Author: @bonnazhu, Bonna | U Yogurt

This wave of STRC linkage rapidly declined; in my opinion, it could be the best financial teaching case.

Still a long warning, with a strong personal touch.

TL;DR

- If MSTR is really going to die, it will still die from reflexivity, but not this time.

- The return to par value for STRC is just a matter of time; this is the essence of floating-rate bonds.

- Selling coins for money is merely quenching thirst with poison; it solves short-term problems but leads to endless troubles.

Detailed interpretation as follows:

First, how to understand this wave of BTC decline?

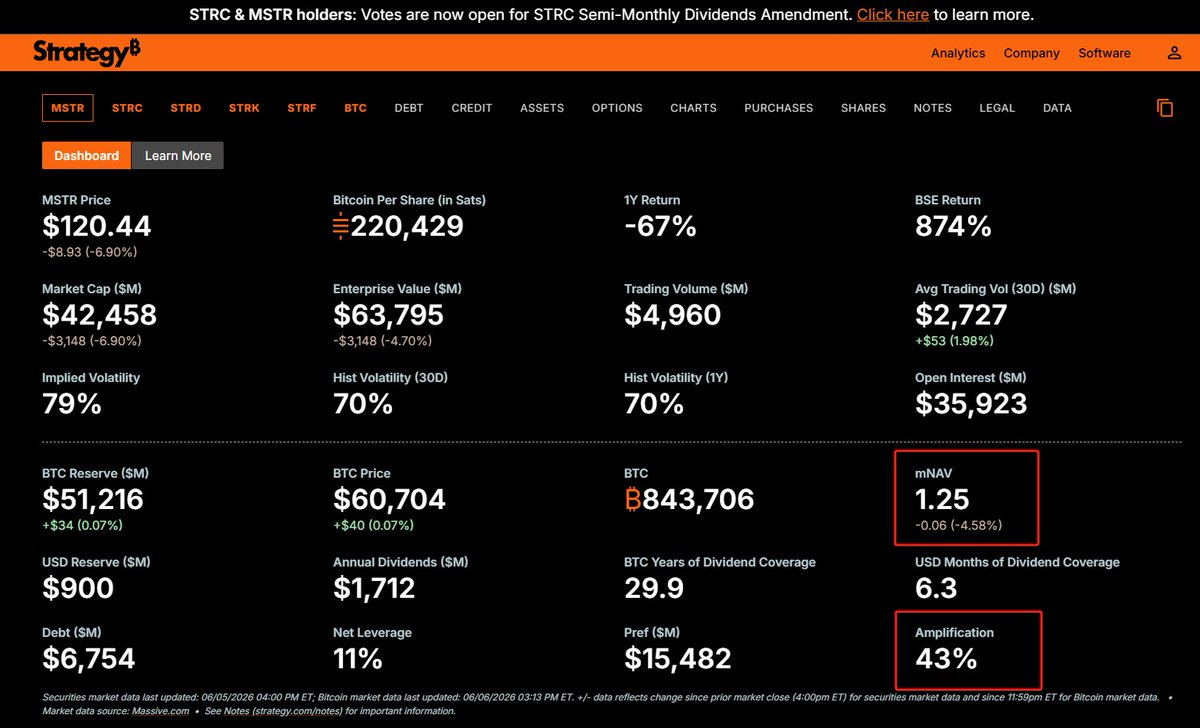

Personally, I tend to believe that this quick decline of BTC is a targeted strike on MSTR from the capital side. The reason is that MSTR repurchased some convertible bonds using its already insufficient cash reserves (which the market generally believes is a safety net reserved for preferred stock dividends), causing the cash reserves' coverage of preferred stock dividends to plummet from over two years to about half a year, followed by the sale of 32 BTC.

The market immediately sensed the smell of "cash flow crisis" and quickly launched an attack, while fears about large IPOs draining resources, the World Cup reallocating attention, rising inflation, and cooling interest rate hike expectations, all bottled up, further facilitated the attackers in realizing this expectation on the market, thereby quickly forcing funds with asymmetric information to surrender or hesitate to intervene to buy the dip.

This is actually a typical reflexivity in traditional financial markets:

Market prices do not passively reflect reality, but instead actively change reality.

In other words:

Expectations are contagious, and this contagion can alter reality.

The same script played out when Soros attacked the pound; the Bank of England's foreign exchange reserves might have been sufficient initially, but once market participants believed it was insufficient and collectively shorted it, the reserves indeed became insufficient. Bank runs work the same way; if everyone simultaneously believes it will fail and withdraws money, the expectation of failure may become reality!

In MSTR's case, the attackers' playbook is:

Cash reserves decreasing → Market expectations of a liquidity crisis leading to forced coin sales → Panic selling pushes down BTC → BTC decline further compresses mNAV and worsens the balance sheet → The expectation of "not being able to hold on" becomes increasingly materialized, thereby reducing the cards available to play → More people join the short selling → Expectations become even more materialized.

Furthermore, BTC itself cannot create a sustainable cash flow to cover dividend payments for MSTR; the reliance on financing is a vulnerability that attackers can easily exploit.

Second, the logic of STRC declining alongside and returning to par value

STRC and MSTR common stock have a relationship of preference and subordination:

Common stock as subordinate absorbs most of the risks from BTC price volatility.

STRC can generally maintain relative stability as preferred.

According to MSTR's overall target debt ratio of about 33-35% (currently, due to BTC's price drop to 61k, the debt ratio has increased to around 43%), theoretically, only if BTC prices drop below 26k will the common stock hit zero, and the preferred stock will truly be affected.

So, why does STRC also decline?

This involves some fundamentals of bond pricing.

STRC is a preferred stock but essentially behaves like debt, with floating interest and no maturity date.

The price of a bond essentially equals the present value of all future cash flows (each period's interest, calculated at face rate + principal at maturity, totals face value of 100), discounted back using a required return rate. This required return rate is the necessary yield currently demanded by the market.

If the face rate is equal to the necessary return rate, then the discounted price equals par value 100, which often happens when the bond is issued; investment banks usually reference the current market conditions and investor yield requirements to set the face rate.

However, the lifecycle of a bond is long; throughout its duration, external interest rate environments and the issuer's creditworthiness can change, impacting the corresponding discount rate (the denominator) for that necessary yield. If the market's required return rate rises while the face interest (the numerator) remains the same, the present value discounted will fall below par value, resulting in a bond trading at a discount; conversely, if the required return rate falls, the bond will be at a premium.

Therefore, the price of a bond is never a static number; it reflects how much return the market currently requires to hold it.

When the price drops below par, it implies: "The market needs higher interest than the face rate." If you indeed buy it at this discount and hold it to maturity, your final yield will indeed exceed the face rate, compensating for the part of the return the face rate didn’t provide. In other words, the market is using the discount to demand compensation it believes is deserved but was not given by the face rate.

STRC is similar. Market concerns over MSTR's cash flow transmit into a repricing of STRC's repayment capability. The narrative of a "cash flow crisis" fermented leads to a jump in required yields for holding STRC, making the 11.5% face rate inadequate.

Of course, from the perspective of external attackers, this is all about staging: only if STRC declines alongside can the "cash flow crisis" be realized under conditions of information asymmetry, making you unable to help but wonder:

Is there something I don't know?

For fixed-rate bonds, the story typically ends here; the rise in market required yields can only be matched through price decline, making discounts potentially long-term fixtures that don’t return to par value. But STRC is not a fixed-rate bond; it has a floating rate, meaning the numerator can be adjusted.

For example, if the market demands a 12% necessary return rate to hold STRC, and MSTR's management raises the face dividend from 11.5%, the price can’t remain below par 100 for long. In such cases, if you buy STRC at a discount, the actual returns will exceed 12%, so buy orders will naturally flood in, driving the price up to the level where the implied return equals 12%, that is, to par value.

This is why medium to long-term floating-rate bonds are certain to anchor to par value 100; this is essentially an attribute of floating-rate bonds.

For MSTR, the return of STRC price to a par value anchor of 100 is even more crucial for its ongoing financing. Because if issued at a discount, the company nominally issues at a face value of 100, but the buyer only pays 90 dollars, it means the company is using the dividend obligations determined at a 100 face value to pay interest for only 90 dollars actually received, effectively raising its true financing cost out of thin air, resulting in losses with each financing, is that possible?

Third, when mNAV > 1, sell stocks, never sell coins

So, what is the key to breaking the deadlock?

As mentioned earlier, this entire decline is a reflexive script of a self-fulfilling prophecy, based on information asymmetry and expectations of a cash flow crisis. To break the deadlock, it’s enough to prove that this liquidity crisis doesn’t exist, replenishing reserves, at which point the attackers will lose their foothold, and the reflexive spiral will self-destruct.

So how do you replenish reserves?

Like many people on X shout, do we let Saylor directly come out and say: "In this wave of decline, we sold more coins, and now we have enough funds for several years"? This move can indeed work; the panic could end.

But its cost comes with another layer of implicit uncertainty.

Because it’s essentially telling the market: you need to reprice me.

The narrative of "continuously increasing holdings, never selling coins, constantly enriching every shareholder’s BTC content" capital market premium wheel is certainly gone, replaced with, "If necessary, I might sell a lot of coins to shrink my balance sheet, thus diluting every share's BTC content," at least a three-step forward, one-step backward, discounted wheel.

The result is that you don’t know how the common shareholders will react, whether mNAV will completely disappear. Even if it doesn’t disappear, contraction is highly likely, after all, the premium of mNAV > 1 corresponds to an implied "future per-share BTC content will be greater" Call Option, and as the acceleration of BTC content increases slow down, the Call isn’t worth as much as before.

The significance of the mNAV premium for MSTR is self-evident because MSTR’s expansion logic does not rely solely on common stock, or on something like STRC which behaves like equity but is fundamentally debt; rather, it’s about adding water to flour and flour to water so that the overall debt ratio remains under control within the ideal 33-35% range. The narrowing of mNAV premium will directly impact the subsequent stock issuance financing windows, representing behavior that quenches thirst with poison.

In my view, a better approach should be to take advantage of the current situation where mNAV = 1.25x with a significant premium still present, to raise funds through issuing additional stock to replenish cash reserves. MSTR still has ample Shelf Offering quota registered with the SEC, which is the only operation that can clearly please both STRC's holders and the common stock shareholders without the risk of repricing.

The specific mechanism is:

When mNAV is significantly greater than 1, choosing to issue and sell stocks first means that with each additional dollar of stock issued, if all of it is used to buy BTC, it can create over a dollar of shareholder value in the capital market. That is precisely why shareholders are willing to hand their money to you. And precisely because of this, in this state, you don’t actually have to spend all the money raised to buy coins: you can completely retain a portion as cash reserves for future principal and interest repayment, without negatively impacting shareholder value. At the same time, with increased cash reserves, STRC holders will also feel safer, alarms alleviated, the risk premium reduces, and STRC will gradually return to anchor, thus even if you later want to raise STRC, it won’t conflict with each other.

Conversely, choosing to sell coins for money is quenching thirst with poison; if the repricing leads to a narrowing or even disappearance of mNAV, the pathway of raising stocks to buy coins will not be viable because, at that point, the fair value of your stock equals the BTC behind it, so why wouldn’t I just buy the coins directly? Moreover, you need to retain a portion of the financing to pay interest, which is a blatant negative for shareholder value: it means taking my money, spending part to buy coins (creating equivalent value in the capital market), and the other part directly used to pay interest, which is a loss.

This is a structure of net loss.

And at that time, since the issuance of additional shares would become infeasible, the issuance of STRC would gradually be affected; not only would the overall expansion wheel likely get stuck, but your financing window would also close, relying solely on cash reserves, and if cash reserves run out, then you are really left with only selling coins, and by that time, it would be the end.

Furthermore, selling stocks has the added benefit of directly improving the debt ratio. Currently, because BTC has dropped to 61k, MSTR's overall debt ratio has risen from the target of 33-35% to around 43%. Issuing and selling stocks brings in equity capital: cash (on the asset side) increases, equity grows, and after deducting a small portion retained for interest payments, the overall debt ratio will further improve.

And what about selling coins? Because the cash obtained from selling coins is immediately paid out as dividends, the asset side first sees a reduction in BTC, followed by cash flowing out; the net effect is a shrinkage of total assets while liabilities remain unchanged, slightly worsening the debt ratio.

Sell stocks: Improve debt ratio ✓, preserve every share's BTC content ✓, don’t harm premium ✓

Sell coins: Worsen debt ratio, reduce every share's BTC content, significantly harm premium

Which is better is crystal clear.

Finally, if I say if,

If MSTR really sells a large number of coins to replenish reserves?

Then, indeed, it will be as many X users and even Delphi’s people say; the short-term crisis will definitely be resolved, BTC will rebound, and STRC will return to anchor. That’s why I say that if MSTR is really going to die, it won’t be from this time; both selling stocks and coins can indeed solve the urgent situation.

But for me personally, it would demystify MSTR and Saylor.

Moreover, due to the repricing of the common stock logic, that call option for "per share BTC content" is not worth as much as it used to be, causing the mNAV premium to gradually disappear, resulting in BTC rebounding, STRC returning to the anchor, while the divergence of MSTR's common stock declining occurs.

The next time cash reserves hit bottom again, and the market re-expects coin sales, the reflexive script will play out once more; who knows if it will be the beginning of the end.

But honestly, if such an outcome truly occurs, I would accept it.

Perhaps "change" is itself a part of this “situation."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。