文章作者:May P、Janus R

文章来源:CoinFound

Takeaway

- USDT 评级下调与争议:USDT 储备中非锚定资产(BTC 与 黄金 等)占⽐已达约 24%,加上治理与透明度不⾜,使其在传统⾦融框架下被视为风险提升,导致评级下调。USDT 评级的下调引发争议。

- Tether 大幅增加黄金与⽐特币⽐例:出于通胀对冲、资产多元化、降低美元单一暴露、提升收益等⽬的,Tether 近年来不断增加黄金与⽐特币储备比例。

- 标普与 Tether 的分歧本质:传统金融的风险认知是「兑付能力优先」,关注「极端挤兑下的储备变现能力」;而 Tether 关注的是「市场流动性优先」与长期的保值抗风险能力(特别是通胀风险)。二者衡量风险的维度完全不同。

- Tether 储备转型的战略意图:Tether 储备模式从「1:1」现金等价物储备转向「硬资产(黄金)+ 数字资产(BTC)+ 低风险资产(美债)」混合模式。本质上,这是从「稳定币发行方」向「全球流动性提供商 + 数字资产储备机构」的转型,核心驱动力包括通胀对冲需求、顺周期收益增厚(例如预测中的 2025 年 BTC/黄金牛市)以及去美元化布局。事实上,Tether 正在变得更像「影⼦央⾏」⽽⾮简单稳定币发⾏⽅。

- 当前评级体系的局限:标普的「稳定性评级」覆盖「兑付风险」,无法回应投资者对 Tether「资产增值能力」、「周期韧性」的需求。未来市场上或许需要更多维度的风险评级信息,此外,或许需要「稳定性评级(监管 + 偿付)+ 投资风险评级(收益 + 周期)」的双框架模式,以衔接传统与加密金融的风险认知。

- USDT 短期风险与长期趋势:USDT 的锚定稳定性仍由链上流动性支撑。但是,短期来看,储备中 24% 的高波动资产(BTC/黄金/贷款)或将在 2026 年降息周期与潜在加密熊市中暴露风险(2025 年 Tether 账面因持有黄金和比特币储备出现巨额浮盈,然而,2026 年情况或发生变化)。长期来看,稳定币的「央行化」趋势(抗通胀资产 + 全球网络 + 能源)将推动行业向「透明化 + 标准化」演进。

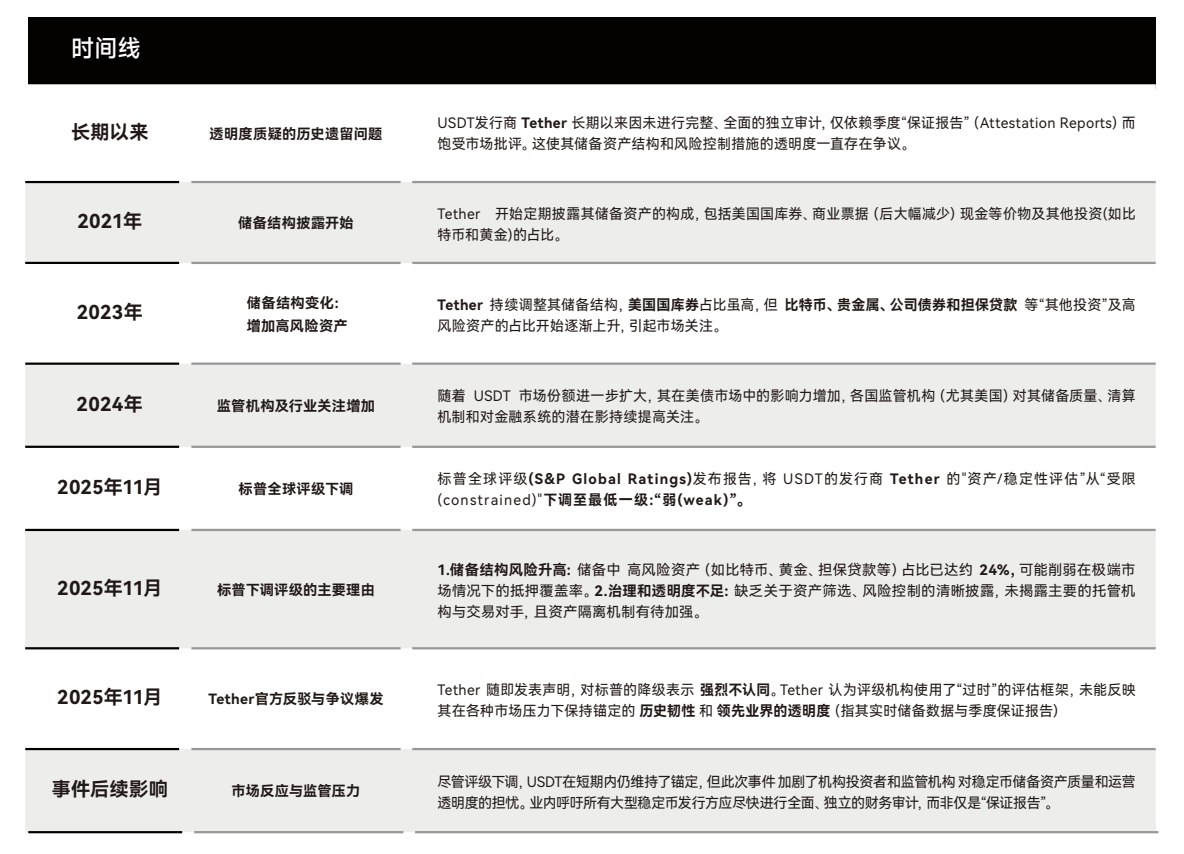

1. 事件回顾:标普下调 USDT 评级的争议与本质

1.1 事件时间线与核心矛盾

2025 年 11 月,标普全球将 USDT 的「资产/稳定性评估」从「受限(constrained)」下调至「弱(weak)」,核心理由有二:

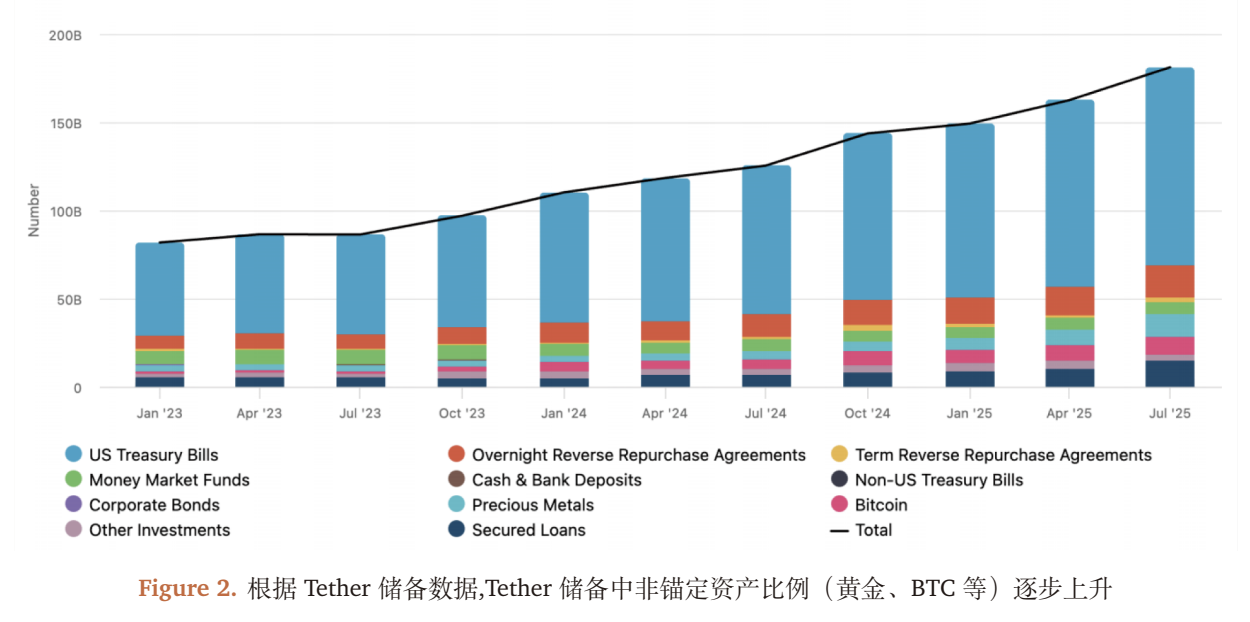

- 储备结构风险:Tether 的储备中高波动资产(BTC、黄金、贷款等)占比已达 24%(2023 年仅 12%),此类资产在「恐慌挤兑」场景下无法快速变现;

- 治理透明度不足:未披露主要托管机构、链上抵押隔离机制细节,且仅提供「季度保证报告」而非完整独立审计。

Tether 的反击则聚焦「市场实际表现」,并对来自于传统金融体系的评级方法提出质疑:

- 历史韧性:USDT 在 2022 年 FTX 倒闭、2023 年硅谷银行危机、2024 年加密监管收紧等 8 次极端事件中均保持锚定;

- 透明度领先:自 2021 年起提供「实时储备数据」(链上地址可查),季度保证报告覆盖 95% 以上资产,优于部分传统货币基金。

(图表 1:USDT 评级下调事件回顾)

1.2 分歧的本质:两种风险衡量体系的碰撞

2025 年 11 月,标普全球(S&P Global Ratings)将 USDT 的稳定性评估下调至最低一级「弱(weak)」。Tether 随即公开反击,指责标普「沿用旧世界的框架」,忽视了 USDT 在过去十年间经受的多次极端压力测试。这场争论,不只是一次评级争议,而是两种金融文明的正面碰撞。

- 标普代表的是:「监管 - 资本充足 - 偿付能力」体系

- Tether 代表的是:「市场流动性 - 全球交易需求 - 链上即时清算」体系

- 这两者衡量风险的方式根本不同,因此注定无法达成共识。标普与 Tether 的争论,表面上是一次「稳定性评级」的口水战,但本质上是两个世界对风险的理解方式完全不同。

- 标普和 Tether, 一个来自 100 年的传统金融,一个来自 10 年的链上高频市场。标普用的是「央行—银行—货币市场基金」的逻辑;Tether 依赖的是「链上流动性—永续杠杆—保险基金—自动清算」的逻辑。

而 Tether 代表的逻辑,是传统金融市场目前无法采用的。

1.3 标普看到的是:传统金融的兑付逻辑

在传统金融的认知框架中,所有「承诺兑付 1:1 的工具」(货币基金、商业银行、稳定币)必须满足两个硬条件:

1. 储备资产必须高度安全、可立即变现:标普在其报告中指出:Tether 储备中 BTC、黄金、贷款类资产占比已超过 20%,这些资产波动大、清算周期长,在「恐慌挤兑」场景中可能无法以面值快速抛售。

2. 治理结构必须透明、托管安排必须可穿透:标普认为 Tether 的托管人信息、链上抵押隔离、风险披露仍不充分。

也就是说,在标普的世界里:一个「稳定币」的关键风险,在于该稳定币能不能在所有人一瞬间来兑付的时候撑住?这就是传统体系的兑付稳定性(redeemability)。

1.4 Tether 坚持的是:加密世界的流动性逻辑

如果说 TradFi 的稳定性来自「储备够不够、够不够快、够不够安全」,那么 Tether 的稳定性则来自「我是否能在链上保持巨额流动性、永续市场的风险能否被吸收、二级市场是否能维持价格锚定」。换句话说

- TradFi 测的稳定性是兑付能力,而 Crypto 测的稳定性是市场流动性 + 清算稳定性。

- 而 Tether 的十年记录(包括多次恐慌行情)确实显示:USDT 的脱锚往往不是因为「储备不足」,而是因为「二级市场流动性短时失衡」,而这每次都被迅速修复。

Tether 为什么强烈反击?因为它坚持的是另一套「市场逻辑」。Tether 的回应强调三个点:

1. USDT 已在所有极端情绪下保持 1:1 锚定:包括多次加密交易所倒闭、美联储快速加息周期、监管收紧、银行挤兑事件等。从 Tether 的角度「我不是理论上稳定,而是实际运行十年从不脱锚。稳定币的真实评级是市场每天给的,而不是模型给的。」

2. 实时储备数据 + 季度证明报告足够透明:Tether 认为它已经优于 TradFi 某些影子银行或 MMF。但标普并不认可「实时网页披露」这种形式,因为标普的方法论认为「未经审计的透明、可信的透明」。

3. BTC/黄金是「抗通胀资产 + 战略储备」,而非高风险暴露:2025 年 BTC 和黄金大涨,让 Tether 获得巨大账面收益(超过 100 亿美元)。这使 Tether 实际上形成了一种「硬资产 + 美债 + 贷款 + 数字资产」的混合央行式模型。Tether 的世界观是「我就像一个国家的央行储备,我的结构不是传统美元体系,而是新全球资产篮子。」但标普的世界观是「你不是央行,你只是一个承诺 1:1 兑付的代币发行方。」

1.5 为什么双方对「风险」的理解完全冲突?

它揭示了一个关键事实:加密市场与 TradFi 在风险承担逻辑上完全不同。

- Arthur Hayes 在 11 月 27 日发表了一篇关于永续合约的文章,永续合约就是一个能充分体现传统金融和加密金融目前无法融合的一个典型例子。在传统金融(TradFi)里,远期合约风险来自「无限追缴责任」。在 TradFi 中,清算不及时、仓位穿仓、投资者亏到负数,需要继续补钱(Margin Call),甚至会动用全部个人资产偿债。所以 TradFi 必须要求储备「极高质量资产」,任何波动都不行。

- 但在加密金融(Crypto)里,风险由「保险基金 + 自动强平 + ADL」承担。这是因为在加密永续合约中,亏损不由交易者承担无限责任。加密金融的体系里,清算盈余补充保险基金、强平手续费注入保险基金、ADL(自动减仓)兜底、交易所自有资金补充。最终结果是加密用户最多亏掉保证金,但不会欠债。所以加密市场更能接受高波动资产,因为有市场结构兜底。

这就是标普与 Tether 分歧的本质:标普测量的是 TradFi 的风险,即「如果所有人都来挤兑,你能不能兑得出来?」Tether 应对的则是 Crypto 的风险,即在 7 x 24 高波动市场,我能不能保证交易、流动性和全球高频使用?两者不是一个维度的衡量体系。

2. Tether 的储备转型:从「稳定币」到「影子央行」的战略逻辑

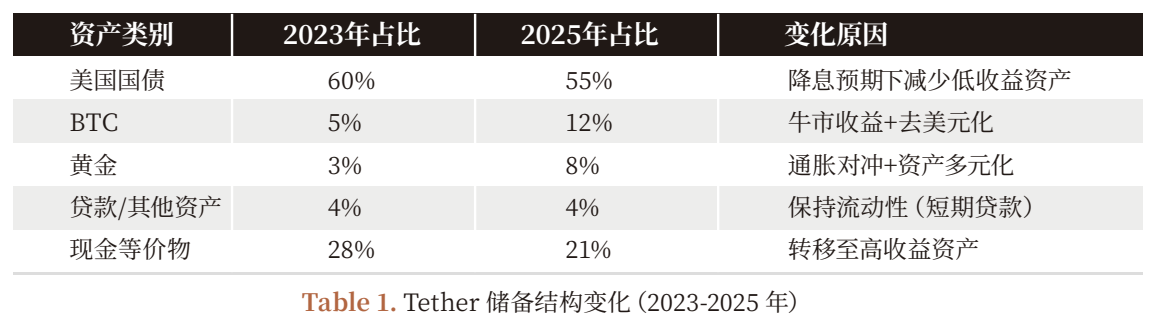

2.1 储备结构的时间序列变化(2023-2025 年)

2.2 为什么增加 BTC、黄金比例?顺周期收益与长期战略的平衡

Tether 的储备结构转型(2023-2025 年)并非随机,而是「收益 - 风险 - 战略」的三重考量:

1. 通胀对冲需求:2022-2024 年美联储加息导致美元购买力下降(美国 CPI 从 2% 升至 8%),黄金(传统通胀对冲工具)与 BTC(数字黄金)成为对冲通胀的核心资产;

2. 顺周期收益增厚:2025 年 BTC 价格从 4 万美元涨至 6.5 万美元(涨幅 62.5%)、黄金从 1900 美元/盎司涨至 2500 美元/盎司(涨幅 $31.6%),Tether 的未实现浮盈占 2025 年前九月净利润(100 亿美元)的 70%(国债利息仅贡献 30 亿美元);

3. 去美元化布局:Tether 的美元储备占比从 2023 年的 75% 降至 2025 年的 55%,通过增加黄金、BTC 的占比,降低对美元单一资产的暴露(应对美国债务上限危机、全球去美元化趋势)。

2.3 利润结构的「甜蜜与隐患」:顺周期下的风险

Tether 的 2025 年业绩(前九月净利润超 100 亿)看似亮眼,但其利润结构高度依赖「牛市周期」:

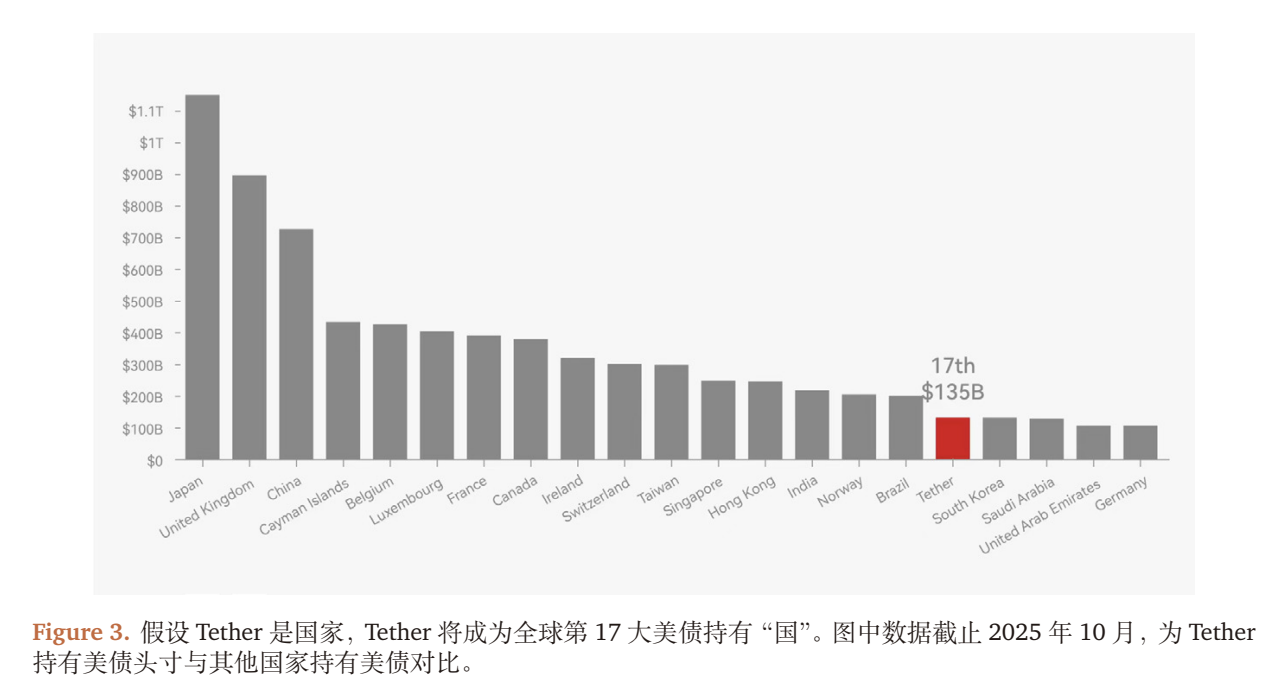

- 稳定收益:约 1350 亿美元美国国债的利息收入(2025 年美债 1 年期收益率约 2.2%),贡献约 30 亿美元;

- 浮动收益:BTC(约 10 万枚)与黄金(约 1000 万盎司)的未实现收益,贡献约 70 亿美元(对应 BTC 涨 2.5 万美元/枚、黄金涨 600 美元/盎司)。

风险传导机制:

- 若 2026 年美联储降息 25bp(市场共识),Tether 的国债利息收入将减少 $3.25 亿美元/年 ($1350 亿 * 0.25%);

- 若 BTC 价格下跌 20%(回归 5.2 万美元),黄金下跌 10%(回归 2250 美元/盎司),Tether 的未实现浮盈将缩水约 25 亿美元(BTC 减值 2.5 亿美元 + 黄金减值 25 亿美元);

- 若加密市场进入熊市(如 2022 年),稳定币发行量收缩(2022 年 USDT 发行量从 800 亿降至 600 亿),Tether 的国债持仓规模将减少,进一步压缩利息收入。

2.4 战略转型的终极目标:从「稳定币」到「影子央行」

我们通过跟踪 Tether 的链上地址与业务布局发现,其已超越「稳定币发行方」的定位,正在构建「抗通胀资产储备 + 全球稳定币发行 + 链上分销网络 + 能源」的「影子央行」体系:

- 抗通胀资产储备:BTC、黄金占比 $24%,对应「央行的外汇储备」;

- 全球稳定币发行:USDT 在 150 国家的链上交易量占稳定币总交易量的 70%,对应「央行的法币发行」;

- 链上分销网络:与 Binance、Uniswap 等 200+ 交易所/DeFi 协议合作,实现 USDT 的全球即时转账;

- 能源布局:投资 10 亿美元于比特币矿场(2025 年算力占全球 5%),对冲 BTC 挖矿的能源成本。

2.5 市场表现:USDT 的锚定稳定性与流动性

- 锚定偏差:2023-2025 年,USDT 的价格偏差(与美元的价差)平均仅 0.02%,远低于 USDC(0.05%)、DAI(0.1%);

- 链上流动性:USDT 在 Uniswap V3 的流动性池规模达 50$ 亿美元(2023 年仅 10 亿),做市商的报价点差(Spread)稳定在 0.01% 以内;

- 机构持有量:2025 年机构持有 USDT 的比例从 2023 年的 15% 升至 30%,说明机构已将 USDT 视为「兼具流动性与资产增值的组合工具(而非纯稳定币)。

3. 未来展望:稳定币评级体系的进化方向

3.1 当前评级体系的局限:仅覆盖兑付风险

标普的稳定性评级解决了稳定币能否兑付的问题,但无法回应机构投资者的核心需求:

- 收益质量:Tether 的利润是否可持续?(如国债降息后的收益下滑)

- 敞口风险:BTC、黄金的占比是否过高?(如 BTC 下跌 $20\%$ 对储备的影响)

- 经营风险:Tether 的治理是否透明?(如托管资产的安全性)

3.2 超越当前评级体系

未来,加密市场或许需要更完善的评级体系,不仅仅关注到兑付和稳定性。未来,可能需要的评级设计或如下

稳定性评级(现有框架的升级)

- 核心指标:储备资产的「安全系数」(现金等价物占比)、「流动性系数」(高波动资产的清算周期)、「透明度系数」(独立审计覆盖率、托管信息披露);

- 目标:回答「稳定币能否在极端挤兑下保持兑付」的问题。

投资风险评级(新增框架)

核心指标:

- 收益质量:稳定收益(国债利息)占比(>=50% 为「低风险」);

- 敞口管理:高波动资产占比(=10% 为「低风险」);

- 经营风险:发行方的利润增长率(>=10% 为「稳定」)、监管合规性(如美国 MSB 牌照、欧盟 MiCA 认证);

- 目标:回答“稳定币的发行方能否持续经营,其储备资产能否增值”的问题。

3.3 行业趋势:从「争议」到「标准」

此次标普与 Tether 的争议,本质是传统金融向加密市场的「规则输出」。我们判断:

- 短期:监管将推动稳定币的「透明化强制要求」(如美国《稳定币法案》要求 100% 现金等价物储备,欧盟 MiCA 要求完整审计);

- 中期:评级体系将获得发展,评级也不局限于「监管—资本充足—偿付能力」体系。机构投资者会根据「稳定性评级 + 投资风险评级」在不同场景下稳定币;

- 长期:稳定币或许进一步分化为「纯稳定工具」(如 USDC,100% 现金等价物)与「兼具增值的稳定工具」(如 USDT,混合储备),满足不同投资者需求。

风险提示

1. 储备资产价格波动风险:BTC、黄金价格下跌将导致 Tether 的储备减值,影响兑付信心;

2. 监管政策风险:若美国、欧盟要求稳定币持有 100% 现金等价物,Tether 需抛售 BTC、黄金,导致利润大幅下滑;

3. 市场流动性风险:极端市场情况下(如 2022 年 FTX 倒闭),链上流动性枯竭可能导致 USDT 脱锚;

4. 经营管理风险:Tether 的治理透明度不足,可能引发内部操作风险(如托管资产被盗)。

《USDT评级风波》研报下载链接:https://app.coinfound.org/research/1

Website:https://dataseek.coinfound.org/

X: https://x.com/CoinfoundGroup

分析师声明:本报告基于公开信息与合理假设,不构成投资建议。分析师未持有 Tether 或 USDT 的头寸。

版权声明:本报告版权归 Coinfound 所有。

关于 CoinFound

CoinFound 是一家面向机构与专业投资者的 TradFi Crypto 数据科技公司,提供 RWA 资产数据终端、RWA 资产评级、Web3 风险关系图谱、AI 分析工具及定制化数据等服务。从数据整合、风险识别到决策辅助,帮助机构以更低成本、更高效率获取关键情报并转化为可执行洞察,构建全球 RWA 底层基础设施。

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。