This report is written by Tiger Research, February 2026. After the airstrikes in Iran, the price of gold rose while the price of Bitcoin plummeted. Can we still believe Bitcoin is “digital gold”? We will explore the conditions Bitcoin must meet to become “the next gold”.

Key Points

- During every geopolitical crisis, the price of gold rises while the price of Bitcoin falls. In six tests, the claim of "digital gold" has never been validated by data.

- Countries hoard gold but exclude Bitcoin from their reserves. For investors, Bitcoin possesses asymmetry: it falls when stocks fall but does not rise when stocks rise. Three structural asymmetries prevent Bitcoin from obtaining a safe-haven status: surplus derivatives (market structure), dominance of leveraged traders (participant composition), and lack of repeated behavioral records (behavioral accumulation).

- Bitcoin is not a safe-haven asset, but it is a "useful asset in a crisis," capable of functioning when borders are closed and banks fail.

- If these three asymmetries diminish, Bitcoin may cease to be a replica of gold and become a whole new “next-generation gold”. Generational turnover and the widespread application of algorithms are key factors that may accelerate this process.

1. Is Bitcoin Really "Digital Gold"?

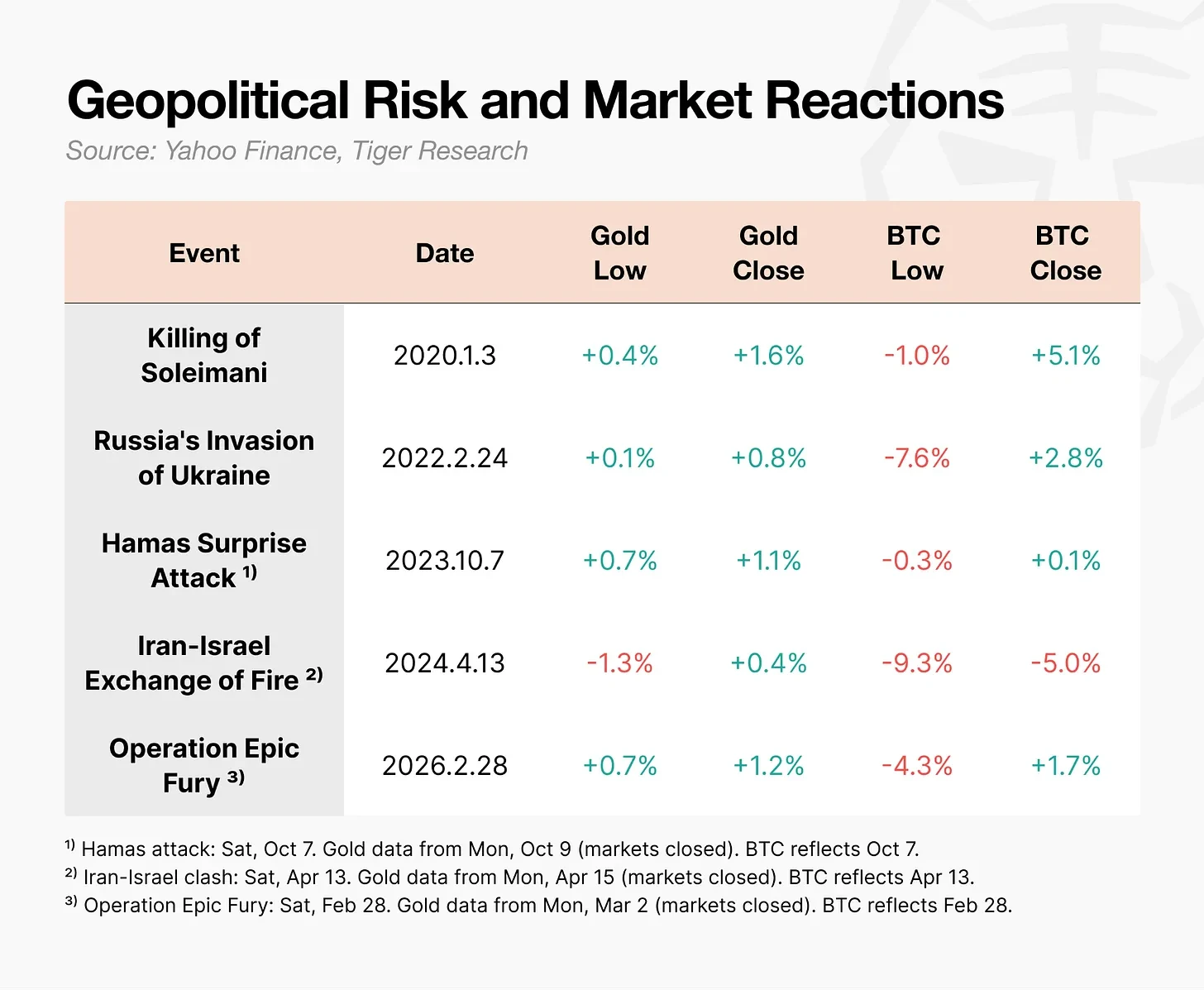

On February 28, 2026, the United States and Israel launched airstrikes against Iran. Following the announcement of the actions, the price of gold surged instantly. In contrast, the price of Bitcoin plummeted to $63,000 that day and then rebounded within a day.

The same event, yet eliciting utterly opposite reactions.

During geopolitical shocks such as war, Bitcoin's trajectory differs from that of gold.

Bitcoin often rebounds quickly after an initial decline, but the forced liquidation triggered by leveraged traders can lead to larger drops. During the Iran-Israel conflict, Bitcoin's intra-day drop reached 9.3%, while during the Ukraine war, it dropped 7.6%. In stark contrast, the price of gold increased during the same periods.

Bitcoin often is the first asset to fall at the outbreak of a crisis; can we truly still call it "digital gold"?

2. Bitcoin is Not "Digital Gold" for Nations or Investors.

Bitcoin was not designed to be "digital gold". Satoshi Nakamoto's white paper released in 2008 was titled “Bitcoin: A Peer-to-Peer Electronic Cash System”. Its starting point was as a transfer mechanism rather than a store of value.

The "digital gold" concept we know today gained popularity during the zero-interest rate and quantitative easing period in 2020. With concerns over currency devaluation peaking, Bitcoin attracted attention as a store of value. However, in practice, neither nations nor investors regard Bitcoin as "digital gold."

2.1. Sovereign Nations: Hoarding Gold, Ignoring Bitcoin

Data from the World Gold Council shows that central banks globally have never ceased to purchase gold annually. However, not a single major central bank has included Bitcoin in its total reserves.

Some might argue that the U.S. formally established a "strategic Bitcoin reserve" through an executive order in March 2025. The text of the order even states, "Bitcoin is often referred to as 'digital gold'." But the specifics are not so. The reserve is limited to assets confiscated through criminal and civil seizure processes. The government is not purchasing new Bitcoin; it only holds confiscated Bitcoin rather than selling it.

It is noteworthy that as the appeal of U.S. government bonds declines, Europe and China are actively purchasing gold, but Bitcoin has not made it onto their alternative shortlists.

2.2 Investors: Falling Together, Not Rising Together

The second half of 2025 is crucial. The Nasdaq index reached an all-time high while Bitcoin plummeted more than 30% from its October peak of $125,000. These two assets began to diverge.

However, the real issue is not the decoupling itself but the direction of movement. Bitcoin falls when the stock market falls but does not rise when the stock market rises. For investors, this is the worst combination. Holding an asset that carries downside risk while missing out on upside potential makes no sense. Bitcoin is far from a safe-haven paradise; even as a risk asset, its allure has been questioned.

3. Why Bitcoin Has Failed to Become "Digital Gold"

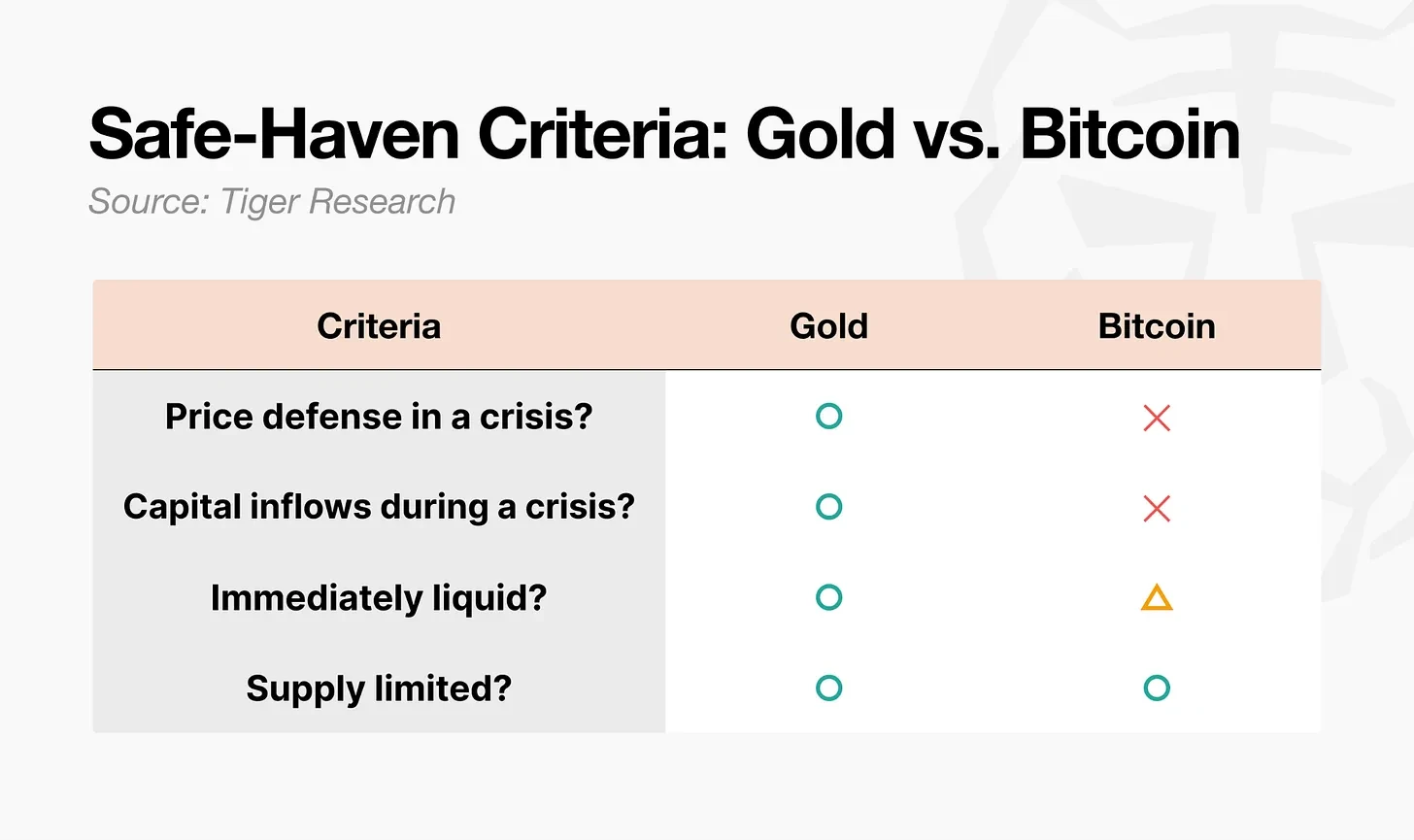

A safe-haven asset is not merely an asset whose price increases. From an academic perspective, it is an asset whose correlation with other assets drops to zero or even becomes negative during extreme economic recessions. The key question is whether its response during a crisis is predictable. By this standard, the gap between gold and Bitcoin is obvious.

Gold meets all four requirements. Bitcoin obviously only meets one: fixed supply. Liquidity is conditional. The other two requirements are unmet. Three structural asymmetries can explain this gap.

- Market Structural Asymmetry: The physical demand for gold supports the price floor, and its futures leverage is relatively low. Bitcoin's derivative trading volume is about 6.5 times its spot trading volume, and its market is traded around the clock, which often leads it to be the first asset sold during crises.

- Participant Asymmetry: Buyers of gold during crises are patient capital such as central banks, pension funds, and sovereign wealth funds. In contrast, the main participants in the Bitcoin market are leveraged traders and hedge funds, which are often the first to withdraw when a crisis erupts.

- Behavioral Accumulation Asymmetry: The pattern of "buying gold during a crisis" has repeated itself for decades, eventually becoming a fixed pattern. Bitcoin requires time to earn the same level of trust.

4. Insecure But Proven Useful

When it comes to safety, it is hard to call Bitcoin "digital gold". Nevertheless, its role in crises is undeniable.

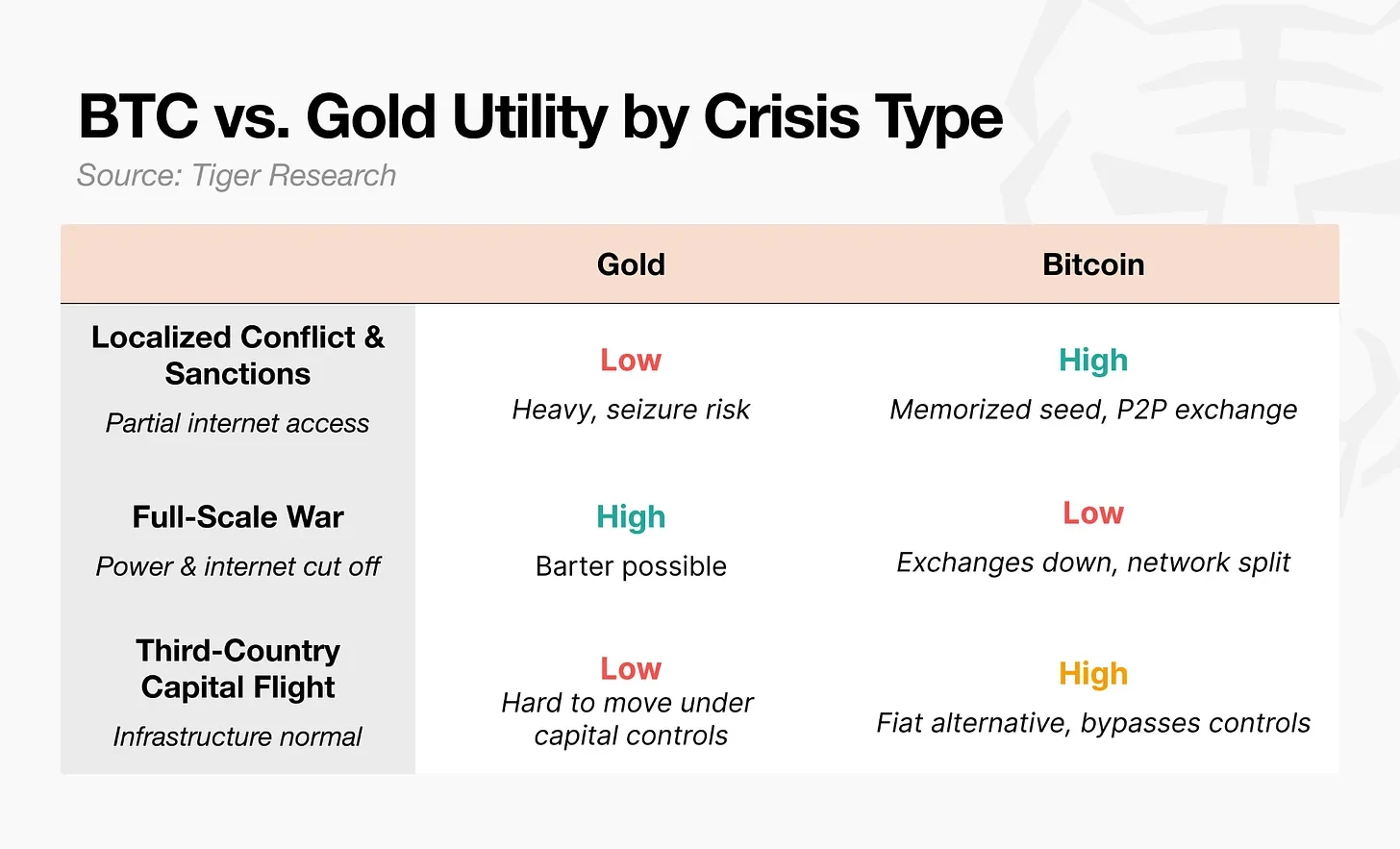

After the outbreak of the Russia-Ukraine war in 2022, the central bank of Ukraine immediately restricted electronic transfers and limited ATM withdrawals. Bank branches were closed, and the public could not even withdraw their own deposits. Some refugees crossed the border carrying USB drives with Bitcoin seed phrases. It was reported that upon arriving in Poland, they exchanged Bitcoin for local currency via Bitcoin ATMs or P2P transactions to cover living expenses.

The United Nations High Commissioner for Refugees went further, distributing stablecoins USDC to displaced individuals and launching a program to allow them to exchange it for local currency at MoneyGram locations. During the “Epic Fury Operation” in 2026, the outflow of funds from Iran’s largest cryptocurrency exchange, Nobitex, surged 700% immediately after the airstrikes.

These cases indicate that people turn to Bitcoin not because it is a safe-haven asset, but because it can be useful when the financial system fails.

In finance, a "safe-haven asset" refers to an asset whose price can remain stable during a crisis. This differs from the concept of an asset that is usable during a crisis. Bitcoin clearly provides functional value for transferring and moving funds during wartime, but it does not guarantee its own price. What constitutes a safe-haven asset is not practicality, but predictability of price behavior. Bitcoin has the former but cannot guarantee the latter.

5. The "Next Generation Gold" Scenario for Bitcoin

In every crisis, Bitcoin's performance is entirely opposite that of gold. Neither nations nor investors have viewed it as "digital gold". However, its utility cannot be overlooked in regions where borders are closed and banks are shut down. Given this potential, if these three major asymmetries are diminished, the path to "next generation gold" will be opened.

5.1 Market Structure Shift

With derivatives trading volume reaching 6.5 times that of spot trading, it triggers chain sell-offs during each crisis. Recently, the volume of open futures contracts has decreased, and the price discovery mechanism shows signs of shifting towards spot and ETFs. But the real test is whether leverage will be rebuilt in the next bull market.

5.2 Participant Shift

After the approval of spot ETFs in 2024, institutional capital poured in, making Bitcoin a mainstream financial asset. However, this has created a paradox: the more institutional investors incorporate Bitcoin into their portfolios, the more readily it is sold off alongside stocks during rising risk aversion. Bitcoin’s accessibility has increased, but its independent price volatility has vanished. This is the paradox of financialization.

Gold ETFs have also become mainstream; however, in crises, gold’s performance moves opposite to stocks because “crisis buying” has been a pattern formed over more than half a century. To break this paradox, the composition of participants must shift from leveraged traders to patient capital.

There is a variable easily overlooked: generational turnover. When Generation Z begins to inherit and manage real wealth, gold may still be a safe haven for their parents. For this generation, their first investment accounts are likely not securities accounts, but cryptocurrency exchanges. For the generation that first encounters assets through Bitcoin, they may instinctively choose Bitcoin over gold when crises occur. This shift in participants might begin not with institutional decisions but with changes in generational behaviors.

5.3 Behavioral Accumulation Shift

After the Nixon shock, it took about 50 years to form the “crisis buying” pattern for gold. Does Bitcoin need the same amount of time? Not necessarily. The recent US-Iran conflict is the sixth test, and the results were again the same: a mid-session plunge followed by a rebound. With the repetition of this pattern, people increasingly believe “it will drop, but it will always rebound.”

The more important variable is algorithms. Nowadays, a large portion of Bitcoin trading volume comes from AI agents and algorithmic trading. If the strategy of “buying Bitcoin during a crisis” is embedded in these algorithms, then this pattern can form without the accumulation of human behavior. In such cases, trust is built on code before it is established among people.

Bitcoin is not yet "digital gold". However, if market structure, participant composition, and behavioral accumulation patterns change on the confirmed utility it possesses, it may become "the next generation gold". It is not a replica of gold but the birth of a completely new category.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。