Author: Jesse Walden, Founder of Variant

Translator: Yuliya, PANews

Editor's Note: Jesse Walden, founder of Variant Fund, presents a forward-looking perspective in the article that "everything is a market," arguing that cryptocurrency extends the boundaries of finance into the cultural realm, becoming a horizontal infrastructure layer. The article explores how finance is evolving into a ubiquitous infrastructure based on three core driving forces: public participation, permissionless innovation, and market programmability, while depicting a future of financial invisibility in combination with cryptographic technology and artificial intelligence.

The full text is as follows:

There has been much debate about whether cryptocurrency is purely for finance or has a grander significance. My perspective is: yes, cryptocurrency is for finance. But the key is that the connotation of finance is becoming much broader than people commonly understand.

Three fundamental driving forces underpin this transformation:

Public Participation: As the barriers to market entry lower, finance is increasingly interwoven with culture and deeply influenced by it.

Permissionless Market: This force acts as a driver of change, allowing global users to exhibit new behavioral patterns and in the process, pushing regulators and traditional institutions forward.

Programmable Endpoints: Financial markets are evolving from discrete venues to APIs. They embed economic data and can generate real-time information that is extraordinarily costly to fabricate, which can be seamlessly utilized by AI Agents.

Public participation is changing who uses the market; permissionless innovation is altering which markets can exist; while the programmability of new markets opens up new design spaces for how we (and AI agents) use the market.

In summary, as the value in the world gradually becomes software-dominated, finance is undergoing a radical transformation that requires us to hold a more expansive view of its final outcome.

Towards a Billion Traders

In 2020, Variant proposed the vision of an "Ownership Economy" at its inception, aiming to enable a billion users to be owners: owning their identities, funds, data, and the products and services they use daily. Today, user ownership has been realized in several important but vertical software domains, primarily focusing on financial attributes: such as store of value assets (BTC/ETH), decentralized blockchain and financial markets (Solana, Uniswap, Morpho, Hyperliquid) - we are fortunate to be investors in these projects.

In hindsight, the argument of 2020 was correct; people want to gain economic upside from things they understand and care about. However, I originally thought this would expand to all products used by consumers daily, like employee stock options; the reality is that the opportunity has transformed into "stakeholder" investments in anything you believe in.

Today, "trading" has become a broader, non-physical way for users to participate in economic upsides (and downsides). It turns out that the feedback from trading is more direct and expressive than owning a digital identity, money, data, or platforms.

Trading is often a gateway to participating in broader markets. Many of the talented people I have encountered in the crypto space follow a similar growth trajectory:

Getting a lesson from a volatile altcoin;

Learning to manage risk like a trader;

Eventually becoming a more mature long-term investor.

Even failed experiences are meaningful: a gambler who loses everything but decides to only bet on things they understand becomes a trader; a trader who finds faith and extends their timeline becomes an investor.

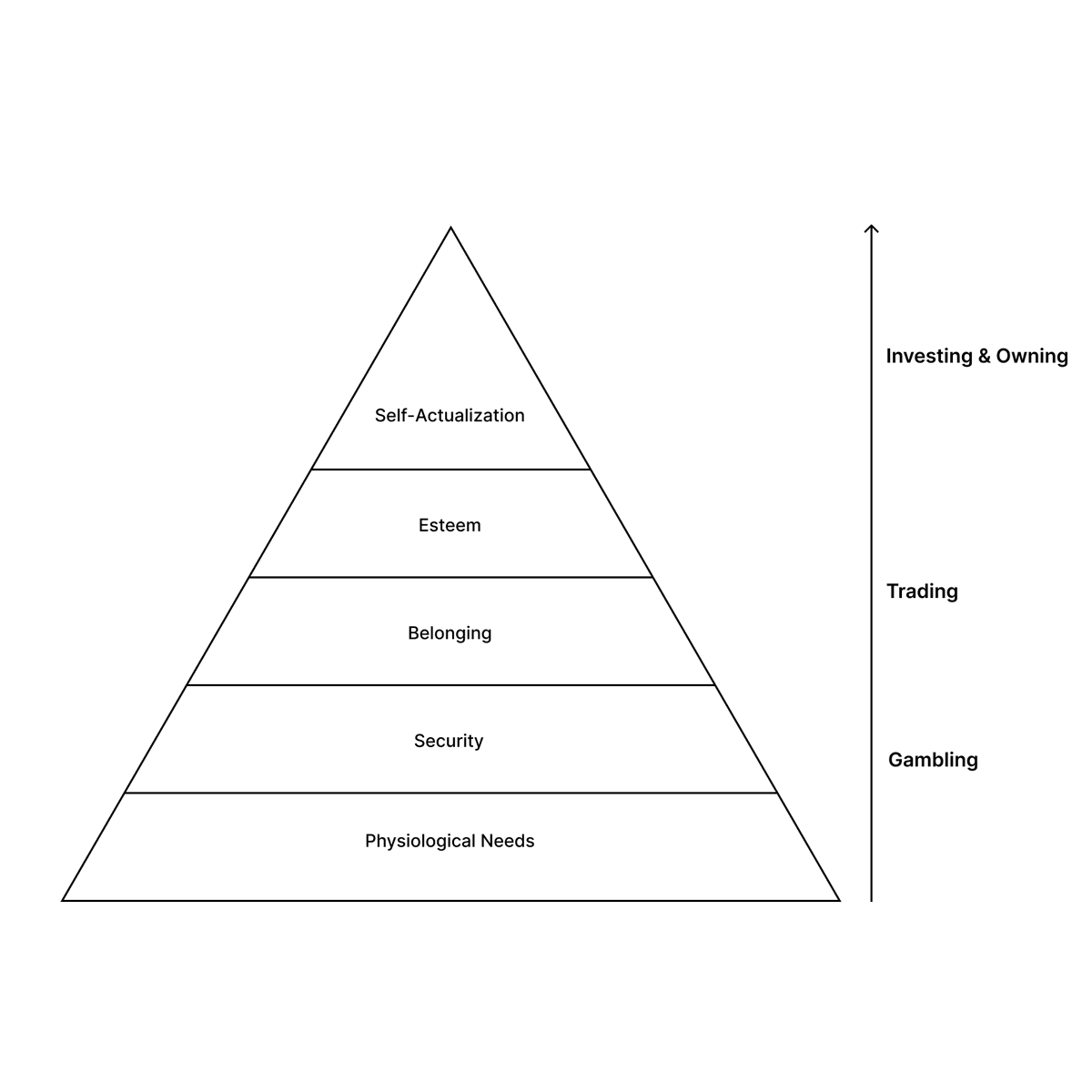

We can view this continuum of risk-taking through Maslow's Hierarchy of Needs:

Gambling and trading satisfy lower-level needs: security (escaping economic hardship through a big win), or belonging (like WallStreetBets trying to take on Citadel, or betting on a team with friends).

Investing is closer to top-level self-actualization and sense of purpose. Owning a house is the American dream, investing in a company expresses belief in its future. But if your attention is still on the lower-level needs, it is difficult to realize this belief.

PANews Note: WallStreetBets (abbreviated WSB) is a famous subreddit on Reddit, known for high-risk, aggressive investing and meme stock trading. It is known for encouraging the use of leveraged options trading and pursuing short-term profits, and made headlines in 2021 for orchestrating the GameStop (GME) short squeeze. Citadel is a top hedge fund and financial services company, known for rigorous risk control and high returns, and is one of the most influential financial giants on Wall Street.

Due to short timeframes and high volatility, trading can meet more urgent needs for many people. Furthermore, because permissionless markets can target almost anything—from derivatives to memes to political outcomes—people's avenues for gaining economic returns have never been so broad.

In many of these markets, life experience can (at least temporarily) become an advantage. A kid who understands TikTok trends knows memes better than Citadel; a player living in a virtual economy understands the game better than gaming analysts.

The old adage "invest in what you understand" has become increasingly feasible today. As a result, market participation is no longer a specialized profession but has transformed into a cultural phenomenon of public involvement, with its own status games, memes, heroes, villains, subcultures, and languages. Due to this newfound expressiveness and accessibility, financial markets are increasingly interwoven with culture. And culture—from trend dynamics to political events—is also increasingly expressed through markets.

(Image: Balenciaga S2023 fashion show at the New York Stock Exchange)

We are witnessing exponential expansion of global economic access through stablecoins; on the other end of the spectrum, financial risk-taking through trading and markets is also expanding, moving towards a billion active traders scale.

Markets as Drivers of Change

In the 1960s, the average holding period for stocks was over 8 years. By 2020, this average had dropped to less than a year. This is the world we live in today: a market of public participation, where trading has become the main artery for people trying to obtain economic upside.

This world has not completely emerged within the boundaries of the traditional financial system. New markets have largely been built externally, often intentionally and out of necessity. Using new technologies and free markets to push regulators and institutions is one of the most reliable models for traditional systems to adapt and evolve.

As I wrote in my initial paper:

“The history of protocol adoption follows a pattern: first, early adopters use new protocols to do things that were impossible before the advent of new technologies. These new behaviors often involve breaking the rules. Then, the winning strategy for founders is to build products that allow these new models to be accepted by a broader audience.”

A classic example is BitTorrent, invented in 2003. It enabled streaming, and at its peak, piracy via that protocol accounted for one-third of total internet traffic. Later, Spotify productized streaming by reaching compliance agreements (which in fact initially also used BitTorrent technology at the base level).

Cryptocurrency is reshaping value in a permissionless way, just like BitTorrent reshaped information.

Prediction Markets: Polymarket operated on an offshore crypto track for years when prediction markets were banned in the U.S. Now, thanks to new regulatory clarity, they have mobile apps in the U.S. (albeit not on-chain).

Stablecoins: Once living in the regulatory gray area and initially directing liquidity in offshore exchanges. Last year, the GENIUS act brought them into the system.

ICOs and Fundraising: In 2017, ICOs accomplished permissionless crowdfunding when early venture capital was constrained. The hostile SEC subsequently cracked down, but this exacerbated a problem: the technology innovations and growth returns were being captured by the private sector, with fewer opportunities for public participation in the upside growth. However, this year, Congress is formulating market structure legislation in the CLARITY act that explicitly allows founders to broadly raise funds and share ownership through public token sales.

Permissionless markets continuously attempt to "break the rules," enabling people to gain economic returns from private companies (don’t you want to own a part of Claude or ChatGPT?). Recently, Robinhood attempted to launch tokenized exposure to private companies like OpenAI and SpaceX in Europe on the crypto track and has applied to the SEC to introduce private market funds to retail investors in the U.S. Startups are trying to provide synthetic exposure to private companies through novel products.

This could be a pathway back to the original "Ownership Economy" argument, where users can indeed gain economic exposure to the products and services they use daily. But as we see in other markets, forcing regulatory change takes time and often relies on scalable and validated market demand.

More directly, I expect to see many brand new net-add markets take off, which raises a question: what does the complete design space of these new markets look like? How do they differ from previous markets? And who, or what, is trading and consuming them?

Markets as APIs

What distinguishes this moment from previous waves of financial innovation is that two forms are expanding in software simultaneously:

Cryptocurrency (Crypto): Provides the most powerful track for new markets—permissionless creation, programmable settlements, composable liquidity, and global access, with costs rapidly approaching zero. Now, we can tokenize and trade things that previously lacked liquidity, were inaccessible, or simply did not exist.

Artificial Intelligence (AI): Makes it possible to build, model, and automate things that were previously unmanageable.

Crypto+AI has established a composite design space: every price generated by the market is an input for AI to act upon, while every new thing AI can model becomes an object for the market to price.

It can be said that intelligence is the ability to predict or make informed decisions. Markets and cryptocurrencies provide the best "prediction" mechanisms known to us. AI can leverage these prices to understand and simulate the future and make decisions.

This design space is precisely why the market is evolving from "output" to "infrastructure." Over the past decade, cryptocurrency has established the underlying infrastructure that has allowed new markets to surge. In the coming decade, markets will increasingly become the infrastructure itself; becoming endpoints consumed as inputs by applications and agents.

(Image: Central Food Wholesale Market in Mexico City)

Traditional APIs return stored data. As APIs, markets generate real-time data through competitive interactions among participants willing to take capital risks for their beliefs. This makes markets more expressive than regular APIs; they not only provide information but also generate it. Moreover, because the cost of producing information generated by markets is high, it is also more difficult to fabricate.

On-chain markets even surpass traditional APIs, as they are by default permissionless and composable (anyone can call them), global, and use standardized interfaces.

Integrating markets directly into products has already begun in the financial sector; this is called "DeFi Mullet": fintech products with familiar front-end experiences built on DeFi back-end tracks, such as the Morpho Vault. Coinbase's lending and earning products offer users dynamic interest rates, which users can pay or earn by querying Morpho's on-chain lending market. Users can enjoy these functions without needing to understand the underlying dynamics of the lending market.

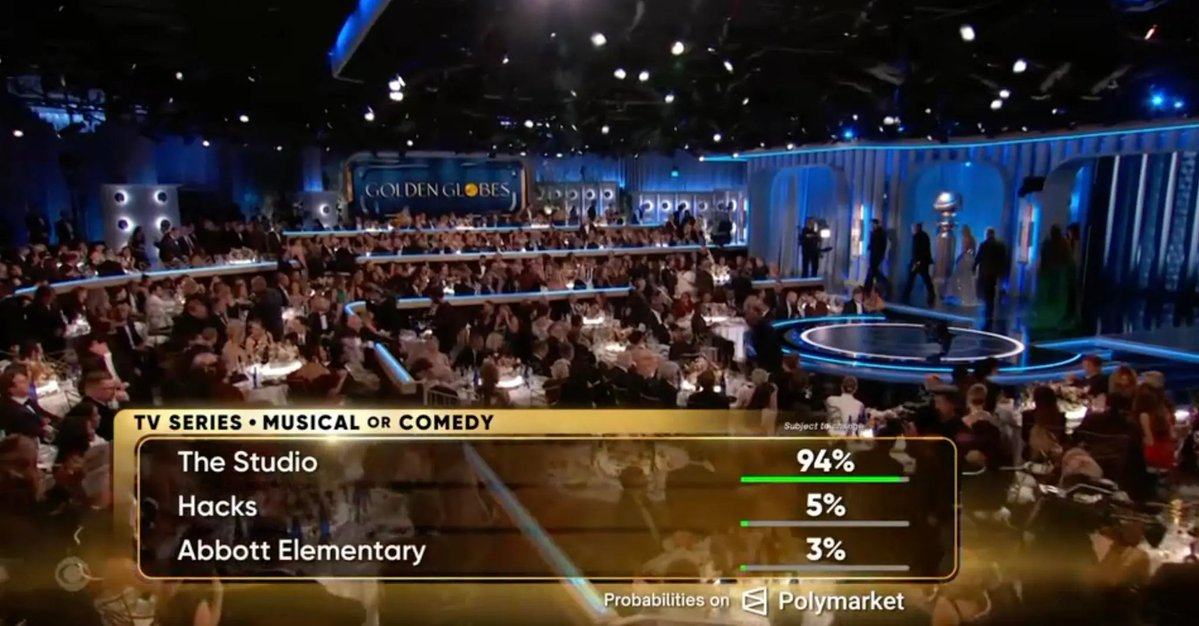

Beyond financial services, Polymarket's odds for the Golden Globe Awards are a recent intuitive example of this phenomenon. APIs provide real-time prices that are integrated into entertainment products (the market accurately predicted 26 out of 27 winners).

As we tokenize more value in the world and bring new markets on-chain, this model will expand beyond fintech packaging or live event odds. Although not currently on-chain, Apple's "Clean Energy Charging" is a telling mainstream example. In the U.S., when you plug in a phone charger, Apple uses real-time predictions of the grid's carbon intensity to schedule charging times for maximum energy and cost efficiency. You never see the underlying energy market, but Apple's products are calling endpoints for market data and using its signals as inputs for decision-making, thus optimizing the product.

MetaDAO, a crowdfunding platform driven by prediction markets, takes this idea further. When facing governance decisions, it creates two contingent markets: one for the token price assuming the proposal passes, and another for the price assuming the proposal fails. Which market prices higher determines the outcome: the proposal automatically takes effect or is rejected. DAOs no longer vote but call markets to make decisions, with participants betting real money on what they believe to be the better future outcome. Here, the underlying market is not just an input for decision-making but the decision-making mechanism itself.

If you assume all finance and markets are becoming programmable, while AI becomes increasingly powerful, then holding an expansive view of the endgame of finance is reasonable and exciting. Price signals, predicted market outcomes, on-chain fund flows, etc., will all become inputs that any application or agent can read, interpret, and act upon. If an agent can earn a penny more than the cost of reasoning by creating or participating in a market, then it is rational to do so.

When we factor in the consumption of AI agents and market participation, "a billion active traders" may still severely underestimate the future scale.

The Endgame of Finance

Finance is undergoing a transformation from a unique vertical industry to a horizontal foundational layer.

As markets become more expressive and accessible, finance is embedding itself into culture, while culture itself is increasingly expressed through finance. At the same time, as markets become permissionless software, they accelerate their role as drivers of change, opening up new opportunities for users to seek economic upside (and downside) in the things they understand and love. Moreover, users will also want their AI agents to improve their lives through market participation.

As markets become more programmable, finance, as a new building block of information infrastructure, is becoming increasingly ubiquitous. The most successful infrastructures are often invisible, and finance is on a path to integrating into the very fabric of everything.

This is why I am willing to hold an extremely grandiose expansive perspective on the endgame of "finance."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。