Taking the lead in discovering prices, trading continuously for 24 hours, and quickly moving toward institutionalization, there are significant opportunities for tokenized stock perpetual contracts in both the investment and business sectors.

Written by: Tiger Research (@tiger_research_)

Translated by: AididiaoJP, Foresight News

The cryptocurrency market is currently in a downturn, but the tokenized stock market is expanding in the opposite direction. It has clearly split into two major camps: fully collateralized spot and perpetual futures, with perpetual futures attracting the most attention and giving rise to various trading strategies.

Key Points

- Although U.S. stocks are reaching new highs, the total market capitalization and trading volume of cryptocurrencies have both declined. As the two trends diverge severely, the tokenized stock market achieves counter-cyclical expansion through the continuous growth of the total value of open perpetual futures positions.

- The market is divided into fully collateralized spot and perpetual futures based on collateral structure. Perpetual futures are particularly noteworthy for allowing trading of stocks not available on local exchanges, enabling 24-hour trading, and offering high leverage.

- After regular trading hours, perpetual futures prices become important leading indicators for the next day’s spot opening, able to predict direction and roughly estimate the degree of volatility.

- Current main strategies include two opening methods for the retail side, neutral basis trading (collecting spot - perpetual premiums as funding fees), and cross-exchange arbitrage.

- This same structure extends into business opportunities like market makers, regional oracles, token issuance, and basis hedge funds. Although the current scale is still small, significant opportunities exist in both the investment and business sectors as institutional funds enter the market.

The Stock Market is Absorbing Cryptocurrency Liquidity

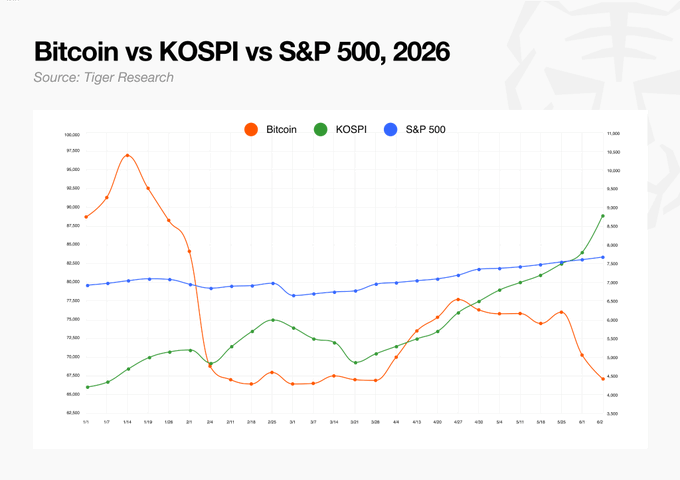

In Q1 2026, the total market capitalization of cryptocurrencies fell by 20.4%, and centralized exchange spot trading volume dropped by 39.1%. Bitcoin has continued to decline since its historical peak in October 2025.

In contrast, the trend in the stock market is completely opposite. The S&P 500 index has surpassed its annual target, while the KOSPI index has doubled this year, thanks to the semiconductor sector. While the total market capitalization of cryptocurrencies has significantly retreated, most national stock markets are setting historical highs. The divergence between these two paths has never been more pronounced.

Collateral Structure Splits the Market, Funds Continue to Flow into Perpetual Futures

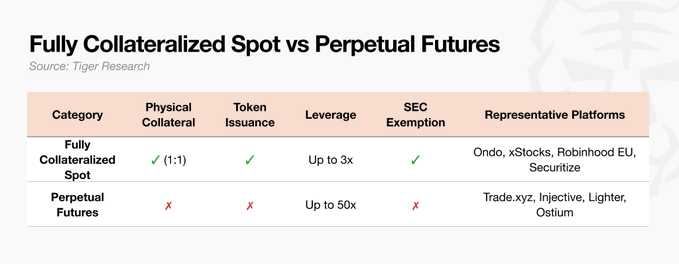

The tokenized stock market is clearly divided into two camps based on collateral structure.

- Fully Collateralized Spot: A platform deposits real stocks on a 1:1 basis and reissues corresponding tokens. Investors hold either the stocks themselves or legal entitlements to the stocks. The issuance details vary across platforms, but the underlying assets always exist authentically.

- Perpetual Futures: Completely different, as no real stocks are held. Traders can open positions simply by paying margin; contracts only track prices, with no extractable underlying assets. Margins are mainly stablecoins, and an increasing number of platforms have begun accepting other assets like ETH.

The reason perpetual futures attract the most attention is that they retain all the advantages of spot trading (24-hour trading of stocks that local exchanges cannot provide) while also offering significantly higher leverage compared to spot. Currently, some fully collateralized spot products on Kraken xStocks support up to 3x leverage, while perpetual futures can reach up to 20x depending on the product.

Since there is no need to custody underlying assets, prices can be tracked swiftly through oracles, allowing for rapid listing and a broader range of tradable targets.

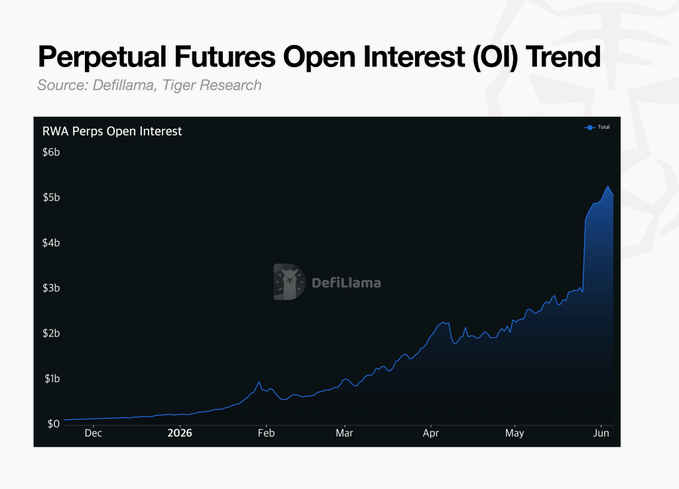

In comparison to traditional markets, the current scale is still quite small. The average daily trading volume of the U.S. stock market is around $1.1 trillion, while the total value of open positions in stock perpetual futures is only $2.25 billion. Although the metrics are different and not directly comparable, it is evident that the market is still in its early stages.

The trend is very clear: the total value of open positions is steadily rising each quarter, and regulatory agencies are beginning to view it as a formal market. The SEC has classified perpetual futures as innovative financial products, and the CFTC is publicly evaluating institutional pathways in the U.S. It started outside the regulatory framework but is quickly entering into it.

24-Hour Market vs Real Market

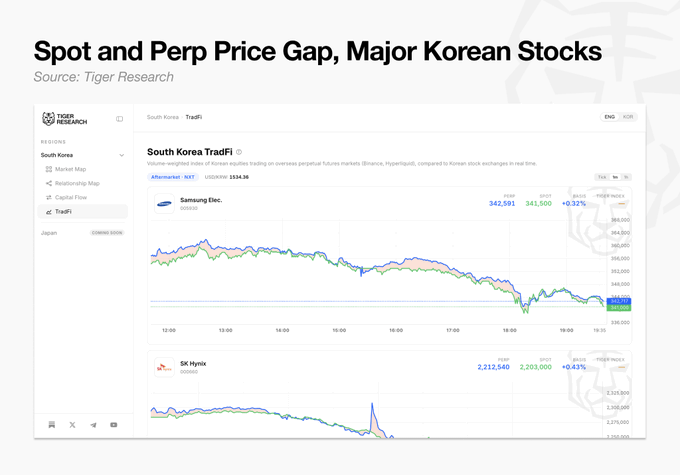

Tiger Research continues to track this transition and has developed a tool to compare the prices of Korean stocks in the overseas perpetual market with KRX spot prices in real-time. This tool aggregates perpetual exchange prices (weighted by volume) for targeted stocks such as Samsung Electronics, SK Hynix, and Hyundai Motor, displaying them alongside local spot prices.

Current data shows three clear patterns:

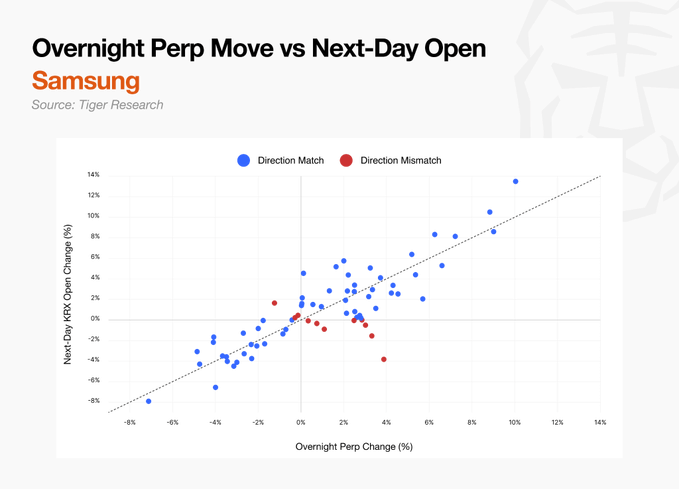

Overnight perpetual prices can predict the next day's opening

The Korean stock market closes at night while the U.S. stock market continues to trade, with global events like Nvidia's earnings report and foreign exchange fluctuations continuing to unfold. Perpetual futures, however, trade continuously for 24 hours.

The key question is: where does the reference price for perpetual futures come from during the spot market's closing hours?

The answer is: it no longer simply replicates the closed spot prices. During trading hours, perpetual futures mainly refer to institutional data; however, after the market closes, the trading of overnight participants directly determines prices. They are not replicating a closed market but discovering a new price reflecting overnight news and macro variables.

The data confirms this. In the samples of Samsung Electronics and SK Hynix, when the overnight perpetual price rises, the probability of an increase in the next day's opening is 82% and 95% respectively; when it falls overnight, the probability of a decrease in the next opening is 96% and 78% respectively. The alignment in direction is about 85%, with a high correlation coefficient of 0.85-0.89.

The magnitude is also highly consistent. When the overnight perpetual rises by 3%, the next day’s opening typically also rises by about 3%. The regression coefficients for Samsung Electronics and SK Hynix reach 0.93 and 1.00 respectively, allowing for a nearly direct prediction of the size of the opening gap.

The weekend effect is even more pronounced. During the period from Friday's closing to Monday's opening, the directional prediction accuracy of perpetual futures for Samsung Electronics and SK Hynix reaches 93% and 87% respectively, as perpetual futures first absorb the global variables from the two days.

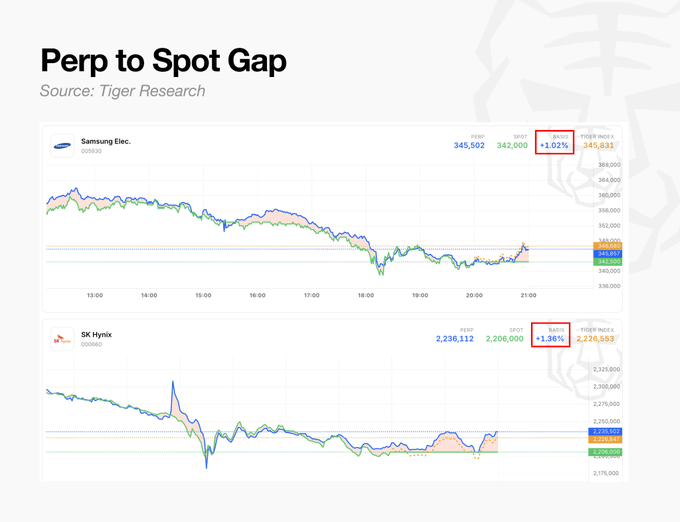

Neutral hedge trading of spot - perpetual premiums

Perpetual futures have no expiration date. To prevent the price from deviating too much from the reference value, both long and short parties exchange funding fees at fixed intervals.

For example, when the perpetual price is higher than the reference value, the profitable long position must pay the funding fee to the losing short position. The larger the premium, the higher the payment amount. To avoid costs, traders tend to converge towards the reference value, achieving price convergence.

Data shows that the perpetual futures of Korean stocks are generally higher than spot, with Samsung Electronics having an average premium of 0.15%, and SK Hynix at 0.23%. Shorting the perpetual can monetize this part of the premium during each funding fee cycle.

This led to the emergence of a trading strategy: buying KRX spot in the intraday while simultaneously shorting an equivalent quantity of perpetual futures. If the stock price rises, the spot gains while the perpetual loses; if it falls, the opposite occurs. The two positions hedge each other, leading to directional risk close to zero. The only source of profit is the funding fee income from the perpetual shorts. This strategy that eliminates directional risk is known as neutral hedge trading.

The premium does not exist long-term; after about 40 minutes on average, the spot - perpetual price difference tends to narrow by half. This strategy is suitable for high-volatility phases and requires continuous monitoring.

Cross-exchange price arbitrage

Perpetual prices for the same underlying asset can also vary across different exchanges. Data from June 2026 shows that the average perpetual futures price of Samsung Electronics on Binance is 0.93% higher than on Hyperliquid, and SK Hynix is 1.03% higher, with the maximum price difference reaching 2.3%.

Perpetual positions cannot be transferred between exchanges. Thus, traders can short on the high-priced exchange and long on the low-priced exchange, offsetting directional gains and losses. After the prices converge, the initial price difference becomes profit. Moreover, the short position on the high-priced side can also collect additional funding fees, further increasing returns.

Newly established exchanges often have higher prices, as arbitrage funds have not yet fully flowed in. In the early stages, as more exchanges come online, such price differences will repeatedly occur and further expand during nights and weekends (when spot markets are closed and exchanges independently price).

Market Changes and Emergent Opportunities

The biggest characteristic of this market is fragmentation, which is both a risk and an opportunity. The same underlying asset is traded across various platforms like local Korean exchanges, Hyperliquid, Binance, and Lighter, leading to fragmented liquidity. Price differences across venues not only increase judgment difficulty but may also trigger manipulation and chains of liquidation risks.

The strategies mentioned above are currently primarily aimed at retail users, but the same structure opens vast possibilities for the business side:

- Market Makers: Price differences of 0.15% to 0.75% for the same underlying asset across different exchanges further expand overnight. In the early market with insufficient arbitrage funds, the demand for market making will continue to grow.

- Regional Oracles: Perpetual futures price independently during the spot market's closing, with high accuracy relying on oracles. Dedicated oracles for Asian time zone assets such as Korean, Japanese, and Taiwanese markets are still a blank area.

- Tokenized Issuance: Currently, Korean stocks are limited to a few assets such as Samsung Electronics, SK Hynix, and Hyundai Motor. In the future, intermediary institutions will be needed to issue and manage KOSPI 200 component stocks and more major Asian companies.

- Basis Hedge Funds: Perpetual futures convert spot premiums into cash funding fees every hour. Dedicated funds that focus on cross-exchange basis and funding fee gaps can achieve faster capital turnover than traditional basis trading, though the current market scale remains small.

The tokenized stock perpetual market is still small compared to traditional markets, but it is playing a key role: taking the lead in price discovery, 24-hour continuous trading, and rapidly moving towards institutionalization. Significant opportunities exist in both the investment and business sectors.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。