

3. Service Provider-Assisted Collaborative Custody

Another middle ground is collaborative custody. In this model, the owner still uses a multisig solution but is assisted by a service provider to complete account setup, key management, recovery operations, and inheritance processes.

Compared to pure custody or pure DIY, this is indeed an improvement. The owner retains more control, while heirs can seek assistance when needed.

Most of these services manage inheritance logic off-chain: waiting periods, survivorship verification, beneficiary arrangements, and recovery processes are coordinated through the service provider's system rather than directly written into the Bitcoin on-chain spending conditions.

There are clear benefits to this approach. Off-chain inheritance is easier to update. If the owner wishes to change beneficiaries, adjust waiting periods, or set up more complex phased distribution plans, off-chain operations are generally much easier than entirely on-chain solutions.

The trade-off is the reliability of the recovery path. Whether inheritance can be realized still depends on whether the service provider exists and is willing to cooperate when the heir makes a request.

For many families, this remains a good option, especially when guided recovery and operational flexibility are comparatively significant.

4. On-Chain Collaborative Inheritance

A newer model adds on-chain backup solutions based on collaborative support.

Owners still gain the security of multisig and guidance from service providers, but the recovery path for inheritance is also written into the on-chain spending rules of Bitcoin. For example, using time locks to set a deadline, after which the spend conditions automatically change, allowing heirs to retrieve Bitcoin independently even if the service provider cannot provide assistance.

This represents a significant change in risk control: the recovery path is anchored in the rules of Bitcoin rather than relying solely on the continual cooperation of a service provider.

This model also has its costs. Due to parts of the plan being enforced on-chain, adjustments may not be as convenient. Changing inheritance times or plan structures may require transferring funds and incurring network fees.

But for holders who want collaborative support while also wishing for a reliable long-term backup, on-chain inheritance is an important advance.

Where the Real Trade-offs Lie

When comparing modern inheritance solutions, the most meaningful question isn’t "which is best," but rather "what do you most want to optimize."

Off-chain collaborative solutions typically excel in flexibility: they are easy to update, can adapt to changes in family circumstances, and can be adjusted over time.

On-chain collaborative solutions typically outperform in durability: the design goal of backup paths is to remain functional even when service providers fail, which is crucial for inheritance plans that need to stay effective for decades.

Many families have valid reasons for choosing either. The key is what matters most to you.

If you view Bitcoin as generational wealth, then durability should be a core consideration.

Smooth Path + Last Line of Defense

Most Bitcoin inheritance plans tend to lean towards two extremes.

On one end, convenience often sacrifices autonomy: easy to understand but heavily reliant on institutions, identity verification, or cooperation from service providers.

On the other end, autonomy sacrifices usability: reducing trust in third parties but shifting the burden of complex technical operations to heirs at their most vulnerable moments.

The most robust solutions balance both paths.

The first path is a smooth path: when the service provider is available and all is normal, heirs retrieve assets through a guided process that is smooth, low-pressure, and prone to fewer errors.

The second path is the last line of defense: a recovery path enforced by the Bitcoin network, allowing the plan to execute even if the service provider disappears.

This combination is crucial because it aligns with real inheritance scenarios: most people want their families to get help instead of facing complex technical operations alone; at the same time, few are willing to entrust their estate to a company that "must exist forever."

Estate Planning Remains Important

There is a common misconception that Bitcoin inheritance is either entirely disconnected from the traditional system or fully integrated into the traditional financial system.

In reality, many families need a hybrid model.

Some holders wish to pass Bitcoin directly and privately to their family. Some want trustees involved, for reasons like phased distribution, protecting minor children, or interfacing with existing trusts. Others want legal documents to clarify intent while allowing the actual recovery path to avoid public probate records.

A good Bitcoin inheritance plan should support these different options.

Thus, it is helpful to think about the two questions separately: Who should receive this asset? Who can actually retrieve this asset?

Wills or trusts can clarify intent, define beneficiaries, and set legal obligations, but they do not themselves solve the issue of "how to recover." Conversely, a purely technical recovery solution cannot escape the demands of taxation, reporting, and estate law.

The most comprehensive plan considers both aspects clearly.

Common Mistakes

Many inheritance plans fail for very ordinary reasons.

One mistake is to assume that spouses, children, or executors will "figure it out themselves." Having a hardware wallet does not equate to understanding the recovery process.

Another mistake is concentrating too much power in a single point: one document, one device, or one envelope can fully unlock the funds. This indeed makes inheritance easier, but it also makes theft easier.

Another mistake is overestimating the security of a "passphrase" without considering the human factors in recovery. Passphrases can enhance the security of single-signature solutions, but only if every step of creation, storage, and communication is conducted with real operational discipline.

Finally, many people make a plan and then never revisit it. Beneficiaries may change, devices may fail, family relationships may shift. A Bitcoin inheritance plan is not a static item but rather a system that requires regular review.

A Simple Action Checklist

Inheritance plans can start simply, as long as each step is conscious and reviewed regularly.

- Step 1: Determine who should inherit your Bitcoin and if these people are capable of directly handling self-custody. Some can directly receive Bitcoin, while others may need a trustee, phased transfers, or guided assistance.

- Step 2: Choose a suitable security model based on the size of the assets and the heirs' situation. The larger the amount, the more important the significance of multisig and formal inheritance design.

- Step 3: Keep secrets and instructions stored separately. Private keys, hardware devices, and "user manuals" (explaining how to recover) should preferably not be kept together or given to the same person.

- Step 4: Clarify what matters most to you. Some families are better suited for flexible off-chain coordination, while others require on-chain backups that can outlast the lifespan of service providers.

- Step 5: Test the plan. Don’t use all the assets, but ensure there are enough to verify whether the recovery path is genuinely usable. A plan that has never been rehearsed is just a theory.

- Step 6: Review your plan after significant life events and regularly. Marriages, divorces, births, deaths, relocations, or changes in service providers can affect the original plan's reasonableness.

The Ultimate Test of Self-Custody

People easily tend to treat inheritance as something to be addressed "later." However, it is the ultimate test of whether a custody plan is genuinely robust.

Custodial solutions provide familiarity, but the cost is a reintroduction of dependency on institutions. DIY solutions can excel under technically sound conditions, but they demand higher standards from owners and heirs. Off-chain collaborative inheritance enhances usability and flexibility. On-chain collaborative inheritance adds a robust long-term backup.

The most significant advancement in this field in recent years has been the design of inheritance that combines guided recovery and autonomous on-chain backups.

For those who wish for Bitcoin to become generational wealth, this directional shift is meaningful. The goal is no longer just to "leave instructions," but to "leave a recoverable path that can be safe, private, and operational for the long term."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。