Author: Oluwapelumi Adejumo

Translated by: Deep Tide TechFlow

Deep Tide Guide: While trading volume has not collapsed, the number of active addresses has been continuously shrinking for six months, dropping to a five-year low. This divergence of "surface prosperity and internal hollowness" is a negative signal for the structural health of the bull market.

The article cross-verifies data from Glassnode, Santiment, and CryptoQuant, presenting three potential future scenarios that serve as a reference framework for assessing BTC trends.

The full text is as follows:

Bitcoin's network activity has weakened for six consecutive months, but this trend is not reflected in core metrics that many traders immediately focus on.

The clearer signal is not the trading volume—trading volume has remained relatively stable—but the breadth of participation. Even if the network continues to process a similar number of transactions, the number of active addresses on the chain has been steadily declining.

In a market where price discovery increasingly occurs in ETFs and derivatives, this split is critical. It signifies that Bitcoin's on-chain footprint is narrowing while market exposure continues to be active elsewhere.

As the bear market persists, this trend has become increasingly difficult to ignore.

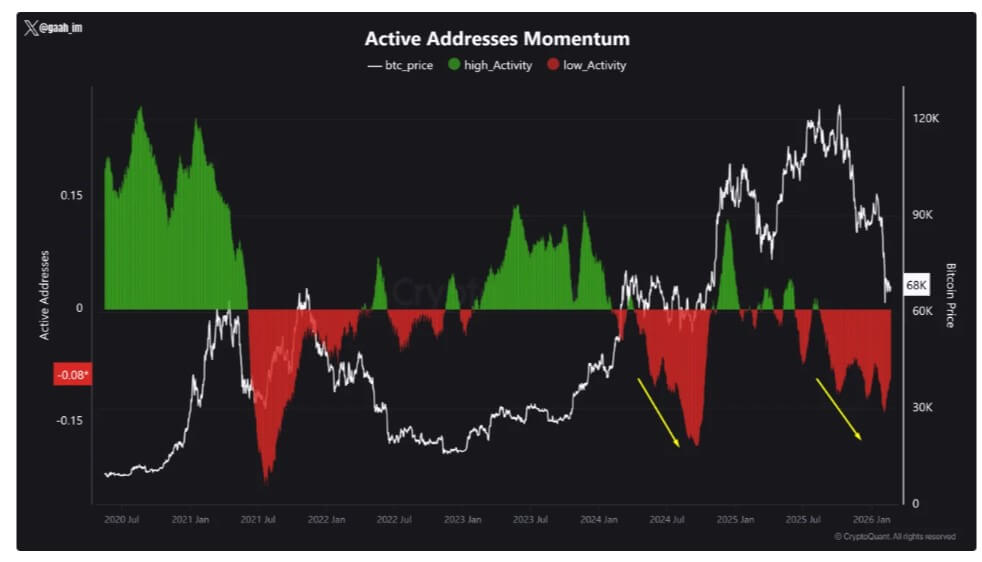

Glassnode data shows that in mid-August 2025, the eight-day average of Bitcoin active addresses was approximately 778,680. As of February 23, this number has dropped to about 535,942, a decrease of approximately 31%.

CryptoQuant has also indicated low network activity for six consecutive months, describing the current phase as a period of continued weakness in on-chain participation.

Bitcoin Active Addresses Momentum

Source: CryptoQuant

The last time the market exhibited a similar pattern was in 2024—subsequently, Bitcoin experienced an approximate 30% correction.

This does not guarantee a repeat of the same now, but it reinforces a historical pattern: prolonged network weakness often coincides with periods of waning market confidence.

Breadth Declines, But Throughput Has Not Collapsed

The number of Bitcoin transactions has not declined in tandem with the number of active addresses.

In mid-August 2025, the average daily number of transactions was approximately 444,000. Data from Blockchain.com shows that in the last 30 days, the daily average was about 439,000.

Data on a daily basis still shows fluctuations, ranging from about 289,000 to 702,000, but the overall throughput trend has not collapsed.

This divergence is key to understanding the current situation.

If trading volume remains stable while active addresses are decreasing, it indicates that fewer entities are engaging in the same amount of on-chain activity.

Multiple factors can lead to this situation, all without the need for retail influx. Exchanges and custodians can handle withdrawals in bulk; whales can consolidate transfers; institutional fund flows can be managed through fewer wallets; operational activities can also cause temporary spikes in transactions without signifying a true return of users.

The result is that while the on-chain activity appears busy, the underlying participants are decreasing.

This is why the decline in breadth is more indicative than the raw throughput. Stable transaction counts may mask a market increasingly concentrated on repeat traders, large institutions, and operational fund flows.

In this pattern, Bitcoin's chain continues to operate normally, but the breadth of user participation it represents has become less authentic.

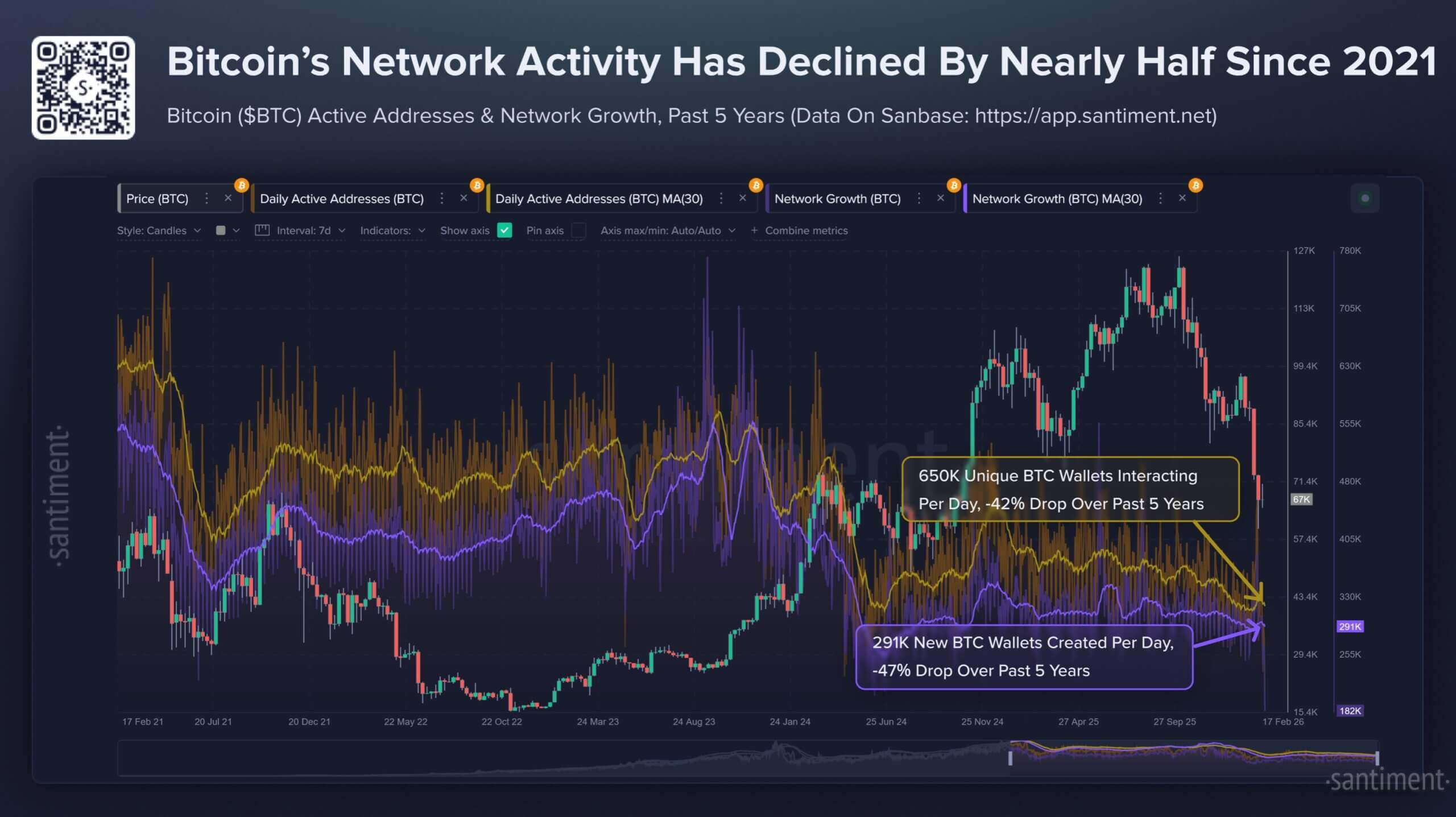

Blockchain analytics firm Santiment provides a more straightforward description from a longer time perspective.

The firm indicates that since February 2021, the number of unique addresses initiating Bitcoin transactions has decreased by 42%, and the number of newly created addresses has decreased by 47%.

Santiment has not categorized this as evidence of crypto being dead or a long-term bear market being locked in, but it does illustrate a bearish divergence throughout 2025—market capitalization is rising while Bitcoin's utility metrics are declining.

This tension is now reflected in a six-month trend. Prices and market narratives can continue to sustain, but the chain itself is becoming increasingly quiet.

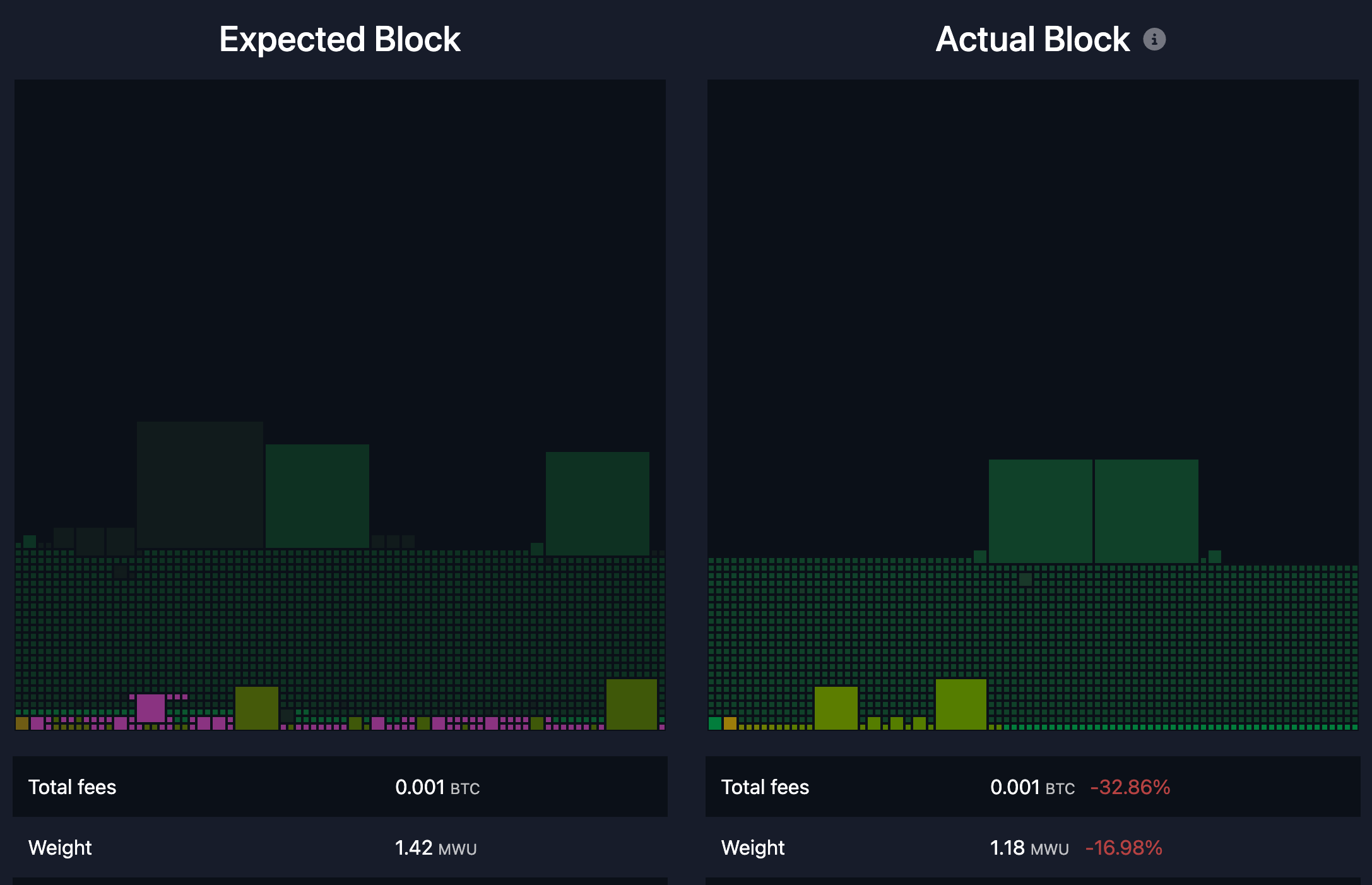

Low Fees Indicate Shrinking Demand for Block Space

Fee data further corroborates that Bitcoin Layer 1 is in a state of weak demand.

Data from mempool.space shows that the recent average transaction fee on the network is about $0.24, approximately 1.8 sats/vB.

This is a low level for a network that previously experienced sustained block space competition during peak cycles. At the current transaction pace, this fee level implies that the network's daily fee income is less than $100,000.

In contrast, block subsidies remain about 450 BTC per day, with fees contributing a very small proportion.

This is not an immediate security issue, nor does it imply that Bitcoin's security model is facing recent pressure.

This is because block subsidies are still dominant in miners' revenue. However, it does point to a long-term reality that Bitcoin has yet to confront in this phase of the current cycle.

The topic of transitioning to a fee-supported security budget resurfaces every cycle, but in the current environment, this transition is yet to be tested—because the demand for fees is inherently weak.

From a practical standpoint, the current quiet fee market allows this discussion to continue to be postponed.

The chain does not face ongoing congestion pressure, and users are not fiercely bidding to get on-chain. Such conditions can change rapidly during volatile events, speculative waves, or new demand shocks, but nothing of that sort has happened yet.

Currently, block space is in a visibly low usage state compared to past bull market phases, in alignment with the broader backdrop of declining participation breadth.

Bitcoin's Empty Mempool

CryptoQuant's assessment also aligns with this fee environment—low network activity is typically associated with a decline in market interest in assets, as well as periods of widespread losses.

As interest wanes, new participants decrease, and self-initiated transfers diminish, fee pressure subsides.

As a financial asset, Bitcoin can still be actively traded, but the chain itself no longer reflects widespread user participation.

The Macroeconomic Environment and ETF Fund Flows Are Changing How Bitcoin Is Traded

The macro context helps explain why this trend persists.

Bitcoin is increasingly resembling a high-beta asset sensitive to macro factors, especially during risk-averse periods.

Over the past year, U.S. inflation has cooled, with the CPI year-on-year growth rate in January 2026 being 2.4%; the Federal Reserve's target interest rate range was cited as 3.50% to 3.75% at the end of January.

In a simpler market environment, cooling inflation may support a clearer rebound in risk assets.

However, market attention is focused on multiple volatility catalysts—including uncertainty around tariff policies. This factor has driven severe fluctuations in interest rates and the dollar, keeping overall risk appetite unstable.

In this environment, both retail and institutional investors tend to reduce their operating frequency. Retail participation declines, and turnover among traders decreases. Institutions can maintain exposure but prefer to adjust positions through products that do not require moving assets on-chain.

This is precisely why spot Bitcoin ETFs have become a key narrative player.

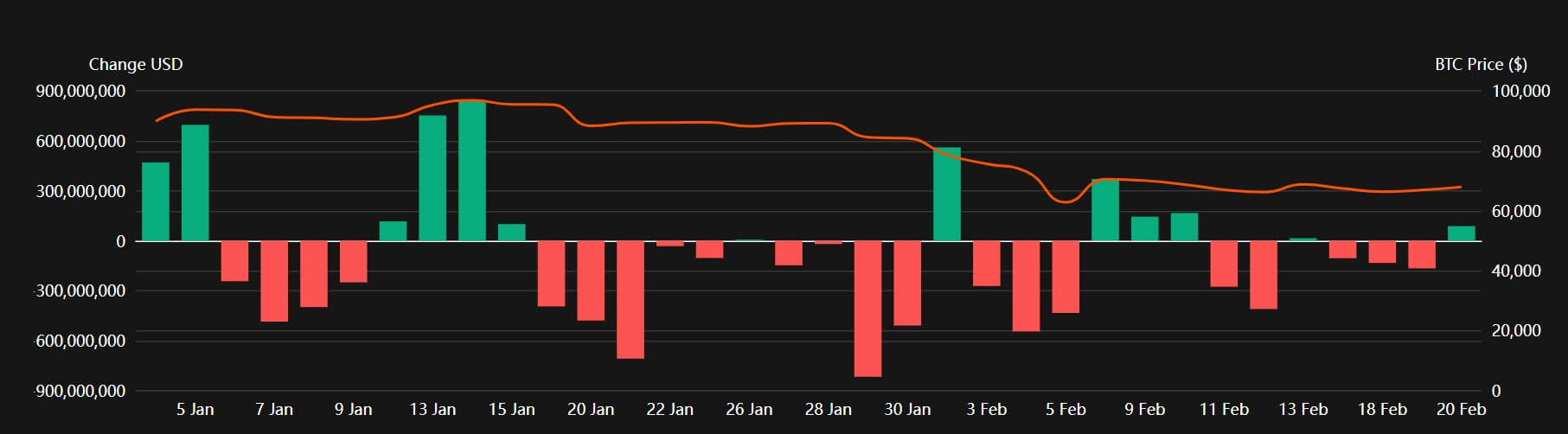

Coinperps data shows that U.S. Bitcoin ETFs have seen net outflows for multiple weeks, with a cumulative outflow of approximately $3.8 billion over the past five weeks, and an outflow of about $4.5 billion year-to-date.

Daily Fund Flows for U.S. Bitcoin ETFs in 2026

Source: Coinperps

This shift has transferred activity from self-custody wallets to brokerage accounts.

This also explains why the market can remain active while the chain becomes increasingly quiet. Exposure continues to change hands, but more turnover is occurring off-chain.

This represents a significant shift in Bitcoin's role. It is increasingly resembling a financial product encased in institutions, while Layer 1 is used more selectively for settlement, storage, and periodic transfers.

Meanwhile, the daily trading energy in the crypto space is increasingly flowing elsewhere, particularly to stablecoins.

Coin Metrics lists stablecoins as a core driver of on-chain activity, with the total supply of stablecoins now approaching $300 billion and transaction volume continually rising.

If stablecoins on other chains absorb more daily settlement demand, Bitcoin's Layer 1 will naturally become functionally more singular.

This in itself does not weaken Bitcoin's investment logic but does alter its form.

Three Scenarios for the Next Three to Six Months

The current six-month decline in network breadth outlines three potential paths for Bitcoin's future trajectory.

The first is a continuation of indifference, which in a risk-averse market environment appears to be the baseline scenario.

In this scenario, active addresses remain low (between 450,000 and 600,000), transaction counts oscillate but do not collapse, fees remain low, and ETF fund flows continue to be steady or slightly negative.

Here, Bitcoin may still be volatile due to macro headlines, but on-chain participation does not confirm a broad recovery. The trading logic of the asset resembles a macro tool rather than a network entering a new expansion phase.

The second is liquidity thawing, which is the more optimistic path.

If inflation continues to cool and expectations of easing stabilize risk appetite, ETF fund flows may shift from net outflows to sustained net inflows. In this environment, growth in active addresses will be a key confirmation signal.

Rebounding to 650,000 to 800,000 active addresses would indicate that participation breadth is recovering, not just the return of price momentum. This looks more like a classic cyclical recovery—where rising prices are supported by growing on-chain user participation.

The third is a structural alternative scenario, which may be the most noteworthy.

In this scenario, Bitcoin prices rise, but on-chain breadth remains subdued. ETFs, derivatives, and custodial settlements continue to dominate, while stablecoins absorb more trading demand in other areas of the crypto space.

Here, Bitcoin increasingly resembles a digital macro asset and settlement layer, rather than a chain with broad daily retail activity.

This scenario would mark an evolution in Bitcoin's role, reflecting deep changes that have occurred compared to years past.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。

{kind=link}

{kind=link}

{kind=link}