Author: Hu Tao, RootData

1. Transparency-Driven Cryptocurrency Exchange Rankings

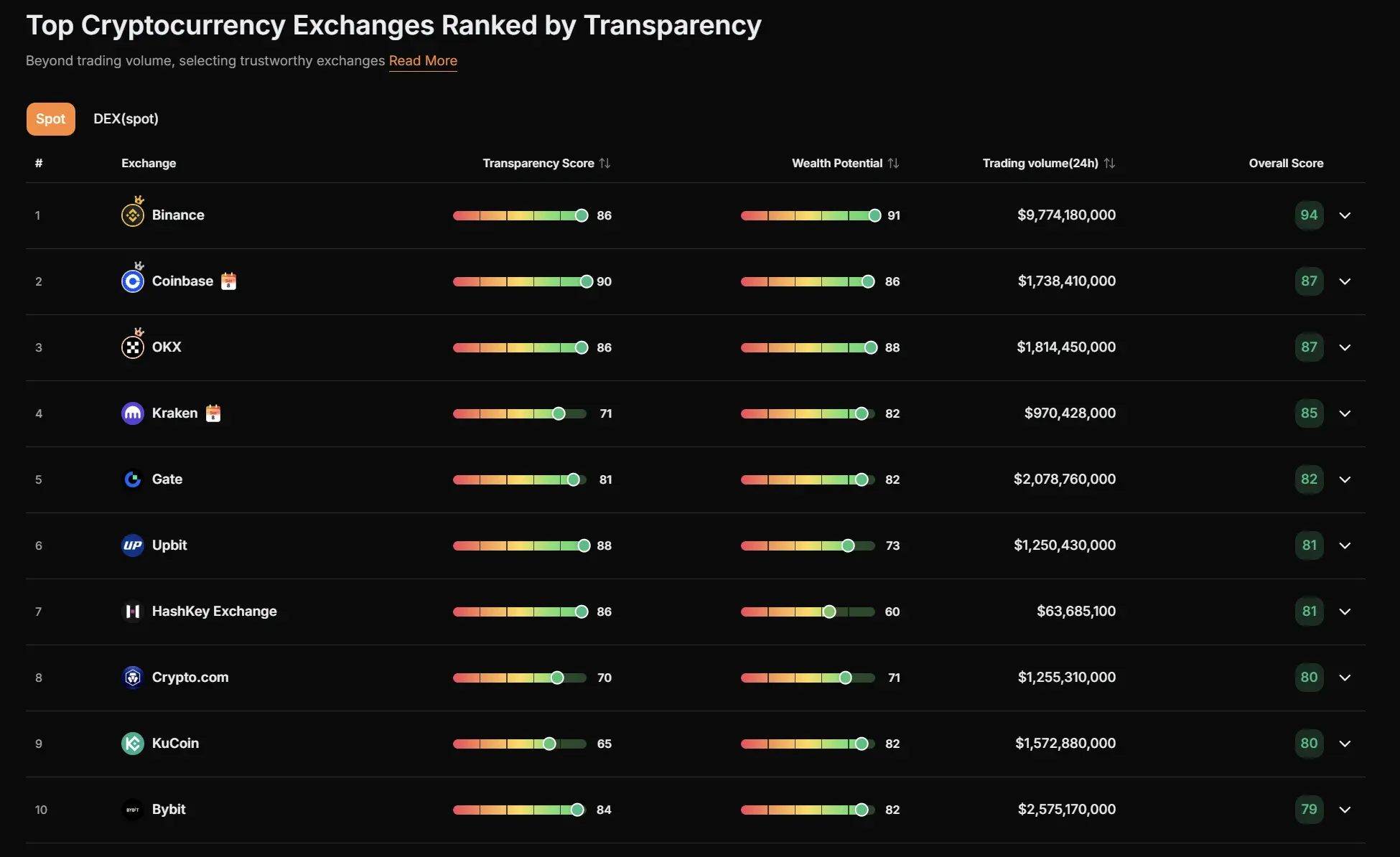

In the May cryptocurrency exchange rankings compiled by RootData, Binance, Coinbase, OKX, Kraken, Gate, Upbit, HashKey Exchange, Crypto.com, Kucoin, and Bitget ranked in the top 10.

This ranking is based on rich data from RootData, integrating multiple indicators from various exchanges including trading volume, reserve size, coin performance, compliance, and transparency, while avoiding the impact of activities like wash trading on the rankings, to objectively reflect the competitiveness and ranking of exchanges in the cryptocurrency market.

In this period's ranking, the changes in rankings among major cryptocurrency exchanges were minimal, with Binance maintaining the top position due to the highest trading volume and wealth effect. Coinbase's rank improved by 1 position to 4th place, and although HashKey Exchange had lower trading volume, it made its first entry into the top ten thanks to its compliance and a transparency score of 86.

2. Overview of the Development Status of Cryptocurrency Exchanges in May

1. Cryptocurrency Market Trading Volume Declines for Five Consecutive Months

In May, the spot trading volume of cryptocurrency exchanges was $725.7 billion, a slight decline of 2.2% from April, marking the fifth consecutive month of decline since January, reflecting the ongoing overall trend in the market.

At the beginning of this month, the cryptocurrency market briefly continued the slight upward trend seen in previous months, with major cryptocurrencies like BTC reaching new highs since the end of January, BTC prices surpassing $82,000, and several tokens such as HYPE, ZEC, WLD, and ONDO seeing overall price increases exceeding 100%.

Market expectations for a new round of upward cycles began to heat up quickly. However, this optimism did not last long. By mid-May, the market began to show a clear turnaround. Bitcoin was the first to end its upward trend and entered a correction phase, with the downward trend gradually expanding.

By the end of the month, within just a few trading days, the price of Bitcoin quickly retreated from around $75,000 to the $62,000 region, not only completely giving back the gains made in May but also erasing most of the accumulated profits from previous months. Accompanied by the price drop, many altcoins saw even greater declines, leading to a rapid cooling of market risk appetite and a simultaneous shrinkage in trading volume.

The reasons for this market reversal were not due to a single event, but rather the simultaneous release of multiple negative factors within the same time window.

First, discussions about the impact of quantum computing on the security of cryptocurrency assets continued to brew in May. Several researchers in post-quantum cryptography and blockchain security indicated that AI is accelerating the development of quantum computing and forcing the crypto industry to reassess the reliability of existing security systems. Although the industry generally believes that quantum computing is still a long way from posing a real threat to mainstream blockchain networks, such discussions have heightened the risk-averse sentiment among some investors.

Second, the siphoning effect of traditional capital markets on funds has further intensified. Throughout May, the technology sector, represented by AI, semiconductors, data centers, and storage industries, continually hit historical highs. Nvidia, AMD, and a series of AI infrastructure companies have been attracting significant global capital inflow driven by both performance and capital expenditure. In contrast, the crypto market lacks new core narratives, as none of the Layer 1s, public chains, DeFi, or meme sectors have managed to create sustained hotspots, leading a large amount of institutional capital to shift toward more deterministic tech assets.

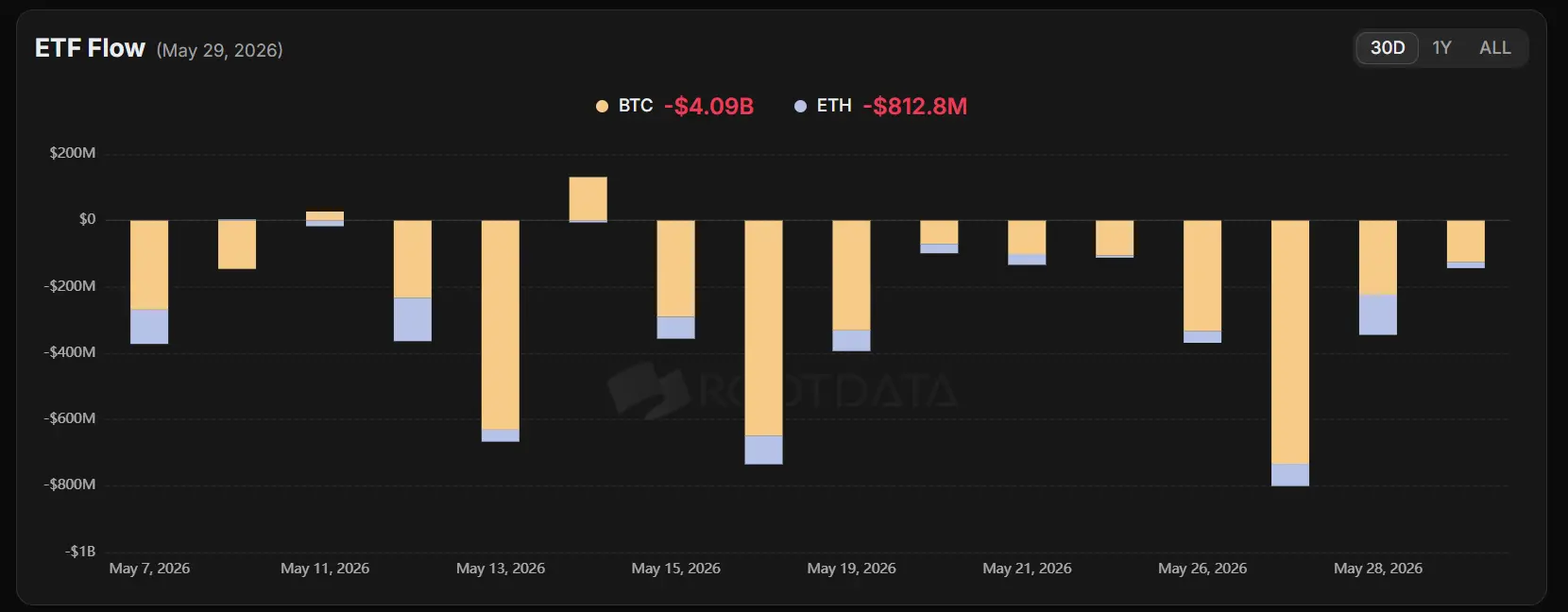

At the same time, changes in the ETF market have also further weakened market confidence. As one of the important forces driving the rise of Bitcoin over the past two years, cryptocurrency ETFs experienced continued net outflows in May, indicating a slowdown in institutional capital influx. For the market, ETF funds not only represent real purchasing demand but also signify institutional investors' judgments on future market trends. When this long-term support force begins to diminish, market expectations for subsequent upward space also decline accordingly.

The most symbolic event, however, stemmed from changes in Strategy's actions. As one of Bitcoin's most steadfast buyers in recent years, Strategy has long acted as a provider of market liquidity and a confidence anchor. However, as the company began selling part of its BTC holdings to meet funding needs, the market's faith in “infinite accumulation” first showed signs of weakening. Although the scale of the selloff is relatively small compared to its overall holdings, the signal it released carries far more meaning than the actual selling pressure itself—when the most steadfast long-term holder in the industry turns to selling, market sentiment inevitably gets impacted.

Under the combined effects of tightening macro liquidity, continuous siphoning of funds by tech stocks, weakened ETF demand, and industry confidence being shaken, the cryptocurrency market in May ultimately ended the months-long upward trend and returned to a downward channel.

For exchanges, the five-month consecutive drop in trading volume reflects issues that are not simply related to market cycle fluctuations but indicate that the growth model of traditional crypto asset trading is gradually reaching a bottleneck. When Bitcoin and altcoins struggle to continuously create new wealth effects, finding new tradable assets and new sources of growth has become the most urgent topic for the entire exchange industry. This has also directly propelled May's most vital industry mainline—the full-scale explosion of the competition for tokenization of U.S. stocks.

2. U.S. Stocks Become Core Strategy for Exchanges

Against the backdrop of a lack of strong trends in native cryptocurrency assets, U.S. stocks have become a new battleground for exchanges to compete for user trading frequency and capital retention, and even a core strategy. The core logic is not complex: U.S. stocks have the deepest liquidity globally, the most mature narrative system, and high-attention sectors such as AI, chips, military industry, and crypto concept stocks. As long as exchanges can integrate these assets into their systems, they can extend the duration that user funds remain and upgrade the “buy coin app” into a “cross-asset trading entry,” thus gaining more trading fee revenue and improving capital market valuations.

Since May, leading exchanges including Binance, Bitget, and Gate have announced or launched new U.S. stock-related products covering various categories such as stock spot, ETFs, tokenized stocks, and stock perpetual contracts.

Among them, Binance's actions are the most representative. At the beginning of June, Binance opened trading functions for over 7,000 U.S. stocks and ETFs in the spot market and simultaneously launched the bStocks program, allowing users to map their holdings to on-chain assets in the future.

Bitget chose a route more aligned with cryptocurrency's native characteristics, launching Stocks 2.0 and Reality platforms centered on tokenized stocks, achieving the circulation of stock assets in the crypto ecosystem through on-chain issuance, USDT settlement, and linkage with margin and yield products.

Exchanges like Gate, Bybit, and BingX are also actively laying out related sectors, competing for market share through stock perpetual contracts, on-chain stocks, and cross-market trading.

The essence of this round of competition is not merely to increase new trading varieties. The deeper significance lies in the fact that crypto exchanges are attempting to upgrade from “digital asset trading platforms” to “global asset trading gateways.”

However, the U.S. stock trading functionality also brings new compliance and product risks. Tokenized stocks are mostly closer to price mapping tools, and users usually do not directly enjoy traditional shareholder rights; different platforms have significant differences in underlying custody, price discovery, trading time, dividend processing, and applicable legal jurisdictions. In the future, competition among exchanges will not only depend on "how many stocks are listed," but also on underlying asset proof, compliance boundaries, liquidity depth, and user protection mechanisms.

3. Capital Markets Frequently Bet on the Exchange Sector

In May, there was a notable increase in capital market interest in the exchange sector, particularly focused on markets in South Korea, Japan, the United States, and Hong Kong, where regulations are relatively clear or institutional demand is strong.

Historically, exchanges primarily earned revenue from spot and contract transaction fees, but now stablecoins, custody, payment, RWA, stock trading, and institutional services are becoming new growth engines.

Especially against the rapid development of U.S. stock tokenization and real-world assets (RWA), exchanges have evolved from mere trading venues to important infrastructures for asset issuance, liquidity management, and cross-market settlement. This transformation has also attracted significant traditional financial capital back into the industry.

Moreover, the number of platforms globally that truly possess licensing resources, brand effect, and liquidity advantages is decreasing, with the industry concentration continuously increasing. For investment institutions, the certainty of investing in leading exchanges is significantly higher than investing in individual cryptocurrency projects.

South Korea is the most active region for exchange equity trading this month. Financial giant Samsung Securities and Hanwha Financial Group successively acquired more than 8.55% of the shares of Dunamu, the parent company of Upbit, enhancing their depth in the digital asset space.

Additionally, Coinone received strategic investments from OKX Ventures and Korea Investment & Securities, and the South Korean payment solution WeHub announced its acquisition of the South Korean cryptocurrency exchange Flybit,

In the Japanese market, the country's second-largest telecommunications operator KDDI reached a strategic investment and business cooperation agreement with Coincheck Group, where KDDI will purchase Coincheck's new shares for approximately $65 million, holding a 14.9% stake afterward. For Coincheck, KDDI's user reach capability helps lower the threshold for opening and using digital assets; for KDDI, Coincheck provides the infrastructure for entering digital assets, reward investments, and potential Web3 financial services.

The Hong Kong-based cryptocurrency options trading platform SignalPlus completed a $50 million B1 round of financing led by HashKey Capital this month, with a post-investment valuation reaching $500 million, and indicated plans to transform into an institutional-level multi-asset trading infrastructure provider.

The capital markets clearly believe that even if the overall growth of the cryptocurrency market slows, exchanges that master user access, liquidity networks, and compliance capabilities will still be one of the most valuable business models in the coming years.

3. Major Exchange Cases and Analysis

1. Binance

In May, Binance's spot trading volume was $250.4 billion, a slight decrease of 1.6% from the previous month, but the decline was significantly lower than that of most competitors, reflecting Binance's leading advantages in global liquidity networks, user scale, and asset coverage capabilities.

In this month, Binance continued to maintain a low frequency of new coin listings, adding only three new currencies: OPG, GENIUS, and AIGENSY. However, on the asset page, Binance announced the launch of the DYOR Research Center, collaborating with platforms such as RootData to provide all users with information on project teams, unlocks, and on-chain dynamics.

Amid the excitement around U.S. stocks, Binance's current focus remains largely on U.S. stock trading functions, further accelerating the transition from a cryptocurrency exchange to a comprehensive asset trading platform.

Following the launch of perpetual contract trading for U.S. stocks and the listing of several tokenized U.S. stocks issued by Ondo, Binance officially announced the launch of its U.S. stock trading feature on June 1, offering spot trading services for over 7,000 U.S. stocks and ETF products to select regional users. Users can conduct transactions directly using stablecoins, and achieve fragmented holdings and round-the-clock market participation.

In team changes, Binance CMO Rachel Conlan announced her departure in June, with former Trust Wallet CEO Eowyn Chen stepping in as interim CMO.

2. Coinbase

As the largest compliant cryptocurrency exchange in the United States, Coinbase also faced challenges brought by the declining market activity in May. This month, Coinbase's spot trading volume was $44.7 billion, a slight decrease of 4.7% from the previous month.

This month, Coinbase launched six new currencies including MetaDAO (META), Derive (DRV), Citrea (CTR), Nexus (NEX), Wrapped Ronin (WRON), and KAIO (KAIO).

More noteworthy than the new tokens, however, is Coinbase's further exploration in the field of traditional financial assets. This month, Coinbase launched perpetual contract products related to gold, silver, and several U.S. stocks for the first time, marking one of its most important product expansion moves in recent years. As more and more exchanges begin to lay out stock, ETF, and commodity trading of on-chain assets, the boundaries between traditional financial markets and the crypto market are rapidly blurring, and Coinbase is also starting to seek new growth space within this trend.

However, unlike exchanges such as Binance, Bitget, and Gate that directly launched tokenized stock products, Coinbase remains relatively cautious in the related fields. This is closely related to its long-standing compliance path in the U.S. Amid the ambiguous regulatory framework, Coinbase prefers to enter the market via derivatives, brokerage services, and collaborations with traditional financial institutions rather than directly providing large-scale U.S. stock trading capabilities.

While this strategy limits its expansion speed in the current tokenization frenzy of U.S. stocks in the short term, it also reduces potential regulatory risks and aligns with its increasingly institutional strategy in recent years.

This strategy saw significant progress at the end of May. Coinbase announced that it has become a regulated futures commission merchant (FCM) under the U.S. Commodity Futures Trading Commission, officially providing global crypto derivatives market access services for U.S. institutional clients. For Coinbase, this not only means it can directly serve professional investors such as hedge funds, asset management institutions, and large trading firms, but also marks an enhancement in its position within the U.S. financial regulatory framework.

3. Upbit

In May, Upbit's spot trading volume was $31.3 billion, a slight decline of 7.6% from the previous month, with its drop being more significant among mainstream cryptocurrency exchanges, reflecting the more pronounced downturn of the South Korean cryptocurrency market compared to the overall market.

This month, Upbit launched eight new currencies including Solstice (SLX), io.net (IO), OriginTrail (TRAC), Irys (IRYS), Superform (UP2), Venice (VVV), Pharos (PROS), and dogwifhat (WIF), more than half of which are assets that have been issued for over six months.

Upbit's operator Dunamu disclosed this month that its consolidated revenue for the first quarter of 2026 was approximately $157 million, down 55% year-on-year; with an operating profit of approximately $59 million, down 78% year-on-year; and a net profit of approximately $46.6 million, down 78% year-on-year.

However, contrastive to the weak operating data, the capital market's interest in Dunamu has not weakened. Samsung Securities and Hanwha Financial Group respectively acquired 2% and 6.55% of Dunamu shares this month, valuing the company at $10.2 billion.

For institutions like Samsung Securities and Hanwha Financial, what they may be targeting is not Dunamu's current profitability but its core access position in the South Korean digital asset market, as well as the potential value in future business areas such as securities tokenization, stablecoin payments, and digital asset custody.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。