Original | Odaily Planet Daily (@OdailyChina)

According to the Financial Times, the crypto trading platform Bullish has recently submitted a confidential initial public offering (IPO) application to the U.S. Securities and Exchange Commission (SEC). For users outside the industry, the name of this exchange may not be very familiar, but within the crypto sector, it has significant backing: Bullish is the parent company of the well-known crypto media CoinDesk, and is supported by Block.one, the company that led the development of the EOS project. As a result, after the IPO application news was announced, the price of EOS (now called A) surged by more than 17%.

However, this is not Bullish's first attempt to enter the capital market. As early as 2021, it attempted to go public through a SPAC (Special Purpose Acquisition Company) merger, but ultimately failed due to multiple factors. This time around, Bullish is not taking shortcuts; instead, it has chosen a more lengthy but safer traditional registration process. It is no longer betting on short-term opportunity windows but is trying to become a player that can survive in the market for the long term.

So, how did this exchange, which has had numerous connections with EOS and has always been low-key in the industry, step by step reach the doorstep of an IPO?

From SPAC Setback to Strategic Restart: Bullish Hits the "Pause" Button

Back in 2021, Bullish announced it would merge with Far Peak Acquisition Corp, planning to go public via SPAC at a valuation of up to $9 billion. This plan was driven by Bullish's current CEO Tom Farley.

Farley is not an outsider; his professional experience has set the tone for Bullish's eventual alignment with regulatory standards. He previously served as the president of the New York Stock Exchange (NYSE), where he promoted several reforms, including the Bitcoin index and early investments in Coinbase. He later worked for the Intercontinental Exchange (ICE) for many years, deeply involved in the integration of the NYSE, and is one of the few figures in traditional finance who understands the "logic of digital assets."

After leaving the NYSE, Farley entered the SPAC arena, founding two shell companies, Far Point and Far Peak. Far Point successfully facilitated the listing of Global Blue in 2020, while Far Peak became the launchpad for Bullish.

However, plans changed. In 2022, the overall crypto market cooled, the SEC tightened its scrutiny of SPACs, and the market contracted due to the Federal Reserve's interest rate hikes. Ultimately, Bullish announced the termination of its merger with Far Peak at the end of that year. Despite the failed transaction, Farley and some members of the Far Peak management team chose to stay, and Bullish did not withdraw but sought other new paths.

No Longer Chasing Trends, Bullish Chooses to "Slow Down"

Bullish launched in May 2021, coinciding with a period of flourishing crypto trading platforms. At that time, whether it was NFTs, GameFi, or platform token incentives, exchanges were competing for users and popularity. But Bullish took a different path.

It does not have a platform token, nor does it engage in incentive activities; the number of crypto trading pairs it supports is just over a hundred, most of which are settled in USDC. Clearly, Bullish has been more concerned with the stability of the platform and its regulatory friendliness from the very beginning, rather than the market's popularity.

While many platforms were scrambling to "roll" users and trading volume, it never emphasized that it was a new entry point for the masses, nor did it create much noise on social media. In hindsight, it was not that it did not understand; rather, it was engaged in a slow and structured self-shaping: an "atypical" crypto platform trying to become a "typical" financial institution.

Born with a "Golden Key," Yet Sparking Community Controversy

Unlike many crypto startups that started from scratch, Bullish had a very high starting point. Its parent company Block.one invested generously, providing $100 million in cash, 164,000 bitcoins (valued at approximately $9.7 billion at the time), and 20 million EOS as startup capital. This was followed by $300 million in external financing, with investors including PayPal co-founder Peter Thiel, hedge fund mogul Alan Howard, and crypto veteran Mike Novogratz.

Thus, although Bullish does not have the brand recognition of established exchanges like Coinbase and Kraken, its financial strength is not lacking, and it does not need to rely on user growth or high-frequency trading to maintain basic operations. Therefore, it has enough "time" to wait for the door to compliance to open.

But problems also arose: although Bullish's funding, technology, and brand are deeply connected to EOS, it has "drawn a line" with EOS in terms of product, direction, and positioning, as if the two had never intersected.

However, the EOS community is well aware that the startup capital, resources, and influence used by this new exchange almost all stem from their initial investment and trust.

From "Blockchain 3.0" to Community Split: EOS's Unfulfilled Dream

EOS was once one of the hottest projects in the crypto world. Launched in 2017, it was hailed as "Blockchain 3.0" and the "Ethereum Killer," led by genius developer BM (Daniel Larimer) for technology, with Block.one responsible for financing and commercialization. Over the course of a year, EOS completed an ICO that raised as much as $4.2 billion, becoming one of the most sensational cases in crypto financing history.

It was a time when idealists and early investors flocked in. The community provided EOS with technical support, public relations resources, and faith endorsement, while Block.one, as the project's parent company, promised to use the funds raised for ecological construction, supporting developers, improving governance structures, and attracting applications.

However, these promises were rarely fulfilled later on. Although the EOS mainnet was successfully launched, it frequently stalled in ecological development: inefficient node operations, high development thresholds, poor user experience, and almost zero incentives for developers from Block.one. Coupled with BM's departure and issues of "familial" internal management, community trust gradually eroded.

Ultimately, at the end of 2021, the EOS Network Foundation (ENF) and multiple nodes initiated a "governance uprising," attempting to negotiate with Block.one to return funds, restore domain names, and transfer governance rights. After negotiations failed, they proposed governance proposals, ultimately achieving on-chain voting to remove Block.one's governance rights.

Although governance liquidation has become a reality, the right to use funds still remains with Block.one, and the legal disputes between the two parties remain unresolved to this day. This has become an unhealed wound for the EOS community.

Zooming out, it's not just EOS; the once "Ethereum Killers," and even Ethereum itself, have not fared well amid the rampant "inflation" of underlying public chains.

Returning to the Mainstream Capital Market, Bullish's "Compliance Narrative"

Now, Bullish has resubmitted its IPO application to the SEC. This time, it has avoided the "fast track" of SPACs and instead returned to the traditional review process, attempting to "restore" itself to a form familiar to traditional financial institutions: clear logic, defined paths, stable structure, and using compliance language to narrate its role in the crypto world.

This reflects a clear signal: it no longer wants to rely on seizing "market opportunities" to rise but is more willing to take root through "structured operations." Its story is no longer just Bullish's attempt but represents the crypto industry's new understanding of "sustainability."

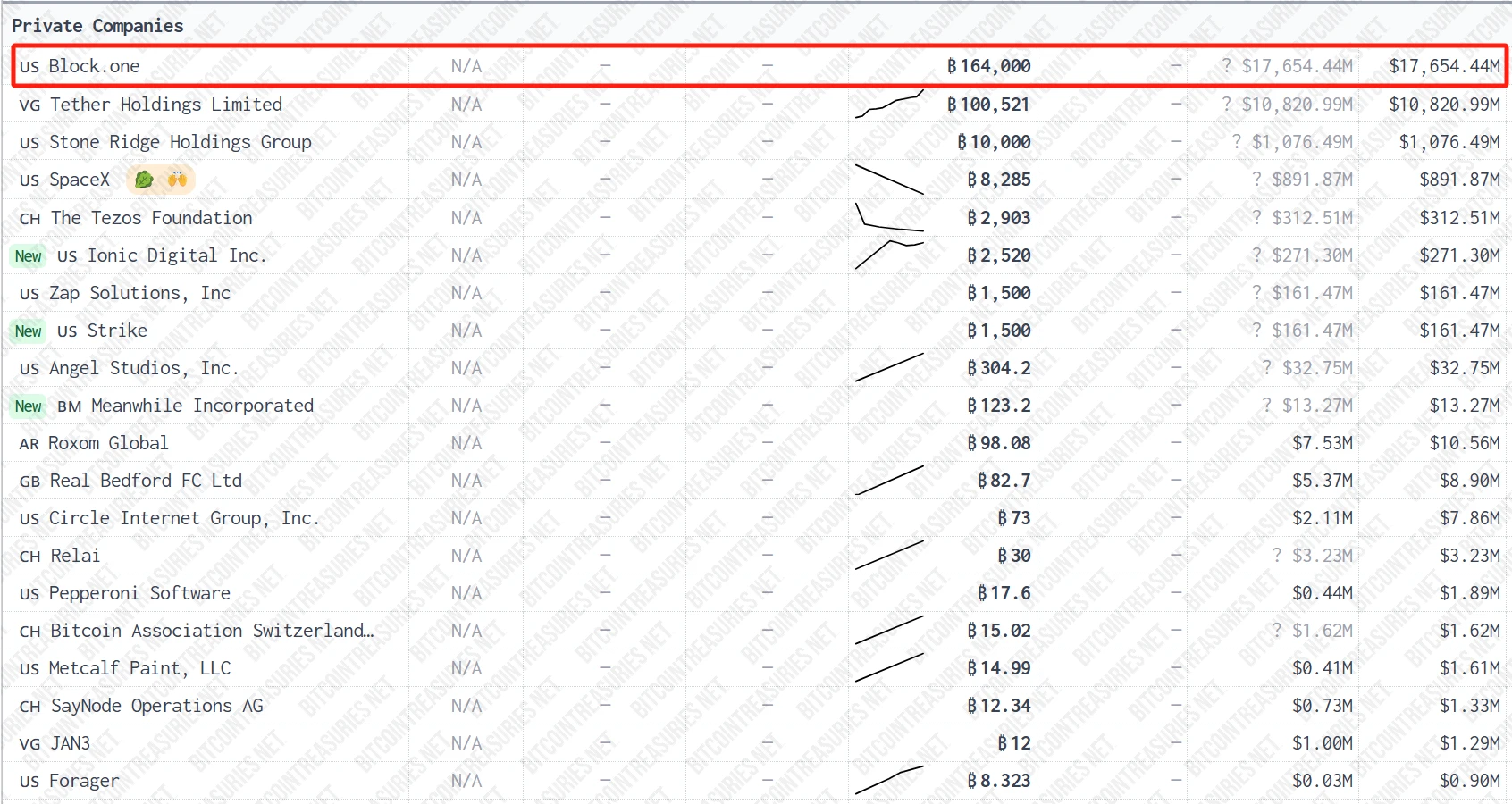

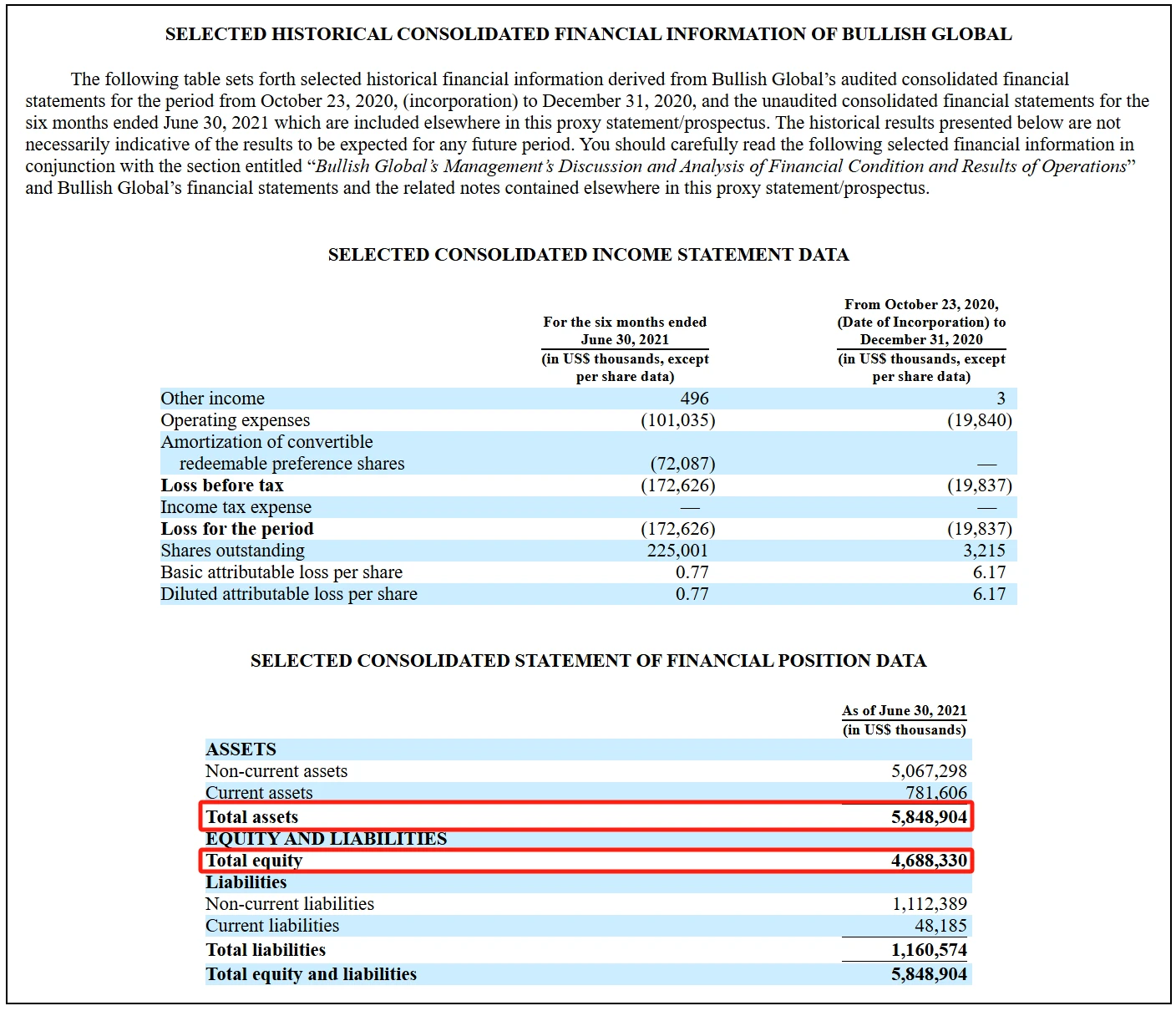

According to bitcointreasuries data, as of now, Block.one still holds 164,000 bitcoins (valued at over $17.6 billion), making it the private company with the largest bitcoin holdings. A financial report published on its official website shows that as of 2021, Bullish had total assets of approximately $5.85 billion, with net assets as high as $4.69 billion, indicating a solid financial condition.

Crypto Heading for IPO, Is Wall Street the Next Stop?

Since Circle's successful listing in 2025, it has become a trend for crypto companies to line up for IPOs: Gemini plans to conduct an IPO within the next year, and stablecoin issuer Paxos is also rumored to be in talks with investment banks.

The logic behind this is a collective narrative shift: from "disrupting finance" to "entering finance."

In the past, crypto projects loved to talk about "decentralized utopias"; now, they speak of a "compliant, controllable, and sustainable" digital financial system. They are no longer relying solely on quick money from volatility but are striving for trust through revenue, user stickiness, and infrastructure development.

In this wave, Bullish's role is quite symbolic:

It is an experimental product of Block.one attempting to "cleanse" its old capital path;

It is a renewed departure towards institutions after the EOS community "cut ties";

It is an active effort by the crypto industry to align with the mainstream, also trying to become a role that can be accepted by the mainstream.

In a sense, it may not be the endpoint of the crypto world, but it is likely a "relay station" connecting the two worlds.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。