The United States has finally welcomed perpetual contracts, but it still cannot access the same products traded in other parts of the world.

Written by: Vaidik Mandloi

Translated by: Block unicorn

Last year, the trading volume of perpetual contracts (Perp) exceeded 90 trillion dollars. In comparison, this is more than the total GDP of the world's top ten countries. Today, perpetual futures account for about three-quarters of all cryptocurrency derivative trading, and its growth rate is almost faster than any other financial product in history.

Nevertheless, at least until last Friday, no American institution could legally trade these contracts. On May 29, the Commodity Futures Trading Commission (CFTC) approved Kalshi to list the first regulated Bitcoin perpetual futures contract in U.S. history. On the same day, the CFTC also approved Coinbase to guide its customers to global perpetual contracts and options trading through the Deribit platform.

After the announcement, Hyperliquid's token HYPE surged by 30%. For reference, Hyperliquid is currently the largest on-chain perpetual contract exchange, but it does not serve U.S. users. Michael Selig, chairman of the Commodity Futures Trading Commission (CFTC), published a commentary on Coindesk stating that perpetual contracts are “fundamental tools for risk management and price discovery in the global crypto asset market.” If you have been active in the cryptocurrency space for a while, witnessing all of this unfold is indeed quite incredible. Let me explain why this is so important.

How did perpetual contracts accumulate to 90 trillion dollars?

It all started in 1993 when Nobel laureate Robert Shiller published a paper proposing a futures contract that never expires. His idea was that homeowners could hedge against the risk of falling home prices without selling their homes.

This concept was interesting, but it had no practical application at the time, as the entire derivatives market operated on an expiry settlement model, with clearinghouses and margin models settling on fixed dates. For example, agricultural contracts settle monthly, and bond futures have interest payment dates. At that time, there was no corresponding supporting infrastructure, so this concept remained in academic journals for decades.

Then, in May 2016, three founders from Hong Kong decided to give it a try. Arthur Hayes, Ben Delo, and Sam Reed launched BitMEX, modifying Shiller's original concept. They built a Bitcoin-based perpetual futures contract and added a mechanism that ties its price to the underlying market, allowing users to trade with leverage of up to 100 times. Within just 18 months, BitMEX became the largest cryptocurrency derivatives exchange.

So, what exactly is a perpetual contract, and how does it work?

In a traditional futures contract, you bet on the price of the underlying asset on a specific date. For example, a Bitcoin futures contract expiring in June 2026 will settle in June at that time's price. If you want to maintain your position, you must buy the next contract. The problem is that each contract rollover incurs costs, leading to a gap in your position.

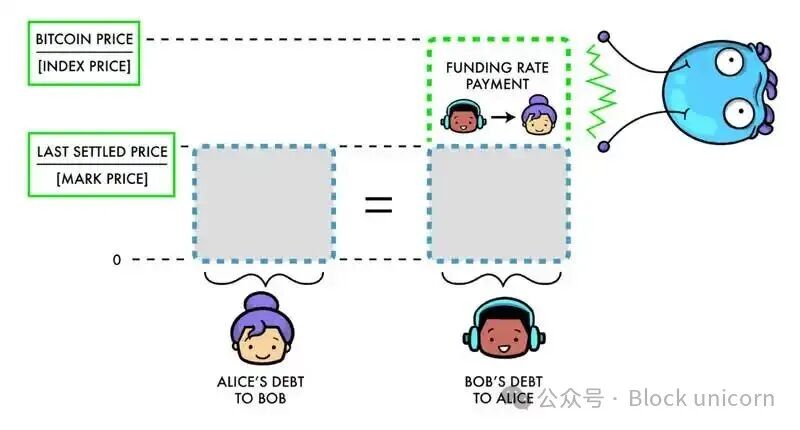

On the other hand, a perpetual contract completely eliminates the expiration date. You can open a position, and it will remain open until you close it. The holding period can be as short as five minutes or as long as five months. The key is that the price of a traditional futures contract naturally reverts to the actual price at expiration. But perpetual contracts do not, so other factors are needed to ensure price accuracy. To achieve this, it uses funding rates.

One reason perpetual contract exchanges are so popular is that, unlike traditional exchanges that disperse liquidity across quarterly contracts (March, June, September, December), perpetual contract exchanges concentrate all trading on one platform with a single order book. This makes perpetual contract exchanges one of the most efficient trading venues, and in financial markets, efficiency often compounds. The more traders there are, the narrower the spreads become, attracting even more traders to participate.

Offshore derivatives trading volume has grown from 28 trillion dollars in 2023 to over 90 trillion dollars by 2025. On-chain derivative trading volume on decentralized exchanges is growing even faster, with a 346% increase in 2025, reaching 6.7 trillion dollars. Moreover, on any given day, derivative trading volume is about 10 to 15 times that of spot trading. This means the price discovery mechanism for assets has shifted from the spot market to the derivative market. When Bitcoin fluctuates by 5% on Tuesday afternoon, this volatility almost always starts with derivative trading. The chain reaction of leveraged positions can trigger liquidations, leading to buying and selling, and the spot market follows suit.

The phenomenon of “the tail wagging the dog” (where the minor part dominates the whole) is occurring; while the part of the market that actually determines the price—the core of the cryptocurrency market—has previously been completely shut out from American institutions.

What does this mean for America?

The United States has finally welcomed perpetual contracts but still cannot access the same products traded in other parts of the world. Even Coinbase's own business needs to transfer funds to Dubai's Deribit through its subsidiary in Bermuda because liquidity has accumulated overseas under years of regulatory hostility and cannot be restored overnight.

U.S. traders have a leverage limit of about 10 times and enjoy full segregation protection from the Commodity Futures Trading Commission (CFTC); in contrast, offshore traders use leverage of 50 to 100 times. A 100x leverage means 1 dollar can control a 100-dollar risk exposure. A 10% price fluctuation can yield 10 times the return. In contrast, the option contracts corresponding to the same price fluctuations yield much less because the pre-paid option premium already includes part of the expected volatility, and the holding period continuously decays over time. A typical Bitcoin one-month call option, under the same 10% price fluctuation, yields about 3 times. Leverage is the key factor, and leverage in the U.S. remains relatively mild.

That is why Hyperliquid's stock price soared on the day the CFTC legalized illegal trading. Many people's first reaction was that trading volume would shift from Hyperliquid to Kalshi and Coinbase, and regulated trading platforms with institutional capital would erode the market share accumulated by Hyperliquid.

Hyperliquid generated 907 million dollars in revenue last year without a single U.S. user. Think about it, who exactly is trading on these platforms? The person shorting a certain memecoin 50 times at 3 a.m. would never go open an account at Kalshi to short Bitcoin 10 times. The regulated, fund-segregated institutional investors wouldn't use Hyperliquid in the first place. These are products aimed at completely different audiences. The CFTC's action actually just confirmed that the product category dominated by Hyperliquid is legal. For Hyperliquid, this is undoubtedly a validation of its own value.

Despite regulatory restrictions, U.S. exchanges are currently limited to Bitcoin trading, but Hyperliquid has completely surpassed cryptocurrencies. Through the HIP-3 protocol, anyone can initiate trades for any asset, and many trades are already live. During the trading peak in February, the daily trading volume for silver exceeded 4 billion dollars at one point, while oil trading volume also briefly surpassed Bitcoin in April.

The CEO of Intercontinental Exchange (ICE, the parent company of the New York Stock Exchange) Jeffrey Sprecher said two days before the CFTC approved the Hyperliquid exchange at a Bernstein conference: “What we are talking about now, Hyperliquid, if you haven't heard of it, it's larger than Nasdaq, do you understand?” Now, ICE is in discussions with Hyperliquid to understand their business model and ask regulators why traditional exchanges cannot offer the same products. The direction of learning has shifted: Wall Street is studying a decentralized exchange that was founded only two years ago with zero venture capital, as the trading infrastructure it built is precisely what the world's largest exchanges now want to replicate.

Perpetual contracts will consume everything

I believe this issue is more important than anything else because perpetual contracts are no longer limited to the cryptocurrency realm.

They initially started as Bitcoin trading tools but later expanded to all altcoins. Today, they have ventured into commodities such as gold, silver, oil, and gas. Then, they expanded into stocks like Nvidia and Tesla, and then to pre-IPO companies like SpaceX and OpenAI, now also encompassing prediction markets via the HIP-4 platform.

In just two years, perpetual contracts have evolved from being aimed solely at cryptocurrency hackers to financial instruments that could reference any global asset, trade around the clock, and have no expiration date or clearing intermediaries. Traditional derivatives made sense in an era where the overnight market was designed for trading and settlement at physical exchanges requiring paper documents.

However, in today’s global digital infrastructure, asset trading occurs around the clock, and time-based markets can have gaps. For example, an oil trader wanting to position ahead of geopolitical events on weekends would be powerless on any regulated exchanges. Such transactions are already possible on the Hyperliquid platform. The Commodity Futures Trading Commission (CFTC) has also acknowledged this. The agency's staff consultation regarding around-the-clock trading explicitly states: “Due to the digital infrastructure and global coverage, derivatives based on crypto assets may be very suitable for around-the-clock trading.”

The real competition now lies in whether U.S.-regulated trading platforms can quickly adapt to have an impact. For example, the average fee for centralized exchange futures is about 4 basis points, while Hyperliquid's fee is only 2 basis points. The gap in spot trading is even larger: 15 basis points versus 5 basis points. Since switching platforms takes only a few minutes, traders will only choose platforms with lower fees.

Analysts at Compass Point gave Coinbase a sell rating in the week that the CFTC approved its derivatives listing plan, arguing that the wave of competition in the derivatives market will weaken its pricing power and squeeze profit margins. Coinbase's revenue from perpetual contracts in Q1 2026 is projected to be 50 million dollars, while retail trading revenue has fallen to its lowest level since Q3 2024. Though the perpetual contract business has grown, it has also cannibalized the more profitable spot trading market.

In fact, this compression effect is evident in many areas. If you can have leveraged directional exposure to any asset anytime and anywhere without an expiration date, then traditional derivatives become insignificant. For example, since perpetual contracts can provide continuous exposure, why extend quarterly futures contracts? Indeed, during crowded trading, funding rates may exceed rollover costs, sometimes increasing by 2% every eight hours. Exchanges also have every incentive to maintain the existence of quarterly contracts, as rollovers mean two extra trades and two rounds of extra fees. But most retail traders hold positions for only a few hours or days. For them, contracts without expiration dates are clearly simpler.

Since perpetual contracts (perp) can also provide similar directional leverage, why buy short-term options? True, the downside risk of options is limited to the premium, but look at the actual trading volume. In 2025, the average daily trading volume of 0-day options on the S&P 500 index was 2.3 million contracts, most of which were pure directional bets. For this purpose, perpetual contracts (perp) are simpler.

I do not think perpetual contracts will completely replace options or traditional futures, as options can provide explicit risks and convexity returns that perpetual contracts cannot replicate. However, for the vast majority of trading activities focused solely on directional leverage, perpetual contracts are undoubtedly the superior, more economical choice. Ultimately, this product has proven successful, with an annual trading volume of at least 90 trillion dollars to back that up.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。