If you are in the mainland and using a mainland bank card, do not treat the C2C within the exchange as a normal withdrawal channel.

Written by: Liu Honglin

Regarding the issue of bank cards being frozen due to cryptocurrency withdrawals, Lawyer Honglin has previously written many articles. It was originally thought that the risk warnings were sufficient, but recently friends have come to consult: the coin is in the exchange; they want to convert it to RMB, isn't there C2C on the platform? Find a certified merchant, the price is appropriate, and the payment is quick, but why is the card still frozen?

This question actually stems from many people's misunderstanding of the C2C on exchanges.

People believe that as long as it is "completed on the exchange page," "the merchant is certified by the platform," and "the order is recorded," this matter is safe. However, the actual problem often lies not with the coins you sold but with the money being deposited into your bank card.

First, the conclusion: If you are in the mainland and using a mainland bank card, do not treat the C2C within the exchange as a normal withdrawal channel.

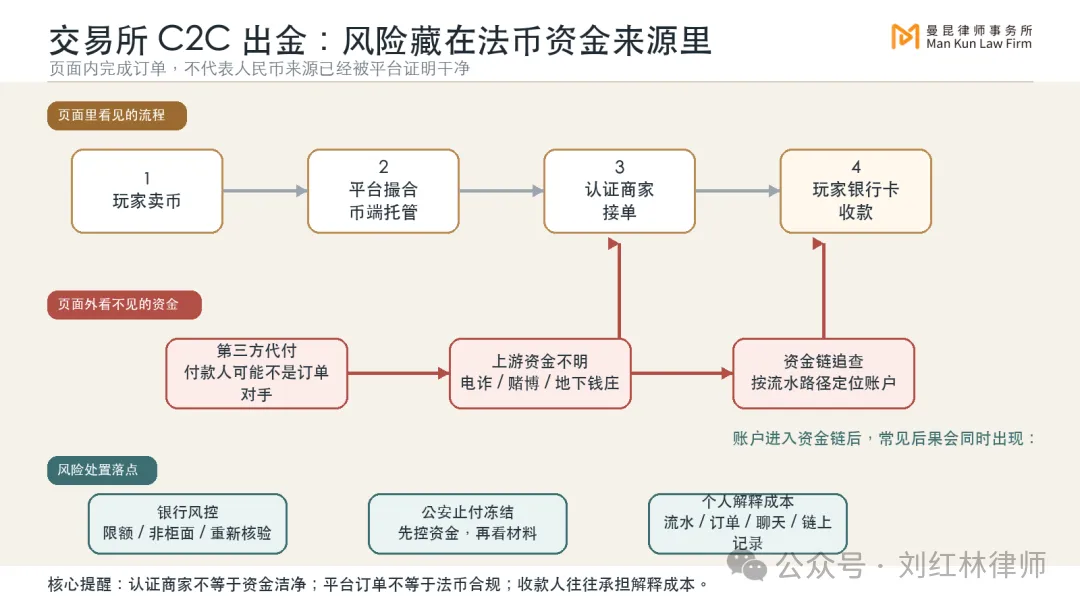

The C2C is the segment where ordinary players are most likely to underestimate the risks. It looks like a button on the exchange, but in reality, it is a RMB transfer that occurs between you and a stranger. The exchange may hold the coins, may display merchant certification, and may provide the order page and chat records, but on the RMB side, the money that ultimately enters your bank card is the amount transferred by the counterpart.

The issue is here: you can confirm that the coins you sold were clean coins from your account, but it is difficult to ascertain where the money transferred to you by the other party came from.

Risk Chain of C2C Withdrawal in Exchanges

C2C is not self-operated by the exchange

Many players have the first layer of misunderstanding, thinking that the C2C within the exchange is the exchange’s own cash register. It seems that users sell coins to the exchange, and the exchange pays RMB to the users, with a big platform backing it, so the risk should be lower than external OTC transactions.

In reality, it is not like this. In most C2C transactions, the platform does advertising display, order matching, coin custody, and dispute handling. The coins circulate within the platform, but RMB usually flows through bank cards, payment accounts, or other fiat payment tools outside the platform. What you receive is not the platform’s own funds, but rather a transfer from the buyer’s counterpart or their designated paying party.

This determines that the risk of C2C is not as simple as "whether the exchange will run away," but rather "whether the fiat currency you receive can withstand anti-fraud, anti-money laundering, and judicial financial chain tracing." In the context of mainland regulation, engaging in activities related to the exchange of fiat and virtual currencies, providing information intermediary services and pricing services for virtual currency transactions are strictly prohibited activities related to virtual currencies. Financial institutions and non-bank payment institutions are also prohibited from providing services such as account opening, fund transfer, and clearing and settlement for activities related to virtual currencies.

Therefore, for mainland players, C2C has never been a "normal exchange window" recognized by regulators. It is more like an influx of foreign unfamiliar funds connected through the exchange page.

Certified merchants on the platform are not safe

From the perspective of criminal groups, one of the biggest attractions of virtual currency is that it can break down, convert, and transfer funds from scams, online gambling, illegal fundraising, and underground banks, and then complete deposits and withdrawals through different accounts. Ordinary players may not recognize these people when selling coins and receiving payments, nor do they know what has happened with the previous funds, but your bank card might just happen to receive a segment of it.

The most troublesome aspect is that when public security and the banking system look at the financial chain, they won’t first ask if you are an old player in the crypto space or judge whether you are a bad person subjectively. What they see first is: after the victim was defrauded, money flowed from Account A to Account B, and then to Account C, with a certain amount reaching your account. As long as your account enters this chain, stops payments, freezes, and restricts non-counter transactions may occur first.

According to the requirements of the "Anti-Telecommunications Network Fraud Law," banking financial institutions and non-bank payment institutions must strengthen monitoring of bank accounts, payment accounts, and payment settlement services, and take measures such as verifying transaction situations, re-verifying identities, delaying payments, or restricting or suspending relevant services for suspicious transactions; Public security agencies and relevant departments should establish systems for instant inquiry of funds related to cases, emergency stops of payments, rapid freezing, timely unfreezing, and returning funds.

The judicial interpretation of money laundering criminal cases released by the two high courts in 2024 has pushed this issue further. The interpretation clarifies that transferring or converting criminal proceeds and their benefits through "virtual assets" transactions can be recognized as one method of money laundering. The judicial interpretation also states that to determine whether a person "knows or should know," factors such as the information they are exposed to, the funds they handle, the types and amounts of funds, the methods of transfer and conversion, transaction behaviors, unusual situations of fund accounts, work experience, and relationships with upstream criminals should be considered comprehensively.

In other words, not everyone whose card is frozen will constitute a crime, but if the trading pattern itself is abnormal, with high frequency, large amounts, complex parties, and evidently unreasonable prices, or if you have long been receiving payments for others, buying and selling on behalf of others, or making a profit on the difference, the matter is no longer as simple as "the bank card is frozen."

Many people will say, I found a platform-certified merchant, the exchange has reviewed it, why should I still worry?

Certification only indicates that the platform has done some kind of identity or trading ability verification according to its own rules; it does not mean that the upstream funds for this RMB are necessarily clean. More realistically, some merchants may just be a node within the fund network. The money they pay you today might come from normal coin-buying users, a third-party payment account, or funds that were recently split from fraudulent activities.

Ordinary players find it hard to penetrate this issue. What you can see are the other party’s nickname, transaction volume, approval rate, payment screenshots, and platform customer service records. What law enforcement and bank risk control systems see are the paths of inflow and outflow between accounts, the duration of funds, transaction frequencies, risk labels for counterparts, and information from reported victims. The worlds seen by both sides are entirely different.

Another detail easily overlooked in the C2C of exchanges is that in many orders, the payer’s real name on the platform, trading counterpart, and chat participants may not be consistent. Some merchants will say "payment from company finance," "family account payment," or "third-party channel payment," and players, eager to complete the transaction quickly, will accept it. But once this money encounters issues, it will be very passive to explain. It is hard to clarify why a stranger is transferring money to you, why the note is inconsistent with the transaction, or why your bank card is receiving multiple unfamiliar funds within a short time.

These types of issues are not minor matters in banks and police. They are directly related to whether your account is identified as an abnormal account and also whether the materials can form a complete and credible transaction chain during subsequent explanations.

A frozen bank card is not a small matter

Some players understand a frozen card as a part of life in the crypto world: if it is frozen, just unfreeze it, and it will be fine after explaining. This mentality is very dangerous.

When a bank card is restricted, it seems to be an account issue, but it can actually affect many aspects of your life. Salary cards, mortgage cards, corporate collection cards, family joint accounts, if they are all associated with the same risk event, the processing cost can quickly escalate. The bank may require you to explain the situation at a counter, and public security may require you to submit transaction records, chat records, platform orders, on-chain transfer proofs, and the source of funds. Some freezes may come from public security in other locations, where communication cycles are longer and material standards are not entirely the same.

What is more troublesome is that when you explain, you often encounter an awkward situation: you want to prove that this was only a coin selling transfer, but in the mainland regulatory documents, the exchange of fiat and virtual currencies is not a business scene that is encouraged or normally served by financial institutions. You can explain that you did not participate in fraud, did not launder money, and did not knowingly receive stolen goods, but it is hard to package this transaction as an ordinary civil receipt without risks.

If it is just sporadic, small amounts, and with complete evidence, the follow-up may lead to account restrictions being lifted, funds being returned, or continued cooperation in the investigation. But if the trading becomes long-term and professional, or if you knowingly transact despite the other party's fund abnormalities, it may lead to more complex criminal risk discussions.

The first common risk is assisting in activities of information network crime. It usually appears in upstream crimes like telecommunications network fraud, where someone knowingly provides a bank card, payment account, collection code, exchange account, or helps with collection, transfer, or withdrawal, even when aware that the other party may be committing internet crimes. For ordinary players, the greatest danger is not occasionally selling coins, but rather lending their bank card or exchange account to others, or receiving payments, exchanging coins, or transferring funds according to directives from others, all for collecting so-called service fees or processing fees.

The second type of risk is concealing and hiding criminal proceeds and benefits from those proceeds. In simple terms, the money from upstream crimes has arrived, and someone helps transfer, convert, split, and cash it out, assisting in turning "dirty money" into assets that seem harder to trace. If you continue trading despite evident abnormal pricing, third-party payments, frequent small splits, and payments from various unfamiliar accounts, the risk will significantly increase.

The third type of risk is money laundering. The judicial interpretation of money laundering in 2024 has already included the transfer and conversion of criminal proceeds and their benefits through "virtual assets" transactions. It doesn't mean that ordinary players selling coins automatically constitute money laundering, but if the types of upstream crimes, paths of funds, transaction frequencies, counterpart identities, abnormal prices, and your professional experience are considered together, they can sufficiently prove that you were aware, or should have been aware, of issues with the funds, and things can become serious.

Another easily overlooked situation is that someone has made C2C withdrawals into a stable business, continuously organizing buy-sells, acting as an intermediary for payments, and facilitating transactions between strangers, earning through exchange differences, fees, or processing fees. At this point, the discussion is not just about a specific frozen card anymore, but may involve illegal operations, assisting in moving criminal funds, or even forming conspiracy with upstream and downstream personnel. Many people before getting into trouble think of themselves merely as "transferring bricks in the crypto space," but in the eyes of law enforcement, you may have already become a fund conversion node between RMB and virtual currency.

What players should avoid

If you are an ordinary individual, the most prudent choice is to avoid using C2C within the exchange for withdrawals to mainland bank cards. Especially avoid frequently receiving large amounts of transfers from strangers, do not accept transfers where the payer is inconsistent with the trading counterpart, do not pursue obviously abnormal buyers for higher exchange rates, do not use family, friends, employees, or company accounts to receive payments on your behalf, and do not lend your bank card, payment accounts, or exchange account to others.

Most importantly, do not engage in businesses like "helping others withdraw", "acting as a payment agent", "running scores", or "transferring bricks to earn differences." Many people initially think they are just helping a friend with coins or just earning a small processing fee, only to later discover that they have played the role of a bank account and virtual currency conversion node in others' designed financial chains.

If the account has already encountered problems, the first reaction should not be to delete records, concoct excuses, or find someone to "manage" the situation. The correct approach is to fully save platform orders, chat records, payer information, bank statement records, on-chain transfer records, and transaction timelines, first clarifying whether it is due to bank risk control, anti-fraud stopping payment, or judicial freezing, and then submit materials as required by the bank or investigative agency. If the amounts involved are significant, there are multiple accounts, or if the freeze is from a different location or has already been inquired about, it is advisable to seek early intervention from a lawyer to organize facts and evidence clearly.

For people who genuinely live, work, or operate abroad, it is recommended to use legally permitted and regulated transaction and payment paths in their location, and try to maintain accounts under their own name for receiving and sending payments, retaining materials related to taxes, wages, investments, transactions, and sources of funds.

The current situation in the cryptocurrency industry is aptly described as a dark forest, so the best way to protect yourself is not to trust strangers. When you encounter trouble during the withdrawal process, the dark and gray industries will not explain for you, the exchange will not help you unfreeze your bank card, and certified merchants will not prove that every penny is clean. After all, the ones who truly face the banks, police, and adverse impacts on life are often yourself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。