A life without a bank card, yet suffering from the disease of having one.

Written by: Pavel Paramonov, Founder of the cryptocurrency research institution Hazeflow

Translated by: Eric, Foresight News

My overall argument is that cryptocurrency cards are merely a temporary solution addressing two well-known issues: bringing cryptocurrency to the masses and ensuring that cryptocurrency is globally accepted as a payment method.

Cryptocurrency cards are still cards; if someone truly identifies with the values of cryptocurrency and believes that the future will be dominated by cards, they may need to rethink their vision.

All cryptocurrency card companies will eventually disappear

Cryptocurrency cards are likely to fade away in the long run, but traditional cards will not. Cryptocurrency cards add an extra layer of abstraction: they are not purely cryptocurrency applications, as the issuing institutions are still banks. Yes, they have different branding, designs, and user experiences, but as I mentioned earlier, this is merely a difference in abstraction layers. Abstraction makes it more convenient for end users, but the underlying processes remain the same.

Different L1s and Rollups are obsessed with comparing their TPS and infrastructure to Visa and Mastercard. For years, this has been the industry's goal: to "replace" or, more radically, to "overthrow" the dominance of payment giants like Visa, Mastercard, and American Express.

Cryptocurrency cards cannot achieve this goal—they are not substitutes; rather, they create more value for Visa and Mastercard.

- These traditional institutions remain key gatekeepers, holding absolute power to set rules and define compliance standards;

- Most importantly, they retain the right to block your card, company, or even bank at any time.

Why is this industry, which has always pursued permissionless and decentralized ideals, now handing over all power to payment processors?

- Your card is Visa, not Ethereum;

- Your card is a traditional bank, not a MetaMask wallet;

- You are spending fiat currency, not cryptocurrency.

Most of the cryptocurrency card companies you love are merely slapping a logo on a card. They survive on hype and will disappear in a few years, and the digital cards issued before 2030 will also become unusable.

The latter part of this article will explain how easy it is to create your own cryptocurrency card today, and in the future, you might even be able to issue one yourself.

The same problems + more fees

The best analogy I can think of is Application-Specific Sorting (ASS). Yes, it is indeed cool for applications to autonomously process transactions and profit from them, but this is only temporary: infrastructure costs are decreasing, communication technology is maturing, and the economic issues are actually deeper, not shallower.

(If interested, refer to @mvyletel_jr for an excellent talk on ASS).

The same goes for cryptocurrency credit cards: while they support depositing cryptocurrency and converting it to fiat for spending via the card, centralization and permissioned access remain the crux of the issue.

In the short term, it is indeed convenient: merchants do not need to adopt new payment methods, and cryptocurrency spending is discreet.

But this is merely a transition towards the ultimate goal of cryptocurrency believers:

What is needed: direct payments using stablecoins, Solana, Ethereum, Zcash

What is not needed: indirect payments through USDT → cryptocurrency card → bank → fiat

Each additional layer of abstraction means extra costs: spread fees, withdrawal fees, transfer fees, and sometimes even custody fees. These fees may seem trivial, but do not forget the effect of compounding: every penny saved is a penny earned.

Using a cryptocurrency card does not mean you are bankless or do not need a bank account

Another viewpoint I see is that people believe using a cryptocurrency card means they do not have a bank account or are bankless.

This is clearly inaccurate. There is always a banking institution behind cryptocurrency cards, and that bank is obligated to submit some of your information to the local government—though not all data, at least key information.

If you are a citizen or resident of the EU, the government has access to your bank account interest income, large suspicious transactions, specific investment returns, account balances, and more. If the issuing bank is located in the United States, the range of information the government has will be even broader.

Surprisingly, from a cryptocurrency perspective, this is both beneficial and detrimental.

- The benefit lies in transparency and verifiability, but these rules also apply when using a regular debit or credit card issued by a local bank.

- The downside is that it is neither anonymous nor pseudonymous: banks can still see your name rather than your EVM or SVM address, and you still need to complete KYC verification.

Restrictions still exist

Some may think that cryptocurrency cards are easy to obtain: download the app, complete KYC, wait 1-2 minutes for verification, and deposit cryptocurrency to use. Indeed, this convenience is a killer feature, but not everyone can enjoy it.

Citizens from Russia, Ukraine, Syria, Iraq, Iran, Myanmar, Lebanon, Afghanistan, and most African countries cannot use cryptocurrency for daily spending without residency rights in another country.

But wait, that’s just a dozen or so countries where cryptocurrency cards cannot be used; what about the other 150+ countries? The focus is not on the eligibility of the majority but on the core value of cryptocurrency: equal nodes in a decentralized network, equal financial access, and equal rights for everyone. Cryptocurrency cards fail to embody these values because they are fundamentally not true cryptocurrencies.

Max Karpis incisively analyzed why "neobanks" are doomed to fail (his core argument is that crypto-friendly new banks have no advantage over Revolut, and the moat established by large enterprises at scale cannot be easily shaken by "former employees of big companies"; as long as the giants want, they can open such a bank at any time with a user base in the tens of millions).

For reference, my real experience of paying with cryptocurrency was when booking a flight on Ctrip. They recently added a stablecoin payment option, allowing users to pay directly from their wallets, and of course, this service is open to users worldwide.

What is presented here is a real application scenario of cryptocurrency and an actual payment case. I believe the final form will be like this: wallets will optimize user experience for consumption and payment scenarios, or (less likely) directly evolve into cryptocurrency cards (if crypto payments are widely adopted in some form).

The function of cryptocurrency cards is similar to liquidity bridges

Another interesting phenomenon I have observed is that self-custodied cryptocurrency cards function similarly to cross-chain bridges.

This only applies to self-custodied cards; cards issued by centralized exchanges do not have self-custody features, so exchanges like Coinbase do not need to mislead users by claiming that user funds are controlled by them.

An important use of centralized exchanges (especially the cryptocurrency cards they issue) is to provide reliable proof for government funding verification, visa applications, and other scenarios. When you use a cryptocurrency card linked to a centralized exchange account, you are technically still within the same ecosystem.

Self-custodied cryptocurrency cards are different: their operation resembles a liquidity bridge, where users lock crypto assets on Chain A and unlock funds (fiat) on Chain B (the real world).

This cross-chain mechanism in the realm of cryptocurrency cards is akin to the shovels during the California Gold Rush—it is a valuable secure channel connecting native crypto users with businesses wishing to issue their own cards.

stablewatch insightfully pointed out that these bridges are essentially a "Card as a Service (CaaS)" model—this is the most overlooked core in all discussions about cryptocurrency cards. These CaaS platforms provide the infrastructure for brands to issue their own branded cards.

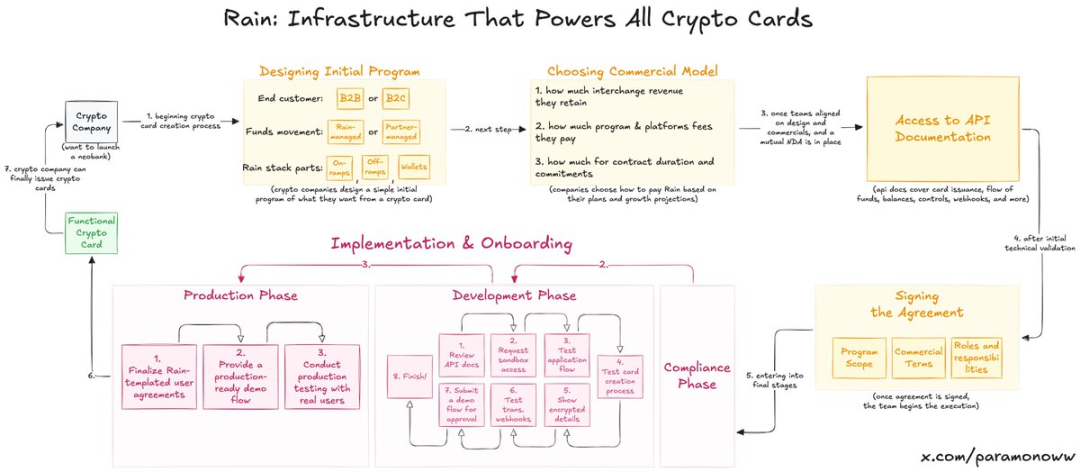

Rain: How cryptocurrency cards come about?

About half of your favorite cryptocurrency cards are likely powered by Rain, a name you may have never heard of. It is one of the foundational protocols in the new banking system, as it carries all the core functionalities behind cryptocurrency cards. Other companies merely need to slap their logos on top (this may sound harsh, but it is quite close to the truth).

Rain enables businesses to easily launch cryptocurrency cards, and frankly, its infrastructure capabilities are even sufficient to continue developing outside the crypto space. So don’t fantasize that teams need to raise tens of millions of dollars to launch cryptocurrency cards—they don’t need that funding; what they need is Rain.

The reason I emphasize Rain repeatedly is that people seriously overestimate the investment required to launch cryptocurrency cards. Perhaps in the future, I will write a separate article discussing Rain, as this technology is indeed severely underestimated.

Cryptocurrency cards lack privacy and anonymity

The lack of privacy and anonymity in cryptocurrency cards is not a flaw of the cards themselves, but rather an issue that those who advocate for cryptocurrency cards deliberately ignore under the guise of so-called "crypto values."

- There are no widely applicable privacy features in the crypto space. Pseudo-privacy (pseudo-anonymity) does exist; we do not see names, only addresses.

- However, if you are ZachXBT, Igor Igamberdiev from Wintermute, Storm from Paradigm, or anyone with strong on-chain analytical capabilities, you can significantly narrow down the ownership of an address.

Of course, the situation with cryptocurrency cards is far from the pseudo-privacy of traditional cryptocurrencies, as you must complete KYC verification when opening a card (in reality, you are not opening a card but rather establishing a bank account).

- If you are in the EU, cryptocurrency card service providers will still submit some data to the government for tax or other governmental purposes.

- Now, you have provided regulators with a new tracking avenue: linking cryptocurrency addresses to real identities.

Personal data will be the currency of the future

Cash still exists (this is the only anonymous payment method unless the seller can see you), and it will circulate for a long time. But everything will eventually be digitized. The current digital systems offer no benefit to consumer privacy: the more you spend, the more transaction fees you incur, in exchange for the other party's deep grasp of your information—what a profitable deal…

Privacy is a luxury, and it will be so in the realm of cryptocurrency cards as well. Interestingly, if we can achieve truly high-quality privacy protection that companies and entities are willing to pay for (not the Facebook model, which requires user consent), in a world dominated by artificial intelligence and devoid of job opportunities, privacy may become one of the currencies of the future, or even the only currency.

If destined to fail, why are Tempo, Arc Plasma, and Stable still building?

The answer is simple: to lock users into the ecosystem.

Most non-custodial cards choose L2 solutions (for example, MetaMask chose Linea) or L1 solutions (for example, Plasma's Plasma Card). Ethereum or Bitcoin are usually not suitable for such operations due to high costs and finality issues. While a few cards use Solana, I do not want to spark a debate here, as its market share remains small.

Companies choose different blockchains not only based on infrastructure considerations but also economic interests.

- MetaMask chose Linea's underlying architecture not because it is the fastest or most secure, but because Linea is part of the ConsenSys ecosystem.

- I specifically used MetaMask as an example because of its adoption of Linea. It is well-known that Linea is hardly noticed and has no chance in the competition against L2 solutions like Base or Arbitrum.

However, ConsenSys made a wise decision by embedding Linea into its product's foundation—users are thus locked into the ecosystem. They gradually form habits through high-quality UX in their daily use. Linea naturally attracts liquidity, trading volume, and various metrics, rather than relying on liquidity mining activities or forcing users to operate cross-chain.

This strategy is similar to Apple's approach when it launched the iPhone in 2007: once users form habits within the iOS ecosystem, it becomes difficult to switch to other systems. Never underestimate the power of habit.

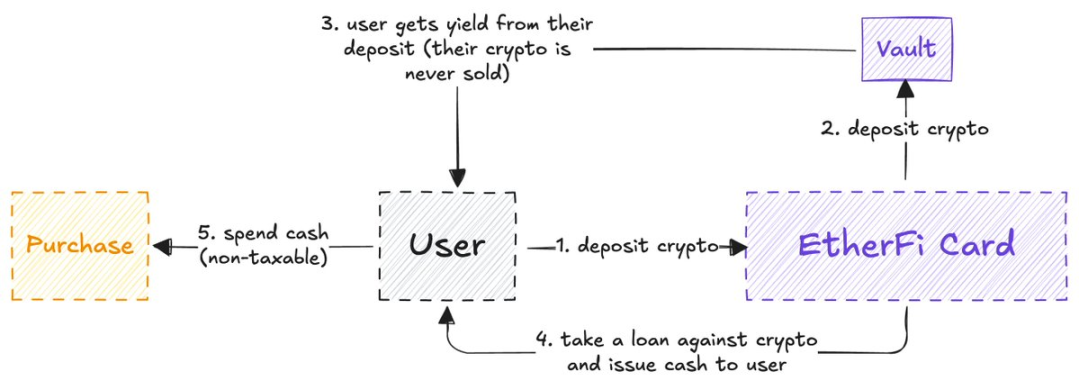

ether.fi may offer the only viable solution

After deep consideration, I conclude that Etherfi may be the only cryptocurrency card that truly aligns with the spirit of crypto (this research is not sponsored by EtherFi, and even if it were, it wouldn't matter).

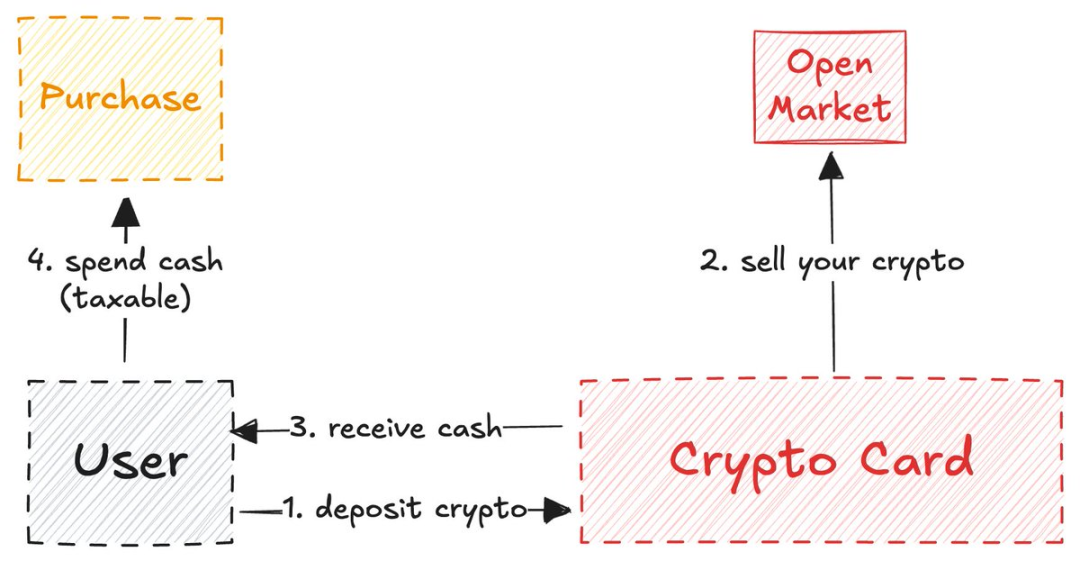

Most cryptocurrency cards sell the crypto assets deposited by users and then use cash to top up account balances (similar to the liquidity bridge mechanism I described earlier).

The model of ether.fi is different: the system will never sell your cryptocurrency; they provide cash in the form of loans and use your cryptocurrency to generate returns.

The operation of ether.fi is similar to Aave. While most DeFi users are still dreaming of seamlessly mortgaging crypto assets for cash loans, this service has already been realized. You might question, "Isn't this the same functionality? I can already deposit cryptocurrency and use a cryptocurrency card as a regular debit card, so why go through all this?"

The issue is that selling cryptocurrency is a taxable event, and sometimes it is even easier to be taxed than regular consumption. Most cryptocurrency cards will tax each transaction, so you end up paying more taxes to the government (again, using a cryptocurrency card does not mean escaping the banking system).

ether.fi cleverly avoids this issue—you are not actually selling crypto assets; you are using them as collateral to obtain a loan. With this feature alone (along with zero fees for USD, cashback, and multiple benefits), ether.fi has become the best example of the fusion of DeFi and traditional finance.

While most cryptocurrency credit cards try to disguise themselves as liquidity bridges, ether.fi genuinely prioritizes crypto users rather than focusing on promoting cryptocurrency to the masses: they allow local residents to access cryptocurrency and guide them to spend in front of the public until the masses realize the coolness of this spending method. Among all cryptocurrency cards, ether.fi may be the only survivor that can withstand the test of time.

I like to view cryptocurrency cards as an experimental field, but unfortunately, most teams merely exploit the narrative hype without giving due recognition to the underlying systems and developers. Let us wait and see where progress and innovation will lead us. Currently, cryptocurrency cards show a significant trend of globalization (horizontal expansion) but lack the necessary vertical development, which is crucial for the early stages of consumer technology like cryptocurrency cards.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。