Futures, options, contracts for difference, these things sound very professional.

In the past, many people thought that derivatives were the most high-threshold play in traditional financial markets, but these plays are becoming increasingly common in the crypto industry.

Recently, discussions in the crypto community have included not only the U.S. stocks themselves but also topics like: “Recently, making arbitrage on Hyperliquid has been so enjoyable that I don’t want to do any research,” and “I only care about funding.”

If these statements were made a few years ago, they would refer to arbitrage opportunities with Bitcoin or Ethereum, but as U.S. stocks have gone on-chain and become a trend, now they are focusing on stocks like Samsung, Nvidia, and GameStop.

Although trading U.S. stocks has almost become a thoughtless activity. In the popular sectors like chips, energy, and optics, if you blindly throw money in, your account is very likely to increase. There are always people around who have doubled their money by hitting one or two stocks. But these smart crypto professionals earn money in a way that has nothing to do with “whether stocks go up or down.”

A group of people from the crypto circle is quietly making a new profit by using the strategies from the crypto market in U.S. stocks.

An Everlasting Contract

This logic starts with something called perpetual contracts. Perpetual contracts are the most traded form of “alternative futures” in the crypto market; they don’t expire, don’t require manual rollovers, and are specifically used to bet on price movements and leverage, allowing you to open a position worth fifty dollars with just five dollars, available for trading twenty-four hours a day, and if you suddenly want to place an order at three in the morning, no one will stop you.

However, perpetual contracts come with a problem: how can a contract that never expires keep its price aligned with actual stocks and not deviate?

The crypto industry’s solution for perpetual contracts is to introduce a mechanism called funding rates.

Simply put, the funding rate is a sort of head tax, where the one with more people has to pay money.

For example, if you are bullish on Nvidia and want to open a long position of five times on the contract without waiting for the U.S. stock market to open.

The problem is, too many people want to do this, the long side is crowded, while the short side has few participants. To balance both sides, the system stipulates: the side with fewer people pays, and the side with more people receives. Thus, if you are going long, every few hours, you automatically send a sum of money to those on the short side. The more people there are doing long with you, the more you pay, and it really feels like paying a fine.

So, how expensive can this fine get? A few real numbers can clarify this.

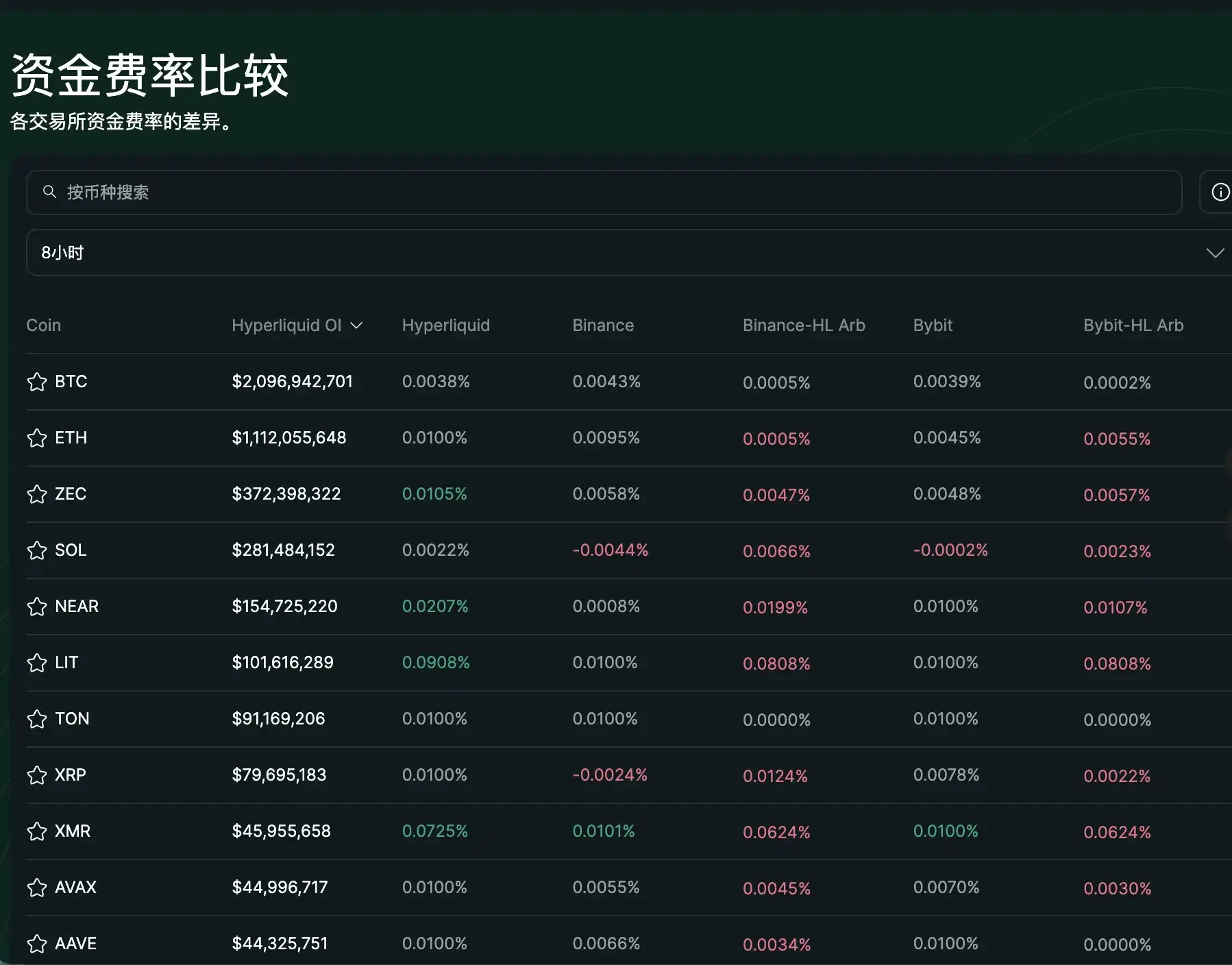

Binance is the world’s largest cryptocurrency exchange by trading volume; on it, the long funding rate for Samsung Electronics' perpetual contract is an annualized 364%, meaning that if you fully leverage to go long on Samsung for a whole year, just this head tax will consume more than three times your principal. Nokia’s annualized is 403%, and BBX is 591%.

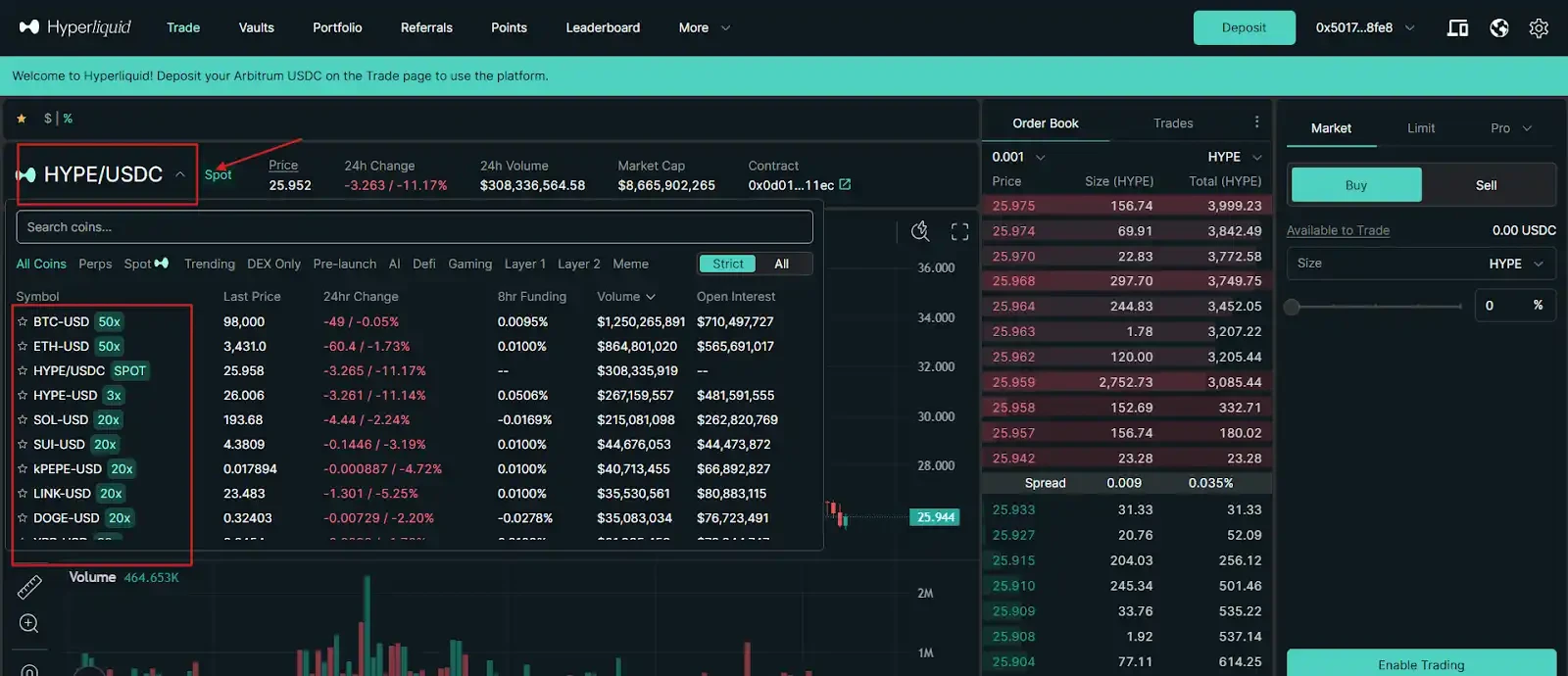

Another platform worth mentioning is Hyperliquid, which is currently the largest decentralized perpetual contract trading platform by on-chain trading volume. It does not require account registration, no KYC; anyone can connect their wallet and trade directly, making it a product in the crypto space that brings the perpetual contract experience closest to that of a centralized trading platform.

Hyperliquid trading interface

On it, Dell shows 281%, GameStop GME 227%, and even Zoom has 287%, with so many people rushing to leverage and bet it will go up.

This funding rate also has an interesting aspect as it clearly signals the level of enthusiasm between longs and shorts.

Currently, the more heated the market, the stock that has been pursued the most recently, filled with long positions, has the highest rate. Conversely, the funding rate for Eli Lilly, one of America’s largest pharmaceutical companies, is negative, being negative on both Binance and Hyperliquid. Going long on Eli Lilly not only incurs no cost but allows you to earn 65% annualized on Binance, or 103% on Hyperliquid.

This indicates that there are too many short sellers on Eli Lilly, so the system has to pay to hire people to go long in order to maintain balance. The same stock can have different rates on different trading platforms; Apple is 0 on Binance and -14% annualized on Hyperliquid, and this difference itself is also an arbitrage opportunity. These numbers don’t lie; the more aggressively you go, the nicer the returns for those on the other side.

These extreme rates are visible in real-time on platforms like Hyperliquid, generating cross-platform arbitrage opportunities (e.g., rate differences between Binance and Hyperliquid)

A New Business After U.S. Stocks Go On-Chain

Cbb (X: @Cbb0fe) is a well-known figure in the crypto space, having made his initial fortune in the crypto market, where he has spent years arbitraging token perpetual contracts. He earlier published a post on how to run an arbitrage bot on Hyperliquid and earned five million dollars.

He is also one of the first to transplant this strategy into U.S. stocks.

Cbb's operational logic is simple: on one side, buy real stocks in the regular market, and on the other side, take an equal amount of short positions in the contracts. If the stock price rises, the money made on the spot fills the loss on the contract; if it falls, the gains from the contract compensate for the losses on the spot.

By hedging both sides, price movements have nothing to do with him; what he cares about the most is that head tax. He stated that by just collecting funding fees recently, he has earned two million four hundred thousand dollars. While everyone outside is crazily trading U.S. stocks for profit, he is selling shovels to the gold diggers. Now that perpetual contracts have taken off in U.S. stocks, he has directly applied the strategies refined in the crypto space to targets like Apple and Samsung.

Some may ask why such opportunities exist only in the crypto space and not in traditional finance? In fact, the traditional market has similar mechanisms known as borrowing fees and overnight interest, where you'd have to pay a cost to finance leverage or borrow stocks to short. However, that money goes into the broker's pocket; the entire mechanism is opaque, and you cannot see the overall long-short ratio in the market, nor can you interact as a counterparty to receive those fees. Brokers keep this business for themselves; ordinary people only have to pay, without the opportunity to earn. Perpetual contracts have made this mechanism transparent, where anyone can see real-time rates and anyone can be the one to collect fees. This is something created by the crypto space now applied to U.S. stocks.

It’s not just individuals like Cbb who are doing this; institutions are also starting to eye this lucrative area.

Ethena is one of the largest stablecoin projects in the Ethereum ecosystem, considering reallocating part of its reserves to hedge. They have calculated that this could generate an additional 40 million to 80 million dollars in revenue per year.

Ethena captures funding fees through delta-neutral hedging (long spot + short perpetual), which has become the core mechanism for its USDe yield. This strategy has been built into its protocol mechanism, qualifying it as a quantifiable “rent-collecting” income rather than mere speculation.

For institutions, this isn't gambling; it's a stable cash flow that can be included in asset allocation, more akin to collecting rent, with those leveraging to trade U.S. stocks as the tenants.

So, the question arises: Will astronomical annualized rates like 364% for Samsung and 591% for BBX always exist, or will they eventually be filled?

Let’s compare this to Bitcoin; early on, the funding rate for Bitcoin perpetual contracts hovered around 18% annually. After the spot ETF was launched, arbitrage funds from Wall Street came in and halved the rate to 9% in just a few months.

It’s likely that U.S. stock perpetual contracts will follow a similar path; the current high rates are because the number of arbitrageurs entering is still small and the market is thin.

However, Binance has now launched spot trading for over 7,000 stocks, the NYSE is pushing for round-the-clock trading, and the U.S. futures regulatory authority, the CFTC, has started to signal compliance pathways for perpetual contracts, with both sides moving towards each other. Currently, the CFTC has opened compliance pathways for Bitcoin perpetuals, platforms like Coinbase have launched simulated perpetual products, and Hyperliquid's open interest on stock perpetuals continues to grow. As arbitrage funds flood in, a compression path similar to Bitcoin’s early drop from 18% to 9% in rates is likely to repeat in U.S. stock perpetuals.

So at this stage, it essentially represents an early dividend window, where those who enter first can take the biggest slice of the pie.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。