If tradeXYZ successfully completes on-chain pricing for SpaceX ahead of schedule again, its influence may further expand.

Written by: SpecialistXBT, Jack, Rhythm

Editor's Note: Last week, the AI chip rising star known as the "Nvidia Challenger," Cerebras Systems, officially landed on NASDAQ. On its first day of listing, the stock price soared to $350, nearly doubling from the IPO issuance price of $185, attracting widespread market attention.

However, even before its official listing, the Pre-IPO perpetual contract on tradeXYZ had already provided on-chain price discovery for CBRS hours or even weeks in advance. tradeXYZ achieves continuous trading and real-time price discovery that traditional finance cannot reach through perpetual contracts, allowing ordinary investors to participate in new stock pricing weeks in advance. This means that the traditional financial IPO grey market and roadshow model are being disrupted by on-chain finance, with traditional pricing power being gradually eroded.

Today, according to official news, tradeXYZ's Pre-IPO market has officially launched SpaceX, with the code SPCX. As one of the most anticipated unlisted companies in the world, SpaceX is seen as a potential candidate for the largest IPO in human history, with market valuation expectations reaching up to $2 trillion. If tradeXYZ successfully completes on-chain pricing for SpaceX ahead of schedule again, its influence may further expand.

This article was first published on March 19, detailing the pricing mechanism and operational logic of tradeXYZ. The following is the original text:

In the early hours of March 9, the situation in Iran escalated. CME was closed, ICE was closed, and major global futures exchanges were shuttered. The next official quotation for crude oil would have to wait for the Monday morning session hours later.

But the crude oil contract CL-USDC on Hyperliquid did not wait. On that day, the trading volume of this on-chain perpetual contract skyrocketed from the usual $21 million to over $1.2 billion. Traders were able to price geopolitical risks in real-time using an on-chain protocol during the closure window of the traditional market.

This incident was spread in the crypto community as another victory for DeFi. But few asked a more fundamental question: Where do the prices from this on-chain exchange come from when the external markets are closed?

Where do prices come from when there are no external quotes?

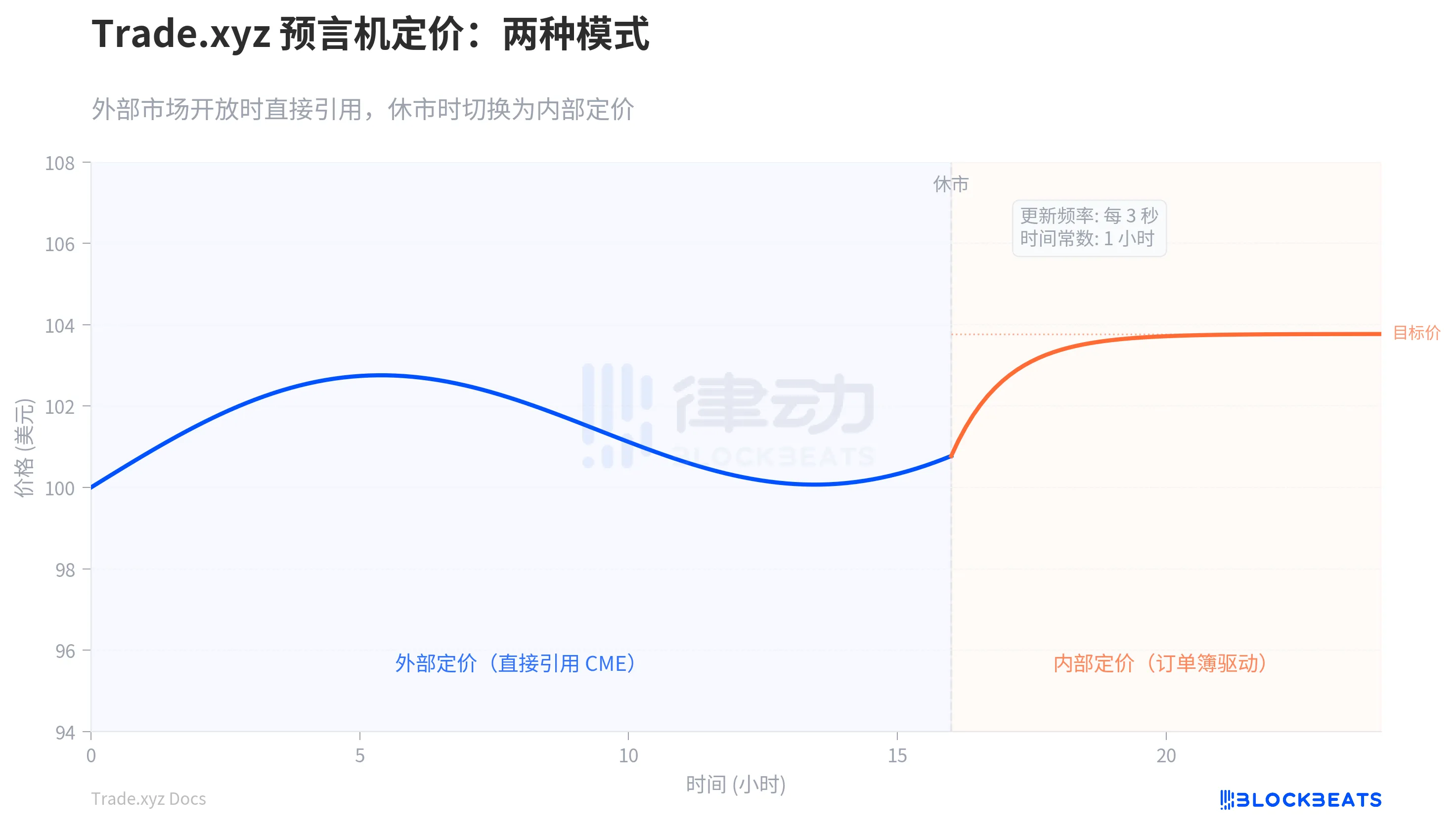

tradeXYZ is the largest provider of traditional asset perpetual contracts on Hyperliquid. It operates on the HIP-3 protocol, accounting for 90% of HIP-3's total open interest. The S&P 500, NASDAQ 100, WTI crude oil, gold, silver, and South Korean stocks can all be traded there 24/7. However, the pricing logic of perpetual contracts is entirely different from spot trading. Spot exchanges derive prices directly from the matching of buyers and sellers, while perpetual contracts require an "anchor" to tie the contract price to the true price of the underlying asset. This anchor is the oracle.

In traditional futures markets, the anchor for pricing is the exchange itself. The CME crude oil futures price is the price of crude oil, and no additional reference point is needed. However, tradeXYZ's contracts run on the Hyperliquid chain, which has no direct connection to the matching engine in Chicago. When CME is open, tradeXYZ's oracle directly references CME's quotes, which is not technically challenging. The real problem arises when CME is closed.

tradeXYZ's solution is to have the oracle extract information from its own order book. The system calculates a "impact price difference," simply put: if someone wants to buy a large amount now, how much higher would the average transaction price be compared to the current price? If someone wants to sell a large amount, how much lower would it be? This deviation reflects the imbalance of buying and selling power in the order book. The oracle adds this deviation to the current price, resulting in a "target price," and then uses a decay function to slowly bring the current price closer to the target price.

The key word is "slowly." The oracle updates every 3 seconds but only moves a small portion of the difference between the current price and the target price each time. This movement speed is controlled by a time constant. The larger the time constant, the more sluggish the oracle becomes, making it harder to manipulate, but also less able to reflect true market sentiment.

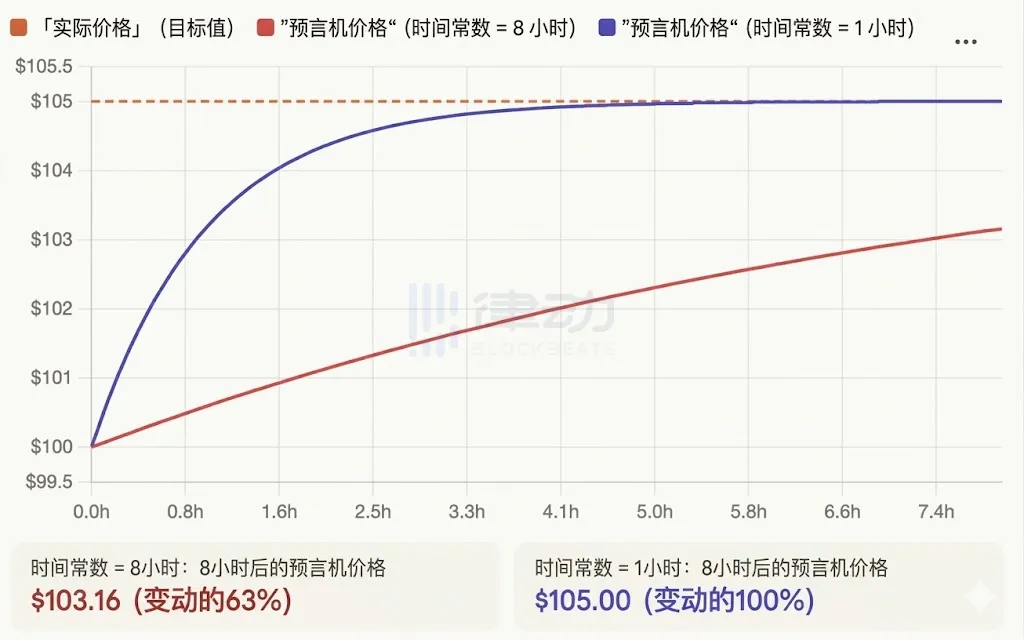

Initially, the time constant on tradeXYZ was set to 8 hours. In November 2025, this parameter was reduced to 1 hour. The reason for the adjustment is related to the traders' real money: tradeXYZ settles the funding rate every hour. The oracle tracks true prices too slowly, causing profit-seeking traders to be continuously drained by the funding rates.

As shown by the red line below, if you've taken a long position in crude oil and are correct, but the oracle takes 8 hours to catch up to the true price, during those 8 hours, the price never reaches your target level (the true price), and your profits are significantly eroded by the funding rates.

After the parameter was reduced to 1 hour, the price reached your expected position (blue line) in just 5 hours, allowing the price to confirm your judgment more quickly and resulting in fewer funding fees than before.

But a faster oracle also brings new risks. If the oracle stops functioning for 6 hours due to a fault and suddenly resumes, according to the formula, it would jump directly to a target price of 99.7%. Such instant price jumps could trigger large-scale liquidations. tradeXYZ's solution is to add a safety valve: regardless of how much actual time has passed, the effective time difference for each update is capped at 6 minutes. Even if the oracle recovers after being down, the price can only catch up in small incremental steps.

Cages, re-anchoring, and Monday opening gaps

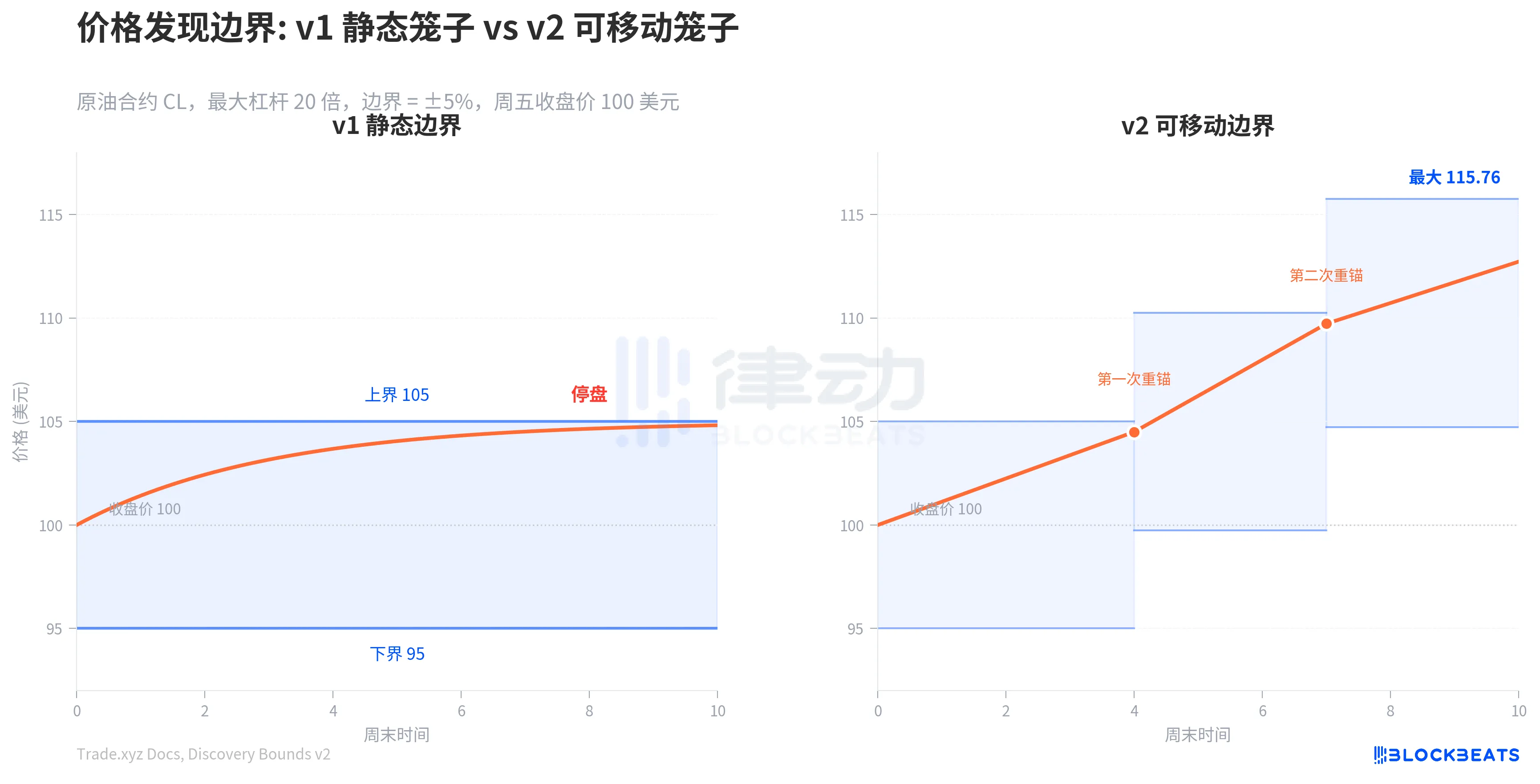

The oracle pricing solves the problem of "how do we price over the weekend." But another problem arises: to what extent can prices move freely?

tradeXYZ draws a "cage" for each contract. The marked price is restricted within a certain percentage above and below the last external closing price. This percentage equals the inverse of the maximum leverage. The maximum leverage for crude oil contracts is 20 times, so the cage is 5% above and below the closing price. If crude oil closes at $100 on Friday, the marked price can only fluctuate between $95 and $105 over the weekend. If it touches the boundary, trading halts directly.

In early March, crude oil contracts halted over the weekend.

Under normal weekends, this mechanism operates well. A 5% buffer is sufficient to digest most overnight fluctuations. However, geopolitical events on the level of March 9 can push prices directly to the cage boundary. All market information is suppressed, and when CME opens on Monday, if the true price jumps 8%, it will create a massive gap. Those holding short positions could be liquidated instantly, and market makers would incur losses due to their inability to hedge gradually.

In March 2026, tradeXYZ deployed "Price Discovery Boundary v2" for crude oil contracts. The core change: while the size of the cage remains the same, the cage can move. When the oracle price hits 90% of the current boundary, the system re-anchors the center of the cage to the boundary value and draws a new cage of the same size around the new anchor point. A maximum of two re-anchors can be executed in each direction.

To put it in specific numbers: the initial cage ranged from $95 to $105. When the oracle rises to $104.50, a re-anchor is triggered, and the new cage becomes $99.75 to $110.25. After a second trigger, it becomes $104.74 to $115.76, which is the endpoint. Starting from $100, the maximum discoverable range expands to about $115.76.

This design keeps the instantaneous fluctuation range at 5% at all times, and the risk model for market makers does not need to change. At the same time, re-anchoring means the system "acknowledges" the price movements that have already occurred, reducing the gap at the Monday opening. However, the costs are clear: a liquidation price at -8% for long positions would be absolutely safe under v1 (since prices would not reach -8%), but under v2 could enter the liquidation zone after a downward re-anchor. tradeXYZ chose to be the first to deploy v2 on two crude oil contracts and indicated that they would decide on a broader rollout after observing the effects.

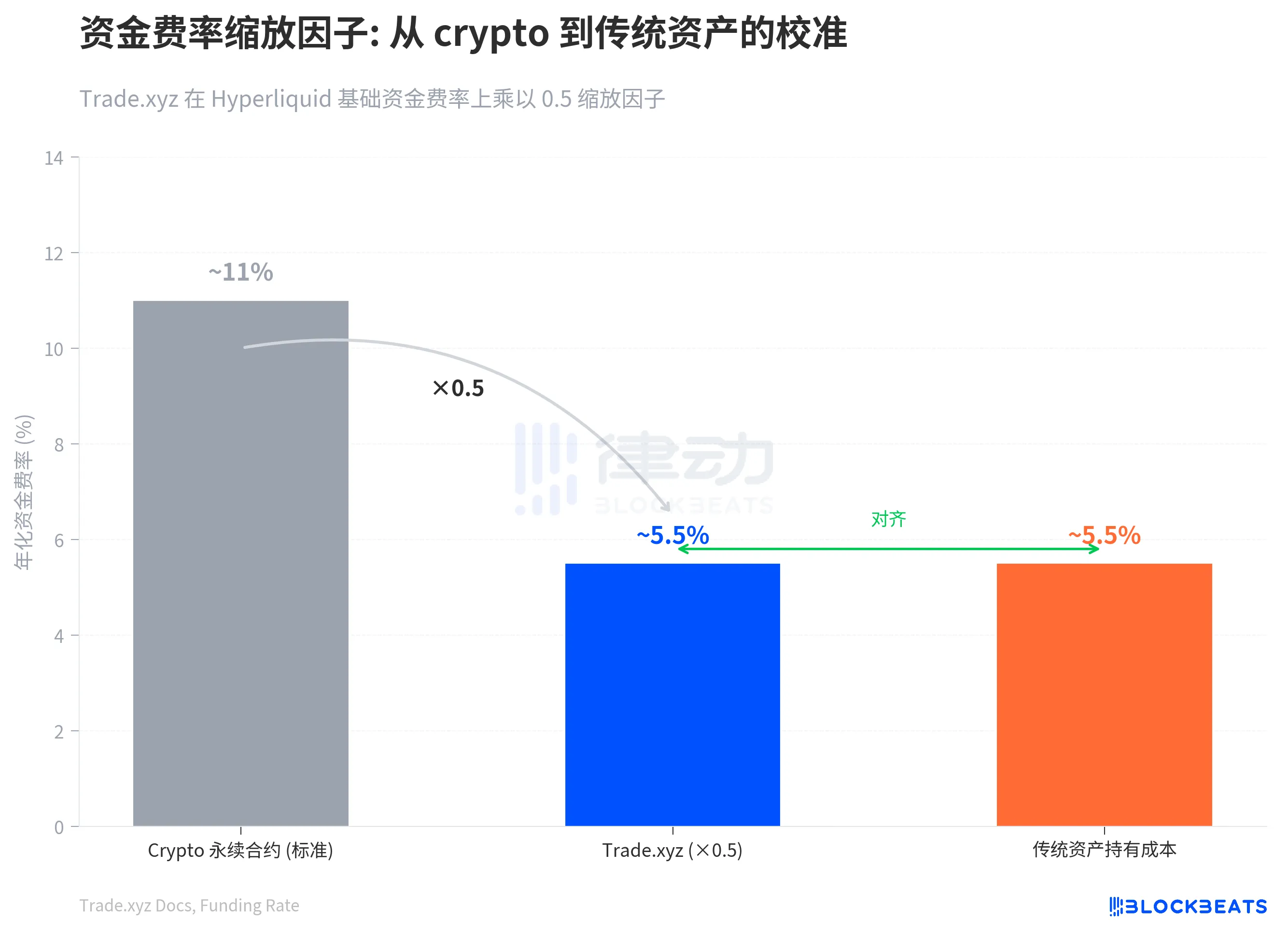

Another key component of the pricing system is the funding rate. The funding rate is the rubber band that ties the perpetual contract price to the oracle price: when the marked price is above the oracle, longs pay shorts; when it is below the oracle, shorts pay longs. tradeXYZ's funding rate formula is similar to that of most crypto exchanges, but it is scaled down by a factor of 0.5.

This 0.5 is a calibration for traditional assets. The basic annual funding rate for crypto perpetual contracts is about 11%, reflecting the pure holding cost of leverage, which is reasonable for assets like Bitcoin with no dividends. But for stocks and commodities, the real holding cost is close to SOFR plus 1 to 2 percentage points, around 5% to 6%. Thus, after being multiplied by 0.5, the basic annualized rate drops from 11% to around 5.5%, aligning with traditional assets. This is particularly crucial over weekends: the scaling factor directly cuts the weekend funding rates in half, working with the oracle's 1-hour time constant, allowing traders with correct directions to retain most of their profits.

Different assets, different handling pipelines

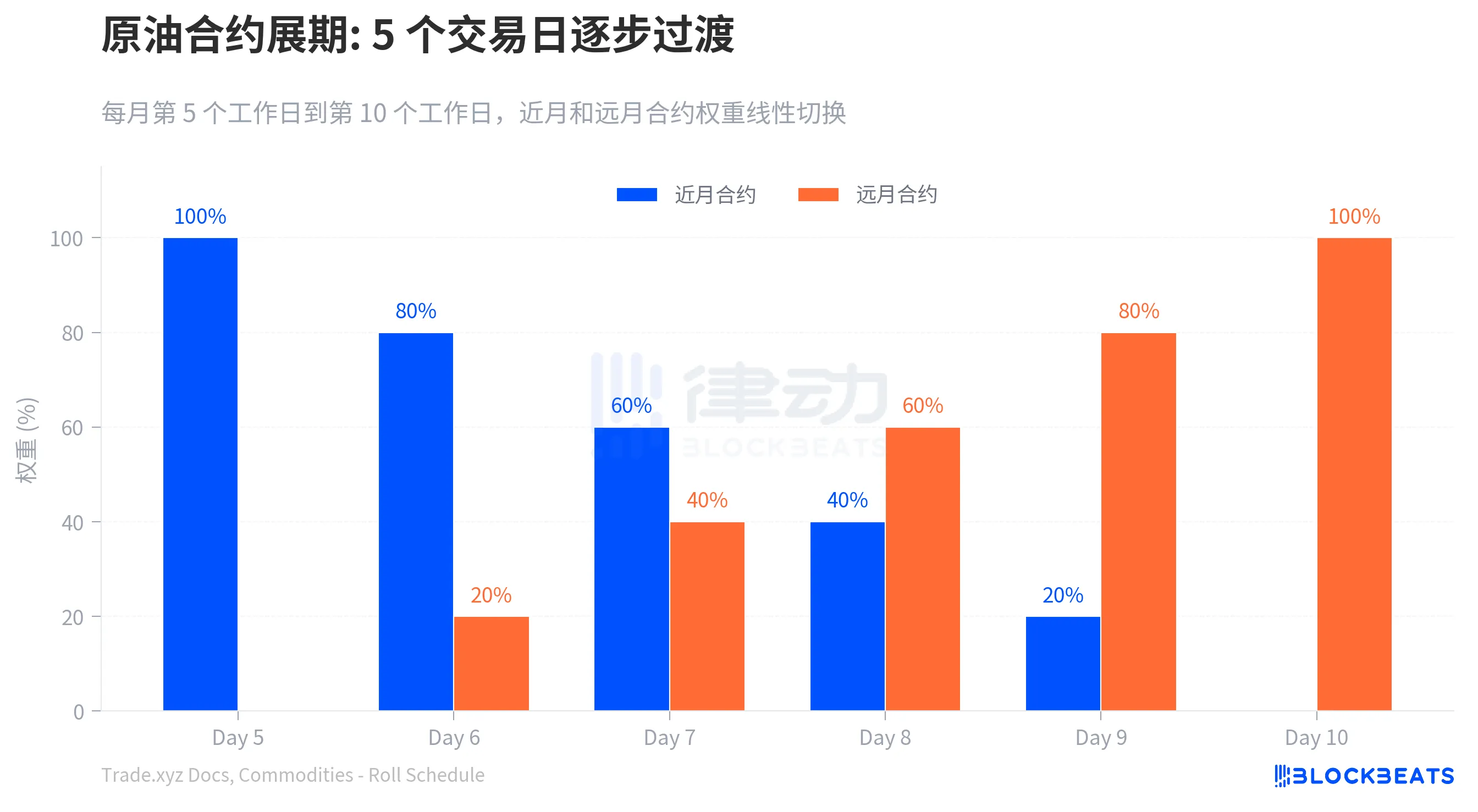

Precious metals have an active global spot market. The external prices of gold, silver, platinum, and palladium are taken directly from spot quotes, with no futures rollover issues. However, crude oil and industrial metals do not have unified spot quotes, so tradeXYZ can only use CME futures contracts as a pricing basis. Futures have expiration dates, so the system needs to switch from the current month's contract to the next month's contract each month. The problem is that the prices of the two contracts are usually not the same. Storage costs and supply-demand expectations can make the prices of the far month contracts higher than those of the near month. If prices jump during the switch, holders' profits and losses may show unreal fluctuations, potentially triggering unintended liquidations.

tradeXYZ's approach is to transition gradually over 5 trading days: from the 5th working day to the 10th working day of each month, the oracle price is the weighted average of the near and far month contracts, with weights changing linearly each day.

The pricing for index contracts is even more complex. XYZ100 tracks the NASDAQ 100, but CME's NASDAQ futures trade almost all day (5 days x 23 hours), providing longer price references than the spot. tradeXYZ initially reversed the futures price to deduce the spot, fixing a 4% discount rate to strip away holding costs. However, when this fixed value is confronted with Fed interest rate hikes, it deviates. The v2 solution launched in February 2026 shifted to dynamic calculations: at the opening of US markets, the spot index value is used directly, while the implied discount rate is back-calculated from the spread between futures and spot; post-market, this discount rate is then used to back-calculate the spot price.

Another special case exists: South Korean stocks. tradeXYZ has listed Samsung Electronics, SK Hynix, and Hyundai Motor, which are priced in Korean won on Korean exchanges. The oracle needs to layer a USD/KRW exchange rate conversion on top of the original quotes. The profits and losses for holders reflect both stock price fluctuations and exchange rate fluctuations.

Who is responsible for the consequences of parameter choices?

All these pricing mechanisms are built on one premise: there are enough market makers willing to continuously provide liquidity. Hyperliquid's HLP liquidity pool provides liquidity for native BTC and ETH perpetual contracts, but does not cover third-party contracts deployed on HIP-3. tradeXYZ's liquidity entirely relies on the voluntary participation of external market makers. In extreme market conditions, if the positions being liquidated cannot find counterparties to take them over, the system does not have the same safety net from the HLP main site, but directly triggers ADL (automatic deleveraging), forcibly liquidating the most profitable counterparty positions in order of profit.

The ingenuity of this pricing system lies in its construction of a self-sufficient pricing environment without external quotes using a set of mutually restraining parameters—oracle tracking speed, boundaries for price discovery, and scaling factors for funding rates. On March 18, the S&P chose to authorize tradeXYZ, potentially seeing this infrastructure as having operated successfully through a genuine geopolitical crisis.

However, this system also comes with its costs. The oracle extracting information from the order book means that during periods of thin liquidity (such as deep night on South Korean stock contracts), a small number of orders can significantly move the oracle. The price discovery boundary v2 expands the liquidatable range over weekends, requiring leveraged traders to reassess their safety margins. ADL means that even if you are correct in your judgment, you may still be forcibly liquidated in extreme markets.

tradeXYZ has chosen a completely different path from traditional exchanges: shifting the pricing power from centralized matching engines to a set of on-chain parameter systems. Traditional exchanges close because clearing, risk control, and market making require human intervention. tradeXYZ cannot close because on-chain contracts do not have the concept of "closing times." It must provide a price at any moment. The crude oil event of March 9 proved this system can operate under pressure. But it also exposed a deep issue: when assigning the pricing functions of traditional financial infrastructure to on-chain protocols, who is responsible for the consequences of parameter choices?

The adjustment of the time constant from 8 hours to 1 hour was a parameter decision made by the tradeXYZ team. The upgrade of the price discovery boundary from v1 to v2 was also such a decision. These decisions affect the liquidation lines and funding rates of every holder. In traditional exchanges, such rule changes require regulatory approval and a public display period. On-chain, a parameter update can be completed in one shot.

In a system that has no HLP safety net, no regulatory arbitration, and relies entirely on parameter design to maintain order, understanding how these parameters impact your position is to understand the true risks you are assuming.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。